Mozambique

Mozambique

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This page explores the current and projected future development of Mozambique, examining various sectoral scenarios and their potential impacts on the country's growth. It explores eight sectors including demographic, economic, and infrastructure-related outcomes for Mozambique up to 2043. The analysis also considers the implications of the Agenda 2063 goals, aiming to offer insights into policy actions that could enhance the country's developmental trajectory.

For more information about the International Futures modelling platform we use to develop the various scenarios, please see About this Site.

Executive Summary

We begin this page with an introductory assessment of the country’s context by looking at current population distribution, social structure, climate and topography.

Mozambique, located in Southern Africa and bordered by six countries, is endowed with abundant natural resources, including mineral reserves, fertile agricultural land and an extensive coastline. Following independence in 1975 and the end of a 15-year civil war in 1992, the country entered a period of socio-economic recovery and growth. Between 1993 and 2015, Mozambique was among Africa’s fastest-growing economies, achieving an average annual growth rate of about 8%. This growth was largely driven by political and macroeconomic stability, post-war reconstruction, a rebound in economic activity and increased foreign direct investment (FDI), particularly in extractive industries.

However, these high growth rates were not inclusive enough and not accompanied by a structural transformation of the economy. Mozambique remains one of the world’s poorest countries, with a GDP per capita of approximately US$1 495 in 2024, alongside persistently high levels of poverty and inequality. Since 2015, economic growth has slowed significantly, averaging around 2.9%, due to a combination of challenges including the “hidden debt” crisis, ongoing insurgencies, recurrent natural disasters and the COVID-19 pandemic. As a result, the Government of Mozambique faces the pressing challenge of fostering sustainable and inclusive growth, with significant expectations placed on the potential of large-scale gas projects.

This section is followed by an analysis of the Current Path for Mozambique, which informs the country’s likely current development trajectory to 2043. It is based on current geopolitical trends and assumes that no major shocks would occur in a ‘business-as-usual’ future.

- Since the end of the civil war in 1992, Mozambique’s population has grown steadily at an average annual rate of about 3% between 1993 and 2024. This makes it the third-largest population in Southern Africa, after South Africa and Angola. Under the Current Path scenario, the population is projected to reach 55.4 million by 2043, driven by declining mortality rates and persistently high fertility.

- Agriculture, mining and energy form the foundation of Mozambique's modest economy. On the Current Path, the economy is projected to grow at an average annual rate of 6.1% between 2026 and 2043. As a result of these expected positive growth rates, Mozambique's GDP (2021 constant US$) will nearly triple from US$19.2 billion in 2026 to US$53.5 billion in 2043.

- In 2024, Mozambique had the sixth-lowest GDP per capita (PPP) in Africa, ranking only above South Sudan, Somalia, the Central African Republic, Eritrea and Burundi. On the Current Path scenario, real GDP per capita (in 2021 PPP terms) is projected to increase by about 57%, rising from US$1,472 in 2026 to US$2,311 by 2043. Despite this improvement, it will remain significantly below the projected average of US$4,780 for low-income countries in Africa.

- Using the US$3 per day poverty threshold, Mozambique had the third-highest poverty rate in Africa in 2023, at 81%, behind only South Sudan and the Democratic Republic of the Congo. On the Current Path, the poverty rate is projected to decline to 65.1% by 2043. However, this will still be about 31.4 percentage points higher than the projected average of 33.7% for low-income African countries in the same year.

- Mozambique’s National Development Plan (ENDE) is structured around five main pillars: (i) Structural Transformation of the Economy; (ii) Social and Demographic Transformation; (iii) Infrastructures; (iv) Governance; and (v) Environment and Circular Economy. Each pillar has strategic objectives, result indicators and targets for the period 2023-2043.

The next section compares progress on the Current Path with eight sectoral scenarios. These are Demographics and Health; Agriculture; Education; Manufacturing; the African Continental Free Trade Area (AfCFTA); Large Infrastructure and Leapfrogging; Financial Flows; and Governance. Each scenario is benchmarked to present an ambitious but reasonable aspiration in that sector.

- Under the Demographics and Health scenario, Mozambique accelerates its demographic transition and could begin to reap the demographic dividend by 2047—seven years earlier than under the Current Path. By 2043, GDP per capita (PPP) is projected to be about US$65 higher than in the Current Path scenario. In addition, an estimated 1.7 million fewer Mozambicans would be living in extreme poverty (below US$3 per day), corresponding to a poverty rate of 63.9%, compared to 65.1% under the Current Path in the same year.

- Agriculture is a key source of livelihood for millions of Mozambicans, yet the sector faces persistent challenges that constrain productivity. Under the Agriculture scenario, average crop yields are projected to reach 6.5 tons per hectare by 2043, aligning with the regional average. This improvement translates into stronger development outcomes: the poverty rate (at US$3 per day) is expected to be 4.4 percentage points lower than under the Current Path, while GDP per capita (PPP) will be US$228 higher by 2043.

- Under the Education scenario, average educational attainment among young adults (aged 15–24) is projected to reach 10.8 years by 2043. The scenario also improves primary school outcomes, with the completion rate rising to 63.5%, compared to 60.6% under the Current Path. These gains translate into modest economic benefits, with GDP per capita (PPP) projected to be about US$40 higher by 2043. Improved education outcomes also contribute to poverty reduction: by 2043, approximately 912 720 fewer Mozambicans are expected to live in extreme poverty (below US$3 per day), lowering the poverty rate to 63.6%, compared to 65.1% under the Current Path.

- Under the Manufacturing scenario, the sector’s value added is projected to be one percentage point higher as a share of GDP than under the Current Path by 2043. This expansion translates into improved livelihoods, with average income per capita (PPP) rising by about US$117 above the Current Path. It also has a significant impact on poverty reduction, with nearly 2.2 million fewer Mozambicans expected to be living in extreme poverty in 2043 compared to the Current Path.

- Under the African Continental Free Trade Area (AfCFTA) scenario, Mozambique’s trade deficit is projected to widen slightly, reaching about 25.6% of GDP by 2043—approximately 2 percentage points higher than under the Current Path. Despite this, the scenario yields notable welfare gains: GDP per capita (PPP) is projected to be US$131 higher, while the poverty rate declines by 3.4 percentage points. This translates to around 2 million fewer people living in extreme poverty in 2043 compared to the Current Path.

- Under the Large Infrastructure and Leapfrogging scenario, GDP per capita (PPP) is projected to be US$256 higher than under the Current Path by 2043. This improvement is accompanied by a reduction in poverty, with approximately 1.4 million fewer Mozambicans living in extreme poverty compared to the Current Path. As a result, the poverty rate declines to 62.8%, compared to 65.1% under the Current Path.

- Under the Financial Flows scenario, average income per capita (PPP) in Mozambique is projected to be US$128 higher than under the Current Path by 2043. This is accompanied by a reduction in poverty, with the poverty rate declining by 1.2 percentage points, equivalent to about 725 830 fewer people living in extreme poverty, compared to the Current Path.

- Under the Governance scenario, GDP per capita (PPP) is projected to be US$131 higher than the Current Path, reaching above the baseline of US$2 311 by 2043. This improvement is accompanied by substantial poverty reduction, with nearly 2.5 million fewer Mozambicans expected to live on less than US$3 per day compared to the Current Path projection of 37.5 million people in the same year. As a result, the poverty rate declines to 60.8%, compared to 65.1% under the Current Path by 2043.

In the fourth section, we compare the impact of each of these eight sectoral scenarios with one another and subsequently with a Combined scenario (the integrated effect of all eight scenarios). In our forecasts, we measure progress on various dimensions such as economic size (in market exchange rates), gross domestic product per capita (in purchasing power parity), extreme poverty, carbon emissions, the changes in the structure of the economy, and selected sectoral dimensions such as progress with mean years of education, life expectancy, the Gini coefficient or reductions in mortality rates.

The Combined scenario forecasts:

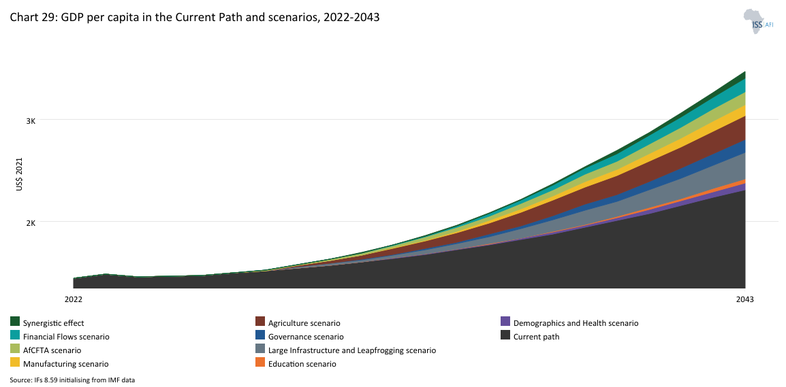

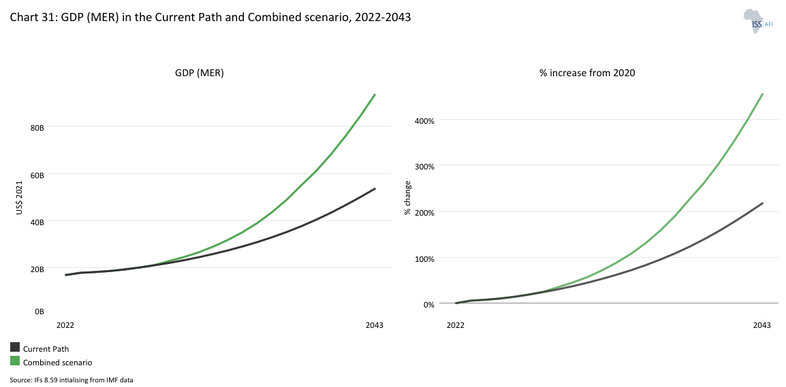

- Mozambique could expect a significant improvement in its human and economic development prospects. Under this scenario, the average annual growth rate between 2023 and 2043 will be about 8.5%. The size of the Mozambican economy measured in GDP at the market exchange rate (MER) will be US$40 billion larger than the Current Path in 2043

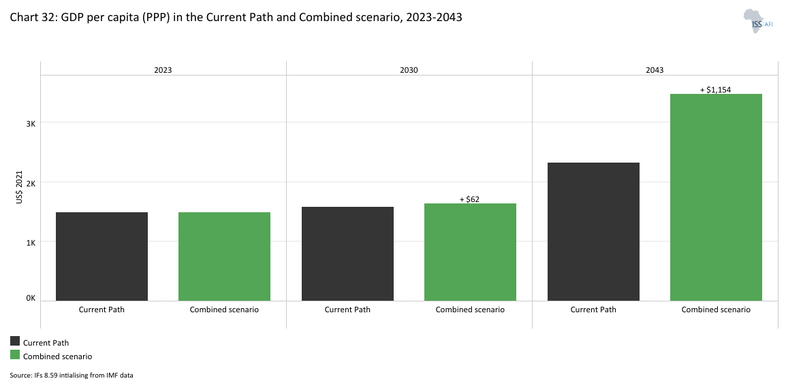

- GDP per capita (PPP) will reach US$3 465 by 2043, an increase of US$1 154 compared to the Current Path (Chart 48). All the sectoral scenarios improve the GDP per capita, however, the Large Infrastructure and Leapfrogging scenario has the most significant positive impact on GDP per capita with an increase of US$148 above the Current Path in 2043.

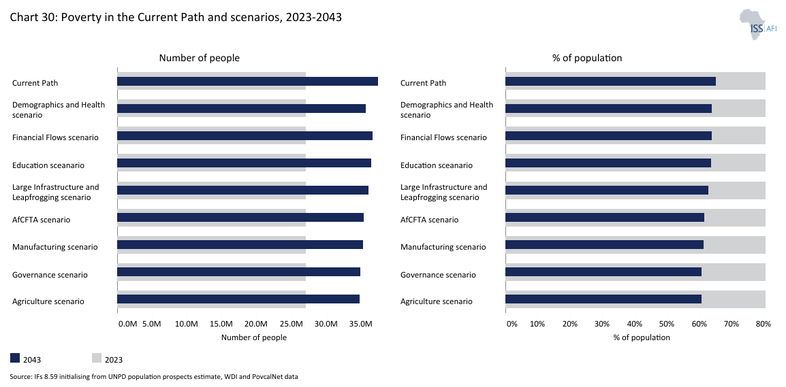

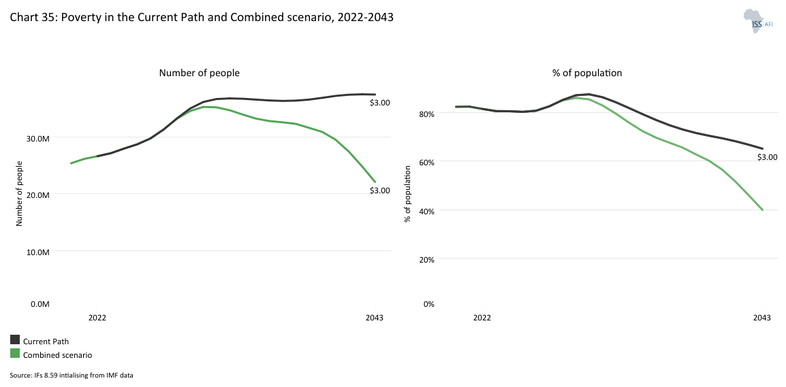

- The poverty rate (measured at US$3 per day) is projected to decline to 40% by 2043, compared to 65.1% under the Current Path in the same year. This would translate into around 15.4 million fewer Mozambicans living in extreme poverty by 2043 under the Combined scenario. All the sectoral scenarios contribute to poverty reduction in Mozambique; however, in the short to medium term, short to medium term, agriculture is projected to have the largest impact on GDP growth and poverty reduction. The AfCFTA scenario also emerges as the most effective in reducing poverty among the sectoral interventions in the short to medium term.

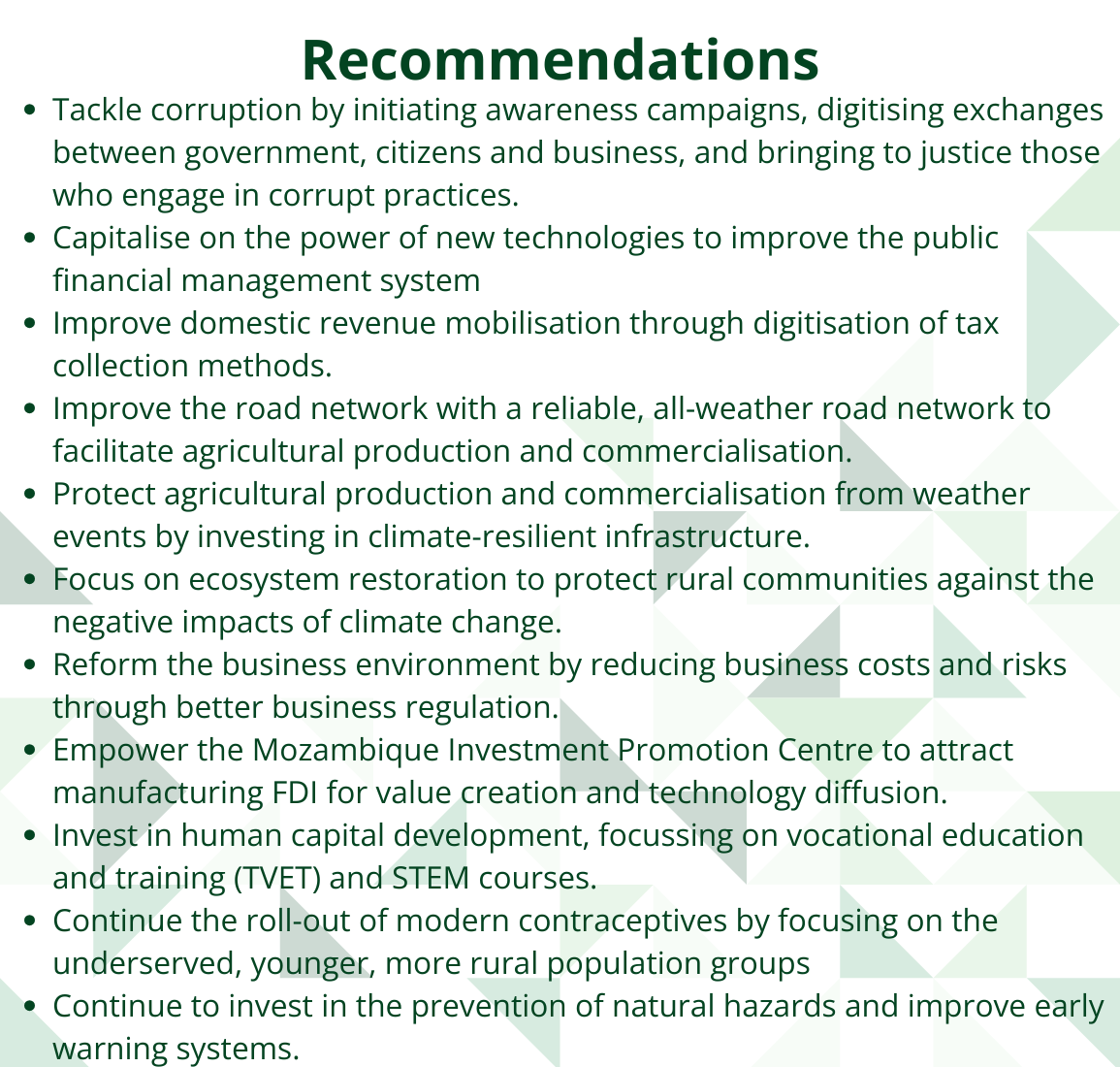

We end this page with a summarising conclusion offering key recommendations for decision-making. The analysis highlights that Mozambique faces a range of significant development challenges that continue to constrain progress, including weak governance, corruption, a slow demographic transition, infrastructure and human capital deficits, low agricultural productivity and limited economic diversification. Despite the anticipated revenues from gas megaprojects, the number of people living in extreme poverty is likely to remain higher by 2043, underscoring the limitations of the Current Path. This suggests that a business-as-usual trajectory is insufficient to achieve meaningful development outcomes. Addressing these challenges will require a coordinated and integrated push across key sectors. Ultimately, progress will hinge on the quality of governance and institutions, as weak governance contributes to public financial mismanagement, macroeconomic instability and ineffective policy implementation.

All charts for Mozambique Development Futures

- Chart 1: Political map of Mozambique

- Chart 2: Population structure in the Current Path, 1990–2043

- Chart 3: Population distribution map, 2023

- Chart 4: Urban and rural population in the Current Path, 1990-2043

- Chart 5: GDP (MER) and growth rate in the Current Path, 1990–2043

- Chart 6: Size of the informal economy in the Current Path, 2020-2043

- Chart 7: GDP per capita in Current Path, 1990–2043

- Chart 8: Extreme poverty in the Current Path, 2020–2043

- Chart 9: National Development Plan of Mozambique

- Chart 10: Relationship between Current Path and scenarios

- Chart 11: Mortality distribution in the Current Path, 2023 and 2043

- Chart 12: Infant mortality rate in Current Path and Demographics and Health scenario, 2020–2043

- Chart 13: Demographic dividend in the Current Path and the Demographics and Health scenario, 2020–2043

- Chart 14: Crop production and demand in the Current Path, 1990-2043

- Chart 15: Import dependence in the Current Path and Agriculture scenario, 2020–2043

- Chart 16: Progress through the education funnel in the Current Path, 2023 and 2043

- Chart 17: Mean years of education in the Current Path and Education scenario, 2020–2043

- Chart 18: Value-add by sector as % of GDP in the Current Path, 2022 and 2043

- Chart 19: Value-add by the manufacturing sector in the Current Path and Manufacturing scenario, 2022–2043

- Chart 20: Exports and imports as % of GDP in the Current Path, 2000-2043

- Chart 21: Trade balance in the Current Path and AfCFTA scenario, 2020–2043

- Chart 22: Electricity access: urban, rural and total in the Current Path, 2000-2043

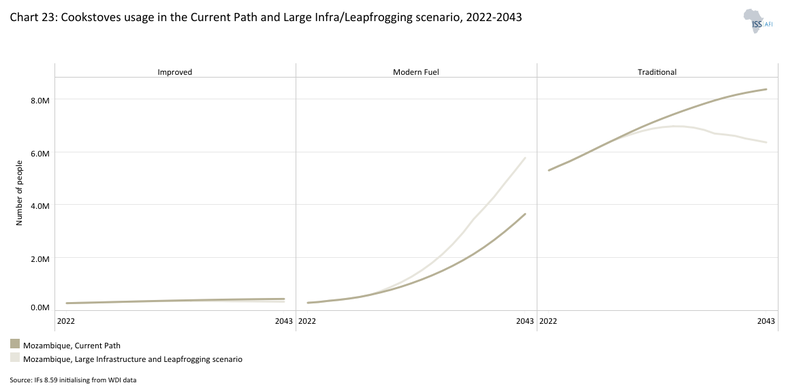

- Chart 23: Cookstove usage in the Current Path and Large Infra/Leapfrogging scenario, 2020–2043

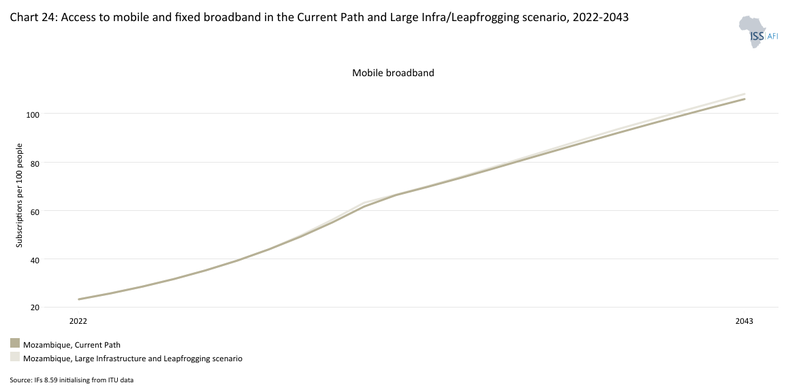

- Chart 24: Access to mobile and fixed broadband in the Current Path and the Large Infra/Leapfrogging scenario, 2020–2043

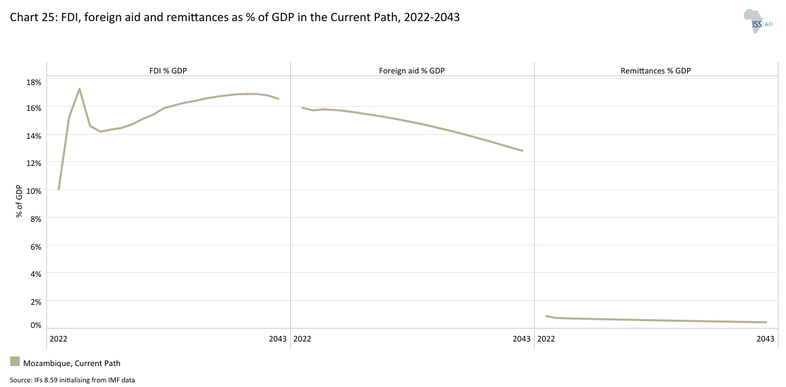

- Chart 25: FDI, foreign aid and remittances as % of GDP in the Current Path and in the Financial Flows scenario, 1990-2043

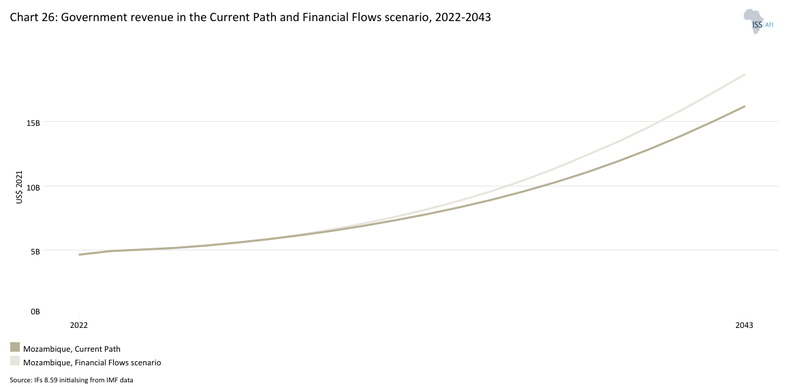

- Chart 26: Government revenue in the Current Path and Financial Flows scenario, 2020–2043

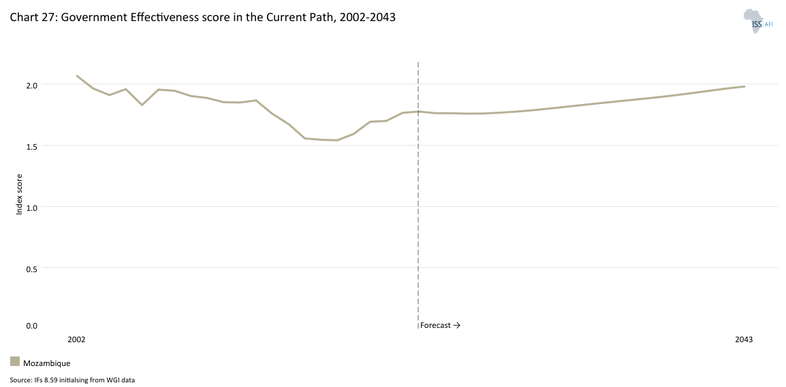

- Chart 27: Government effectiveness score in the Current Path, 2002-2043

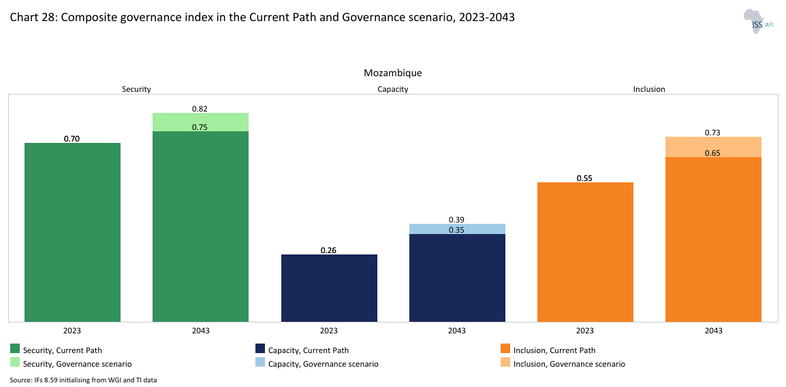

- Chart 28: Composite governance index in the Current Path and Governance scenario, 2023 and 2043

- Chart 29: GDP per capita in the Current Path and scenarios, 2020–2043

- Chart 30: Poverty in the Current Path and scenarios, 2020–2043

- Chart 31: GDP (MER) in the Current Path and Combined scenario, 2020–2043

- Chart 32: GDP per capita in the Current Path and Combined scenario, 2023-2043

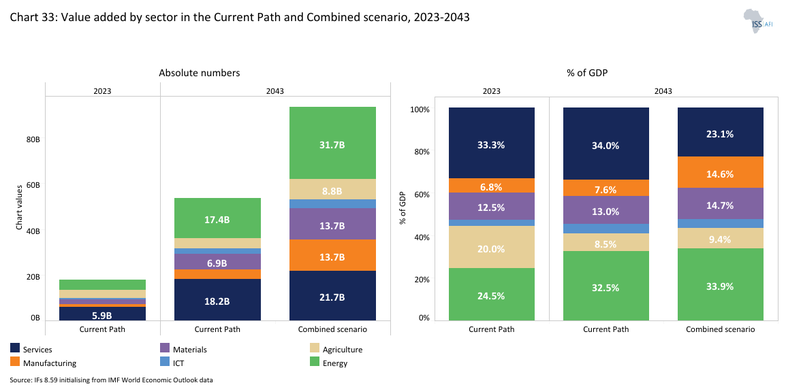

- Chart 33: Value-add by sector in the Current Path and Combined scenario, 2023 and 2043

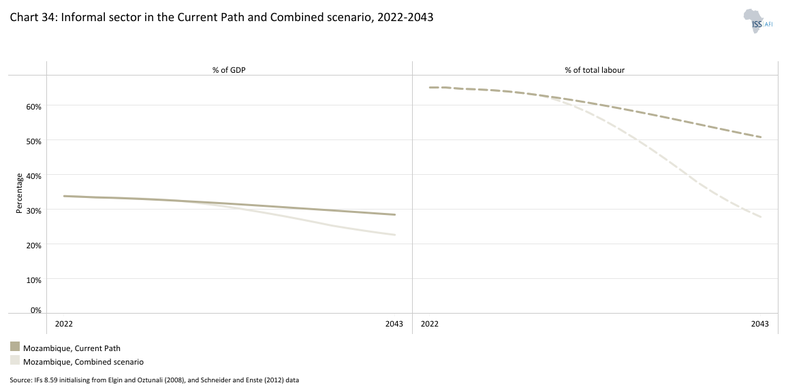

- Chart 34: Informal sector in the Current Path and Combined scenario, 2020–2043

- Chart 35: Poverty in the Current Path and Combined scenario, 2023 and 2043

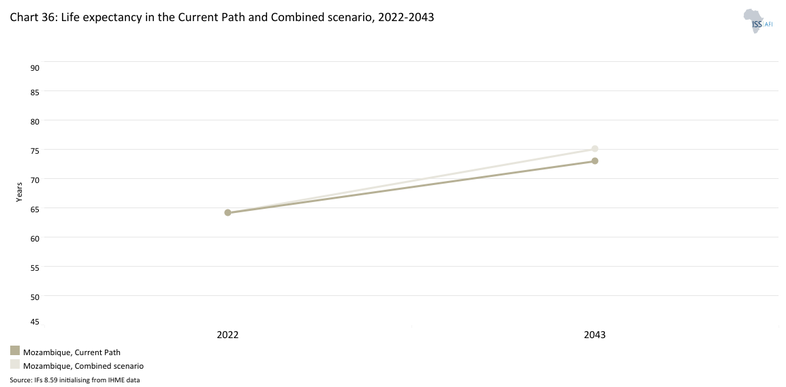

- Chart 36: Life expectancy in the Current Path and Combined scenario, 2020–2043

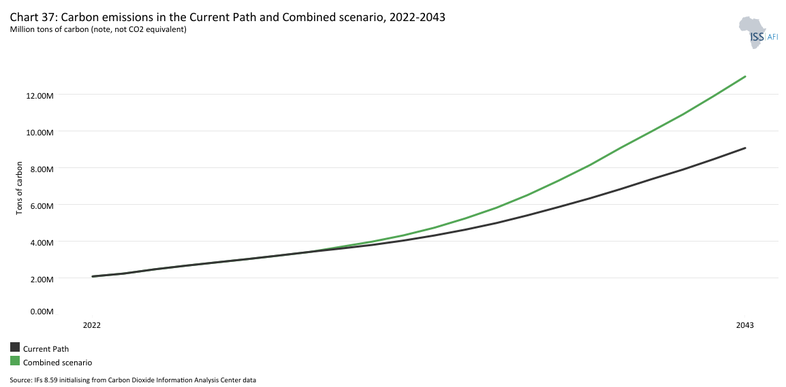

- Chart 37: Carbon emissions in the Current Path and Combined scenario, 2020–2043

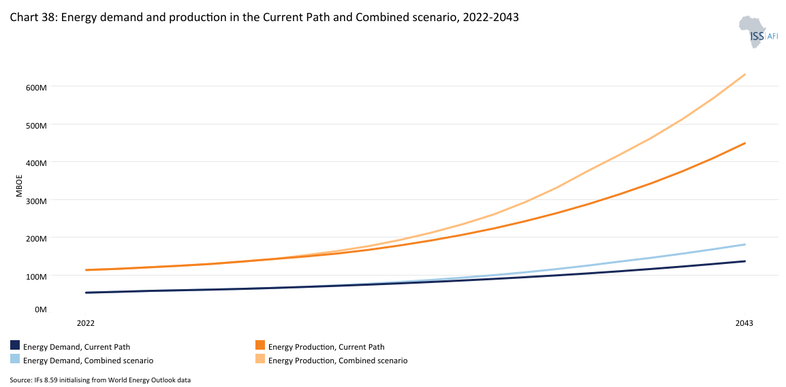

- Chart 38: Energy demand and production by type in the Current Path and Combined scenario, 2020-2043

- Chart 39: Policy recommendations

Chart 1 is a political map of Mozambique.

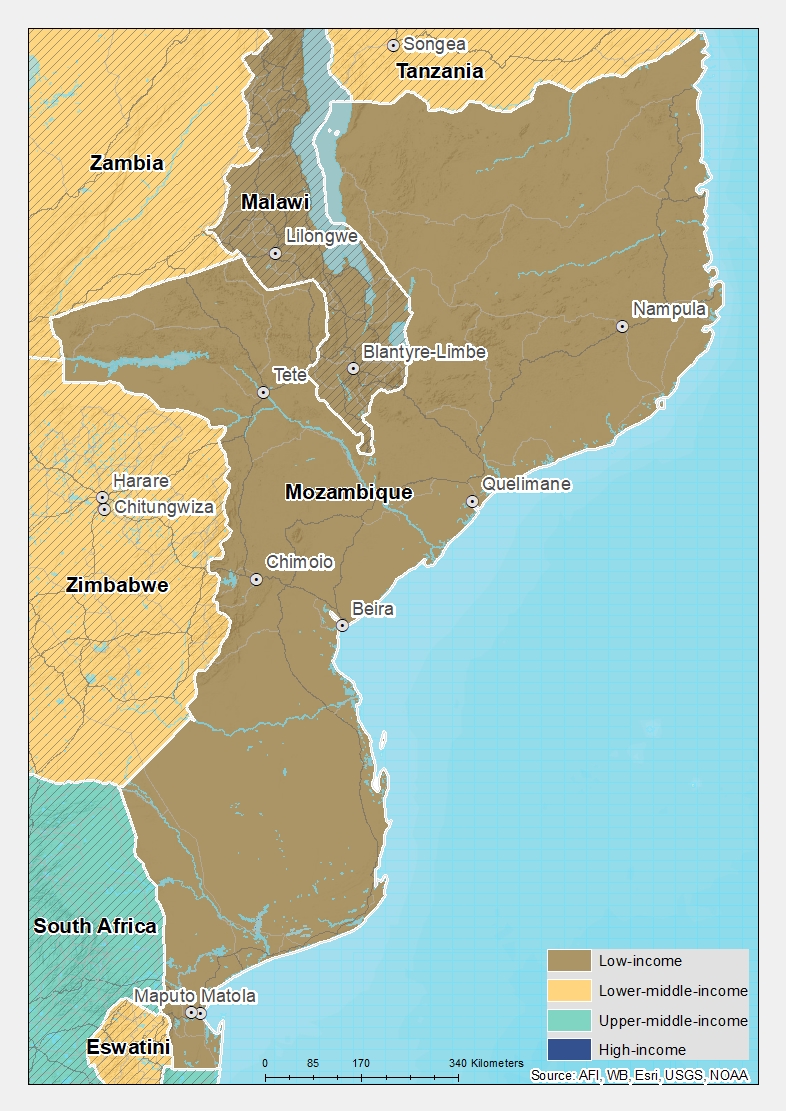

Located in Southern Africa, Mozambique shares borders with Tanzania, Malawi, Zambia, Zimbabwe, South Africa and Eswatini, and stretches along a long coastline on the Indian Ocean. Classified as a low-income country, it had an estimated population of approximately 34.7 million in 2024, reflecting steady demographic growth averaging around 3%. This is slightly above the average GDP growth between 2016 and 2024. The country is endowed with significant mineral reserves, extensive tracts of arable land and abundant marine resources. Its coastline is influenced by the warm Mozambique current, which supports rich marine biodiversity and underpins important fisheries and coastal livelihoods.

Mozambique gained independence in 1975, but it was only after the end of a 15-year civil war in 1992 that the country began to experience sustained socio-economic recovery. From 1993 to 2015, Mozambique ranked among Africa’s fastest-growing economies, recording average annual growth of around 8%. This strong performance was driven by a combination of relative political and macroeconomic stability, the rebound of economic activity following the war, substantial post-war reconstruction efforts and rising foreign direct investment, particularly in large-scale extractive industry projects. During this period, Mozambique recorded notable social gains. Maternal and child mortality rates declined significantly, and access to basic education expanded for both girls and boys. Access to essential services also improved: electricity coverage increased from just 3.7% of the population in 1998 to roughly 36% by 2023, reflecting sustained investment in energy infrastructure. Public health outcomes have also strengthened. Over the past decade, new HIV infections have declined by approximately 34% and AIDS-related deaths by 27%. Together, these improvements have translated into longer lives for many Mozambicans. Life expectancy increased from approximately 53 years in the early 1990s to around 64 years by the early 2020s, reflecting cumulative gains in healthcare, nutrition and access to basic services.

Despite these gains, Mozambique's economy did not undergo a meaningful structural transformation. Growth was largely driven by capital-intensive extractive industries, which have generated limited backward and forward linkages with the broader economy. As a result, the productive base remains narrow, with few spillovers into manufacturing and other value-adding sectors. At the same time, agriculture, which employs the majority of the population, continues to be characterised by low productivity and limited modernisation, leaving livelihoods highly vulnerable to weather shocks and the growing impacts of climate change.

Efforts to diversify the economy and improve the quality and inclusiveness of growth have been constrained by persistent structural bottlenecks. These include inadequate infrastructure, particularly in energy, transport and logistics; weak and inconsistent policy implementation; governance challenges such as corruption; and an unfavourable business environment that discourages private investment and innovation. Together, these factors have weakened economic resilience and slowed progress towards broader, more sustainable development.

Mozambique remains one of the poorest countries globally, with GDP per capita estimated at US$1 495 (PPP) (or about US$529 at market exchange rates (MER)) in 2024, only ahead of South Sudan, Somalia, the Central African Republic, Eritrea and Burundi. Poverty levels remain exceptionally high. In 2023, about 81% of Mozambicans lived below the international extreme poverty line of US$3 per day, the third highest after South Sudan and the Democratic Republic of Congo.

Inequality is also pronounced, placing Mozambique among the most unequal countries in sub-Saharan Africa. According to the 2024 Global Inequality data published by the World Inequality Lab, the top 10% of the Mozambican population captures approximately 72% of the country’s wealth. In contrast, the bottom 50% of the population captures only around 2% of Mozambique’s national income. In the 2025 Human Development Index (HDI) rankings, Mozambique is classified as a low human development country, with an HDI score of approximately 0.49 and a global ranking of 182nd out of 191, well below many of its regional peers. These indicators underscore the scale of the structural and institutional challenges the country must address to achieve inclusive and sustainable development.

The post-2015 economic growth has been slow, averaging about 2.9% between 2016 and 2024. This slowdown followed the ‘hidden debt’ scandal and was compounded by a series of shocks, including the insurgency in northern Mozambique, recurring tropical cyclones and the COVID-19 pandemic. Over this period, unemployment, poverty and inequality have all worsened.

The government now faces a pressing challenge: how to secure long-term, stable and inclusive growth that delivers sustained reductions in income inequality and extreme poverty. There are high expectations that the gas megaprojects in the northern provinces will transform the country’s economic trajectory and unlock a new phase of development. However, experiences across Africa show that natural resource extraction has rarely fulfilled such ambitions and, in some cases, has exacerbated economic distortions and governance challenges. Turning resource-driven growth and revenues into meaningful, inclusive development outcomes will require deliberate, strategic action. This entails visionary leadership and development-oriented governance capable of managing resource revenues transparently and prudently, while investing them into economic diversification, human capital and resilient infrastructure.

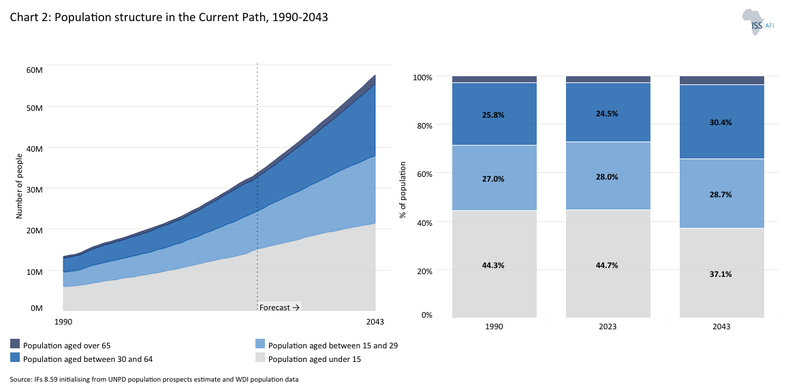

Chart 2 presents the Current Path of the population structure, from 1990 to 2043.

The structure of a country’s population shapes its long-term social, economic and political trajectory. Thus, an understanding of a country’s demographic profile is important for assessing development prospects. Since the end of the civil war in 1992, Mozambique’s population has grown rapidly, increasing from about 13.6 million in 1992 to approximately 34.7 million in 2024—an average annual growth rate of around 3% between 1993 and 2024. As a result, Mozambique is ranked the 13th most populous country in Africa and the third-largest in Southern Africa, after South Africa and Angola.

On the Current Path, Mozambique’s population will reach about 55.4 million by 2043, driven by declining mortality and persistently high fertility. Between 2023 and 2043, the population will grow at an average annual rate of 2.7%, significantly above the 1.8% target set in the National Development Strategy (ENDE) for the same period. By 2043, annual population growth will remain high at 2.3%, well above the ENDE target of 1.3% for that year.

Mozambique’s total fertility rate peaked in 1972 at about 6.7 births per woman. Fertility remained persistently high over the following decades, averaging about 6.4 births per woman between 1972 and 1999. This was a result of limited access to family planning services, high levels of child mortality and a predominantly rural population where larger families were often viewed as economically and socially beneficial.

Since the early 2000s, fertility has gradually declined as child and youth mortality fell and access to education, particularly for girls, improved, alongside expanded access to reproductive health and family planning services. By 2024, Mozambique’s fertility rate had declined to about 4.7 births per woman. Despite this progress, fertility remains well above the replacement level of 2.1 births per woman. The country’s fertility rate is forecast to remain above the replacement rate by 2043, when it is forecast to reach 3.3 births per woman.

According to the Demographic and Health Survey (DHS) 2022/2023, 26% of currently married women ages 15–49 and 47% of unmarried women sexually active use some method of family planning. And the fertility rate is not homogeneous across the country. On average, women in rural areas have 5.8 children compared with 3.6 children in urban areas. The percentage of modern methods of contraception used among currently married women aged 15–49 is higher in urban areas (40%) compared to rural areas (18%). In relation to the provinces, Zambézia (11%), Nampula (13%) and Cabo Delgado (14%) have the lowest percentage of currently married women using some modern methods.

The GoM has reiterated that population growth management is a critical priority to meet the country’s social and economic development goals. This is currently prioritised as a focus area in the ENDE.

Persistently high fertility rates, combined with relatively low life expectancy, have contributed to Mozambique having one of the most youthful age structures in Africa. Mozambique’s median age was estimated at 17.5 years in 2024, the 19th lowest in Africa. This represents a modest increase from 16 years in 1992, at the end of the civil war, indicating a gradual shift in the country’s age structure. On the Current Path, the median age will reach 21.1 years by 2043, meaning that half of the population will still be younger than 21. This gradual ageing is reflected in a declining share of the population under 15 and a corresponding increase in the working-age population.

In 2024, about 44.4% of the Mozambican population was under 15 years old. This large cohort of children below 15 years of age requires a huge investment in education and healthcare infrastructure. With an expected drop in fertility rates by 2043, 37.1% of the population will be under 15 years of age. The increase in life expectancy is evident in the growing elderly-dependent population group, which will rise from 2.9% in 2024 to 3.8% by 2043.

The working-age population cohort (15-64 years) will increase from 52.7% in 2024 to 59.1% by 2043. Properly educated and skilled, this growing workforce can contribute to innovation, entrepreneurship and economic diversification, allowing Mozambique to enter a potential demographic window of opportunity by 2054. The demographic dividend, or demographic gift, is the economic growth generated by changes in a country’s demographic structure. It generally materialises when a country reaches a ratio of at least 1.7 people of working age (15–64 years of age) for each dependant (children (0–14 years) and elderly people (65+ years). The ratio was 1.1 in 2024 and will be 1.4 by 2043 and 1.7 in 2054.

When there are fewer dependants to care for, it frees up resources for savings and investment and eventually allows women, in particular, to pursue careers, skills and training. It increases female labour force participation in ways they would otherwise not be able to realise if they are caring for large families.

Studies have shown that about one-third of economic growth during the East Asian economic miracle can be attributed to the large worker bulge and the relatively small number of dependants. However, the growth in the working-age population relative to dependents does not automatically translate into rapid economic growth unless the labour force acquires the needed skills and is absorbed by the labour market. In 2024, about 79% of the population aged 15 and above was economically active, reflecting the large share of workers engaged in subsistence agriculture and informal activities.

Mozambique has a large youth bulge at 50.4% in 2024, which, on the Current Path, will decline to 45.6% by 2043. A youth bulge, defined as the percentage of the population aged 15 to 29 relative to the population aged 15 and above, exhibits a strong relationship with upsurges in violence and socio-political instability in poor countries, particularly when opportunities are scarce, education quality is low and democratic expression is inhibited.

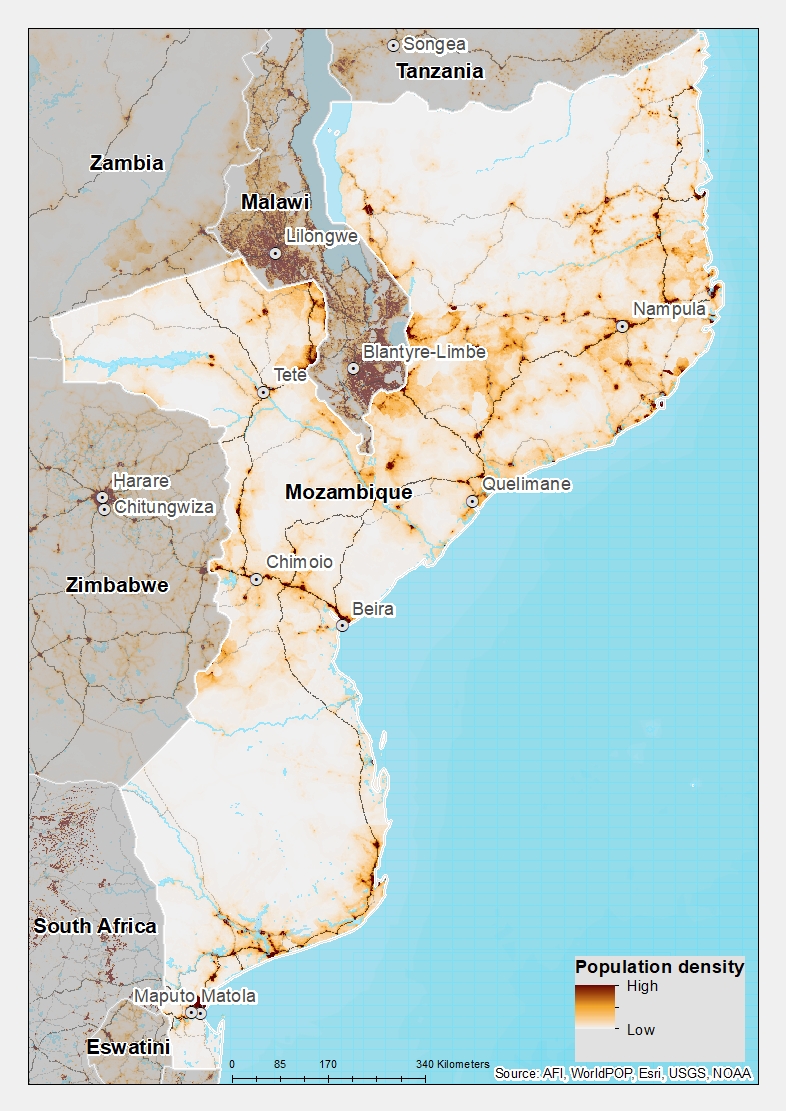

Chart 3 presents a population distribution map for 2023.

Mozambique is a sparsely populated country. In 2023, its population density was around 43 people per square kilometre. Three large population clusters are found along the southern coast between Maputo and Inhambane, in the central area between Beira and Chimoio along the Zambezi River, and in and around the northern cities of Nampula, Cidade de Nacala, and Pemba; the northwest and southwest are the least populated areas.

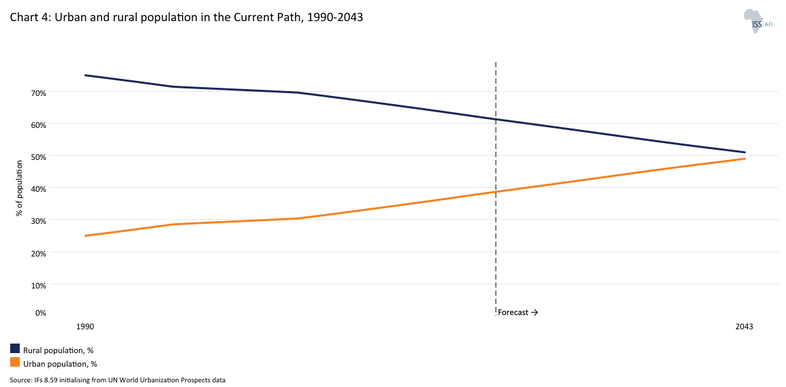

Chart 4 presents the urban and rural population in the Current Path, from 1990 to 2043.

Together with population growth and structural demographic changes, Mozambique is expected to see a dramatic shift towards urban areas. Mozambique is one of the least urbanised countries in the world, with 60.7% of its population dwelling in rural areas as of 2024.

On the Current Path, the urban transition will gain momentum, with 49% of the population in urban areas and 51% in rural areas in 2043. Urbanisation is critical to economic growth and development as it fosters entrepreneurship and increases productivity. Cities in Africa generate between 55% and 60% of the continent’s GDP.

Despite constituting only about 5% of the country’s population, Maputo is responsible for about 20% of Mozambique’s GDP. Urbanisation can reduce poverty and provide several social and economic benefits when managed sustainably.

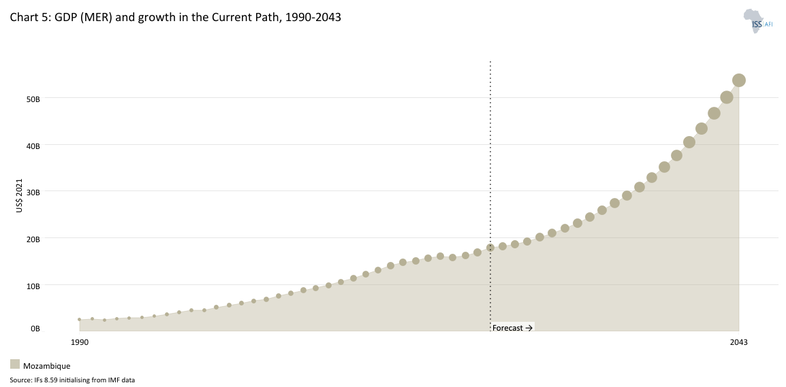

Chart 5 presents GDP in market exchange rates (MER) and growth rate in the Current Path, from 1990 to 2043.

Agriculture, mining and energy remain central to Mozambique’s economy, but its growth trajectory has been uneven in recent years. Following sustained high growth from the early 1990s through the mid-2010s, Mozambique frequently ranked among the world’s fastest-growing economies. However, the 2016 “hidden debt” crisis, triggered by the revelation of previously undisclosed government loans, abruptly derailed this momentum, leading to a sovereign debt distress classification and credit downgrades that undermined economic confidence and access to international finance. The economic slowdown that followed saw growth fall sharply from around 7.4% in 2015 to a negative 1.2% by 2020, as fiscal pressures, governance weaknesses and external shocks mounted. Severe natural disasters exacerbated the situation, the impact of the COVID-19 pandemic, and an insurgency in northern Mozambique that disrupted local economies and delayed major investments.

The 2024 general election introduced fresh political and economic stress. President Daniel Chapo and the ruling FRELIMO party were declared winners. Still, opposition disputes and the resulting unrest contributed to a contraction in economic activity in the fourth quarter of 2024, with data showing a significant decline in growth from 5.4% in 2023 to around 1.9% by 2024. Cyclones disrupted agricultural production, while weaker performance in the extractive sector further weighed on overall economic activity.

Mozambique’s growth outlook is cautiously optimistic, largely underpinned by the anticipated expansion of liquefied natural gas (LNG) production and the associated fiscal revenues accruing to the Government of Mozambique (GoM). The gradual resumption and scaling up of major LNG projects are expected to provide a significant boost to GDP growth, strengthen export earnings, and improve the external balance.

Given delays in LNG extraction, the full growth dividends from megaprojects are likely to materialise beyond the forecast horizon (2043). Under the Current Path, average annual GDP growth is projected at around 5.1% between 2026 and 2034, accelerating to about 7.1% over 2035–2043 as LNG extraction scales up. Over the entire 2026–2043 period, growth is expected to average 6.1%, which is 3.1 percentage points below the GoM’s more optimistic projection of 9.2% outlined in the National Development Strategy (2023–2043).

Reflecting these projected growth rates dynamics, Mozambique's GDP (2021 constant US$) will expand significantly over the long term, rising from an estimated US$19.2 billion in 2026 to approximately US$53.5 billion by 2043. This represents more than a doubling of real output over the forecast horizon, driven primarily by the gradual scaling up of LNG production alongside the recovery of agriculture production and a rebound of services, the sector most affected by the post-election disruptions.

However, this outlook remains subject to substantial downside risks. Climate-related shocks continue to threaten agricultural output and infrastructure, while the security situation in the North, although improved relative to previous years, remains fragile and could disrupt investment and production. In addition, persistent macroeconomic vulnerabilities, including high public debt (forecast to reach 102% of GDP by 2027) and fiscal pressures, may constrain the government’s ability to fully leverage resource-driven growth for broader economic stability and inclusive development.

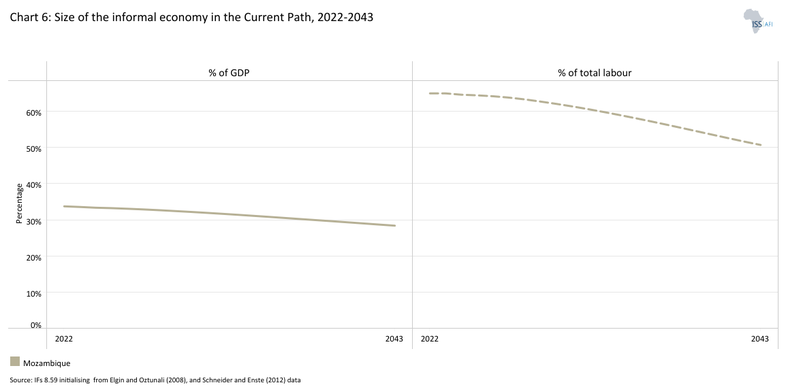

Chart 6 presents the size of the informal economy as per cent of GDP and per cent of total labour (non-agriculture), from 2020 to 2043. The data in our modelling are largely estimates and therefore may differ from other sources.

As in many other low-income countries, the informal economy is very large in Mozambique (Chart 6). In 2021, Mozambique had around a 96% informality rate among its workforce. Countries with high informality face a range of development challenges, such as low revenue mobilisation. Economic growth tends to be below potential in countries with high levels of informality. A study conducted in Mozambique shows that compared to formal micro enterprises, informal firms sell about 14 times less, make 17 times lower profits and are 2-3 times less productive.

In 2024, Mozambique’s informal sector was estimated at 33.4% of GDP, highlighting the structural nature of informality within the economy and its close link to limited formal job creation. On the Current Path, informality will decline gradually to 28.4% of GDP by 2043. While this represents modest progress, it signals a slow pace of structural transformation. By 2043, Mozambique would sit slightly below the average for African low-income countries (28.9%) but remain well above the Southern African average (18.5%), suggesting that deeper reforms in productivity, private-sector development and labour absorption will be required to accelerate formalisation and broaden the tax base.

Our fieldwork findings point to persistent structural barriers to formalisation. Lengthy registration processes, high fees, cumbersome administrative requirements and limited access to information and compliance training remain key constraints for informal enterprises. Interviews further revealed inconsistencies in the implementation of regulations, with some officials requesting unnecessary documentation due to limited familiarity with existing procedures—practices that increase transaction costs and discourage transition into the formal economy.

Given that the informal sector currently serves as a critical livelihood source for Mozambique’s rapidly growing youth population, formalisation efforts will need to be gradual and sequenced. Abrupt enforcement measures could undermine incomes in the absence of sufficient formal employment opportunities. A more sustainable pathway would combine regulatory simplification with clear incentives for formalisation. This includes improving access to finance, business development services, skills training and market linkages with larger formal firms. Strengthening the capacity of public officials responsible for business registration, alongside improvements in transparency and the standardisation of procedures, will also be essential to reduce uncertainty and build trust in the formal system.

Without such reforms, the pace of formalisation is likely to remain slow, limiting domestic revenue mobilisation and constraining inclusive economic transformation over the forecast horizon.

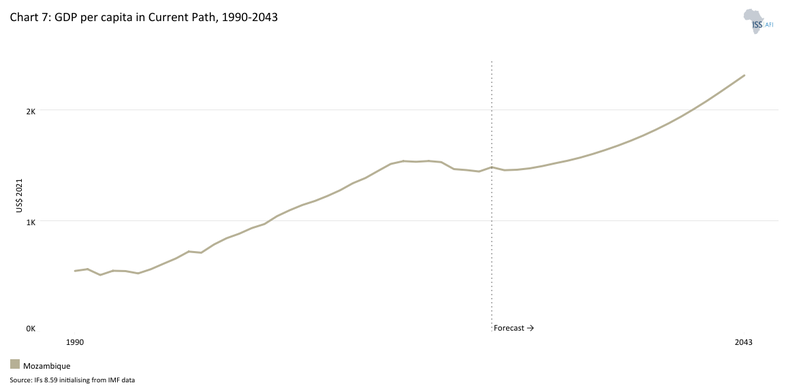

Chart 7 presents GDP per capita in the Current Path, from 1990 to 2043, compared with the average for the Africa income group.

According to the World Bank’s income classification, Mozambique has consistently remained in the low-income category and has not yet transitioned to lower-middle-income status. In 2024, Mozambique ranked among the six lowest countries in Africa in terms of GDP per capita (2021 PPP), underscoring the persistent income and development challenges facing the economy despite periods of relatively strong aggregate growth. As illustrated in Chart 7, the country made substantial progress in narrowing the gap between its GDP per capita and the average of its African income peers between 1995 and 2015, reflecting the strong growth performance during that period. However, this convergence has since reversed. Weaker economic growth after 2015, coupled with persistently high population growth, has led to a renewed widening of the income gap.

On the Current Path, Mozambique is unlikely to converge toward the average income level of its peer group. GDP per capita will increase by approximately 56.9%, rising from an estimated US$1 472 in 2026 to US$2 311 by 2043. Despite this improvement, it would remain well below the projected average of US$4 780 for low-income African countries over the same period. Higher population growth will continue to dilute aggregate economic gains, meaning that even relatively robust GDP growth translates into more modest increases in per capita income.

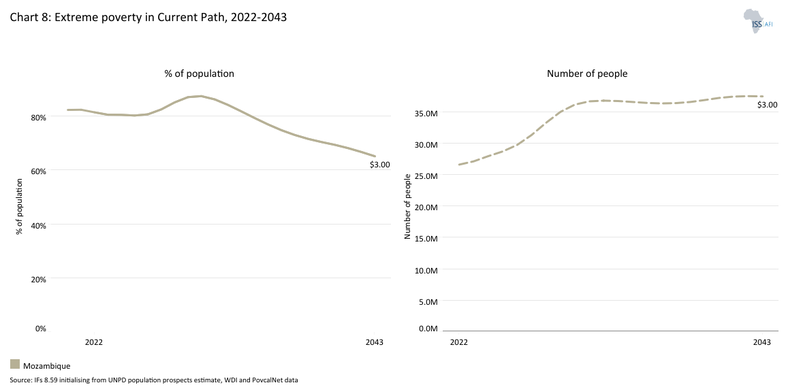

Chart 8 presents the rate and number of poor people in the Current Path from 2020 to 2043.

In 2025, the World Bank updated the poverty lines to 2021 constant dollar values as follows:

- The previous US$2.15 extreme poverty line is now set at US$3, also for use with low-income countries.

- US$3.20 for lower-middle-income countries, now US$3.65 in 2017 values.

- US$5.50 for upper-middle-income countries, now US$6.85 in 2017 values.

Monetary poverty only tells part of the story, however. In addition, the global Multidimensional Poverty Index (MPI) measures acute multidimensional poverty by measuring each person’s overlapping deprivations across 10 indicators in three equally weighted dimensions: health, education and standard of living. The MPI complements the international US$3 a day poverty rate by identifying who is multidimensionally poor and also shows the composition of multidimensional poverty. The headcount or incidence of multidimensional poverty is often several percentage points higher than that of monetary poverty. This implies that individuals living above the monetary poverty line may still suffer deprivations in health, education and/or standard of living.

Poverty in Mozambique disproportionately affects young people, women, individuals with lower education levels, residents of larger rural households and those working in the agricultural sector. Geographically, provinces in the Northern and Central regions of the country are hardest hit by poverty. In contrast, the Maputo Province and Maputo City in the South have the lowest poverty rates, standing at 22.4% and 11.4%, respectively.

Using the US$3 per day (2021 PPP) poverty threshold, Mozambique had the third-highest poverty rate in Africa in 2024, at an estimated 80.5%. Chart 6 shows the past trends in poverty and projections on the Current Path. It indicates that poverty is not a new phenomenon but a long-standing issue in Mozambique. Although the country recorded notable progress between 2002 and 2015, when poverty declined steadily, this trend has since reversed. The poverty rate increased from 74.5% in 2015, effectively eroding much of the gains achieved during the preceding decade.

In absolute terms, the situation is even more concerning. The number of people living in extreme poverty rose from approximately 19.8 million in 2015 to nearly 28 million in 2024, reflecting the combined effects of slow structural transformation, rapid population growth and vulnerability to economic and climate-related shocks.

After 2015, economic instability reversed earlier poverty reduction gains. The hidden debt crisis caused macroeconomic instability, currency depreciation and reduced investor confidence, slowing economic growth. This situation worsened due to external shocks, including Cyclones Idai and Kenneth in 2019, the COVID-19 pandemic and global supply chain disruptions, which increased food and fuel prices. By the end of 2021, before the additional impacts of the Ukraine war and the global cost-of-living crisis, about 81.8% of the population (25.9 million people) were living in extreme poverty. Political uncertainty during election periods also weakened investor confidence, delayed reforms and further limited the government’s ability to implement effective poverty-reduction policies.

Monetary poverty, however, captures only part of the picture. The global Multidimensional Poverty Index (MPI) provides a broader assessment by measuring overlapping deprivations across ten indicators within three equally weighted dimensions: health, education and living standards. The MPI complements the international extreme poverty line of US$3 per day by identifying who is multidimensionally poor and highlighting the different forms of deprivation they experience. According to UNDP estimates, 60.7% of Mozambique’s population was multidimensionally poor in 2022/2023, with a further 16.9% considered vulnerable to falling into multidimensional poverty.

Poverty in Mozambique is projected to decline gradually over the long term, but will remain significantly higher than the peer's average. By 2043, the poverty rate (at US$3 per day) is expected to fall to 65.1%, which is about 31.4 percentage points higher than the projected average of 33.7% for low-income African countries in the same year. Despite this gradual decline in the poverty rate, rapid population growth means the absolute number of people living in poverty will continue to rise. The number of poor people will reach 36.1 million by 2030 and increase further to 37.5 million by 2043.

For economic growth to translate into meaningful poverty reduction, it must be inclusive and generate broad-based benefits for the population. While the resumption of the LNG extraction is expected to create employment opportunities, many of these jobs are likely to be temporary and limited in scale. On the Current Path trajectory, Mozambique will miss the SDG target of eliminating extreme poverty by 2030 by a wide margin.

In the Mozambique National Development Plan (ENDE), the target is to reduce the proportion of the population living below the national poverty line from 68.2% currently to 35.8% by 2043. On the Current Path, Mozambique will struggle to reduce poverty because of its extraordinarily high levels of inequality and unemployment. According to the Global Inequality Update 2024, published by the World Inequality Lab, the top 10% of the Mozambican population capture about 72% of the country's wealth. In contrast, the bottom 50% of the population captured around 2% of Mozambique's national income. The country’s Gini coefficient was estimated at 0.5 in 2024, indicating substantial income and consumption disparities.

While economic growth is necessary for poverty reduction, it is not sufficient on its own, as levels of inequality matter. Higher levels of inequality have been shown to undermine the poverty-reducing effect of economic growth. This is because an initial maldistribution of physical, human and financial resources makes it much harder for poor people to participate in and therefore gain from the proceeds of economic growth. Public expenditure and investment have been unevenly distributed across the regions, with the wealth concentrated in the southern region, especially in Maputo.

Chart 9 depicts the National Development Plan.

The Mozambique National Development Plan or Estratégia Nacional De Desenvolvimento (ENDE) 2023-2043 guides the country's development process, aiming to achieve a long-term vision for the country. Its objectives include improving the country's infrastructure, increasing productivity and competitiveness, promoting economic diversification, promoting access to basic services, promoting social inclusion, strengthening governance and transparency, as well as environmental sustainability to increase the country's productive capacity, the population's living conditions, and reduce social and regional inequalities.

To achieve these objectives, the ENDE is structured around five main pillars: (i) Structural Transformation of the Economy; (ii) Social and Demographic Transformation; (iii) Infrastructures; (iv) Governance; and (v) Environment and Circular Economy. Each pillar has strategic objectives, result indicators and targets for the period 2023-2043.

Mozambique National Development Plan (ENDE) targets to:

- Reduce the proportion of the population living below the national poverty line from 68.2% currently to 35.8% by 2043. Reach a Gini coefficient of 0.3 by 2043.

- Reduce population growth rate to 1.8% by 2043. Increase life expectancy to 69.5 years.

- Increase the share of exports as a percentage of GDP to 42.3% by 2043.

The eight sectoral scenarios as well as their relationship to the Current Path and the Combined scenario are explained in the Technical page. Chart 10 summarises the approach.

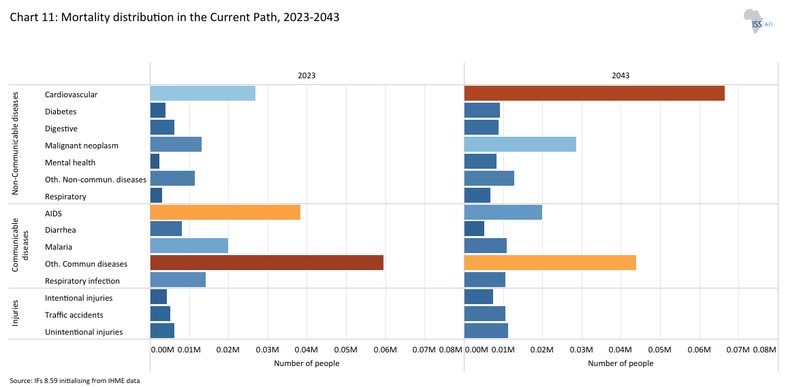

Chart 11 presents the mortality distribution in the Current Path for 2023 and 2043.

The Demographics and Health scenario envisions ambitious improvements in child and maternal mortality rates, enhanced access to modern contraception, and decreased mortality from communicable diseases (e.g., AIDS, diarrhoea, malaria, respiratory infections) and non-communicable diseases (e.g., diabetes), alongside advancements in safe water access and sanitation. This scenario assumes a swift demographic transition supported by heightened investments in health and water, sanitation and hygiene (WaSH) infrastructure.

Visit the themes on Demographics and Health/WaSH for more detail on the scenario structure and interventions.

There are strong interactions between population and health. A country’s health status influences fertility, mortality, and morbidity. At the same time, high population growth increases the demand for basic necessities of life, such as nutrition and health.

Despite efforts to improve Mozambique’s public health sector, it remains one of the least resourced in the world, which has negatively affected the GoM's ability to improve its population's healthcare. As a result, Mozambique has some of the worst healthcare statistics in the world. In 2019, the country ranked 184th for overall health efficiency among 191 World Health Organisation (WHO) member states, with a low score of 0.26 out of 1.0.

The country has a ratio of only three doctors per 100 000 people, a proportion that is among the lowest in the world. Systems for tracking, motivating and retaining staff are weak, and frontline health providers are often poorly trained and have limited management skills. For those in rural areas and the extremely poor, women, adolescent girls and children, quality healthcare is very unsatisfactory and hard to reach, exposing health system inequalities between genders and geographic regions.

Mozambique spends relatively less on healthcare compared to its peer countries, although health expenditure has been on an upward trend since 2014. According to WHO data, Mozambique allocated about 6.8% of its total government expenditure to healthcare in 2023, a slight decrease from 7% in 2022.

The efficiency of a country’s health system can be assessed through indicators such as maternal mortality, infant mortality and life expectancy. Mozambique has made notable progress in reducing mortality rates and expanding access to primary health services. In 2023, the country recorded 99 maternal deaths per 100 000 live births, lower than the average for low-income African countries (331) and Southern Africa regional peers (162). The Sustainable Development Goal target for maternal mortality (SDG 3.1) is to reduce maternal mortality to fewer than 70 deaths per 100 000 live births by 2030. On the Current Path, Mozambique is likely to meet this target, with maternal mortality projected to decline to 64 deaths per 100 000 live births by 2030 and 42 by 2043.

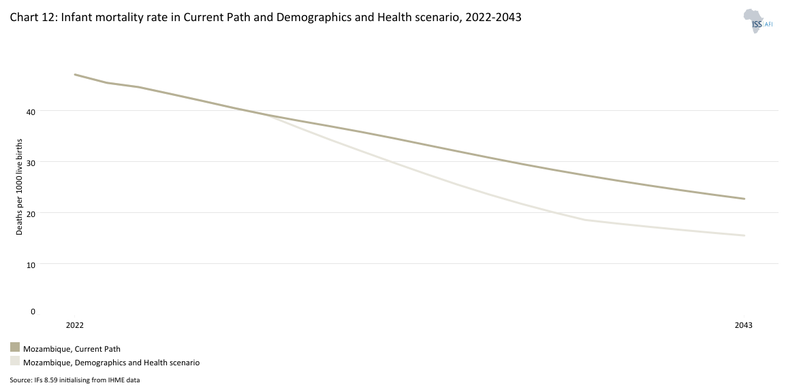

Chart 12 presents the infant mortality rate in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

In 2024, Mozambique’s infant mortality rate remained among the highest in low-income African countries, at 44.7 deaths per 1 000 live births. The SDG target is to reduce infant mortality to below 25 deaths per 1 000 live births by 2030. On the Current Path, Mozambique is unlikely to meet this target, with the infant mortality rate projected to decline to 37 deaths per 1 000 live births by 2030 and 22.7 deaths per 1 000 live births by 2043. While this represents substantial progress over the long term, the 2030 level will remain above the SDG target, although the 2043 forecast would fall below the GoM’s target of 35 deaths per 1 000 live births in the same year.

Low life expectancy and high infant mortality in Mozambique are closely linked to the high prevalence of communicable diseases, which impose significant human and economic costs. In 2024, the death rate from communicable diseases in Mozambique stood at about 4 per thousand, which was 7.2% higher than the average for low-income African countries (3.8 per thousand) and 4% higher than the average of its regional peers (3.9 per thousand). This comparatively high disease burden highlights ongoing limitations in healthcare access, disease prevention, and treatment capacity.

The cohort death rate distribution shows that most premature deaths in Mozambique occur in the early stages of life and are heavily skewed toward communicable diseases. Premature mortality in Mozambique is concentrated largely in the early stages of life and is predominantly driven by communicable diseases. Higher mortality among infants and children not only reflects poor health conditions but also undermines the accumulation of human capital, potentially constraining the country’s long-term economic growth. Even in the working age groups, communicable disease deaths dominate. In particular, AIDS represents the largest health burden among individuals aged 30–44 and 45–59. High mortality within these cohorts reduces the working-age population, dampens productivity, limits human capital development and raises fiscal pressures on the healthcare system.

Much of the communicable disease burden for infants and children aged 1 to 4 years is the result of a lack of health infrastructure. The use of traditional fuel sources (i.e., coal, dung) is a core driver of childhood pneumonia and other respiratory infections. Lack of health facilities for malaria testing and treatments, and low bed net use contribute to Mozambique’s high malaria burden. Meanwhile, poor water and sanitation access are a core driver of communicable disease deaths (such as diarrhoea) for children under five years of age. This high communicable disease prevalence in children under five years of age can also lead to undernourishment and stunting.

The prevalence of malnutrition has remained high in Mozambique, with 38% stunting and 6% wasting among children under five years of age. Around 209 250 children aged 6-59 months suffer from acute malnutrition, and 72 199 cases of acute malnutrition in pregnant (or lactating) women were recorded between May 2023 and March 2024. On the Current Path, the stunting rate of children under five years of age will decline to 25.1% by 2043, about 14.9 percentage points above the GoM target rate in the same year in the National Development Strategy (2023-2043).

In the older age cohort (60-69 years), the disease burden shifts toward non-communicable diseases, such as cardiovascular disease, diabetes and cancers. This shift reflects Mozambique’s gradual epidemiological transition, a point at which death rates from non-communicable diseases exceed those of communicable diseases. This transition has important implications for Mozambique’s healthcare system. Managing this dual burden will require expanded investment in healthcare infrastructure, improved capacity for chronic disease management and stronger preventive health systems.

Strengthening disease prevention efforts, improving access to healthcare services and reinforcing public health systems will therefore be essential to improving population health and supporting Mozambique’s long-term economic development.

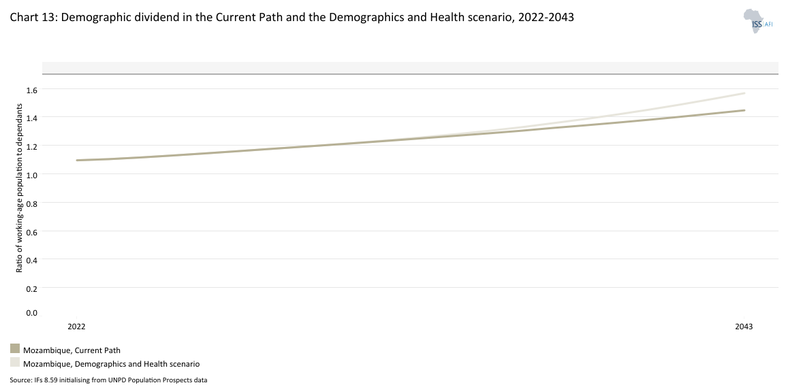

Chart 13 presents the demographic dividend in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The dividend is the window of economic growth opportunity that opens when the ratio of working-age persons to dependants increases to 1.7 to 1 and higher.

The Demographics and Health scenario aims to improve health and expand the demographic dividend. It consists of reasonable but ambitious reductions in child and maternal mortality, increased access to modern contraception and reductions in the mortality rate associated with both communicable diseases (e.g. AIDS, diarrhoea, malaria and respiratory infections) and non-communicable diseases (e.g. diabetes), as well as improvements in access to safe water and better sanitation.

If the Demographics and Health scenario is implemented, Mozambique could accelerate its demographic transition to reap the demographic dividend by 2047 (Chart 13), seven years earlier than under the Current Path. Generally, the demographic dividend materialises when a country reaches a ratio of at least 1.7 working-age people for each dependent.

Chart 14 presents crop production and demand in the Current Path from 1990 to 2043.

The Agriculture scenario envisions an agricultural revolution that ensures food security through ambitious yet feasible increases in yields per hectare, thanks to improved management, seed, fertiliser technology and expanded irrigation. Efforts to reduce food loss and waste are emphasised, with increased calorie consumption as an indicator of self-sufficiency and prioritising it over food exports. Additionally, enhanced forest protection signifies a commitment to sustainable land use practices.

Visit the theme on Agriculture for our conceptualisation and details on the scenario structure and interventions.

Mozambique has significant untapped agricultural potential, with 45% of its land arable, yet only 16% is currently cultivated. The country’s strategic geographic position allows it to play an important role as an entrepot for agricultural trade with its neighbouring landlocked countries.

The agriculture sector is the mainstay of Mozambique's economy. It accounts for over a quarter of its GDP and employs 80% of the workforce. The majority of agricultural output comes from smallholder farmers, who account for approximately 3.2 million individuals and contribute 95% of the nation's agricultural production, while the remaining 5% is attributed to commercial farming enterprises.

Maize and cassava are the main food staples and are grown by 80% of all Mozambican smallholders. Other important staples are wheat and rice. Animal production, particularly poultry and small ruminants, holds significant importance in rural livelihoods and nutritional sustenance. In urban settings, formal meat outlets rely heavily on beef and poultry, supplying over 80% of the meat demand. The limited number of commercial farmers focus on cash crops such as tobacco, cotton, cashew nuts and sugar. The volatility of commodity prices and fluctuations in global markets considerably impact Mozambique's commercial agriculture and overall economic landscape.

The potential has not translated into production. Mozambique has one of the lowest average crop yields per hectare in Africa. With an estimated 3.4 tons per hectare in 2024, the country ranked 26th out of 55 African countries and had the 5th-lowest crop yields in Southern Africa in 2024. On the Current Path, the average crop yields per hectare in Mozambique will marginally increase to 4.5 tons by 2043, below the estimated average of 6.5 tons for Southern Africa but slightly above the average of 3.8 tons for low-income countries in Africa.

The low agricultural productivity in Mozambique stems from various factors, including limited access to agricultural finance and improved inputs, slow adoption of technology, insufficient agricultural services and reliance on rain-fed farming coupled with vulnerability to climate hazards.

Mozambique ranks as the third most vulnerable African country to climate change, facing threats such as tropical cyclones, droughts and coastal flooding. Its extensive coastline, spanning 2 700 km, exacerbates this vulnerability, particularly for the 60% of the population residing in low-lying coastal regions. These areas face risks to infrastructure, coastal agriculture, ecosystems and fisheries from intense storms and rising sea levels, with repercussions felt inland as well. Between the period 1980–2019, Mozambique experienced a total of 53 natural disaster events, comprising 21 tropical cyclones, 20 floods and 12 drought occurrences. According to the Global Climate Risk Index, Mozambique was the most affected country in the world by the impacts of extreme weather events in 2019 and the fifth most affected when considering the period 2000–2019.

Disasters further impede access to markets, compounding challenges for rural producers heavily reliant on climate-sensitive agriculture for sustenance and income. In addition to being among the most vulnerable countries regarding natural disasters, Mozambique is among the least prepared countries for these climatic hazards, ranking 154th out of 185 nations on the Global Adaptation Index (ND-GAIN).

Moreover, inadequate road infrastructure poses a significant obstacle to agricultural development; it hinders the establishment of essential linkages along value chains and impedes the adoption of modern technologies crucial for enhancing productivity, such as fertilisers, pesticides, improved seeds and mechanised equipment. They increase transportation costs, hampering farmers' access to both domestic and international markets. Our interviews conducted during the fieldwork found that food importers in Maputo prefer to import from South Africa rather than from the local production zones because it can take a week to bring produce from these areas to Maputo due to poor road conditions.

Compared to many developing countries, the GoM's support for the agriculture sector is high, although the recent period has seen a slow decline in public spending on agriculture. The average share of agriculture in the national budget was above 4% from 2010 to 2014 and fell to 4% in the subsequent five-year period (2015–2019), less than half of the 10% target recommended by the Comprehensive Africa Agriculture Development Programme (CAADP).

The low agricultural productivity is unable to meet the nutritional demands of the growing population. Many rural farmers remain net food consumers and vulnerable to increases in food prices. As a result, the nutrition situation in the country remains precarious, with about 43% of children under five suffering from chronic undernutrition. In 2022, the Global Food Security Index ranked the country at the lower end (94 out of 113 countries), with particularly low scores in food quality, safety, and affordability.

Going forward, climate change will exacerbate their frequency and intensity in Mozambique. Feeding the growing population under such conditions will be one of the country's biggest challenges. In 2024, an estimated 19.1 million metric tons of crops were produced, a significant increase from the 5.1 million metric tons produced at the end of the civil war in 1992. On the Current Path, crop production will increase to about 27.5 million metric tons by 2043, while crop demand is set to increase from 22.1 million metric tons in 2023 to about 42.5 million metric tons by 2043, causing a deficit of about 15 million metric tons (Chart 14). The Current Path paints a picture of a growing gap between domestic food production and demand, a situation that will exacerbate Mozambique's agricultural trade deficit.

Boosting agricultural productivity would not only raise the incomes of farm households, which account for a significant share of the country's population, but it would also lower food costs for the non-farm population and pave the way for agro-industry development. The GoM should enhance the efficiency of its agricultural support policies and programs to boost agricultural development, reduce poverty and ensure food security. Efforts should be made to address the high gender gap in agriculture. Women are disproportionately concentrated in subsistence agriculture in Mozambique, but they face more constraints than men in accessing essential productive resources and services, technology, market information and financing.

Chart 15 presents the import dependence in the Current Path and the Agriculture scenario, from 2020 to 2043.

Agriculture is the source of livelihood for millions of Mozambicans. Yet, according to the Current Path analysis, the sector faces several challenges that negatively impact productivity. Investing in agriculture can ensure food security, reduce resource conflicts, provide jobs, increase income and pave the way for economic diversification through agro-processing. Therefore, the interventions in this scenario constitute a coordinated push to unlock Mozambique’s agricultural potential.

The interventions in the scenario reflect an aggressive yet reasonable improvement in agricultural productivity (average yields) as a result of adopting modern, climate-smart agricultural technologies, improved seedlings, and increased fertiliser and pesticide use. Likewise, irrigated land is increased to reduce the vulnerability of rainfed crops. The scenario also reduces post-harvest losses through improved storage facilities and enhanced market access (rural roads). Forest protection is also increased as a proxy for sustainable land practice. While the sector can benefit from increased export revenues, it should focus its attention first on establishing food security.

Under the Agriculture scenario, the average crop yield will be 6.5 tons per hectare by 2043, on par with the regional average. The country will produce about 10.2 million metric tons of additional food (crops) in 2043 compared to the Current Path. The agricultural crop import dependence will be about 22.1% of total crop demand compared to 36% in the Current Path in 2043.

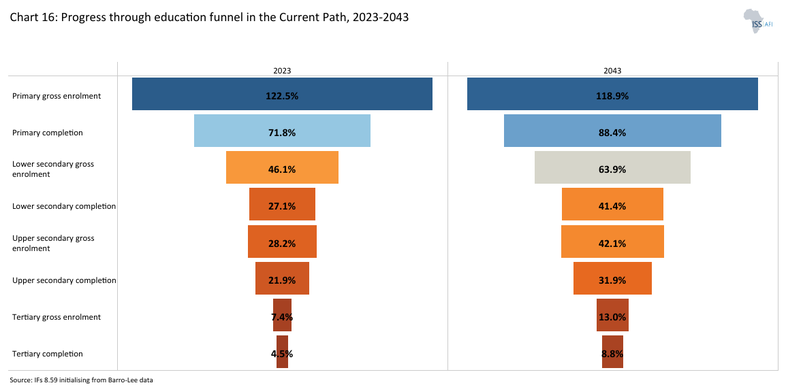

Chart 16 depicts the progress through the educational system in the Current Path, for 2023 and 2043.

The Education scenario represents reasonable but ambitious improvements in intake, transition, and graduation rates from primary to tertiary levels and better quality of education at primary and secondary levels. It also models substantive progress towards gender parity at all levels, additional vocational training at the secondary school level, and increases in the share of science and engineering graduates.

Visit the theme on Education for our conceptualisation and details on the scenario structure and interventions.

Education is a critical driver of human development and economic productivity, and can be conceptualised as a pipeline through which learners progress. Children enter the system at the primary level and move through successive stages—lower-secondary, upper-secondary and, in some cases, tertiary education. Ideally, this process equips individuals with the skills needed to meet the country’s economic and labour market needs. Ensuring that a large proportion of learners successfully navigate key transition points, particularly the progression from primary to secondary education, is therefore essential for improving educational attainment and strengthening human capital development.

The educational system under Portuguese rule in Mozambique had a distinct dual structure. It aimed to provide basic skills to the majority of the African populace while offering liberal and technical education to the settler community and a small fraction of Africans. The vast majority of students, more than four-fifths, were limited to basic education within this colonial framework. Public education, supported by the state and the Roman Catholic Church, was predominant, although private options, primarily affiliated with religious institutions, also existed. Literacy in Portuguese, the primary language of instruction, was limited among the African population at the time of independence.

The introduction of the National System of Education in the early 1980s aimed at enhancing literacy and technical skills across all age groups, catering to both part-time and full-time students. The nationalisation of private and religious educational institutions facilitated the restructuring and consolidation of the education system. Despite rapid expansion, the state struggled to meet the growing demand for education. Primary school enrolment surged from 643 000 in 1973 to approximately 1.5 million by 1979, but declined in the 1980s due to the destruction of schools by Renamo insurgents. The civil war destroyed critical infrastructure, including schools, and prevented meaningful education for the majority of the Mozambican older generation.

Only about 63.2% of the adult population was literate in 2024, which was about 21 percentage points below the average for Southern Africa, while only 47% of the adult population (15-24 years) completed primary school, and about 11.6% completed secondary education in 2024.

The education system in Mozambique is structured similarly to those of many countries in the region, comprising three main levels: primary, secondary and tertiary education. In 2018, the National Education System Law was revised, introducing a new sector structure and extending compulsory (and free) education from seven to nine years. As part of this reform, the duration of the education cycles was adjusted: primary education was reduced from seven to six years, while secondary education was expanded from five to six years. The law also formally recognised preschool as a sub-sector of education for the first time, although attendance is not required for entry into primary school. These reforms, together with increased government commitment and sustained investment in the sector, have contributed to notable progress. However, the system continues to face efficiency challenges, and a significant bottleneck between primary and lower-secondary education still limits overall educational attainment.

The GoM has made significant progress in expanding primary school enrolment, with the enrolment rate increasing by more than 80% between 1998 and 2024. As a result, Mozambique now records a higher primary school enrolment rate than many of its regional peers (Chart 20). This progress is largely due to primary education in Mozambique being free and compulsory. However, several barriers continue to limit students’ ability to access and remain in school, including the cost of school supplies, malnutrition during early childhood, gender norms and inadequate transport infrastructure. In 2024, Mozambique’s gross primary school enrolment rate stood at 123.1%. Gross enrolment rates above 100% typically indicate the presence of students who are outside the official age range for the level of education they are attending.

Despite high primary school enrolment rates, Mozambique’s human capital outcomes remain constrained by low completion rates. Only 36.5% of students enrolled in primary school reach the final grade of the primary cycle. As a result, although many Mozambican children enter primary education, only about half complete it, limiting the accumulation of foundational skills.

A significant bottleneck also exists in the transition from lower- to upper-secondary education. Only 27.7% of students who enter lower-secondary school complete it, and just 29% of those who do go on to enrol in upper-secondary education. As a result, the already small group of students who complete primary education becomes even smaller as they progress through the education pipeline. Consequently, only a limited number of students reach upper-secondary school. These weak outcomes at the lower-secondary level are a key factor behind low tertiary education attainment, ultimately constraining progress in reducing poverty and inequality.

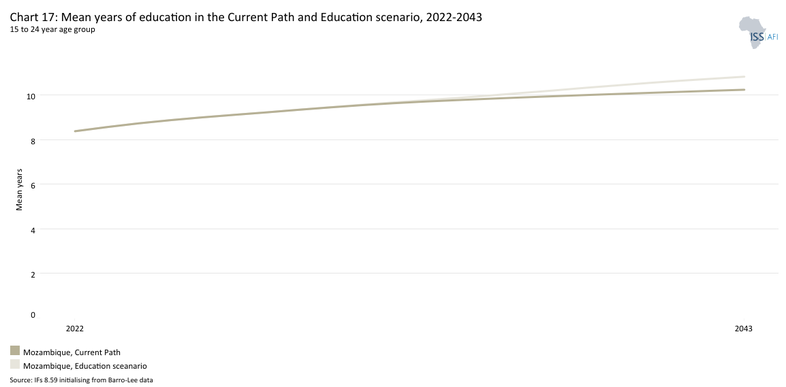

Chart 17 presents the mean years of education in the Current Path and in the Education scenario, from 2020 to 2043, for the 15 to 24 age group.

The average years of education in the adult population aged 15 to 24 is a good first indicator of how the stock of knowledge in society is changing.

The average years of education among the adult population aged 15-24 years is a valuable indicator of how the stock of knowledge in society is changing. In Mozambique, the mean for this cohort is below the averages for its peers. In 2024, it was estimated at 8.7 years, slightly below the average of 8.7 years for Southern Africa.

According to the African Development Bank (AfDB), the low quality of Mozambique’s labour force remains a significant challenge. Employers often struggle to find adequately qualified workers, while the limited skills base also constrains the development of entrepreneurship. Due to low educational levels, some foreign companies operating in the country have resorted to importing labour. In response, the GoM recently increased the maximum quota for employing foreign workers as a share of the workforce—from 10% to 15% for companies with up to 10 employees, and from 8% to 10% for companies with 11–30 employees. The quotas remain unchanged at 8% for firms with 31–100 employees and 5% for those with more than 100 employees. At the same time, the government has expanded scholarship programs that enable Mozambican students to study abroad and acquire specialised skills, particularly in the extractives sector.

Skills mismatches are prevalent in Mozambique. In 2008, between 43% and 8% of the employed were underqualified for the positions they held, even as the labour market requires relatively low-skilled labour. The severe shortage of skilled labour is not only in managerial positions but also in skilled professionals such as engineers, technicians and accountants. Some companies often import skilled labour. The lack of sufficiently skilled labour is, therefore, a major challenge for moving the workforce from low-paying, low-productivity, informal and rural work to the more productive, formal sectors.

The Current Path forecasts gradual improvements in education outcomes over time. By 2043, the mean education among the adult population aged 15-24 years will increase to 10.2 years. Under the Education scenario, the average educational attainment of adults aged 15-24 will increase to 10.8 years by 2043. The scenario will also improve primary school outcomes, with the completion rate rising to 63.5% by 2043, compared to 60.6% in the Current Path. In addition, the Education scenario will significantly expand secondary education participation and completion. By 2043, nearly 76% of age-appropriate students are projected to enrol in secondary school, compared to 55% in the Current Path. Lower-secondary completion will reach 50.1% (up from 41.4% in the Current Path), while upper-secondary completion rises to 37.4%, compared with 31.9% in the Current Path. As a result, the adult literacy rate will increase to 81.8%, about one percentage point higher than in the Current Path.

Since the benefits of education improvements take decades to materialise, expanding access and ensuring that more children progress from primary to secondary education now will be critical for improving long-term outcomes.

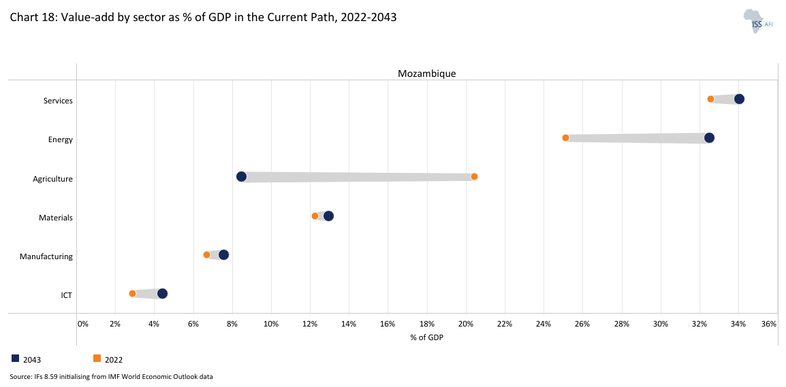

Chart 18 presents the value-add by sector as share of GDP in the Current Path, for 2023 and 2043.

In the Manufacturing scenario, reasonable but ambitious growth in manufacturing is envisaged through increased investment in the sector, research and development (R&D) and improved government regulation of businesses.

Visit the theme on Manufacturing for our conceptualisation and details on the scenario structure and interventions.

The manufacturing sector in Mozambique is weak and unable to play a leading role in economic growth and development; it is limited to small-scale processing, and its contribution to GDP has declined since 2005. According to the 2022 Mozambican Manufacturing Firms survey, only 5% of firms export. The sector accounted for about 10% of GDP, on average, over the period 2000-2022, while agriculture, the extractive industry and services accounted for 24%, 18% and 45%, respectively. In 2023, manufacturing value added accounted for 7.3% of GDP, below the average of 9.2% for low-income countries in Africa. On the Current Path, manufacturing will account for 7.6% of Mozambique's GDP by 2043, below the projected average of 16.2% for low-income Africa.

In the interviews conducted during our fieldwork trip, many experts and economists indicated that the manufacturing sector in Mozambique has significant potential. Still, its performance has been hamstrung by several factors, such as weak transport infrastructure, which prevents the connection between farmers and manufacturing firms (downstream beneficiation), poor implementation of business regulation (officially one day is required to register a business but three months in practice), the high cost of credit, technological delay and fierce competition from South African manufacturing firms.

Like in other African countries, many impoverished individuals in Mozambique find themselves entrenched in low-productivity sectors and informal service-based activities. Boosting the manufacturing sector will drive inclusive growth by facilitating the transition of low-income individuals from these sectors into higher-productivity areas. This structural shift not only boosts incomes but also fosters a positive cycle in which the growth of productive employment, capacities and earnings mutually reinforce one another, propelling economic expansion and poverty reduction. Expanding more dynamic sectors can further fuel this virtuous cycle, leading to sustained growth and increased prosperity.

There is a need to enhance the manufacturing industry through strong backward and forward linkages with the agriculture, mining and service sectors to achieve sustained growth, reduce poverty and diversify sources of income and foreign exchange earnings. However, industrialisation or economic transformation is a long-term process. It requires constructive relationships between the state and the private sector that encourage and support it. Firms need a state that has strong capabilities in setting an overall economic vision and strategy, efficiently providing supportive infrastructure and services, maintaining a regulatory environment conducive to entrepreneurial activity and making it easier to acquire new technology and enter new economic activities and markets.

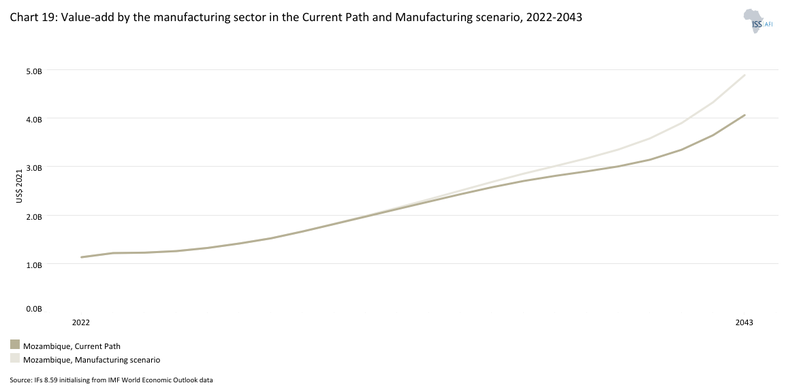

Chart 19 presents the contribution of the manufacturing sector to GDP in the Current Path and in the Manufacturing scenario, from 2020 to 2043. The data is in US$ and % of GDP.

Without a robust manufacturing sector, sustained growth cannot be achieved, and sufficient jobs cannot be created to reduce poverty in the country. This scenario, therefore, models the impact of a concerted effort by the Mozambican authorities to unleash the potential of the non-extractive sector with a particular focus on manufacturing.

Under the Manufacturing scenario, the value added of the manufacturing sector will be US$826 million (equivalent to a percentage point of GDP) above the Current Path in 2043 (Chart 19).

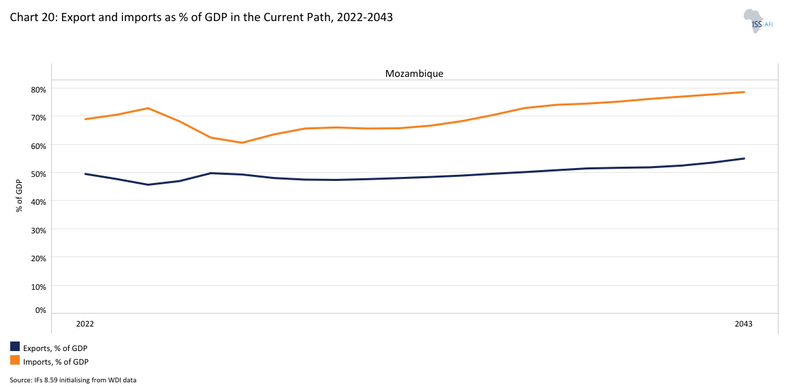

Chart 20 depicts exports and imports as a percentage of GDP, from 2000 to 2043, in the Current Path.

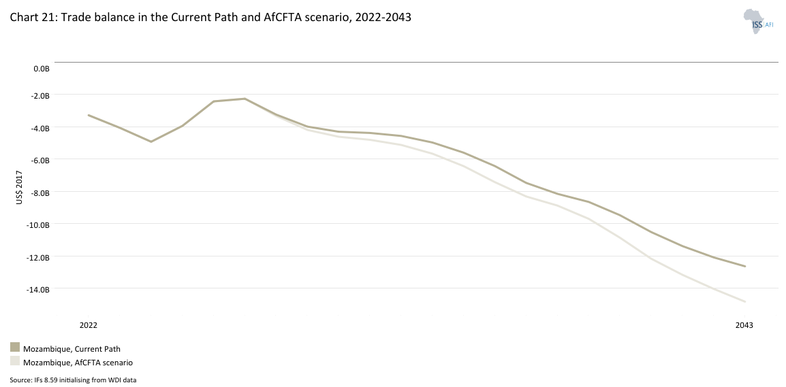

The AfCFTA scenario represents the impact of fully implementing the African Continental Free Trade Agreement by 2034. The scenario increases exports in manufacturing, agriculture, services, ICT, materials and energy exports. It also includes improved multifactor productivity growth from trade and reduced tariffs for all sectors.

Visit the theme on AfCFTA for our conceptualisation and details on the scenario structure and interventions.

Mozambique’s economy is highly open to international trade, with total trade (exports plus imports) estimated at 96% of GDP in 2024, significantly higher than the averages for its peer groups—reflecting strong integration into global markets. However, the country’s trade structure remains narrow and commodity-dependent, with exports heavily concentrated in mineral fuels, particularly natural gas and coal. This concentration exposes the economy to external shocks, including fluctuations in global commodity prices and demand, as foreign-exchange earnings depend largely on the performance of the extractive sector.

At the same time, Mozambique relies substantially on imports of manufactured products and capital inputs, reflecting the limited diversification of its productive base and weak domestic industrial capacity. However, capital imports, such as machinery, industrial equipment and advanced technologies, are critical for supporting investment and production, particularly in capital-intensive sectors such as mining and energy. These imports enable the development and operation of large-scale extractive and infrastructure projects, which remain key drivers of export revenues, foreign-exchange inflows and government fiscal revenues.

At the regional level, Mozambique is a member of several regional integration frameworks, most notably the Southern African Development Community (SADC). Mozambique is also a member state of the Tripartite Free Trade Area (TFTA) Agreement, which seeks to integrate the markets of COMESA, the East African Community (EAC) and SADC into a single larger free trade area. However, Mozambique has not yet signed the agreement, which entered into force on 25 July 2024. Mozambique is also a state party to the African Continental Free Trade Area (AfCFTA), having ratified the agreement in July 2023. Participation in the AfCFTA is expected to expand market access across Africa, support export diversification and enhance the country’s resilience to external economic shocks, including fluctuations in global commodity prices and disruptions to international supply chains.

At the multilateral level, Mozambique is a member of the China-Africa Cooperation Forum (FOCAC), a platform for consultation and dialogue between China and African states, established in October 2000. In February 2018, Mozambique joined the European Union (EU)-SADC Economic Partnership Agreement (EPA) that was signed in June 2016 by Botswana, Eswatini, Lesotho, Namibia and South Africa. The EU-SADC EPA entered into force provisionally in October 2016. Mozambique has remained eligible for the African Growth and Opportunity Act (AGOA) since its inception. AGOA is still in force in 2026, but it has only been extended until December 2026, and its long-term future remains uncertain. AGOA provides preferential access to the United States (US) market, which would allow eligible countries to invest, upgrade and diversify their exports while producing opportunities for increased employment and value-capture of locally grown and produced goods. The country has not taken full advantage of the duty-free preference. In 2023, Mozambique’s exports to the US were just US$210 million.