9 Leapfrogging

9 Leapfrogging

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This theme explores the potential of modern technology to accelerate Africa’s development, including through the widespread adoption of decentralised renewable energy systems, expanded Internet access and other frontier technologies. The subsequent Large Infrastructure and Leapfrogging scenario combines these interventions with the potential impact of investments in large infrastructure, such as paved roads, ports, railways and airports. The latter is discussed in a separate theme on Large Infrastructure, using the same scenario.

Summary

This theme begins with an introductory overview of technological leapfrogging and its relevance to Africa’s development trajectory. It situates leapfrogging within the continent’s broader structural context, highlighting both its potential and its limitations.

- Africa faces major infrastructure gaps in electricity, transport and water. However, these challenges create a unique opportunity to bypass traditional development models and adopt decentralised, digital, and more efficient technologies.

- Africa’s mobile revolution is a leading example of leapfrogging: Fixed-line access has remained minimal, while mobile subscriptions have surged dramatically. Internet penetration, though still low (35% in 2024), has grown rapidly from just 7.5% in 2009.

- Mobile technology has transformed access to financial services, enabling millions of unbanked people to use payments, savings, credit and insurance services without traditional banks.

- Sub-Saharan Africa leads globally, with over 1 billion mobile money accounts and 280 million active users.

- Annual transaction values exceeded US$1 trillion by 2025, supported by a growing digital ecosystem.

- Africa can leapfrog fossil fuel–based systems by scaling renewable and decentralised energy solutions, particularly solar. Off-grid and mini-grid systems are already expanding electricity access faster and more affordably than traditional grid infrastructure, especially in rural areas.

- New technologies provide an opportunity to gradually formalise the informal sector, improving productivity, financial inclusion and economic participation.

- Artificial intelligence represents the next frontier of leapfrogging in Africa, building on expanding digital connectivity and offering potential to transform key sectors and accelerate development.

- Realising these opportunities depends on enabling conditions, including infrastructure, skills, financing and regulatory frameworks, which remain uneven across countries.

The second half of this theme report then models a positive Large Infrastructure and Leapfrogging scenario and its impacts on the economy and poverty.

- Strategic investments in infrastructure and digital technologies could deliver substantial gains in Africa by 2050.

- GDP per capita could increase by about US$510.

- Extreme poverty could be reduced by 63 million people, bringing the total to around 299 million.

- The overall economy could expand by nearly US$1 trillion compared to the Current Path projections.

The theme concludes with recommendations for African policymakers, highlighting the importance of coordinated investments, enabling policy environments and inclusive approaches to ensure that leapfrogging translates into sustained and broad-based development outcomes. Leapfrogging is both a challenge and an opportunity for Africa. If strategically managed, it can drive rapid economic growth, poverty reduction and greater economic independence.

All charts for Leapfrogging

- Chart 1: Electricity access in Africa, 2022-2024 with forecast to 2050

- Chart 2: Mobile phone, mobile broadband and fixed broadband subscriptions, 2022-2024 with forecast to 2050

- Chart 3: Internet access, 2022-2024 with forecast to 2050

- Chart 4: M-Pesa transactions volume in Africa, 2017-2025

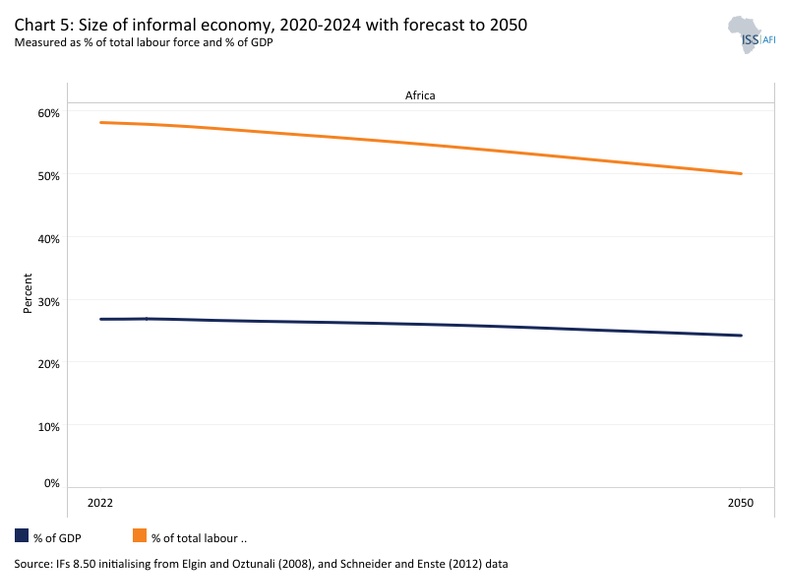

- Chart 5: Size of informal economy 2022 to 2024 with a forecast to 2050: per cent of GDP and per cent of labour force

- Chart 6: Schematic of the Large Infrastructure and Leapfrogging scenario

- Chart 7: Renewable share of energy production, Current Path vs scenario: 2022-2024 with forecast to 2050

- Chart 8: Internet access, Current Path vs scenario: 2022-2024 with forecast to 2050

- Chart 9: GDP (MER), Current Path vs scenario: 2022-2024 with forecast to 2050

- Chart 10: GDP per capita (PPP), Current Path vs scenario: 2022-2024 with forecast to 2050

- Chart 11: Extreme poverty rate in Large Infrastructure and Leapfrogging scenario vs Current Path, 2020 to 2024 with forecast to 2050

- Chart 12: Recommendations

Development leapfrogging refers to a country's, particularly a developing economy's, ability to skip intermediate stages of technological and industrial development and move directly to more advanced systems. Rather than following the historical pathway taken by industrialised nations, latecomers can adopt newer technologies and institutional models that enable faster productivity gains and more rapid structural transformation.

Leapfrogging has long accompanied major technological shifts. Innovations such as the printing press, the steam engine, and later the personal computer replaced older systems and transformed economic activity.

What distinguishes the 21st century is the speed and scale of technological progress. Advances in digital technologies, artificial intelligence (AI), biotechnology and renewable energy are rapidly translating scientific knowledge into practical applications, expanding countries' potential to adopt more efficient solutions without replicating outdated systems.

Although many frontier technologies originate in high-income economies, their impact may be particularly significant in developing regions, where legacy infrastructure is limited. In economies with extensive established systems, such as centralised energy grids, large transport networks and complex industrial supply chains, existing investments often create strong incentives to maintain current technologies. This phenomenon, known as path dependency, can slow the adoption of alternative approaches. By contrast, countries with limited infrastructure may have greater flexibility to adopt newer, more efficient technologies from the outset.

Africa presents one of the most compelling opportunities for development leapfrogging in the modern global economy. The continent faces significant infrastructure deficits, particularly in electricity, transport and water and sanitation systems. However, these gaps can also create opportunities to adopt new, decentralised and digital technologies rather than replicating traditional infrastructure systems. Rapid urbanisation, a young and increasingly connected population and expanding digital networks further strengthen the potential for accelerated technological adoption.

New technologies are already opening pathways for leapfrogging across multiple sectors. Digital mobile communications have expanded connectivity and financial inclusion, while drones are increasingly used for logistics and precision agriculture, improving service delivery and productivity in remote areas. Similarly, decentralised renewable energy systems, such as solar mini-grids and off-grid power solutions, are enabling electricity access in rural communities far from national grids. These technologies demonstrate how developing countries can adopt modern systems that bypass the costly and time-consuming infrastructure trajectories followed by earlier industrialisers.

Leapfrogging is increasingly visible in sectors such as mobile finance, renewable energy, agricultural technology and digital services. AI is reinforcing this trend by enhancing productivity and decision-making, for example, through crop monitoring, health diagnostics, energy optimisation and automated digital services. While these applications can reduce costs and improve efficiency, progress remains largely driven by the adoption and adaptation of existing technologies, reflecting ongoing constraints in research capacity, infrastructure and skilled human capital. AI also introduces new challenges, including limited data ecosystems, skills shortages, potential job displacement and concerns around data governance, bias and regulatory readiness.

Realising all these opportunities, however, depends on supportive enabling conditions. Innovation policies, appropriate regulatory frameworks, investments in digital infrastructure and the development of relevant skills will shape how effectively countries can deploy and adapt frontier technologies. These factors are critical to ensuring technological adoption.

This theme starts by examining Africa’s potential to leapfrog by analysing the key drivers of technological adoption, highlighting emerging examples across sectors, and assessing the enabling conditions and constraints that will shape the continent’s development trajectory. It then models the potential impact of a leapfrogging scenario on Africa’s long-term development prospects, using the same scenario modelling as the impact of large infrastructure developments, which is examined in a separate theme, before concluding.

Importantly, this theme does not do justice to the full impact of new technologies including generative artificial intelligence to improve development outcomes. The impact of advances in health, for example, is modelled and included as outcomes in that theme, similarly regarding education, manufacturing, financial flows and even governance. The real effect of leapfrogging is, therefore, dispersed across various themes and only fully captured in the Combined scenario.

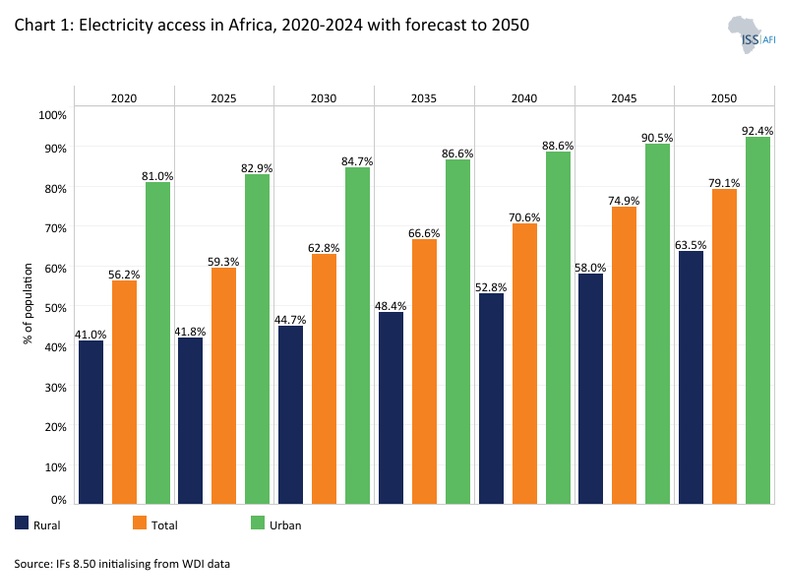

Despite progress, energy access remains a major challenge in Africa. In 2022, only 58.5% of the population had electricity, leaving about 600 million people (41.5%) without power.

Sub-Saharan Africa accounts for most of this deficit. While global electricity access reached 91.3% in 2022, sub-Saharan Africa lagged far behind at 51.5%. Countries such as Nigeria, DR Congo and Ethiopia have the largest numbers of people without access to electricity. In contrast, South Sudan, Burundi and Chad have the highest proportions of their populations without access.

Access is also strongly unequal between urban and rural areas. In 2022, 83% of urban residents had electricity, compared with just 42% in rural areas.

Even where electricity is available, it is often unreliable and expensive. In many countries, households and businesses rely on costly backup generators, driving up the effective price of electricity and constraining economic activity. Rapid population growth in sub-Saharan Africa is also offsetting gains in electrification, slowing progress.

According to United Nations data, Africa’s per capita electricity consumption declined from approximately 660 kilowatt-hours (kWh) in 2015 to just 514.7 kWh in 2022, marking its lowest level in over two decades. This downward trend highlights a critical challenge: while access to electricity has expanded in many countries, actual consumption is not keeping pace. In many cases, households and businesses remain constrained by unreliable supply, high costs and weak grid infrastructure, limiting the amount of electricity they can effectively use.

As a result, electricity consumption across much of the continent remains well below global averages, reflecting both limited access and affordability barriers. This persistent energy gap has significant economic consequences. It constrains industrial development, reduces agricultural productivity, particularly where cold storage and processing are needed, and discourages private investment in sectors that depend on consistent, reliable power.

On the current trajectory, electricity access in Africa will reach 79% of the population by 2050, about 63.5% in rural areas and 92% in urban areas. Traditional grid expansion alone is unlikely to close Africa’s energy gap quickly enough, especially given that a large share of the population lives in rural and dispersed communities. Extending centralised grids to these areas is often prohibitively expensive and slow.

Africa’s energy challenge presents a unique opportunity to leapfrog traditional fossil fuel–based development and transition directly to cleaner, cheaper, decentralised systems. Renewable energy offers a practical pathway to rapidly expand access to affordable and reliable electricity, particularly in underserved areas. Unlike conventional grid expansion, which is often slow and costly, off-grid and mini-grid solutions, especially solar-based ones, are already delivering power to millions of households more quickly and at lower cost. These systems are central to closing the access gap, with mini-grids providing a scalable, flexible option when extending the national grid is not feasible.

Geospatial analyses reinforce this conclusion, showing that achieving universal electrification in sub-Saharan Africa by 2030 will require a cost-effective mix of technologies, with solar-based off-grid and mini-grid systems playing a central role. According to World Bank estimates, supplying electricity to 380 million people by 2030 will require more than 160 000 mini-grids at a cost of around US$ 91 billion. With projected costs as low as US$0.20 per kWh, mini-grids could become the most affordable solution for over 60% of the unelectrified population. Yet deployment remains too slow to meet demand. Progress is constrained by rapid population growth, limited access to long-term financing, insufficient concessional funding, poverty, regulatory bottlenecks and information gaps among key stakeholders.

Expanding electricity access would have wide-ranging social and economic benefits. Reliable power reduces reliance on polluting fuels, improves health outcomes, strengthens education and healthcare systems and supports income-generating activities. It also enables digital connectivity, financial inclusion and innovation, key drivers of modern economic development.

Africa is well positioned to lead this transition, with about 60% of the world’s best solar resources and substantial untapped wind, hydro and geothermal potential. Yet the continent attracts only a small share of global clean energy investment. Africa continues to face a persistent shortfall in clean energy financing. Although global investment has rebounded since COVID-19, it remains highly uneven. Between 2021 and 2022, clean energy finance grew by over 100% in Latin America but only 2.5% in sub-Saharan Africa. Looking ahead, financing prospects are increasingly uncertain. Shifting geopolitical and fiscal priorities, such as the United States’ decision to end its Power Africa initiative after more than a decade, together with rising military spending in Europe, may further constrain climate and development finance.

Domestic structural challenges add to the difficulty. High public debt, shallow capital markets and undercapitalised utilities limit the ability to fund large-scale energy projects. Addressing these barriers will require innovative financing mechanisms that reduce risk, attract private investment, and mobilise domestic and regional capital.

At the same time, emerging technologies such as green hydrogen offer new opportunities for industrial development, positioning Africa to meet its own energy needs and to become a global supplier of clean energy. With the right mix of investment, policy support and technological innovation, the continent can bypass outdated energy systems and build a more inclusive, resilient and sustainable energy future.

Africa’s experience with mobile technology is one of the clearest examples of technological leapfrogging. In the early 2000s, many African countries had limited access to landline telecommunication systems, but in subsequent years, mobile networks rapidly expanded across the continent. Today, hundreds of millions of Africans rely on mobile devices for communication, financial services and internet access, making mobile phones the primary gateway to digital participation for individuals and businesses. This transformation has delivered significant economic benefits, including increased access to information, improved business communication and expanded digital markets.

Instead of following the traditional path of building extensive fixed-line infrastructure, many countries moved directly to mobile networks, dramatically accelerating access to communication services and digital tools.

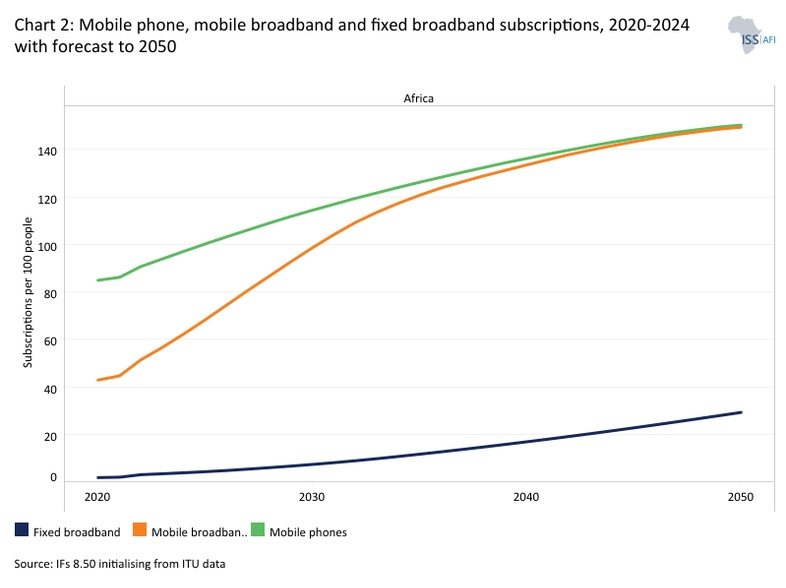

Falling ICT costs played a critical role, enabling mobile penetration to grow across both urban and rural areas. While fixed-line access has remained minimal in Africa, rising only from 2.4 to 2.9 lines per 100 people between 2000 and 2023, mobile subscriptions surged from 1.9 to over 100 per 100 people over the same period. Today, mobile phones provide access not only to communication but also to financial services, education, healthcare and agricultural support, significantly broadening economic opportunities.

Mobile-enabled digital tools are transforming livelihoods. Farmers use platforms to access market prices and connect directly with buyers, while small businesses increasingly rely on smartphones and social media to reach customers. In education, digital platforms are extending learning opportunities beyond traditional classrooms, particularly in underserved areas.

Despite these gains, broadband access remains uneven. While mobile internet use is expanding rapidly, high-speed fixed broadband, critical for large businesses and data-intensive applications, lags. Emerging solutions such as low Earth orbit satellite internet are helping extend connectivity to remote areas, though cost and regulatory challenges persist. Starlink, developed by SpaceX, uses a constellation of satellites in low Earth orbit that provide high‑speed, lower‑latency internet connectivity where terrestrial networks are limited. In early 2026, Starlink launched services in Senegal, contributing to national efforts to extend connectivity to remote and underserved areas. Over the past year, Starlink has also expanded operations in countries such as the Central African Republic, São Tomé and Príncipe, Chad, Somalia, Lesotho, Guinea‑Bissau, DR Congo, Niger and Liberia, significantly broadening its continental footprint.

By offering an alternative where fibre‑optic and traditional mobile network infrastructure are limited, satellite broadband can support remote work, e‑learning, telemedicine, digital commerce and other data-intensive uses. However, relatively high equipment and subscription costs, as well as regulatory hurdles in several markets, remain barriers to widespread adoption.

Chart 2 illustrates the projected number of subscriptions per 100 people in Africa for fixed broadband, mobile broadband and mobile phones. By 2050, mobile phone subscriptions will reach 150 per 100 people, mobile broadband 149 per 100, and fixed broadband 29 per 100 on the current trajectory. The projected near one-to-one alignment between mobile phone and mobile broadband subscriptions in Africa by 2030 means that most phone users will also be internet users, marking a shift to data-driven connectivity where mobile networks become the main platform for services like banking, education and communication. However, this does not eliminate inequality, as affordability, quality and digital skills gaps will remain, shifting the focus from access to the effectiveness and inclusiveness of mobile internet use.

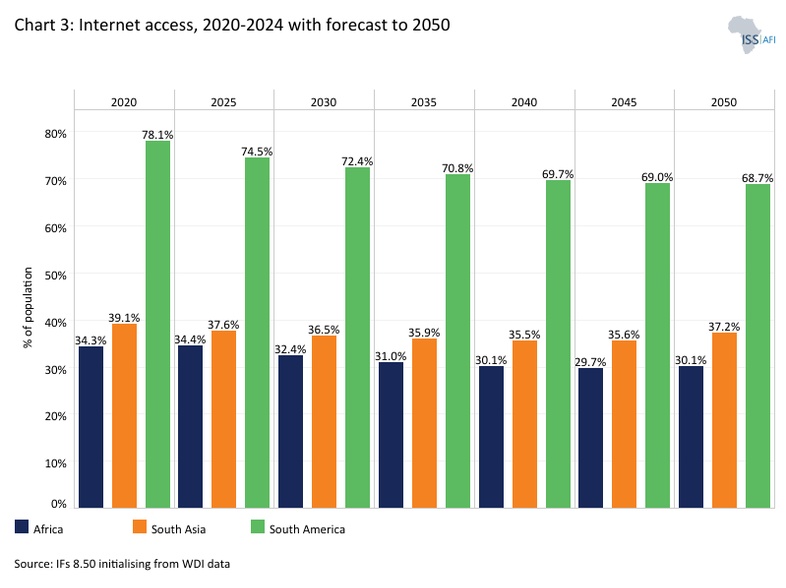

Chart 3 depicts the share of the population with internet from 2020 to 2024, with a forecast to 2050. Although internet penetration in Africa remains the lowest globally, at around 35% in 2024, it has increased rapidly from 7.5% in 2009. Much of this expansion has been driven by private-sector investment, underscoring Africa’s significant growth potential as a digital connectivity market. Broadband, as a general-purpose technology, has far-reaching economic effects: higher penetration is consistently linked to gains in GDP, productivity, market access and poverty reduction.

A study by GSMA (Global System for Mobile Communications Association) and the World Bank, using data from Nigeria, finds that just one year of mobile broadband coverage can increase total household consumption by around 6%, rising to 8% after two years. The impact on poverty is similarly significant: the share of households living below the extreme poverty line falls by about 4 percentage points after one year of coverage and by 7 percentage points after two or more years, effectively lifting roughly 2.5 million people out of extreme poverty.

Looking ahead, sustained investment in infrastructure, including undersea cables, satellite systems and next-generation mobile networks, will be essential. While 3G and 4G technologies still dominate in sub-Saharan Africa, the broader rollout of 5G networks promises substantial improvements in speed, capacity and innovation. Globally, more than 90% of people in high- and middle-income countries were covered by 4G and 5G in 2024, with 5G dominant in high- and upper-middle-income countries, reaching over two-thirds of the population. In contrast, 5G remains limited in low-income countries at just 4%.

Expanding both electricity access and internet connectivity will be critical to unlocking these opportunities. Africa’s growing digital ecosystem, anchored in mobile and broadband networks, provides a strong foundation for integrating emerging technologies such as AI, which can help extend services to underserved and rural areas, narrowing the digital divide. When countries combine technological adoption with investments in education, skills development and effective regulatory frameworks, leapfrogging can deliver significant economic, social and environmental benefits.

Access to formal financial services in Africa has historically been limited. Structural constraints, including shallow financial markets, macroeconomic volatility, weak credit infrastructure and the high cost of serving low-income populations, have made it difficult even for creditworthy individuals and small businesses to obtain loans. Traditional banking systems have struggled to scale across large, dispersed and predominantly informal economies.

Mobile and digital technologies have fundamentally altered this landscape. Across the continent, mobile telephony has enabled millions of previously unbanked individuals to access financial services such as payments, savings, credit and insurance, often without ever entering a physical bank branch. This transformation represents a clear case of technological leapfrogging, in which new technologies enable countries to bypass legacy systems and move directly into more advanced financial ecosystems.

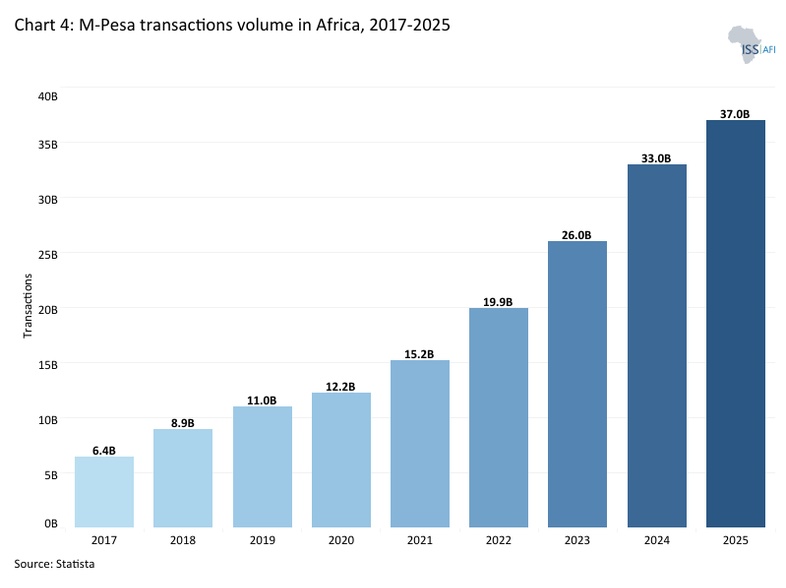

A pivotal innovation was M-Pesa, launched in Kenya in 2007. By enabling users to deposit, transfer and withdraw money with basic mobile phones, it created a scalable, accessible alternative to traditional banking. Chart 4 shows the trends in M-Pesa transaction volume in Africa from 2017 to 2025. By 2025, M‑Pesa, the mobile money service operated by Vodafone and Kenyan telecom provider Safaricom, had become a critical financial platform, enabling payments and other financial services even for customers without bank accounts. That year, M‑Pesa processed approximately 37 billion transactions, marking nearly a sixfold increase in transaction volume since 2017 and confirming its status as one of the world’s largest mobile money platforms.

The success of M-Pesa has catalysed the growth of a continent-wide mobile money industry. According to the GSMA State of the Industry Report 2025, sub-Saharan Africa continues to lead the world in mobile money adoption. The region has surpassed one billion registered mobile money accounts. It now counts over 280 million monthly active users, supported by a growing number of service providers and a rapidly expanding ecosystem. This reflects strong momentum across both East and West Africa, where mobile money has become deeply embedded in daily life, serving as the primary gateway to financial services for millions of people.

Sub-Saharan Africa also remains dominant in transaction value, with annual mobile money transactions exceeding US$1 trillion in 2025. This rapid increase underscores the region’s continued dependence on mobile money for payments, remittances, savings and business transactions. The sustained growth highlights not only rising adoption but also increasing usage intensity, reinforcing mobile money’s role as a cornerstone of financial inclusion and a key driver of the region’s digital economy.

Beyond finance, digital payment systems have become platforms for broader service delivery. In many African countries, utilities, including water, sanitation and electricity, have increasingly been digitised, allowing users to pay bills and schedule services via mobile platforms. In urban areas like Kampala, integrated systems combine call centres and mobile applications to improve service delivery in contexts where infrastructure gaps remain significant. Pay-as-you-go solar energy systems have similarly expanded, leveraging mobile payments to provide affordable electricity to low-income households.

Mobile money continues to play a significant role in boosting GDP, reducing poverty and enhancing economic resilience in countries where the service is available. In sub-Saharan Africa, its contribution to GDP increased from around US$150 billion in 2022 to US$190 billion in 2023, highlighting its growing impact on economic growth and financial inclusion. A recent study shows that access to M-Pesa increased per capita consumption levels and lifted 194 000 households, or 2% of Kenyan households, out of poverty. The impacts, which are more pronounced for female-headed households, appear to be driven by changes in financial behaviour, particularly increased financial resilience and saving, as well as labour market outcomes, such as occupational choice. This is true especially for women who moved out of agriculture and into business. Mobile money has therefore increased the efficiency of consumption allocation over time while allowing a more efficient allocation of labour.

Beyond poverty reduction, mobile money has helped households better manage shocks such as droughts, illness and income volatility by providing faster, more reliable access to funds. It has also promoted improved savings behaviour: secure digital storage of money has increased trust in financial systems and encouraged long-term financial planning. Some studies indicate that savings rates among mobile money users have risen by over 20%, demonstrating how digital financial services can strengthen both individual and household economic stability.

Despite these gains, important challenges remain, particularly in cross-border payments. While domestic mobile payment systems have scaled rapidly, international transfers within Africa remain slow, expensive and opaque. Efforts to address this fragmentation, including regional payment integration initiatives to link national systems and create interoperable platforms for cross-border transactions, could have a transformative potential. The IMF highlighted the possibility of interoperable digital payment systems, or even central bank digital currencies, that could enable near-instant, low-cost cross-border transfers. However, such innovations must balance technical efficiency with macroeconomic considerations, including capital flow management, exchange rate stability and monetary sovereignty. Most associated challenges could be overcome as part of implementing the African Continental Free Trade Area (AfCFTA), which is examined separately.

Digital finance has also had broader governance and social impacts. The use of mobile and internet technologies has improved transparency in public finance through tools such as Public Expenditure Tracking Surveys (PETS), which have historically revealed significant leakage in government spending across countries like Uganda, Tanzania and Ghana. Digitisation offers new opportunities to reduce corruption by improving traceability and accountability in public service delivery.

At the same time, risks have emerged. Mobile money platforms can be exploited for illicit financial flows, including fraud and the financing of criminal or extremist activities. Weak regulatory oversight in some jurisdictions has made monitoring difficult, highlighting the need for stronger financial regulation and cross-border cooperation.

Finally, mobile and internet technologies have influenced political processes. In countries such as Ghana, civil society organisations have used mobile phones and SMS-based systems to monitor elections, independently verify results and enhance transparency. These innovations have strengthened electoral credibility in tightly contested races and contributed to democratic resilience, although challenges persist in other contexts.

In sum, Africa’s fintech revolution illustrates how digital innovation can accelerate financial inclusion, economic transformation and institutional development. While significant regulatory, infrastructural and integration challenges remain, the continent’s experience demonstrates the powerful role of technology in enabling leapfrogging across multiple dimensions of development.

Africa has long been characterised by a large informal economy, which in many countries accounts for over 60% of employment and up to 40% of GDP. While this sector provides livelihoods for millions, it often operates outside formal financial and regulatory systems, limiting access to credit, savings, insurance and social protections.

A large informal sector not only affects productivity and incomes but also limits governments’ ability to generate domestic revenue. Because informal businesses and workers often operate outside official tax systems, they contribute little to VAT, corporate or income taxes. This constrains public budgets, reducing resources available for infrastructure, education, health and social protection programs.

Formalisation, therefore, has a dual benefit: it raises productivity while expanding the tax base. Digitisation and digital ID systems can help capture informal economic activity for taxation in a low-burden, efficient way. For example, mobile payment platforms and digital transaction records make it easier to monitor economic activity without imposing onerous compliance requirements on small-scale operators. Incremental formalisation strategies, such as PAYG models, can encourage participation without stifling entrepreneurial activity.

Chart 5 shows the informal sector’s share of GDP and its proportion of the total labour force in Africa from 2020 to 2024, with a forecast to 2050. In 2024, the informal sector accounted for approximately 27% of GDP and 58% of the total labour force, with projections indicating a gradual decline to 24% of GDP and 50% of the labour force by 2050.

Advances in internet access, mobile phones and digitisation do allow governments and businesses to reduce barriers between the informal and formal sectors, making it easier for informal businesses to access services, credit and markets. Traditionally, the informal sector naturally shrinks as GDP per capita rises. Still, modern technology, combined with supportive policies and incentives, can streamline and accelerate this transition by lowering costs, improving access to digital IDs, financial services and formal registration processes.

The introduction of digital ID systems is the critical first step toward formalisation. According to the World Bank, roughly half of the world’s one billion people without official identification live in Africa. Most African countries with stable governments now have active biometric ID programs, with South Africa and Nigeria among the most advanced, according to ID4Africa, an NGO promoting identity-for-all.

Digital IDs unlock access to banking, government benefits, education and other essential services. They enable precise identification of all parties to an interaction, low-cost communication and accurate, accountable, convenient payment processes. A McKinsey study across seven countries (Brazil, China, Ethiopia, India, Nigeria, the UK and the US) estimated that full digital ID coverage could unlock economic value equal to 3–13% of GDP by 2030, provided programs enable multiple high-value use cases and achieve widespread adoption.

A large informal sector also constrains African governments’ ability to mobilise domestic revenue. By gradually formalising the informal economy, governments can expand the tax base in a low-burden and efficient way. Digital payment systems, biometric IDs and mobile-based transaction records allow authorities to monitor economic activity without imposing heavy compliance costs on small-scale operators. This simultaneously supports economic growth, raises incomes and strengthens fiscal capacity.

Modern technology presents an unprecedented opportunity to formalise Africa’s informal sector incrementally. Digital ID systems, mobile payment solutions, PAYG models and carefully designed policies can collectively boost productivity and incomes, reduce poverty and inequality, expand access to financial and social services and strengthen domestic revenue mobilisation. By leveraging these tools, African governments can foster a more formal, inclusive and fiscally sustainable economy, unlocking long-term developmental gains for the continent.

Artificial intelligence (AI) is a branch of computer science dedicated to creating systems capable of performing tasks that typically require human intelligence. Although the concept dates back to the 1950s, AI capabilities have improved significantly in recent years due to the availability of massive amounts of data, better training data and more powerful computer hardware.

For instance, the global adoption of generative AI (GenAI), such as ChatGPT and CoPilot, has far outpaced previous technologies. While it took decades for inventions like the telephone (75 years), cars (33 years) and even the internet (7 years) to reach 100 million users, ChatGPT achieved this milestone in just two months. By June 2025, hundreds of AI tools were in use, with the top 60 attracting nearly 6 billion monthly visits. However, adoption remains uneven: by April 2025, 24% of internet users in high-income countries used ChatGPT, compared to just 5.8% in upper-middle-income countries, 4.7% in lower-middle-income countries and 0.7% in low-income countries.

AI represents the next frontier of technological leapfrogging in Africa, building on the continent’s rapid expansion of mobile and digital connectivity. With a growing digital ecosystem, favourable demographics and increasing data availability, Africa is well- positioned to harness AI to accelerate development.

The economic potential is substantial. More recent analysis by the African Development Bank indicates that inclusive AI deployment could generate as much as US$ 1trillion in additional GDP by 2035, nearly one-third of the continent’s current economic output, positioning AI as a major driver of productivity, economic growth and job creation across the continent. These gains are expected to be concentrated in high-impact sectors such as agriculture, retail, manufacturing, finance and healthcare, where AI can significantly enhance productivity and service delivery.

AI’s leapfrogging potential lies in its ability to bypass traditional constraints. In contexts where access to high-quality education, healthcare or extension services is limited, AI-powered tools can deliver low-cost, scalable solutions. For example, AI-enabled advisory systems can provide farmers with real-time guidance on crops, weather and market conditions, improving productivity and resilience. Similarly, AI applications in healthcare and education can expand access to diagnostics, personalised learning and decision support, particularly in underserved and remote areas. Beyond these sectors, AI can also help strengthen defence and security capabilities, particularly in surveillance, intelligence and decision-making, without going through costly traditional stages.

Importantly, AI can also help overcome some of the structural barriers that have limited internet use in Africa. Pilot studies show that AI-based tools, such as chatbots accessible on basic mobile platforms, can deliver relevant information more efficiently and at significantly lower data costs than traditional web searches. This makes AI particularly well-suited to low-connectivity environments, where affordability and data constraints remain major barriers to digital inclusion.

A particularly promising area is public sector transformation, especially in tax administration. In South Africa, for example, artificial intelligence is significantly enhancing tax compliance through the work of the South African Revenue Service (SARS), which has adopted data-driven technologies to modernise its operations. By integrating vast datasets from employers, financial institutions and other third parties, SARS uses AI and advanced analytics to automatically detect discrepancies, identify high-risk taxpayers and prioritise audits with greater precision. These systems rely on techniques such as predictive analytics, data matching and pattern recognition to uncover previously hidden forms of tax evasion, while also enabling the pre-population of tax returns and real-time compliance monitoring. As a result, AI is shifting the tax system from reactive enforcement to proactive compliance, improving efficiency, reducing fraud and strengthening revenue collection.

These innovations highlight the AI leapfrogging potential in Africa. Many countries on the continent face similar challenges in tax collection, including informality, limited administrative reach and weak data systems. By adopting AI-enabled solutions, African governments can bypass slower, traditional reforms and move directly to more efficient, data-driven systems. This can significantly enhance domestic revenue mobilisation, which is critical for financing development priorities.

However, realising this potential depends on addressing key enabling factors. These include access to data, computing infrastructure, digital skills, investment and regulatory frameworks. While adoption is growing, more than 40% of African institutions have begun experimenting with AI, deployment remains uneven across countries and sectors. Significant gaps persist in infrastructure, education and governance, which risk widening existing inequalities if not carefully managed.

A growing number of continental initiatives are already emerging to operationalise this potential. Notably, the African Development Bank Group and the United Nations Development Programme (UNDP), through the AI Hub for Sustainable Development, have launched the AI 10 Billion Initiative, a major effort to accelerate responsible AI adoption and inclusive digital growth across Africa. Announced at the Nairobi AI Forum 2026, the initiative aims to mobilise up to US$10 billion by 2035 to support investments in AI infrastructure, entrepreneurship, policy frameworks and skills development. By focusing on building foundational enablers and scaling practical applications, the initiative seeks to unlock up to 40 million jobs while ensuring that AI-driven transformation is anchored in trust, local value creation and broad-based development impact.

Looking ahead, AI could act as a powerful general-purpose technology, amplifying the benefits of earlier digital investments in mobile and broadband networks. As connectivity expands and electricity access improves, AI systems can be deployed more widely to support innovation across sectors. When combined with investments in human capital, local innovation ecosystems and inclusive policies, AI has the potential to enable Africa not only to catch up but in some areas to leap ahead, driving productivity, creating new industries and supporting more inclusive and sustainable development.

There are also many other leapfrogging opportunities arising from technologies that provide alternatives to the costly infrastructure required by traditional development pathways. For instance, drones offer a powerful opportunity to advance precision agriculture in developing countries by enabling farmers to better monitor and respond to variations in crop and livestock production. Compared with conventional remote-sensing systems, drones provide more affordable, accessible agronomic data.

An example is the Third Eye project in Mozambique, where low-cost drones helped smallholder farmers increase crop yields by 41% while reducing water use by 9%. These outcomes highlight the systemic nature of innovation, combining not just the technology itself but also the training of local drone operators, effective communication of agronomic insights and the widespread use of mobile phones.

Beyond agriculture, drones can also transform logistics and service delivery in hard-to-reach areas. In Rwanda, the government partnered with the company Zipline to use drones to deliver blood to medical facilities, cutting delivery times from 4 hours to just 15 minutes and helping address maternal mortality.

In Bangladesh, the Internet of Things is being used to assess groundwater chemistry and protect people in the Ganges Delta from drinking water that is contaminated with arsenic. This lessens the need for investments in the implementation and maintenance of traditional monitoring networks. Small-scale satellites are used in communication networks and applications that rely on high-resolution imagery for land-use monitoring and urban planning. These satellites will soon be affordable for more developing countries, businesses and universities, diminishing the need for investment in more costly and traditional satellite technologies. These examples highlight the potential for leapfrogging by adopting technologies developed elsewhere.

This section outlines the structure of the Large Infrastructure and Leapfrogging scenario, which presents a more optimistic pathway for human development in Africa compared to the Current Path. In this scenario, the pace and scale of progress are broadly benchmarked against the historical and ongoing development trajectories observed in South Asia and South America. The same scenario is also applied in the theme on large infrastructure and is illustrated in Chart 6.

The Large Infrastructure and Leapfrogging scenario highlights the transformative potential of African governments fully harnessing new technologies and the digital economy to drive development outcomes. It underscores how strategic investments and policies that embrace innovation can accelerate progress, enhance productivity, and deliver broad-based social and economic benefits across the continent.

The first set of interventions models a faster transition to a modern energy system, reflecting the kind of accelerated adoption seen in parts of these benchmark regions. This includes greater reliance on solar and wind power, improved energy storage and the deployment of intelligent, decentralised power systems such as micro-, mini- and off-grid solutions. In practical terms, the scenario assumes increased renewable energy production and reduced transmission losses. Together, these changes represent a rate of technological progress that outpaces the Current Path within the IFs modelling platform.

The next step focuses on expanding electricity access in both rural and urban areas, aiming to mirror the gains achieved in South Asia and South America over recent decades. Under this scenario, electricity access improves significantly across income groups by 2050. An average of 15 percentage points above the Current Path in low-income countries, seven percentage points in lower-middle-income countries and about two percentage points in upper-middle-income countries, although outcomes vary widely between countries. This pattern largely reflects differences in starting points, with low-income countries improving more rapidly because they begin from a much lower base of electricity access.

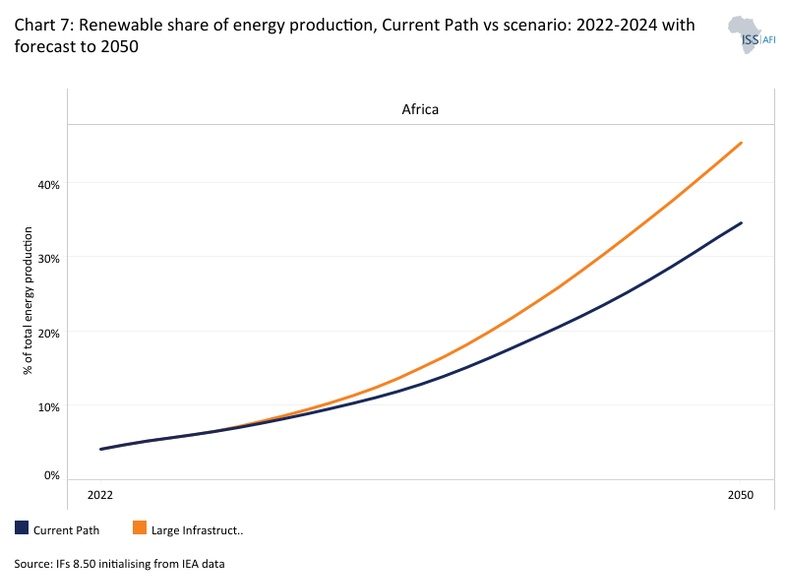

As a result, by 2050, 89.5% of Africans will have access to electricity, compared to 79% under the Current Path. The number of people without electricity will decline from 543 million to 273 million in the Large Infrastructure and Leapfrogging scenario. In other words, the scenario interventions reduce the number of unserved people by almost half. Chart 7 depicts the renewable share of energy production in the Current Path versus the scenario from 2020 to 2024, with a forecast to 2050. Renewable energy production increases substantially. The share of renewable energy in total energy production will reach 45% by 2050, compared with 34% under the Current Path in the same year.

The Large Infrastructure and Leapfrogging scenario significantly accelerates progress in internet connectivity, particularly in fixed broadband adoption. Under this scenario, fixed broadband subscriptions rise to 47 per 100 people by 2050, well above the 29 per 100 projected under the Current Path. At this level, Africa would be broadly aligned with projected rates in South America and notably ahead of South Asia. This marks a meaningful step in narrowing the gap with other developing regions, especially in high-capacity fixed-line connectivity that supports data-intensive applications. Higher fixed broadband penetration and faster internet speed are among the key factors that predict higher AI adoption.

The Large Infrastructure and Leapfrogging scenario increases mobile broadband penetration to 151 subscriptions per 100 people, only marginally higher than the 149 per 100 projected under the Current Path. While this still places Africa roughly on par with South America, the small difference suggests that mobile broadband is already approaching saturation under baseline trends, leaving less room for rapid acceleration.

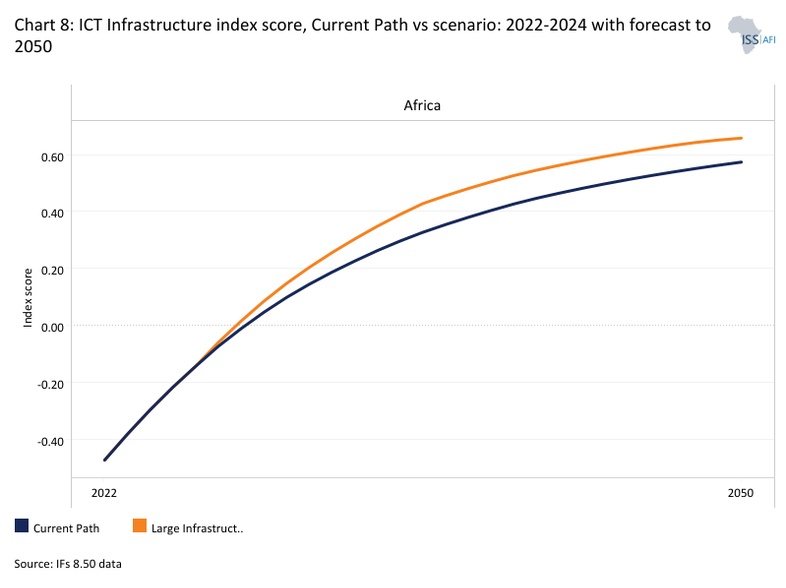

These connectivity gains translate into a stronger ICT sector overall. Chart 8 shows internet access in the scenario versus the Current Path from 2020 to 2024, with a forecast to 2050. Africa’s score on the IFs ICT infrastructure index rises to 0.66 (out of a maximum of 1) by 2050, compared to 0.56 under the Current Path. In economic terms, ICT value added will be US$233 billion higher than in the Current Path, equivalent to about 1.75 percentage points of GDP. Even so, the sector remains relatively modest, accounting for roughly 8% of the continent’s GDP.

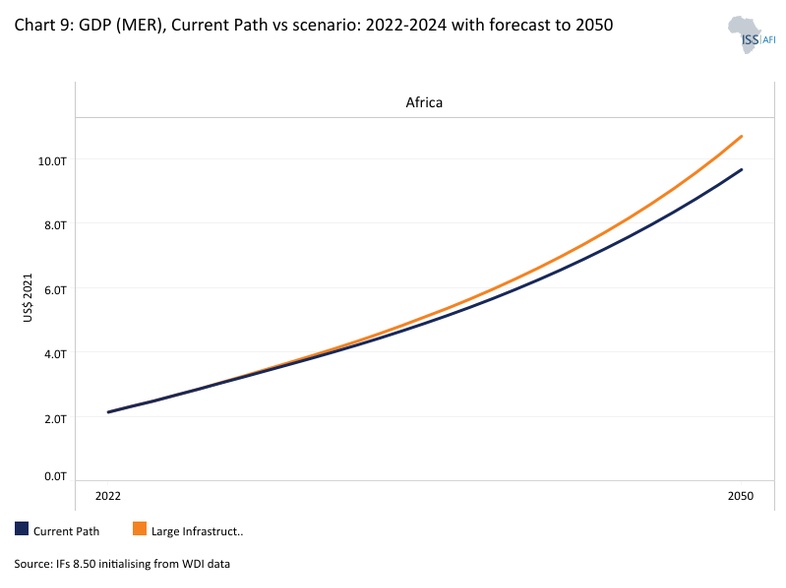

Chart 9 presents the size of Africa’s economy from 2020 to 2024, with a forecast to 2050. Under the Large Infrastructure and Leapfrogging scenario, Africa’s economy will expand at an average annual rate of about 6% between 2027 and 2050, one percentage point faster than the 5% growth projected under the Current Path over the same period. This performance will result in a substantially larger economy, with total GDP nearly US$1 trillion (US$948 billion in 2017 dollars) higher by 2050 compared to the baseline.

While all countries will experience gains relative to the Current Path, the largest economies, including Nigeria, Egypt and South Africa, will record the most pronounced increases in absolute terms.

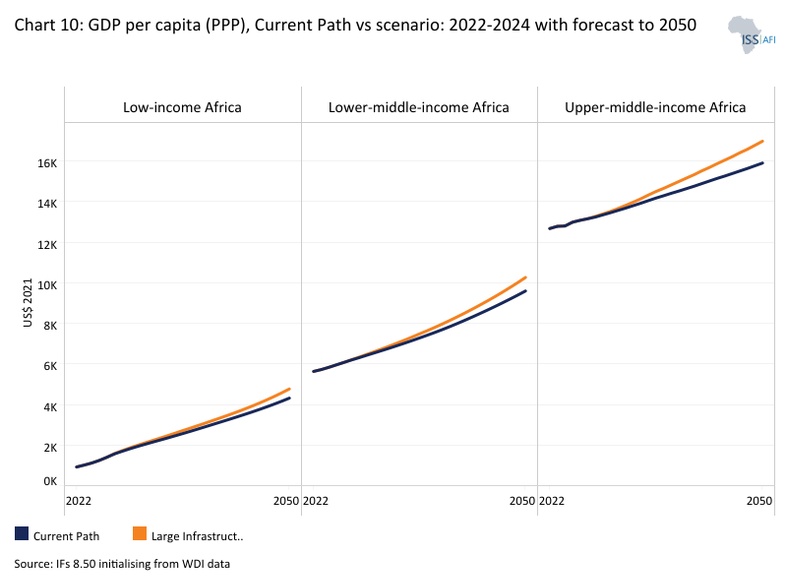

Chart 10 shows GDP per capita from 2020 to 2024, with a forecast to 2050. By 2050, Africa’s average GDP per capita (at purchasing power parity) will be approximately US$510 higher in the Large Infrastructure and Leapfrogging scenario than under the Current Path. This represents a significant gain, especially given that the continent’s population is expected to exceed 2.5 billion by that year.

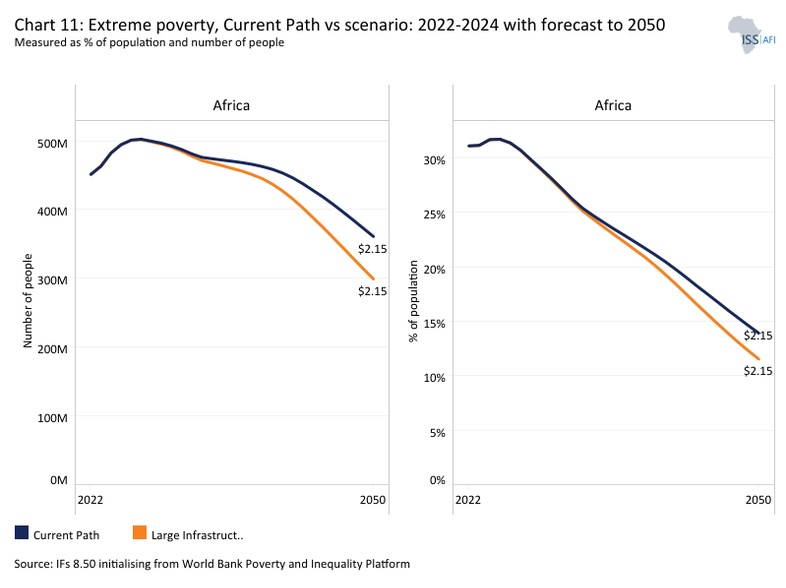

Chart 11 depicts the extreme poverty rate from 2020 to 2024, with a forecast to 2050. The Large Infrastructure and Leapfrogging scenario shows how these innovations, combined with improved energy and transport infrastructure, can lift millions out of extreme poverty. By 2050, the number of people living in poverty will fall to 299 million, 63 million fewer than under the Current Path. This will reduce the poverty rate to 11.5%, 2.4 percentage points lower than the baseline. Low-income countries will see the largest gains, with 38.6 million fewer people in extreme poverty, followed by lower-middle-income countries with 23 million fewer. Countries with large poor populations, including DR Congo and Nigeria, will experience the biggest absolute reductions. These outcomes demonstrate that technological leapfrogging and strategic infrastructure development not only drive economic growth and expand opportunities but also directly translate into measurable improvements in human development, lifting millions out of poverty and promoting more inclusive economic prosperity across Africa.

This report explored Africa’s potential to leverage technological adoption for transformative development, beginning with the concept of leapfrogging, bypassing traditional stages of industrial and infrastructural development. Examples range from mobile phone adoption replacing landlines to the use of renewable energy instead of fossil fuels, illustrating both stage-skipping and path-creating opportunities. By embracing these approaches, Africa can address critical development gaps without replicating the incremental trajectories of developed countries.

In interpreting these results, the reader is reminded about the caveat included in the introduction, namely that the modelling in this theme does not do justice to the full impact of new technologies. The impact of advances in health for example, is modelled and included as outcomes there since advances in medical technology, for instance, could substantially reduce the burden of malaria, HIV, tuberculosis and other prevalent diseases. Similarly regarding education, manufacturing, financial flows and even governance. The real effect of leapfrogging is, therefore, dispersed across various themes and only fully captured in the Combined scenario to the degree that we can estimate the extent to which new technologies will effect Africa’s future.

Even then, realising its potential requires deliberate policy and strategic action. Leapfrogging is not the mere imitation of high technology; it is a process of sequential learning, capacity-building and innovation. African countries must develop the capability to adapt, improve and ultimately create new technologies, navigating global intellectual property regimes to ensure that growth is locally driven.

Digital technologies offer unprecedented opportunities to accelerate development in energy, health, infrastructure and beyond. Yet the benefits will only materialise if governments combine technological adaptation with effective governance, transparent regulations and open markets. Ironically, restrictive policies, such as internet shutdowns in many African countries during elections, pose a greater threat to leapfrogging than any technological constraint, highlighting the importance of enabling, rather than stifling, innovation.

Leapfrogging requires more than regulatory leniency; it demands flexibility, experimentation and active engagement between policymakers, entrepreneurs and technologists. Strategic industrial and innovation policies must facilitate the development and deployment of frontier technologies, build local capacities and ensure that Africa produces, rather than merely consumes, advanced technologies.

To accelerate technological leapfrogging in Africa, policymakers must adopt a coordinated and inclusive strategy that simultaneously addresses infrastructure gaps, institutional weaknesses and human capital constraints. Evidence from institutions such as the World Bank demonstrates that while digital technologies are already transforming finance, employment and service delivery across the continent, their full potential remains constrained by structural bottlenecks. Effective policy must therefore focus not only on expanding access to technology but also on ensuring that its benefits are widely shared and sustainably embedded in local economies.

A foundational priority is expanding reliable digital and energy infrastructure. Technological leapfrogging depends critically on widespread access to affordable internet and consistent electricity, yet large segments of the population, particularly in rural areas, remain underserved. Governments should prioritise investments in broadband networks and support the scaling of decentralised energy solutions such as minigrids, which have proven effective in reaching off-grid communities. By fostering public-private partnerships and reducing barriers to infrastructure investment, states can create the enabling environment necessary for digital services, mobile finance and AI applications to flourish. Without these foundational systems, higher-level technological innovations cannot scale effectively.

At the same time, strengthening digital financial ecosystems is essential for enabling inclusive economic participation. Mobile money has already become a cornerstone of financial inclusion in Africa, supporting everything from household resilience to small business operations. However, to move beyond basic transactions, policymakers must promote interoperability across providers, expand access to savings and credit products and integrate digital payments into government services. Leveraging digital finance for social protection programs can further enhance efficiency, reduce corruption and increase trust in digital systems. A mature digital financial ecosystem not only facilitates commerce but also underpins broader digital transformation.

Equally important is the need to support informal digital entrepreneurship. As observed in the widespread use of social media platforms for commerce, small merchants are already leveraging accessible technologies to participate in digital markets without relying on formal e-commerce infrastructure. Rather than attempting to replace these systems, policy should aim to strengthen them by improving access to finance, building trust mechanisms and investing in logistics and delivery networks. Providing targeted training in digital skills and business management can help informal enterprises transition from survival-oriented activities to scalable ventures. Recognising and supporting this form of grassroots innovation is critical for ensuring that leapfrogging is inclusive and grounded in existing economic realities.

Human capital development represents another central pillar of effective policy. The transition to a digital and AI-driven economy requires a workforce equipped with both basic digital literacy and advanced technical skills. Reports from the World Bank highlight the growing demand for such competencies and the risks of exclusion for those without them. Governments must therefore reform education systems to integrate digital skills at all levels, while also investing in vocational training, STEM education and specialised programs in data science and artificial intelligence. Particular attention should be given to closing gender and rural-urban gaps in access to education and technology, as failure to do so could exacerbate existing inequalities.

In parallel, the development of inclusive and secure digital identification systems is crucial for improving governance and service delivery. Digital ID can enable more accurate targeting of social programs, reduce fraud and facilitate access to financial services. However, as research underscores, poorly designed systems risk excluding vulnerable populations and undermining trust. Policymakers must therefore ensure universal access, incorporate robust data protection frameworks and provide alternative mechanisms for those unable to enrol digitally.

Looking ahead, enabling the responsible development and deployment of artificial intelligence will be key to sustaining long-term leapfrogging. AI offers significant potential to address sectoral challenges in agriculture, healthcare, finance and climate adaptation. Still, its adoption in Africa is constrained by limited data availability, weak infrastructure and skills shortages. Governments should invest in local data ecosystems, including the development of datasets that reflect African languages and contexts, and support research institutions and innovation hubs. Establishing clear regulatory frameworks that promote ethical AI use without stifling innovation will be essential for fostering trust and encouraging investment. Importantly, AI strategies should prioritise applications that deliver tangible social and economic benefits, rather than replicating models from advanced economies that may not align with local needs.

Finally, improving the overall regulatory and business environment is necessary to unlock private sector participation and innovation. Across sectors, from fintech to energy, complex and inconsistent regulations continue to hinder growth. Policymakers should streamline licensing processes, adopt regulatory sandboxes to test new technologies and harmonise policies across regions to facilitate cross-border digital markets. By creating a predictable and supportive regulatory environment, governments can attract investment, encourage competition and accelerate the scaling of successful innovations.

In sum, Africa’s ability to leapfrog hinges on a proactive, integrated and inclusive approach. By aligning technological innovation with development priorities, African countries can not only narrow the gap with developed nations but also pioneer new models of sustainable and inclusive growth. Leapfrogging presents both a challenge and an opportunity; pursued strategically, it can unlock rapid growth, alleviate poverty and empower the continent to shape its own technological and economic future.

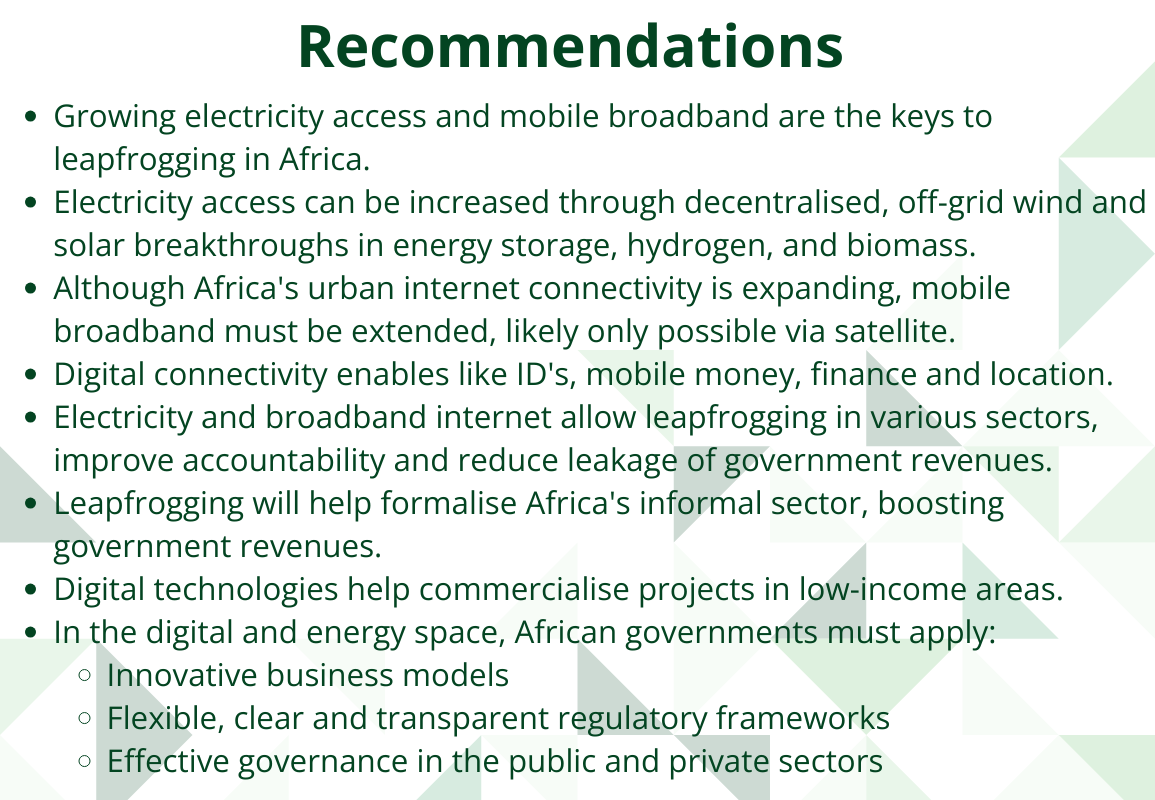

Chart 12 summarises the policy recommendations.

Governments in Africa should:

1. Expand digital and energy infrastructure:

- Scale broadband networks and mobile connectivity, prioritising rural and underserved areas.

- Integrate reliable electricity access through decentralised, renewable energy solutions, including off-grid and mini-grid systems, to ensure digital technologies function effectively.

- Promote infrastructure sharing, spectrum management, and efficient permitting to reduce deployment costs and expand reach.

2. Improve affordability and access to technology:

- Reduce taxes and tariffs on digital devices and internet services.

- Support targeted subsidies, shared internet access points and innovative financing to make connectivity and devices accessible to low-income households.

- Ensure programs prioritise the poorest and most vulnerable populations to prevent the digital divide from deepening poverty.

3. Invest in human capital and digital skills:

- Reform education and vocational programs to strengthen digital literacy, STEM skills and AI competencies.

- Launch community-level digital literacy initiatives to improve adoption among rural and low-income populations.

- Target efforts to reduce gender and rural–urban disparities in digital skills.

4. Strengthen financial inclusion and digital entrepreneurship:

- Promote interoperable mobile money, digital savings, credit and social transfer systems to empower households and small businesses.

- Support informal and small enterprises with access to finance, logistics, digital tools, skills training and trust-building mechanisms to drive grassroots innovation.

5. Develop inclusive digital systems and AI governance:

- Implement secure, privacy-conscious and universally accessible digital ID systems to expand access to financial services and public programs.

- Foster responsible AI adoption through local data ecosystems, innovation hubs and ethical regulatory frameworks, focusing on sectors such as agriculture, health, finance and climate adaptation.

6. Create an enabling regulatory and investment environment:

- Streamline licensing and regulatory processes to reduce barriers to network and service deployment.

- Harmonise policies, maintain regulatory stability and promote fair competition.

- Liberalise foreign investment to attract capital and stimulate private sector innovation.

Page information

Contact at AFI team is Kouassi Yeboua

This entry was last updated on 25 May 2026 using IFs v8.50.

Donors and sponsors

Reuse our work

- All visualizations, data, and text produced by African Futures are completely open access under the Creative Commons BY license. You have the permission to use, distribute, and reproduce these in any medium, provided the source and authors are credited.

- The data produced by third parties and made available by African Futures is subject to the license terms from the original third-party authors. We will always indicate the original source of the data in our documentation, so you should always check the license of any such third-party data before use and redistribution.

- All of our charts can be embedded in any site.

Cite this research

Kouassi Yeboua (2026) Africa Leapfrogging Futures. Published online at futures.issafrica.org. Retrieved from https://futures.issafrica.org/thematic/09-leapfrog/ [Online Resource] Updated 25 May 2026.