Sudan

Sudan

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This report analyses Sudan’s current development path and prospects, examining how various sectoral interventions could shape the country’s economic and social landscape through to 2043, the end of the third ten-year implementation plan of the African Union’s Agenda 2063. Grounded in scenario modelling, the analysis explores eight key sectors and assesses their individual and combined impact on Sudan’s long-term growth and development trajectory. It does so in the context of a country whose strategic location, natural resources and youthful population are constrained by conflict, institutional fragility and economic underperformance. The report concludes by summarising the key findings and offering policy insights to support Sudan in moving from crisis toward recovery and a more inclusive, resilient and sustainable future.

Visit the Technical section for additional information on the International Futures (IFs) modelling platform, which serves as the analytical foundation for this report’s scenario simulations.

Executive Summary

We begin this page with an introduction and context to Sudan.

- Straddling and connecting north, east and central Africa, Sudan is the third-largest country in Africa after Algeria and DR Congo, with a land area of approximately 1 868 000 square kilometres. It shares borders with seven neighbouring countries, including Libya, Chad, the Central African Republic, Eritrea, Ethiopia, South Sudan and Egypt.

- Sudan’s maritime access to the Red Sea has the potential to serve as a logistical hub for countries in East Africa and as a gateway to landlocked countries in Central Africa. This geographical setup offers development opportunities through trade and regional integration. However, it has also brought geopolitics into a region with a long history of destabilisation, external interference, persistent intra-state conflict and proxy efforts, most notable in the context of the ongoing war.

The introductory section is followed by an analysis of the Current Path for Sudan, which informs the region’s likely current development trajectory to 2043, mostly comparing Sudan with its low-income peers in Africa. It is based on current developmental trends and assumes that no major shocks would occur in a ‘business-as-usual’ future.

- Sudan is the eighth-most populous country in Africa, the fourth-most populous country in East Africa after Ethiopia, Tanzania and Kenya, and the 30th globally. The Sudanese population is estimated at 52 million people, more than double the 22 million in 1990. The total population increased from 22 million in 1990 to 52 million in 2022, and by 2043, it will be 81.7 million. In terms of population structure, Sudan has a youthful and dependent population. In 2023, 57.2% of Sudanese were under the age of 15, 41.3% were in the 15–64 age group (working age), and 3.4% were 65 years and older.

- Sudan has urbanised rapidly over the years, such that the urban population stood at 35.3% in 2023, making Sudan the 13th most urbanised country among low-income African countries. On the Current Path, Sudan's urban population will grow modestly, reaching 42.8% by 2043

- The Sudanese economy revolves around the export of oil. Its GDP measured in market exchange rates (MER) tripled from US$15.7 billion in 1990 to US$45.4 billion in 2010 before the secession of South Sudan. In 2023, Sudan’s GDP stood at US$32.4 billion, a contraction of 12% from the previous year and is projected to reach US$38.9 billion by 20243.

- Sudan has a large informal sector that is vital to its economy. In 2023, the informal sector accounted for approximately 14% of GDP, below the average of 32% for its income peers in Africa. In the Current Path, the size of the informal sector will largely remain the same, even reaching 14.7% of GDP by 2043. The large contrast between its labour force share and contribution to GDP reflects the underlying low productivity, wages and inefficiency that characterise the sector.

- Since South Sudan's secession, Sudan has generally experienced a downward trend, with its GDP per capita dropping from US$4 884 in 2011 to US$2 961 in 2023. By 2043, Sudan’s GDP per capita will rise to US$2 998, indicative of a slower growth in GDP per capita

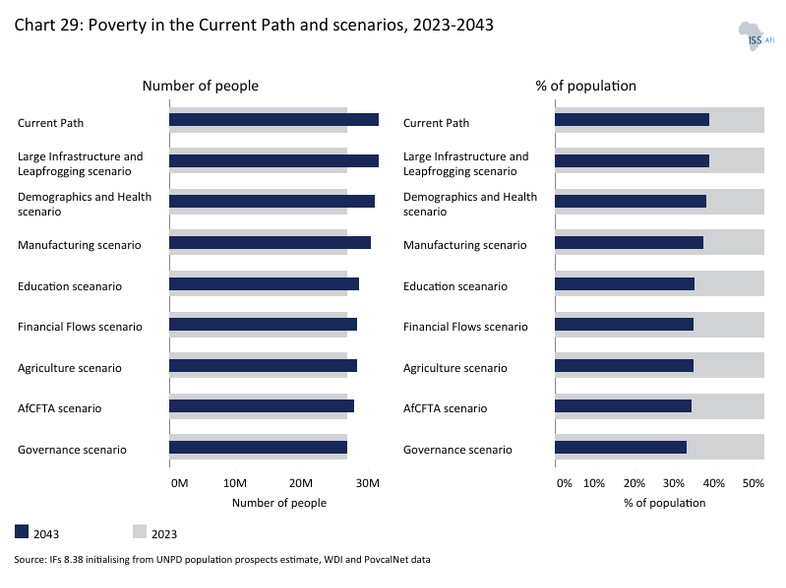

- Like many low-income countries in Africa, poverty in Sudan is widespread. In 2023, 22.8 million Sudanese, representing 45% of the population, lived below the poverty line of US$2.15 per day, above the average of 41.5% for low-income countries in Africa. By 2043, the poverty rate of 38.8% (equivalent to 31.7 million people) means that Sudan will miss the Sustainable Development Goal 1 target, which can only be met in 2088.

The next section compares progress on the Current Path with eight sectoral scenarios . These are Demographics and Health; Agriculture; Education; Manufacturing; the African Continental Free Trade Area (AfCFTA); Large Infrastructure and Leapfrogging; Financial Flows; and Governance. Each scenario is benchmarked to present an ambitious but reasonable aspiration in that sector.

- Sudan’s rapidly growing population constrains potential improvements in income. The Demographics and Health scenario will reduce the infant mortality rate from 41.9 deaths per 1 000 births in 2023 to 25.5 deaths by 2043, 14 deaths fewer than in the Current Path. The scenario pushes the ratio of the working-age population to 1.4 working-age persons to one dependants by 2043, close to the ratio of 1.7 to one that is required to enter a potential demographic window of opportunity.

- In 2022, Sudan’s net import of crops stood at 12.4% of total crop demand, which was less than the average of 7.9% for low-income countries in Africa. Sudan will reduce its crop import dependency, so that by 2043, the net crop import share will reach 25% in the Agriculture scenario instead of the 45.9% in the Current Path.

- In 2023, the mean years of education attained by adults between 15 and 24 years in Mali stood at 5.3 years — slightly below the average of 5.9 years for low-income countries on the continent. In the Education scenario, the mean years of adult education will rise to 7.6 years by 2043, 1.7 years more than the Current Path. By 2043, the scenario further increases average test scores for primary and secondary school students by 33.7% and 41.4%, respectively, significantly closing the gap with its income peers.

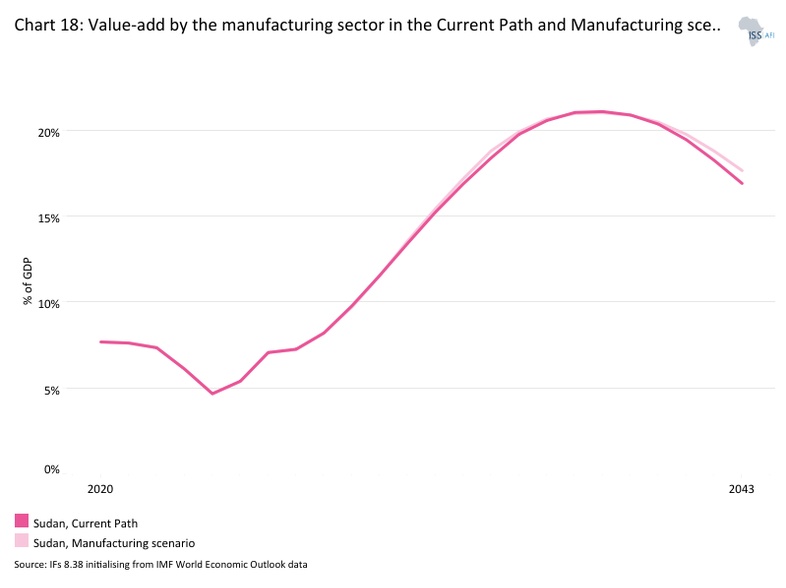

- In the Manufacturing scenario, Sudan makes substantial progress in industrialisation such that, by 2043, the share of the manufacturing sector in GDP is about 17.6%, equivalent to US$7.0 billion, which will be about US$439 above the Current Path.

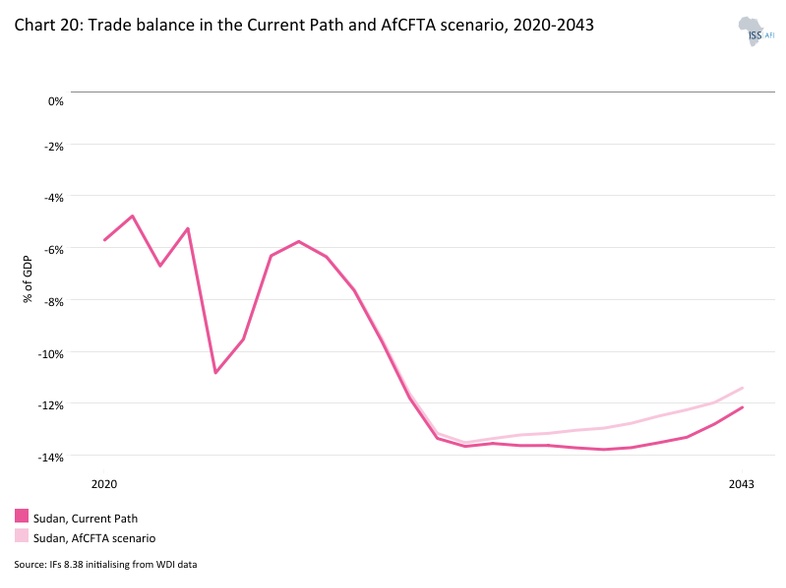

- In the African Continental Free Trade Area (AfCFTA) scenario, Sudan’s trade deficit will constitute about 11.4% of GDP by 2043 instead of the 13.6% of GDP on the Current Path.

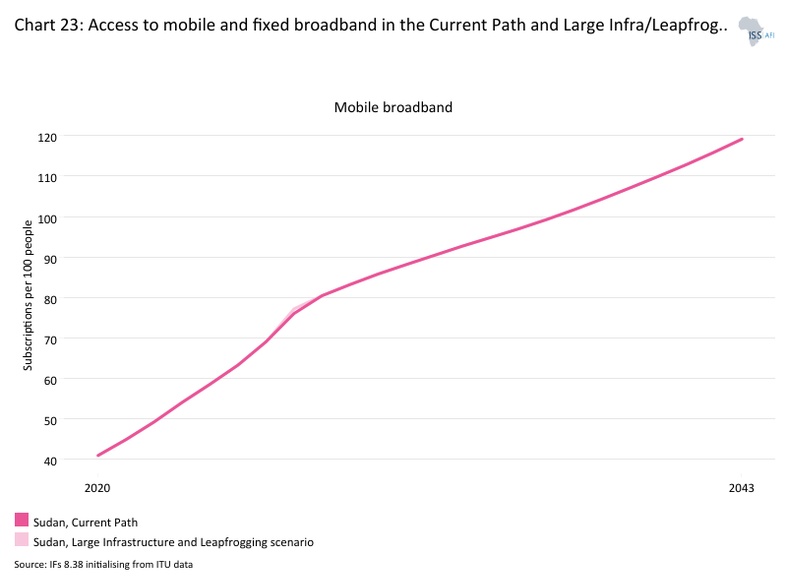

- Based on the Large Infrastructure and Leapfrogging scenario, 67.7% of Sudanese will have access to electricity by 2043. As a result, 28.0% of households in Sudan will use modern fuel for cooking in the Large Infrastructure and Leapfrogging scenario. The scenario will further lead to a larger increase in fixed and mobile broadband access, so that, by 2043, subscriptions will likely be at 21.1 and 127.4 per 100 people, respectively.

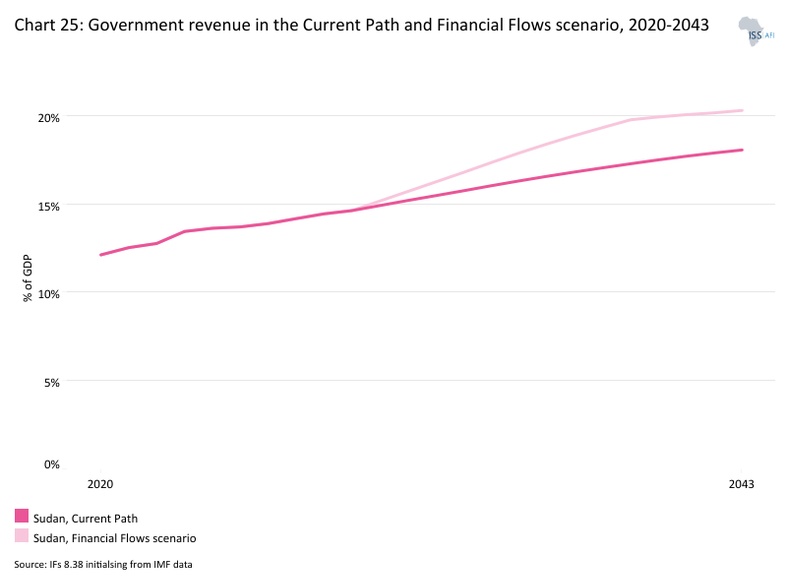

- In 2022, the government’s total revenue in Sudan amounted to US$3.1 billion, equivalent to 12.8% of GDP — lower than the average of its income-group peers in Africa. Compared to the Current Path, the Financial Flows scenario will improve government revenue in Sudan by an additional US$1.3 billion by 2043.

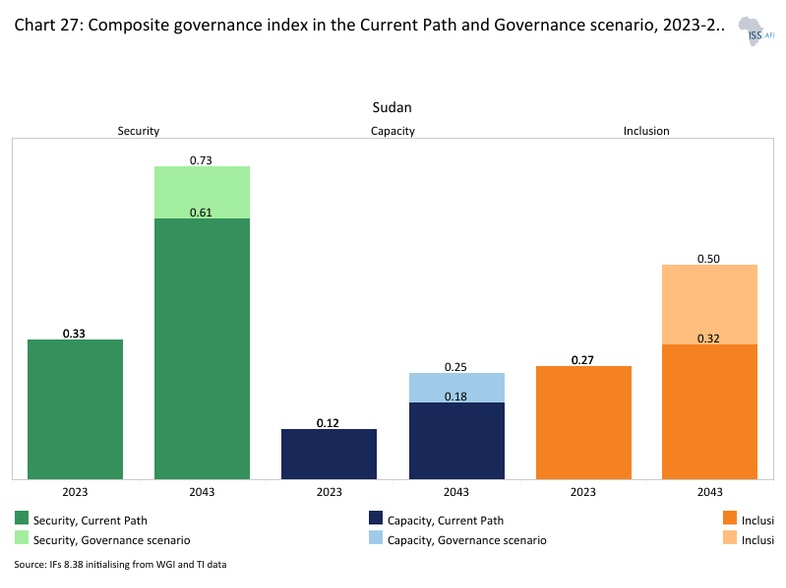

- Generally, Sudan performs poorly on governance indices compared to its income peers in Africa. Sudan’s score on the composite governance index of 0.23 in 2023 was 55% of the average for its income peers in Africa. In the Governance scenario, Sudan's score on the composite governance index will improve to 0.50, which is about 34% above the Current Path by 2043.

In the third section, we compare the impact of each of these eight sectoral scenarios with one another and subsequently with a Combined scenario (the integrated effect of all eight scenarios). In our forecasts, we measure progress on various dimensions such as economic size (in market exchange rates), gross domestic product per capita (in purchasing power parity), extreme poverty, carbon emissions, the changes in the structure of the economy and selected sectoral dimensions such as progress with mean years of education, life expectancy, the Gini coefficient or reductions in mortality rates.

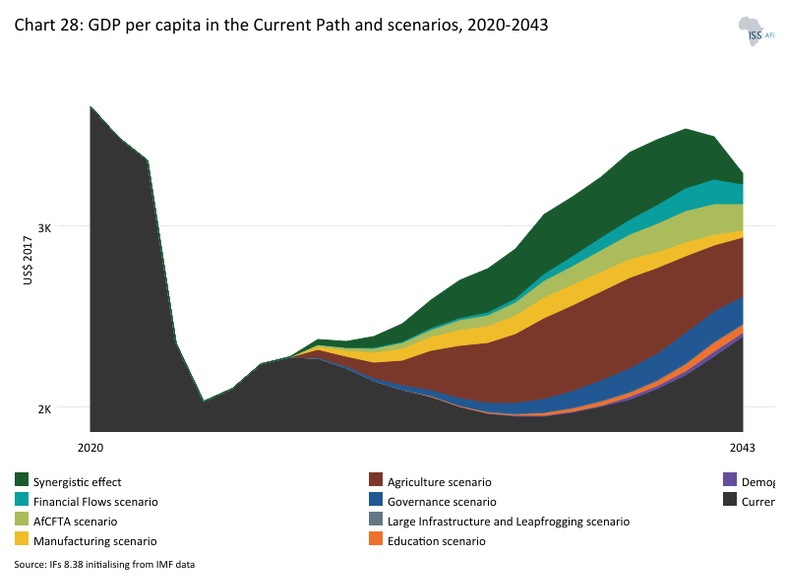

- The scenarios with the greatest impact on GDP per capita in Sudan by 2043 will be the Agriculture scenario, followed by the Governance, the AfCFTA and the Financial Flows scenarios. Regarding poverty reduction, the Governance scenario has the greatest impact, followed by the Agriculture, AfCFTA, and Financial Flows scenarios. These four sectors are the most critical for raising living standards and eradicating poverty in Sudan.

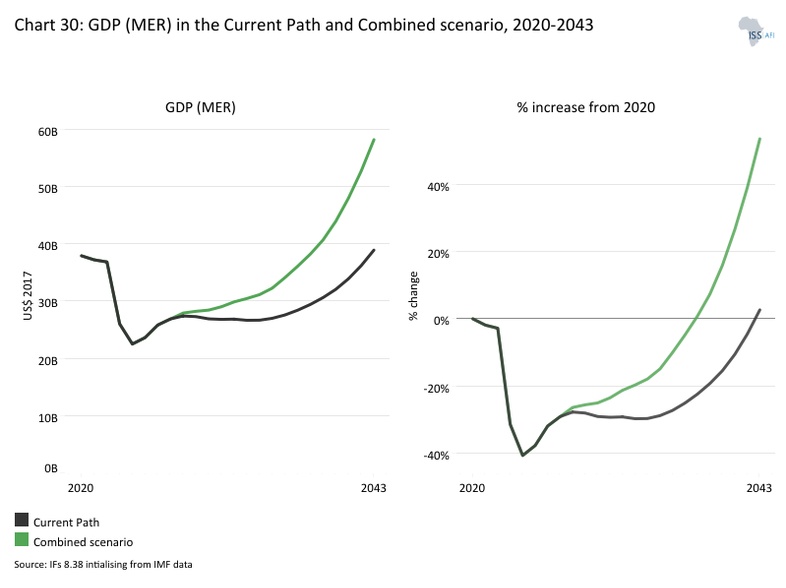

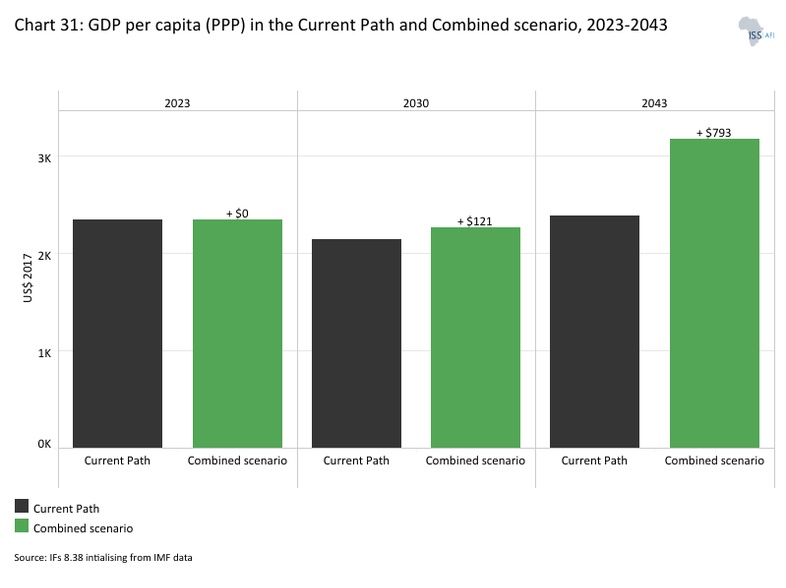

- In the Combined scenario, Sudan’s GDP will rise to US$58.2 billion, exceeding the Current Path by US$19 billion. Similarly, in the Combined scenario, GDP per capita will increase to US$3 176 by 2043. This will be US$792 more than the Current Path.

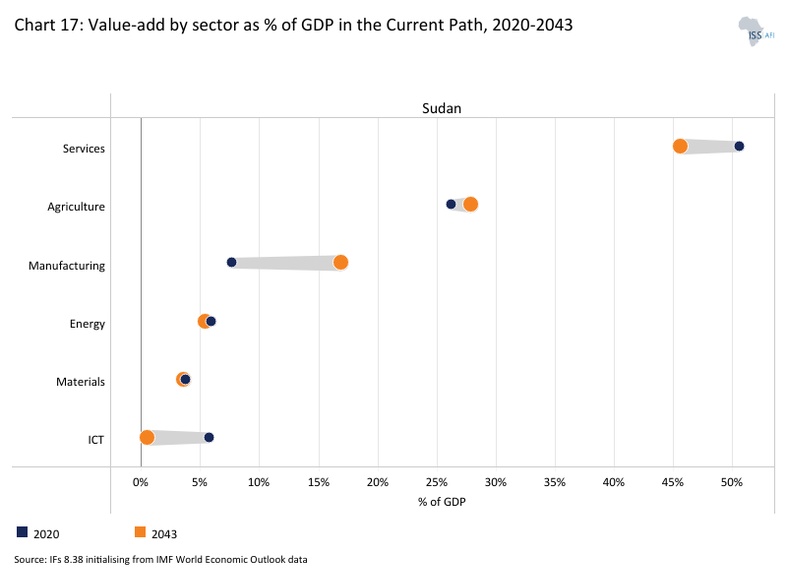

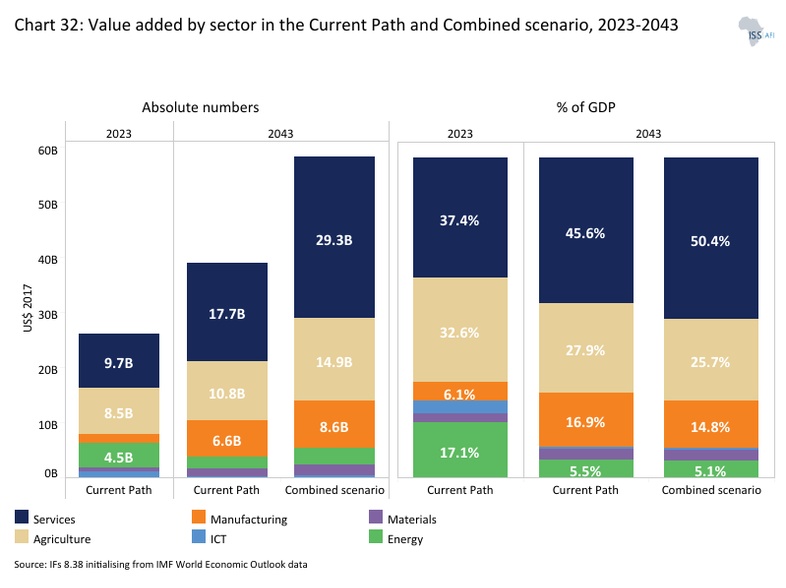

- By 2043, the services sector will still be the largest contributor to GDP at 50.4%. The agriculture sector will be the second-largest contributor to GDP in the scenario by 2043 with a share of 25.7%. The share of the manufacturing sector will decline to 14.8%.

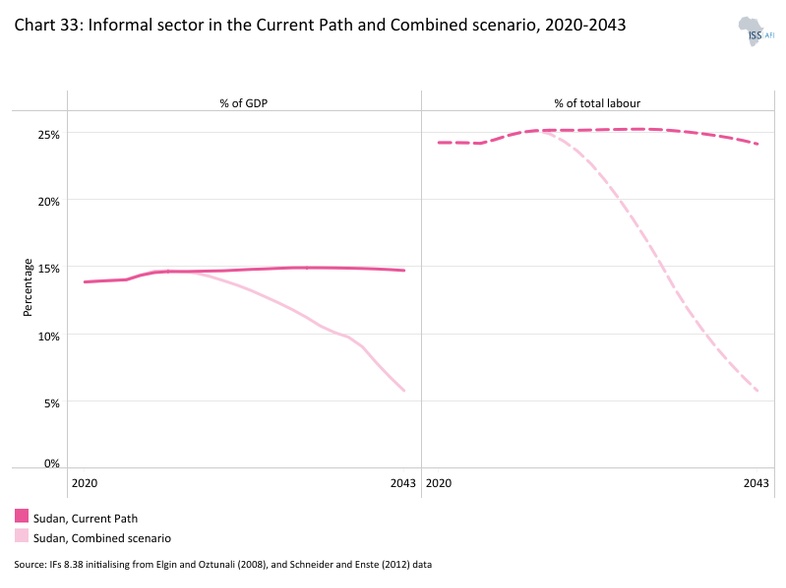

- By 2043, the size of the informal sector in Sudan will decline to 5.8% of GDP, valued at US$3.3 billion. At this rate, the contribution of the informal economy will be lower than the Current Path at 14.7% (valued at US$5.7 billion).

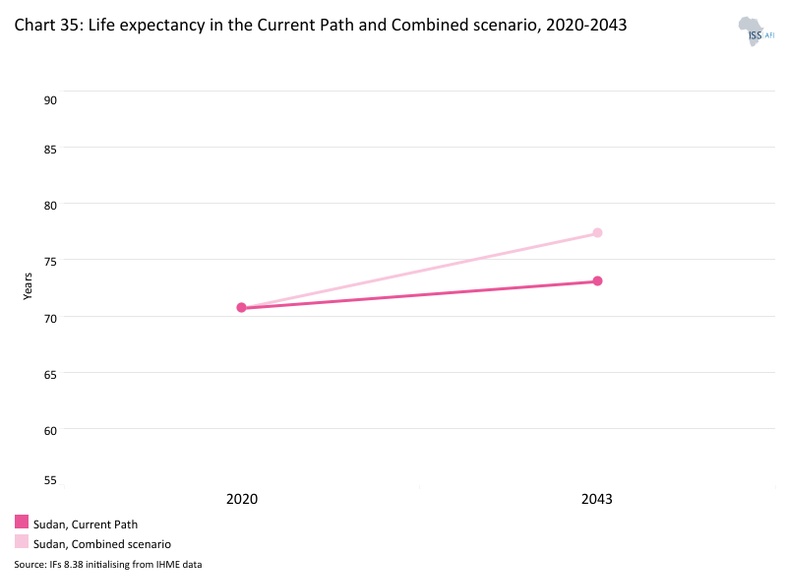

- In 2023, the average life expectancy at birth in Sudan was 70.3 years, which was about 6 years lower than the average for the country’s income-group peers in Africa. In the Combined scenario, life expectancy will increase to 73.1 years by 2043, which will be 4.2 years more than the country’s Current Path in the same year.

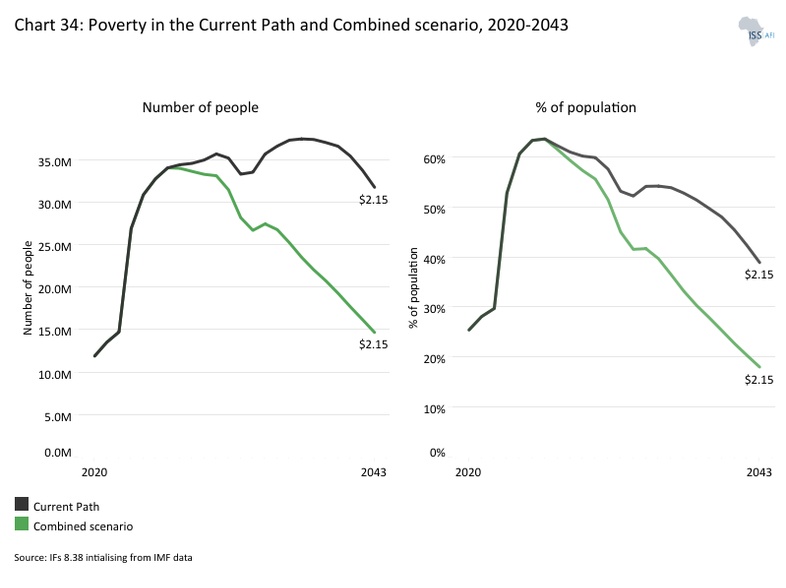

- In the Combined scenario, both the number and the proportion of poor people will significantly decline. By 2043, only about 18% of Sudanese, equivalent to 14.4 million people, will be living in extreme poverty, meaning 17.3 million more people could be lifted out of poverty.

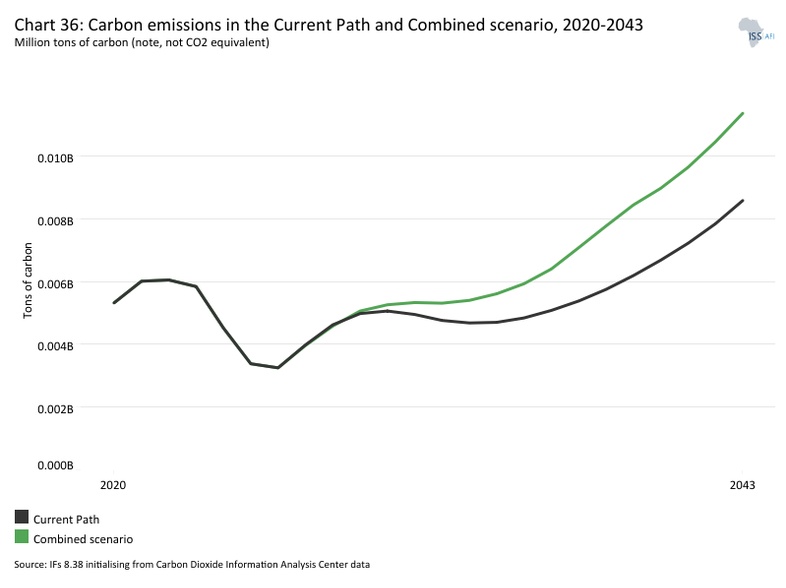

- In the Combined scenario, Sudan’s total carbon emissions will rise to 11.4 million tons, 32.6% higher than what is estimated in the Current Path for the same year.

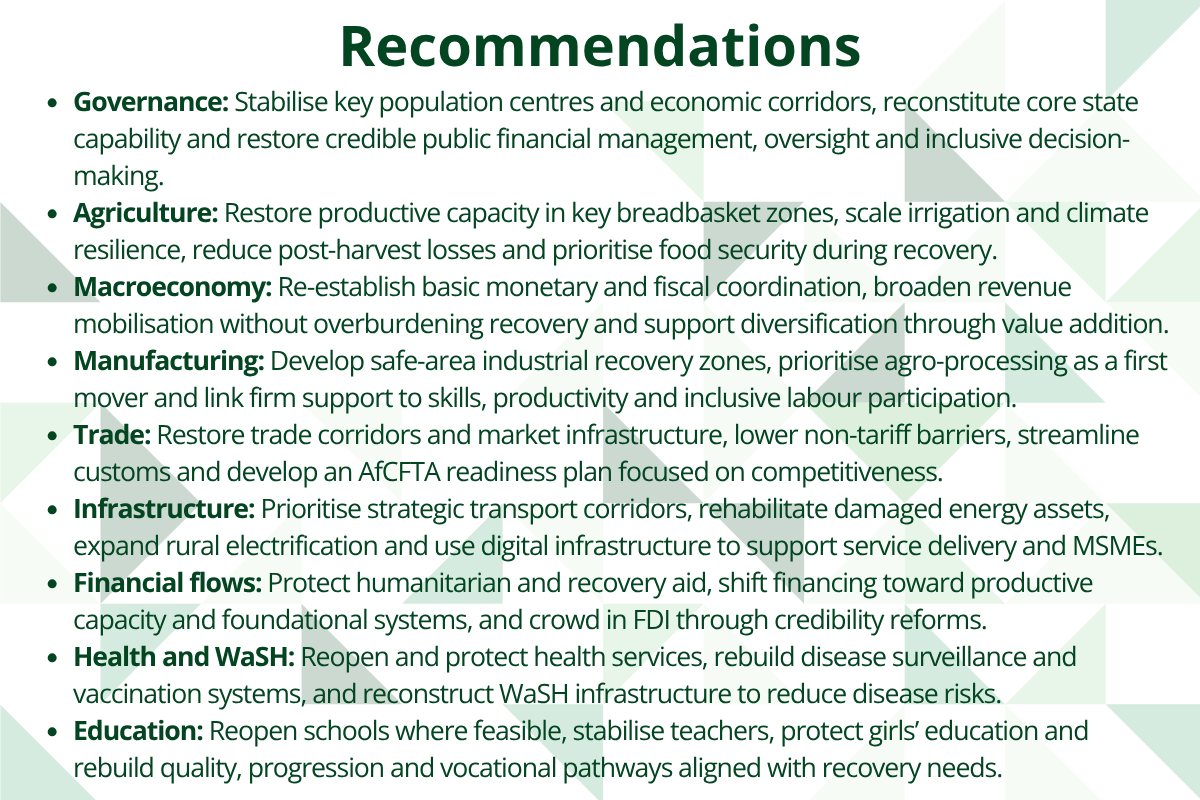

We end this page with a summarising conclusion offering key recommendations for decision-making.

Sudan is at a critical juncture. Despite its strategic location, substantial natural and agricultural resources and youthful population, the country has remained trapped in a prolonged cycle of conflict, institutional fragility and economic underperformance. Nearly seven decades after independence, development outcomes remain far below potential. The civil war that erupted in April 2023 has profoundly intensified these challenges, precipitating one of the world’s most severe humanitarian and development crises and bringing state institutions close to collapse.

The analysis confirms that violent conflict is the single most binding constraint to Sudan’s development, directly undermining all dimensions of human development addressed in the UNDP Strategic Plan. Since 2023, the war has resulted in large-scale loss of life, displaced more than 13 million people, destroyed infrastructure, disrupted markets and severely weakened the delivery of basic services.

The modelling identifies agricultural transformation, governance reform, regional trade integration and sustained external financial flows as the most powerful levers for raising incomes and reducing poverty. The strategic implication is clear: peace is a necessary condition for development, but peace alone is not sufficient. Sudan’s transition from fragility to resilience requires an urgent political settlement, the restoration of core state institutions and a coherent, data-driven development framework that prioritises governance, agricultural transformation, inclusive economic growth and climate resilience. With sustained and well-coordinated international support, Sudan can still move from crisis to recovery and from unrealised potential to inclusive and sustainable development. The window for action remains open, but it is rapidly narrowing.

All charts for Sudan Development Futures

- Chart 1: Political map of Sudan

- Chart 2: Population structure in the Current Path, 1990–2043

- Chart 3: Population distribution map, 2023

- Chart 4: Urban and rural population in the Current Path, 1990-2043

- Chart 5: GDP (MER) and growth rate in the Current Path, 1990–2043

- Chart 6: Size of the informal economy in the Current Path, 2020-2043

- Chart 7: GDP per capita in Current Path, 1990–2043

- Chart 8: Extreme poverty in the Current Path, 2020–2043

- Chart 9: Relationship between Current Path and scenarios

- Chart 10: Mortality distribution in the Current Path, 2023 and 2043

- Chart 11: Infant mortality rate in Current Path and Demographics and Health scenario, 2020–2043

- Chart 12: Demographic dividend in the Current Path and the Demographics and Health scenario, 2020–2043

- Chart 13: Crop production and demand in the Current Path, 1990-2043

- Chart 14: Import dependence in the Current Path and Agriculture scenario, 2020–2043

- Chart 15: Progress through the education funnel in the Current Path, 2023 and 2043

- Chart 16: Mean years of education in the Current Path and Education scenario, 2020–2043

- Chart 17: Value-add by sector as % of GDP in the Current Path, 2020 and 2043

- Chart 18: Value-add by the manufacturing sector in the Current Path and Manufacturing scenario, 2020–2043

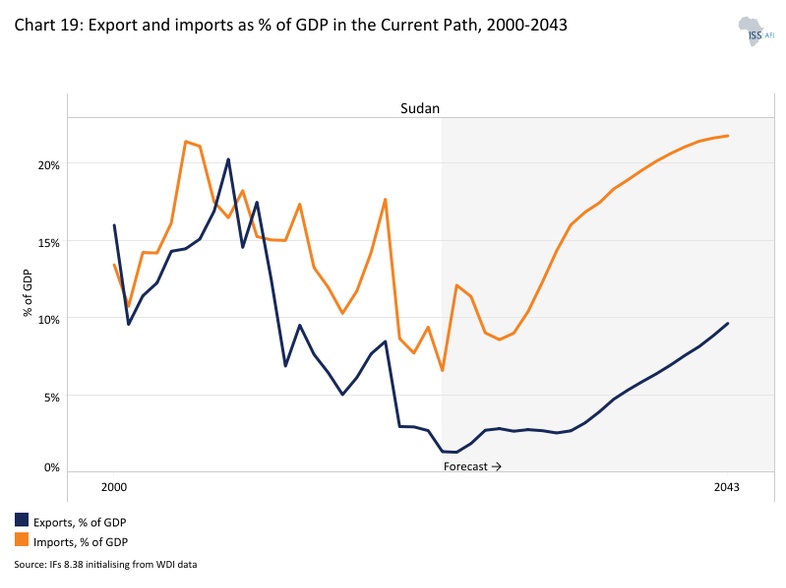

- Chart 19: Exports and imports as % of GDP in the Current Path, 2000-2043

- Chart 20: Trade balance in the Current Path and AfCFTA scenario, 2020–2043

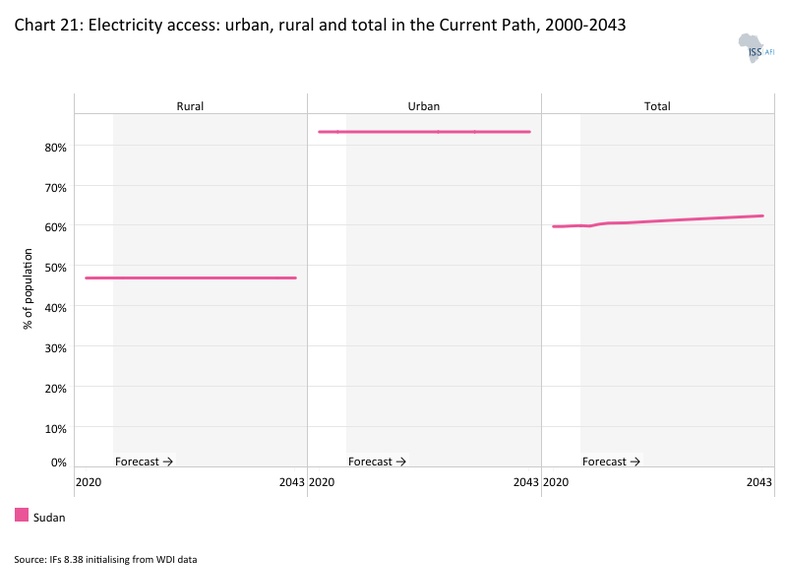

- Chart 21: Electricity access: urban, rural and total in the Current Path, 2000-2043

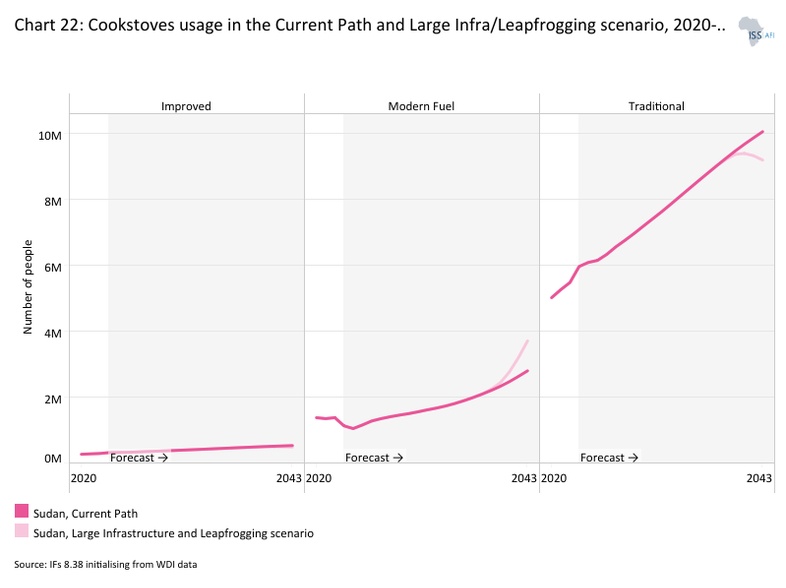

- Chart 22: Cookstove usage in the Current Path and Large Infra/Leapfrogging scenario, 2020–2043

- Chart 23: Access to mobile and fixed broadband in the Current Path and the Large Infra/Leapfrogging scenario, 2020–2043

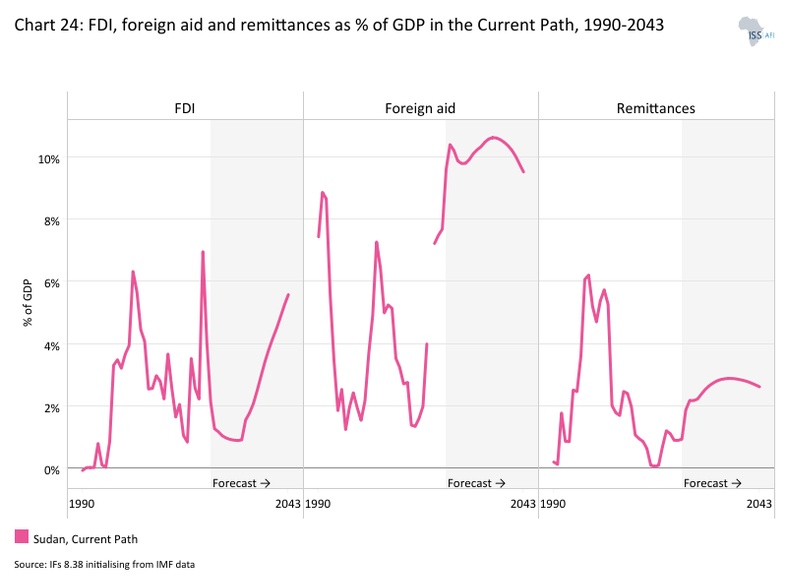

- Chart 24: FDI, foreign aid and remittances as % of GDP in the Current Path and in the Financial Flows scenario, 1990-2043

- Chart 25: Government revenue in the Current Path and Financial Flows scenario, 2020–2043

- Chart 26: Government effectiveness score in the Current Path, 2002-2043

- Chart 27: Composite governance index in the Current Path and Governance scenario, 2023 and 2043

- Chart 28: GDP per capita in the Current Path and scenarios, 2020–2043

- Chart 29: Poverty in the Current Path and scenarios, 2020–2043

- Chart 30: GDP (MER) in the Current Path and Combined scenario, 2020–2043

- Chart 31: GDP per capita in the Current Path and Combined scenario, 2023-2043

- Chart 32: Value-add by sector in the Current Path and Combined scenario, 2023 and 2043

- Chart 33: Informal sector in the Current Path and Combined scenario, 2020–2043

- Chart 34: Poverty in the Current Path and Combined scenario, 2023 and 2043

- Chart 35: Life expectancy in the Current Path and Combined scenario, 2020–2043

- Chart 36: Carbon emissions in the Current Path and Combined scenario, 2020–2043

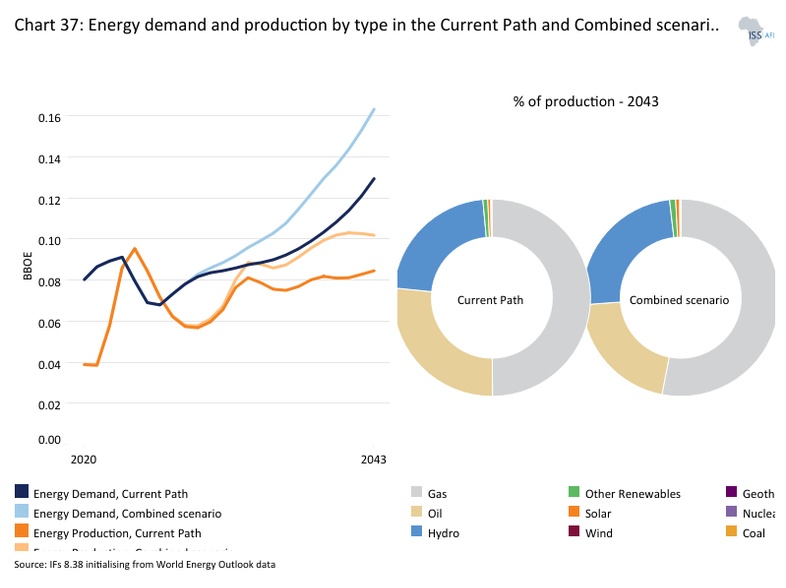

- Chart 37: Energy demand and production by type in the Current Path and Combined scenario, 2020-2043

- Chart 38: Policy recommendations

Chart 1 is a political map of Sudan.

Sudan gained independence in 1956. Despite attaining nearly seven decades of autonomy and self-rule from the Anglo-Egyptian condominium, the country’s socio-economic achievements do not match its potential, given its geography, natural resource endowments, and population size. A poor governance record, evident in protracted conflicts and authoritarian rule, has constrained effective state-building and left few prospects for transformative development.

Straddling and connecting north, east and central Africa, Sudan is the third-largest country in Africa after Algeria and DR Congo, with a land area of approximately 1 868 000 square kilometres. It shares borders with seven neighbouring countries, including Libya, Chad, the Central African Republic, Eritrea, Ethiopia, South Sudan and Egypt. Sudan’s maritime access to the Red Sea has the potential to serve as a logistical hub for countries in East Africa and as a gateway to landlocked countries in Central Africa. This geographical setup offers development opportunities through trade and regional integration. However, it has also brought geopolitics into a region with a long history of destabilisation, external interference, persistent intra-state conflict and proxy efforts, most notable in the context of the ongoing war.

Sudan’s capacity to serve as a hegemonic player in the region is heightened by its natural resource endowments. Sudan’s mineral deposit catalogue includes gold, uranium, chromite, gypsum, mica, marble and iron ore. Arable land and a wealth of livestock give Sudan the potential to serve as a key regional player in food value chains. However, these endowments have not translated into broad-based growth, employment creation, or improved welfare. Recurrent conflict, weak institutions, and policy inconsistency have constrained investment, undermined productivity, and limited value addition, leaving natural resource wealth insufficient to drive structural transformation.

Before South Sudan's secession in 2011, Sudan was one of the largest oil producers. Categorised as a petro-state, oil exports accounted for approximately 50% of government revenues and between 90-95% of total export earnings. Other prominent sectors comprising the Sudanese economy include agriculture, manufacturing, mining and services. Chronic trade deficits, particularly after South Sudan’s secession, and a lack of diversification created a contracting economy with high inflation, growing debt and chronic unemployment.

For most of its post-independence political history, the country has been beset by internal conflicts that have weakened its ability to play a leadership role in the region. Decades of internal conflicts have eroded Sudan’s governance and economic resilience, leaving its agricultural systems vulnerable. Today, this legacy of instability continues to undermine food security, as disrupted supply chains and weakened institutions struggle to meet the population’s needs. For example, continuous food price hikes due to a drop in export earnings led to the December 2018 demonstrations that resulted in the removal of President al-Bashir from power in April 2019. This led to the formation of a transitional government in September 2019. The power-sharing agreement between the military and civilian forces, which was expected to last 39 months, was cut short on 25 October 2021 when the Sudanese military, led by General Abdel Fattah al-Burhan, seized power in a military coup.

Since April 2023, Sudan has been embroiled in another civil war between the Sudanese Armed Forces (SAF) and the paramilitary Rapid Support Forces (RSF). The conflict has led to catastrophic humanitarian consequences. More than 150 000 people have been killed and nearly 15 million have been displaced, with 24 million people facing food insecurity, while 19 million people lack access to safe water and sanitation. The war has paralysed governance and resulted in the near-total collapse of state institutions. Beyond displacement and food insecurity, the war has disrupted health and education service delivery, damaged market infrastructure, and weakened production systems across agriculture, manufacturing, and services, deepening vulnerabilities and complicating recovery.

Despite its potential given its natural resources, youthful population, arable land, blue economy and maritime attributes along the Nile and access to the Red Sea, Sudan often ranks amongst the poorest countries according to the world’s human development indicators. According to the 2023-2024 Human Development Report (HDR), Sudan ranks 170 out of 193 countries. This low ranking reflects multi-dimensional constraints, including economic hardship and inequality, disrupted schooling and low learning outcomes, and a health system under severe strain. Recent years suggest stagnation and, since the outbreak of war, a likely regression in key human development outcomes, such as service delivery and household welfare deterioration.

While Sudan's future looks precarious given the nature of the war and the tremendous investments required for post-conflict reconstruction, once a permanent ceasefire is achieved, there’s hope for stabilisation and recovery scenarios. The trifecta of natural resources, a youthful population and propitious geography could help Sudan to realise its development potential and act as a pivotal player in the region. However, there is an urgent need for a political solution to end the conflict and address the humanitarian crisis. Building resilience and reimagining development in Sudan could be crucial steps towards achieving peace and stability.

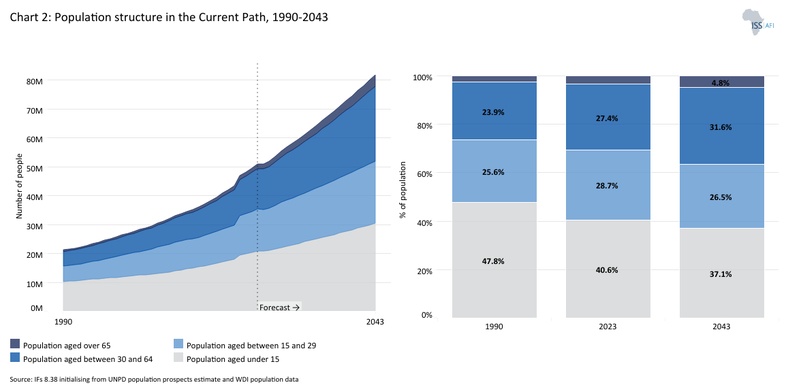

Chart 2 presents the Current Path of the population structure, from 1990 to 2043.

Sudan is the eighth-most populous country in Africa, the fourth-most populous country in East Africa after Ethiopia, Tanzania and Kenya, and the 30th globally. The Sudanese population is estimated at 52 million people, more than double the 22 million in 1990. Before the war, the country’s population grew by 2.7% in 2022, making it the 14th-highest growth rate in Africa and the highest in East Africa. Sudan’s population growth places significant pressure on government finances, as the government must increase its spending on essential social services, including education, healthcare and other amenities, to accommodate the growing population.

The war has had a devastating impact on demography and population, resulting in widespread displacement, loss of life and major disruptions to health, food security and infrastructure. As of mid-2025, nearly 12 million people had been forced to evacuate their homes as a result of the violence, with 7.7 million internally displaced persons (IDPs) and approximately 4.1 million crossing borders to seek refuge in neighbouring nations such as Egypt, South Sudan and Chad. The country now has the world's fastest-growing displacement crisis. Prolonged conflict will continue to influence Sudan's demographic and population profile for many years, affecting population density, age structure and urbanisation trends.

Sudan’s fertility rate fell from 6.1 children per woman of reproductive age in 1990 to 4.3 in 2023. Despite this decline, it remains high and far above the replacement rate. Several factors contribute to this, including the age at marriage, limited levels of female education, low urbanisation, extremely low contraceptive use and cultural norms. On the Current Path, the total fertility rate will decline further to 4 children per woman by 2043. As a result of this high fertility rate, the country has a youthful population. In 2023, 57.2% of Sudanese were below the age of 15 years, 41.3% were in the 15-64 years age group (working age), and 3.4% were 65 years and older. Comparing this with the structure in the 1990s reveals that Sudan’s population structure has not fundamentally changed over the past three decades. The high dependency ratio (population aged 15 and below and 65 and above) significantly affects the government's ability to generate the necessary revenue for development, as fewer individuals are in the working-age population. At the household level, families with more dependents typically save less, reducing overall domestic savings. This, in turn, limits the capital available for investment, impeding economic growth.

Sudan has the 5th-largest youth bulge (the ratio of its population aged 15-29 to the total adult population) in East Africa, after Uganda, Somalia, Eritrea and Ethiopia. The country’s youth bulge stood at about 48.3% in 2023, close to the East African average of 48.9% and below the African average of 45.6%. The median age for Sudan is 18.5 years, which is close to Africa’s median age of 19.3 years.

The large youth population in Sudan presents both opportunities and challenges. On the one hand, it can lead to a youthful labour force and drive positive political change and activism in the country. On the other hand, if the needs of the youth are not adequately addressed, it can increase the risk of criminal violence, conflict and instability, especially with relatively high youth unemployment, estimated to be 12% as of 2023. However, the country can harness the potential of its youthful population by making substantial investments in education and training, equipping young people with the skills they need, and creating opportunities through both government initiatives and private sector involvement.

The structure of Sudan’s population will not change much across the forecast horizon to 2043. The country’s population growth rate will increase to 2.3% by 2043, and the total population will rise to 81.7 million on the Current Path, making Sudan the sixth-most populous country in Africa. The median age will increase to 20.2 years by 2030 and 21.7 years by 2043, while the youth bulge will fall to 45.8% by 2030 and further to 42.1% by 2043. The proportion of people under 15 will decline slightly to 39.3% in 2030 and 37.1% in 2043. Consequently, the share of the working-age population and the population aged 65 and older will increase to 56.7% and 4.0% in 2030, and to 58.1% and 4.8% by 2043, respectively. Despite these shifts, the rapid population growth will continue to place pressure on development and limit improvements in average income, as the government will face significant challenges in addressing the needs of its rapidly expanding, youthful population.

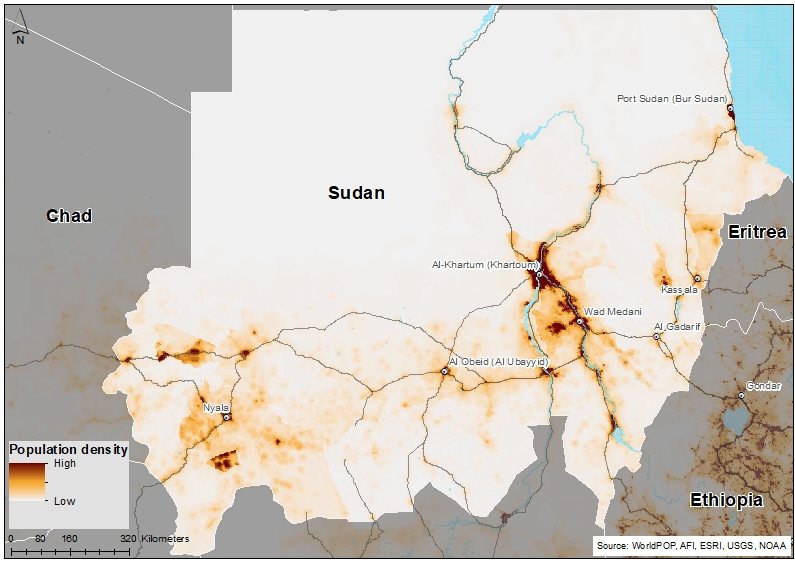

Chart 3 presents a population distribution map for 2023.

Sudan has a population density of approximately 0.29 people per hectare, ranking 11th-least-populated country in Africa. Half of the population lives on just over 15% of the land because of inadequate water supplies in many parts of the country. One-quarter of Sudan is virtually uninhabited, including the deserts of the north and north-west.

Khartoum and Omdurman are Sudan's most densely populated cities, with estimated populations of 6.8 million and 1.2 million, respectively. Its dense population is due to its role as a political, economic and cultural hub, hosting government institutions, businesses, trade centres and transport. Additionally, many internally displaced people seek refuge in Khartoum due to better security and services. Cities and regions in the arid and semi-arid western and southern parts of Sudan tend to be sparsely populated due to harsh climatic conditions that limit agricultural potential and water availability, ongoing conflicts and natural disasters that force population displacement, poor infrastructure and fewer economic opportunities, all of which discourage settlement. Some oil-producing border regions have displaced local populations due to concessions for exploration, contributing to a sparse population in those areas.

In the Current Path, Sudan’s population density will reach 0.47 people per hectare by 2043. However, that will still be significantly lower than the average of 0.77 and 1.0 people per hectare for Africa and East Africa, respectively.

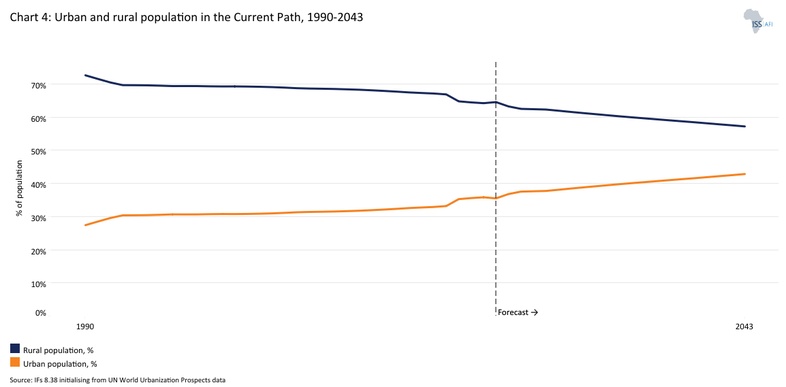

Chart 4 presents the urban and rural population in the Current Path, from 1990 to 2043.

Urbanisation in Sudan is driven largely by conflict-induced displacement, environmental and economic challenges in rural areas, and the concentration of opportunities in a few key urban centres. In 1990, close to two-thirds of Sudanese lived in rural areas, making Sudan predominantly rural. The country has experienced relatively rapid urbanisation over the past three decades compared to its income peers in Africa. It ranked 8th among the urbanised countries in East Africa and 13th among Africa’s low-income countries. Now, over 18.2 million Sudanese, equivalent to 35.3% of the population, live in urban areas. This rate is above the 30.2% and 32.6% averages of low-income countries in Africa and East Africa, respectively.

Urbanisation has been more pronounced in areas of the country with better-developed trade. With few exceptions, all major cities and towns in Sudan are located along the Nile, and one of its tributaries or along the coast of the Red Sea. The largest urban areas are the capital, Khartoum, and Omdurman, located roughly in the centre of the country, along with other regional capitals such as Nyala, Port Sudan and Kassala.

On the Current Path, Sudan's urban population will grow modestly, reaching 42.8% by 2043. Despite the country's overall slow pace of urbanisation, some cities, particularly the capital, are set to experience rapid growth due to the war's impact. As the SAF recaptures Khartoum in early 2025, it is likely to experience an influx of returnees. If not well managed, such urbanisation could lead to problems such as unemployment, poverty, inadequate healthcare, poor sanitation, the expansion of urban slums and environmental degradation. Already, a high proportion of the urban population lives in slums, estimated at 74% in 2022. This places considerable strain on public infrastructure, resulting in overcrowded roads, inadequate public transportation, and limited access to essential services such as healthcare and education. It thus requires careful planning and investment in sustainable development to ensure positive outcomes.

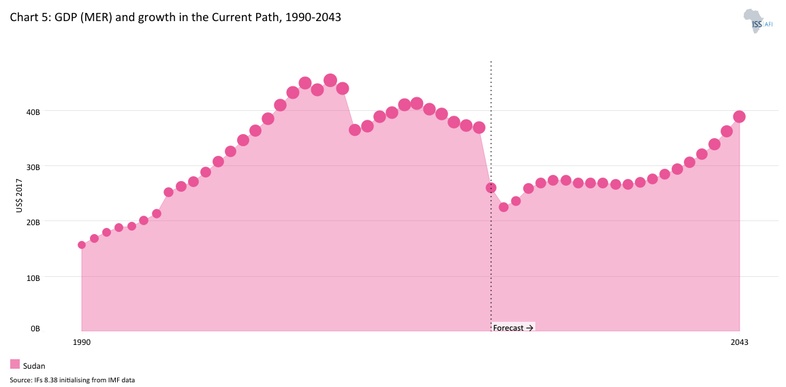

Chart 5 presents GDP in market exchange rates (MER) and growth rate in the Current Path, from 1990 to 2043.

The Sudanese economy was the fifth-largest in East Africa (after Ethiopia, Kenya, Tanzania and Uganda) and the fourth-largest among the 23 low-income countries in Africa (after Ethiopia, DR Congo and Uganda) in 2022. Its GDP measured in market exchange rates (MER) tripled from US$15.7 billion in 1990 to US$45.4 billion in 2010 before the secession of South Sudan. During this period, the average GDP growth was estimated at 5.0% per annum, above the average of 3.6% for low-income countries in Africa. This relatively stronger performance compared to its income peers can be attributed to its large volumes of oil export that spur growth in the country. The secession of South Sudan led to the loss of 75% of its oil resources, which accounted for more than half of Sudan's government revenue and 90% of its exports. This shock resulted in severe challenges, including double-digit consumer price inflation of over 40%, rapid exchange rate depreciation, and a significant trade deficit, which, together with increased fuel prices, triggered violent protests in the country. Ultimately, the economy contracted by 17% in 2012, reflecting the underlying macroeconomic shocks occasioned by the secession.

The economy began to recover in 2013 and continued a positive economic trajectory until 2017. The stable growth within this period was driven by increased exports of gold and oil and supported by government economic reforms. These reforms include the implementation of the Five-Year Economic Reform Program (2015-2019), exchange rate liberalisation and the Investment Encouragement Act (2013), which provided fiscal incentives and legal protections to attract investment. A modest attempt at fiscal consolidation through subsidy reductions and improved revenue mobilisation also reduced fiscal deficit and curbed inflation, all of which contributed to increased investment and donor support.

However, since the coup in April 2019, Sudan has been trapped in political instability, conflict and an economic mire with currency depreciation, crippling debts, rising inflation and food shortages. Multiple shocks to the economy have derailed Sudan’s economic recovery and worsened macroeconomic conditions, leading the country to regress from a lower-middle-income to low-income status in July 2020. Within this period, three key factors underlie this economic contraction. The first is the recurrent political instability that has plagued the country. Continuous food price hikes led to the December 2018 demonstrations that resulted in the removal of President al-Bashir from power in April 2019. The October 2021 military coup that toppled the transitional government also constrained economic recovery. As such, even the removal of Sudan from the US State Sponsors of Terrorism list to end the 23-year sanctions, which was expected to open the door to aid, debt relief, trade, and investment badly needed to pull the country out of its severe economic crisis, did not materialise. Sudan’s economic growth was further disrupted by the COVID-19 pandemic in 2020. The restrictive measures and protocols instituted to control the virus curtailed economic activities. This, coupled with Russia’s invasion of Ukraine that led to a global food crisis, worsened the domestic economic vulnerabilities.

In 2023, Sudan’s GDP stood at US$32.4 billion, a contraction of 12% from the previous year. It is estimated to have contracted further in 2024. Sudan’s economy was already under severe strain before the current conflict, burdened by high debt levels, weak revenue generation, and stalled structural reforms. The outbreak of conflict has further exacerbated these vulnerabilities, leading to widespread institutional breakdown and economic dislocation. Monetary accommodation and rapid deposit growth have fueled persistent inflationary pressures and widened currency market disparities, prompting authorities to implement emergency measures—such as suspending corporate mobile money transactions—to curb speculative activity.

Annual inflation reached an all-time high of 360% in 2021. It was estimated at 170% in 2024, mainly driven by high food inflation, with soaring prices and foreign exchange shortages placing immense strain on households and businesses alike. High public spending is also resulting in a large fiscal deficit and public debt, largely financed by external borrowing. Public debt stood at about 148% of GDP by the end of 2024, with external debt constituting about 137% of total debt. While this is very high, it represents a decline from the 281% it recorded in 2020 during the COVID-19 pandemic.

The government continues to grapple with limited revenue mobilisation, large fiscal deficits and rising public debt, all of which constrain its policy response. External pressures have compounded the situation: the UAE’s ban on Port Sudan’s maritime and air operations and ongoing US sanctions have significantly restricted trade and access to international financing. Moreover, the emergence of a parallel government in Nyala poses a serious risk of further political fragmentation and an escalation of conflict, threatening to derail any prospects for economic stabilisation and recovery. The attacks in May 2025 on Port Sudan and oil facilities expanded the conflict to previously stable regions, increasing broader economic recovery risks.

A nascent economic recovery is emerging in some urban centres, supported by the gradual return of displaced populations and government initiatives to reestablish key institutions. Satellite trade data indicate improving economic activity in less-affected states and a rebound in external trade during early 2025. Notably, inflation has begun to ease, with monthly inflation rates declining—primarily driven by lower housing and food prices.

On the Current Path, Sudan’s GDP will reach US$38.9 billion by 2043. The average growth rate within this period (2024-2043) is estimated at 1.2%, far below the 6.2% estimated average for low-income countries on the continent. This suggests that Sudan’s growth potential is hindered by recurrent conflict and political instability, even in the long term. The country, therefore, needs to rethink its economic development strategy to focus on economic diversification and value addition to its main commodities. Its huge natural resource deposits, along with its agricultural and renewable energy potential, offer opportunities to grow and transform the economy. Nonetheless, the most pressing need is for peace and stability, which is sine qua non for any economic recovery agenda.

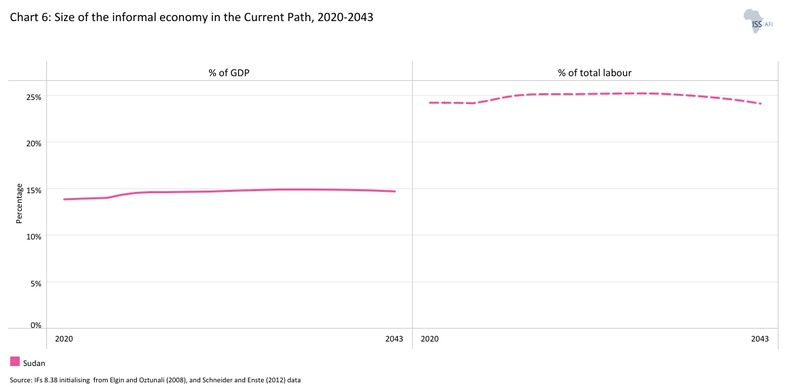

Chart 6 presents the size of the informal economy as per cent of GDP and per cent of total labour (non-agriculture), from 2020 to 2043. The data in our modelling are largely estimates and therefore may differ from other sources.

The informal sector in Sudan constitutes a significant portion of the national economy and exhibits several defining characteristics. The relatively low barriers to entry in the informal sector compared to those in formal industrial enterprises allow individuals to sustain livelihoods with minimal start-up capital. A large share of Sudan’s workforce operates within this sector, with approximately 85% engaged in vulnerable employment and 60% working in subsistence agriculture. Informal enterprises are commonly characterised by low-cost, small-scale activities such as food preparation and sales, tea and coffee vending, tailoring, street vending, domestic services and small-scale manufacturing, including bread and charcoal production.

In 2023, the informal sector in Sudan accounted for approximately 14% of GDP, below the average of 32% for its income peers in Africa. This represents a significant drop from the 27.2% of GDP recorded in 1990. In the Current Path, the size of the informal sector will largely remain the same, even reaching 14.7% of GDP by 2043. The large contrast between its labour force share and contribution to GDP reflects the underlying low productivity, wages and inefficiency that characterise the sector.

Since the 1990s, informal economic activity has increasingly shifted toward urban areas as a result of internal migration driven by conflict, drought and economic hardship. Major cities such as Khartoum, Omdurman and Port Sudan now host substantial concentrations of informal businesses. Most of these enterprises remain unregistered, untaxed and outside formal legal frameworks, which limits their access to financial services, government support and legal protections. Workers in this sector often face precarious employment conditions, lacking social protection or employment benefits. Women are particularly disadvantaged, facing higher unemployment rates and lower wages than men.

Due to their exclusion from formal systems, informal workers often lack access to education, healthcare and social security. The sector’s broad scope—spanning agriculture, trade and services—complicates the design and implementation of targeted policy interventions. Moreover, microfinance institutions have largely failed to meet the needs of informal workers, frequently trapping them in cycles of debt rather than facilitating sustainable economic growth. The private sector has also shown limited engagement, with fragmented and uncoordinated initiatives that rarely address critical areas such as capacity development, credit access and institutional support. Macroeconomic instability and inconsistent policy frameworks further constrain efforts to formalise the sector. Many informal workers remain resistant to formalisation, fearing loss of flexibility or increased taxation, while government-led efforts have often emphasised tax collection over meaningful inclusion and support.

Several initiatives have attempted to extend protection and support to informal workers. The Sudan Family Support Programme (SFSP) and Zakat schemes sought to provide social safety nets, but their effectiveness has been limited by political instability. Programs such as Mobile Training Centres have offered vocational training in carpentry, electrical maintenance and automobile repair to enhance workforce skills. In contrast, organisations such as the Sudanese Women’s General Union (SWGU) have provided health insurance to informal workers, particularly women tea sellers. However, these efforts face sustainability challenges due to limited resources and weak institutional capacity.

Expanding social protection coverage through simplified and inclusive systems can promote productivity and income growth in the informal economy, laying the foundation for gradual formalisation. It also encourages collective bargaining and worker representation through structured stakeholder dialogue. The International Labour Organization (ILO) advocates combining macroeconomic reforms with micro-level interventions, including entrepreneurship support, vocational training, improved access to microfinance and legal frameworks that incentivise formalisation.

Despite ongoing initiatives to formalise the informal sector through training programs, social protection schemes and policy frameworks, persistent challenges—such as economic instability, poor coordination and worker resistance—continue to hinder progress. A comprehensive, multi-level strategy that addresses these systemic barriers is essential to promoting successful formalisation and inclusive economic transformation in Sudan.

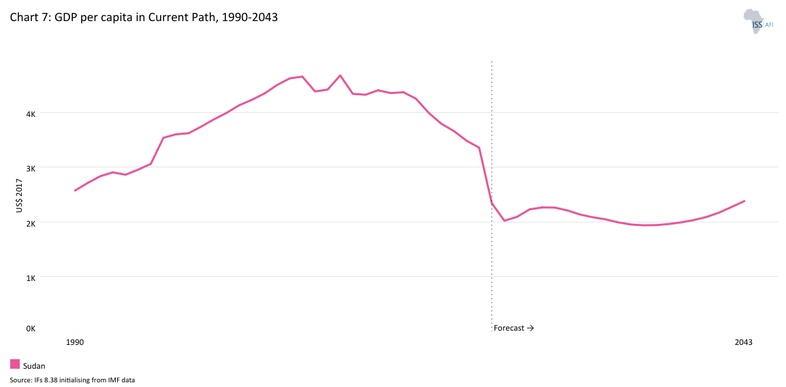

Chart 7 presents GDP per capita in the Current Path, from 1990 to 2043, compared with the average for the Africa income group.

In terms of GDP per capita (using the purchasing power parity (PPP) measure for this analysis), Sudan’s GDP per capita improved from US$2 868 in 1990 to US$4 884 in 2011 before the secession of South Sudan. Since then, Sudan has generally recorded a downward trend, with its GDP per capita dropping to US$2 961 in 2023. This represents a 54% contraction from the country's 2012 levels and sends Sudan back to the per capita income levels it recorded in 1992. This is a clear demonstration of the impact that the recurrent conflicts, political instability and the secession of South Sudan have had on the welfare of the Sudanese.

In the medium term (2035), per capita income in Sudan is set to drop further to US$1 941. However, after 2035, the country will begin to record modest improvement with its GDP per capita reaching US$2 384 by 2043. Despite this improvement, Sudan will lose ground to its income-group peers, as their average GDP per capita reaches US$2 998 by 2043, placing Sudan tenth among low-income African countries. The country’s GDP per capita Current Path forecast for 2043 remains below the current levels and worse than the 1960s levels. Slower growth in GDP per capita can have several implications. First, it can lead to slower poverty reduction and limited improvements in living standards in Sudan. Additionally, slow GDP per capita growth may imply that the benefits of economic growth are not evenly distributed or broadly shared, thereby worsening inequality in the country. It may also constrain government revenue, limiting the ability to invest in critical areas such as education, healthcare and infrastructure.

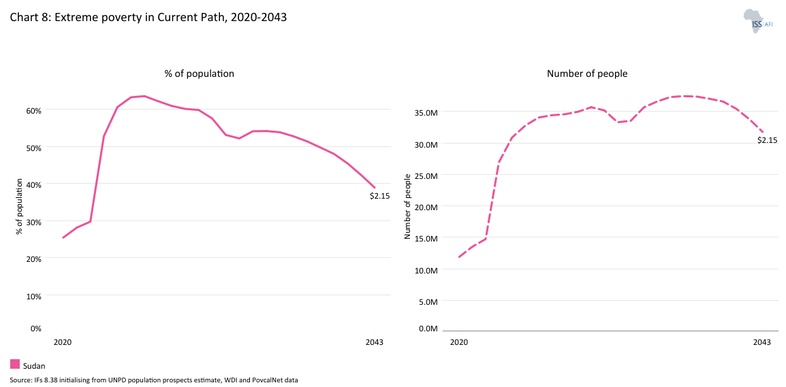

Chart 8 presents the rate and number of poor people in the Current Path from 2020 to 2043.

The IFs forecasting platform projects international measures for extreme poverty. Thus, this study uses the US$2.15 per day poverty line (2017 PPP), unless otherwise specified, to remain consistent with international poverty analyses. As a result, the poverty rates reported here differ from those measured using the national poverty line.

Like many low-income countries in Africa, poverty in Sudan is widespread. In 1990, 8.4 million Sudanese, representing 38.1% of the population, lived below the poverty line of US$2.15, which was half the average rate of 66.6% for low-income countries in Africa. In the past two decades that followed, the country’s efforts at poverty eradication have yielded results, as the poverty rate declined to 15.6% in 2011, far below the average of 50% for low-income countries in Africa. However, since then, Sudan has backslidden with poverty levels rising substantially over the last decade to reach 45% of the population, which corresponds to 22.8 million Sudanese living below the poverty line of US$2.15 in 2023. This takes the country back to extreme poverty levels higher than those it recorded in the 1980s.

Extreme poverty levels in Sudan are set to worsen, reaching nearly 60% of the population in 2030 under the Current Path, translating to almost 36 million people. Yet, the world is targeting to eliminate extreme poverty. However, beyond 2030, extreme poverty is projected to decline to 38.8% of the population by 2043, equivalent to 31.7 million. This means that Sudan will not meet either Sustainable Development Goal 1, which aims to eliminate extreme poverty below 3% by 2030, or the AU Agenda 2063 Goal 1, Aspiration 1, a feat that can only be achieved in 2088 if the current development trajectory persists.

To appreciate the full extent of poverty, one must look beyond monetary poverty, as it tells only part of the story. The Human Development Index (HDI), which measures the average achievement of countries in three main areas: health, knowledge and standard of living, is one such measure. Sudan’s HDI score of 0.511 in 2023 ranks 170 out of 193 countries globally. The global Multidimensional Poverty Index (MPI) also measures acute multidimensional poverty by assessing each person’s overlapping deprivations across 10 indicators in three equally weighted dimensions: health, education and standard of living. The MPI complements the international US$2.15-a-day poverty rate by identifying who is multidimensionally poor and by showing the composition of multidimensional poverty. The headcount or incidence of multidimensional poverty is often several percentage points higher than that of monetary poverty. This implies that individuals living above the monetary poverty line may still suffer deprivations in health, education and/or standard of living.

According to the 2023 UNDP Multidimensional Poverty Index, about 52.3% of Sudanese were considered multidimensionally poor with an intensity of deprivation estimated at 53.4%. An extra 17.7% of the population was considered vulnerable to multidimensional poverty. Likewise, inequality is high in Sudan, although better than the average for Africa’s low-income countries. In 2023, Sudan’s Gini coefficient was 0.33 compared to the average of 0.40 for low-income countries in Africa. Given the devastating impact of the conflict, the actual levels of inequality may be much worse than estimated. Such high levels of income inequality have many negative effects, including a breakdown of social structure and cohesion, which can result in instability. On the Current Path, income inequality in Sudan remains unchanged across the forecast horizon, only slightly declining to 0.30 by 2043.

Sudan has implemented a range of strategies and projects to address poverty and inequality, including Sudan’s Poverty Reduction Strategy Paper (PRSP) for 2021-2023, which focused on macroeconomic stability, inclusive economic growth, human and social development, peace promotion and governance strengthening. The PRSP also integrated gender equity, emphasising job creation for women and youth. Complementary measures include expanding fiscal policies to mobilise domestic and external resources for public investment, improving access to credit for small-scale farmers and supporting microfinance initiatives to generate employment opportunities. Collectively, these strategies aim to reduce poverty and foster sustainable development nationwide. In addition, the World Bank approved US$182 million in 2025 for two key initiatives: the Sudan Health Assistance and Response to Emergencies (SHARE) Project and the Sudan Emergency Crisis Response Safety Net Project. These initiatives aim to enhance healthcare services, provide emergency safety nets and address food insecurity among vulnerable populations affected by conflict and natural disasters.

However, several structural and contextual factors continue to perpetuate poverty in Sudan. Prolonged conflicts have destroyed infrastructure, displaced millions and disrupted livelihoods. The secession of South Sudan in 2011 further deepened fiscal deficits by eliminating a major source of oil revenue, previously a cornerstone of Sudan’s economy. In addition, droughts and desertification have severely reduced agricultural productivity, leading to food shortages and worsening rural poverty. Weak healthcare and education systems limit access to essential services, particularly in remote areas, while high illiteracy rates constrain economic opportunities, further entrenching poverty.

Ongoing political instability and security challenges have also undermined development efforts. The loss of oil revenues, coupled with a heavy external debt burden and restricted access to financing, limits the government’s capacity to implement effective poverty reduction programs. Furthermore, pro-poor spending remains inadequate due to fiscal constraints and low execution rates for poverty-targeted expenditures. Poor infrastructure—especially in transportation, energy and communication—continues to hinder economic growth potential, while climate-related shocks exacerbate food insecurity and displacement. Addressing these challenges requires sustained international support, comprehensive structural reforms and enhanced governance frameworks to build resilience, stimulate inclusive growth and establish a stable foundation for sustainable development.

The eight sectoral scenarios as well as their relationship to the Current Path and the Combined scenario are explained in the Technical page. Chart 9 summarises the approach.

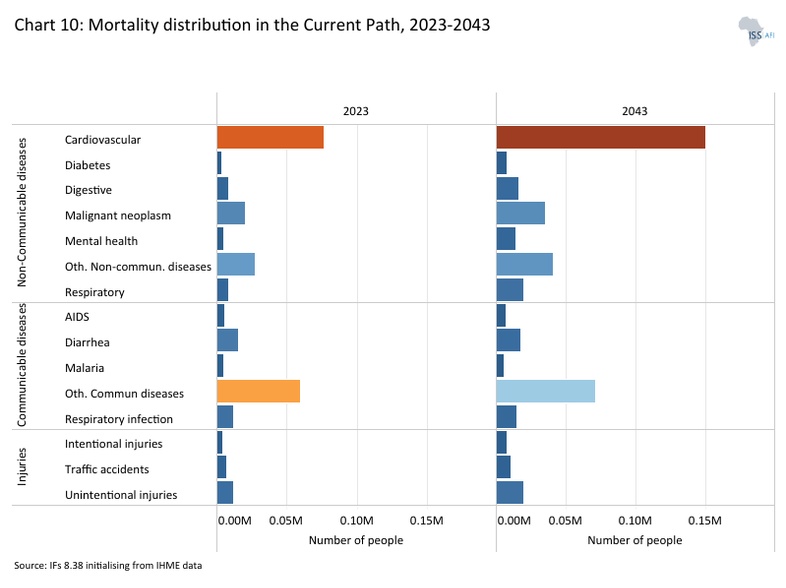

Chart 10 presents the mortality distribution in the Current Path for 2023 and 2043.

The Demographics and Health scenario envisions ambitious improvements in child and maternal mortality rates, enhanced access to modern contraception, and decreased mortality from communicable diseases (e.g., AIDS, diarrhoea, malaria, respiratory infections) and non-communicable diseases (e.g., diabetes), alongside advancements in safe water access and sanitation. This scenario assumes a swift demographic transition supported by heightened investments in health and water, sanitation and hygiene (WaSH) infrastructure.

Visit the themes on Demographics and Health/WaSH for more detail on the scenario structure and interventions.

The IFs model uses the International Classification of Diseases (ICD) to differentiate between three broad categories of diseases: communicable, non-communicable and injuries, as well as 15 subcategories of mortality and morbidity. Historically, Sudan has recorded a relatively large share of deaths from non-communicable diseases and injuries compared to many African countries. In 1990, communicable diseases caused about 131 000 deaths, representing about 51% of total deaths in that year. This was followed by non-communicable diseases that caused 97 740 deaths (38.5% of total deaths) and injuries that caused 25 190 deaths (9.9% of total deaths). Due to the rapid increase in deaths from non-communicable diseases, Sudan reached its epidemiological transition in 2002: the point where deaths from non-communicable diseases outweigh deaths from communicable diseases. This transition will inevitably increase health sector costs, as these patients are more expensive to treat.

By 2023, deaths from non-communicable diseases had risen to 149 360, constituting 55.4% of all deaths in the country, while deaths from communicable diseases and injuries fell to 97 170 (36.1% of all deaths) and 22 860 (8.5% of all deaths), respectively. According to the WHO, the leading causes of death in Sudan are: ischaemic heart disease, stroke, preterm birth complications, lower respiratory, road injury, malaria and measles. However, due to the ongoing conflict, deaths from injuries may be underestimated. Conservative estimates show that over 61 000 deaths occurred between April 2023 and June 2024, with high intentional injury in Khartoum State and Gezira State, the Kordofan and Darfur regions.

Since the onset of the war, Sudan’s healthcare system has suffered catastrophic disruptions, with an estimated 70-80% of health facilities in conflict zones rendered non-functional due to attacks, looting and destruction. Hospitals and primary healthcare centres in Khartoum, Darfur, Kordofan and Al Jazirah have been particularly affected. More than 145 verified attacks on health facilities and personnel have resulted in deaths, service disruptions and severe shortages of essential medical supplies. Consequently, around 65% of Sudan’s population lacks adequate access to healthcare, and in Khartoum, only one in four hospitals remains operational.

The conflict has forced many skilled healthcare professionals to flee or become displaced, leaving those who remain to work under unsafe and resource-constrained conditions. Disease outbreaks such as measles in White Nile State have emerged among displaced populations, worsened by the breakdown of vaccination programs and disease surveillance systems. Women face life-threatening complications due to the absence of reproductive health services, while children are disproportionately affected by malnutrition, disease outbreaks and inadequate paediatric care.

The collapse of healthcare infrastructure has fueled the spread of cholera, malaria, dengue fever and measles, driven by poor sanitation, disrupted vaccination campaigns and inadequate disease surveillance. These outbreaks have disproportionately affected women, children, the elderly and persons with disabilities. Approximately 35% of women lack access to reproductive health services, and 55% of children are at risk of preventable diseases. The situation is further aggravated by economic instability, which has reduced funding for public health and left two-thirds of the population without access to essential services.

Despite these challenges, several efforts are underway to mitigate the crisis. The World Health Organization (WHO) has launched emergency appeals and distributed medical supplies nationwide, providing care for over 22 000 war-wounded patients in 2023. The International Committee of the Red Cross (ICRC) has deployed mobile surgical teams and delivered emergency medical aid to conflict-affected regions. The World Bank has approved US$182 million to support healthcare restoration and social safety nets, including financing for WHO and UNICEF to rebuild health infrastructure and contain disease outbreaks. Collaborative efforts among health institutions, local organisations and civil society groups aim to improve immunisation rates, expand access to healthcare in underserved areas and reduce preventable illnesses. Additionally, partnerships between health and WaSH (Water, Sanitation, and Hygiene) clusters seek to limit disease transmission by improving access to safe drinking water and sanitation facilities.

These interventions are critical as Sudan’s health vulnerabilities deepen amid ongoing conflict, mass displacement and structural instability. Sustained international support, improved governance and long-term investment in healthcare infrastructure are crucial to rebuilding the system and ensuring access to essential health services for all Sudanese. On the Current Path, the epidemiological transition that is already visible will continue, such that non-communicable diseases will be the highest cause of death with 282 720 deaths in the country (about 64.9% of all deaths) by 2043. By then, deaths from communicable diseases will also rise to 115 540, constituting 26.5% of all deaths, while deaths from injuries will constitute the remaining 8.6%. These conditions underscore the urgent need for coordinated humanitarian interventions to restore healthcare delivery and address the escalating crisis.

Access to improved, safe and treated water as well as proper sanitation is crucial for preventing the spread of communicable diseases. Poor water sources and inadequate sanitation are linked to diseases such as diarrhoea, which disproportionately affect children. Sudan has made significant progress towards achieving SDG 6.1 on universal access to safe drinking water. In 2023, 30.6 million Sudanese (constituting 87.2% of the population) had access to an improved water supply. Out of this, 15.6 million people (about 45.8% of the population) had access to a piped water supply in the country. Despite this progress, Sudan’s water systems face severe and compounding challenges, exacerbated by ongoing conflict, infrastructure degradation and limited institutional capacity. Many water delivery systems have become inoperable due to battle damage, poor maintenance and fuel shortages needed to power pumping stations. Urban water networks have been destroyed or neglected, while rural communities rely primarily on hand pumps and protected wells.

On the Current Path, Sudan’s progress will lag behind the SDG target as only 91.3% of the population will have access to improved water by 2030. Even by 2043, it is projected that access to improved water in Sudan will largely remain the same (90.5%), although the share of piped water will rise to constitute 36% of connections, meaning that the country will still miss the SDG target by then.

Access to improved sanitation is limited in Sudan, with many citizens resorting to open defecation and other unimproved methods. In 2000, more than half of the Sudanese resorted to open defecation and 23% used unimproved sanitation. Despite efforts to improve access to safely managed sanitation, the country still lags. By 2023, only about 8.6 million Sudanese (16.9% of the population) had access to safely managed sanitation services, which is slightly above the average of 15.5% for its income-group peers in Africa. More than two-thirds of the Sudanese resort to unimproved sanitation, including open defecation, an inadequate waste management system and the absence of proper toilet facilities, which pose major health and environmental risks to the country.

On the Current Path, the proportion of the population with access to safely managed sanitation will decline to 13.8% in 2030, before rising to 22.5% by 2043. This means that Sudan will lag in achieving SDG target 6.2, which aims to ensure access to adequate and equitable sanitation and hygiene for all, and to end open defecation. Consequently, the share of the population with unimproved sanitation access will rise to 45.8% in 2030, before falling to 36.5% in 2043. The use of open defecation will constitute 23.5% of the population in 2030 and 20.6% by 2043.

Emergency sanitation measures have often been temporary and inadequate, exposing communities to waterborne diseases and gender-based violence due to the lack of privacy and safe sanitation facilities. With the escalation of conflict, the situation has worsened, particularly for women and children, who face disproportionate health risks and vulnerabilities. The government, with international support, has developed strategic frameworks for WaSH, aiming to achieve universal access by 2030. However, the current humanitarian crisis—marked by millions of internally displaced persons (IDPs), limited access to potable water, worsening cholera outbreaks and a broader public health emergency—has severely undermined progress toward these goals.

Key challenges include damaged infrastructure, climate variability leading to both droughts and floods, economic constraints that restrict investment and population displacement, which place additional pressure on already scarce water resources. In response, UNICEF and other humanitarian partners are working to provide emergency water supplies through chlorination, water trucking and rehabilitation of water facilities. However, lasting improvements will require significant infrastructure reconstruction, sustained financing and the implementation of coordinated national strategies for water and sanitation reform.

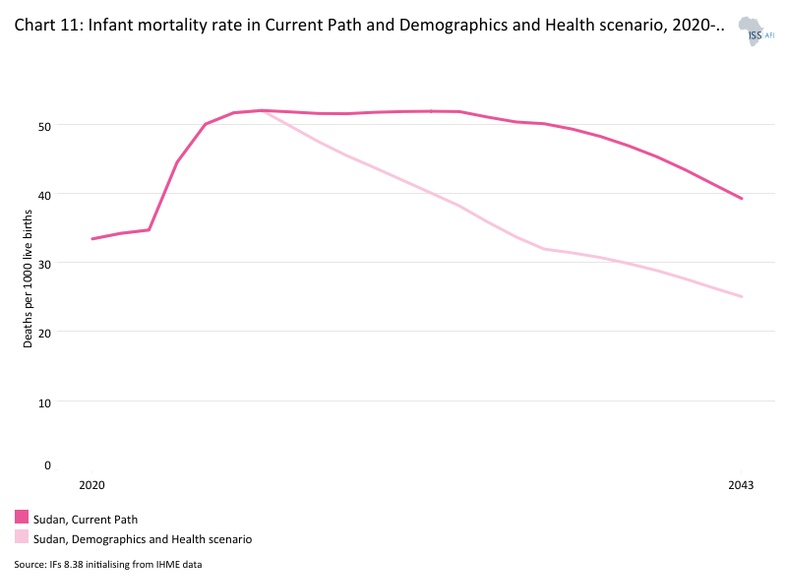

Chart 11 presents the infant mortality rate in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The infant mortality rate is the probability of a child born in a specific year dying before reaching the age of one. It measures the neonatal survival rate and reflects the social, economic and environmental conditions in which children live, including their health care. It is measured as the number of infant deaths per 1 000 live births and is an important marker of a country's overall health system quality.

Historically, Sudan’s infant mortality rate has been lower than the average for its income peers in Africa. In 1990, the country recorded the fifth-lowest infant mortality rate among low-income nations on the continent. However, progress has been slow over the years, as other countries have made faster improvements, causing Sudan to slip to the 12th position by 2023. Beginning in 2022, the infant mortality rate started to rise, surpassing the average rate observed among other low-income African countries. In 2023, the infant mortality rate in Sudan was 44.5 deaths per 1 000 live births, a drop of more than half from the 1990 rate. However, this was slightly higher than the average of 43.8 deaths for low-income countries in Africa.

Infant mortality in Sudan is driven by a combination of interrelated factors, including infectious diseases, malnutrition, limited access to healthcare, maternal health complications and poor sanitation. The leading direct causes include septicemia (blood poisoning), malaria, respiratory infections, gastrointestinal diseases and neonatal malnutrition. The situation in Sudan is aggravated by the lack of functional health facilities, the high cost and limited availability of transportation to medical centres, and unsanitary conditions during delivery and neonatal care. Socioeconomic factors also play a crucial role: lower household income and limited parental education are strongly associated with higher infant mortality rates. Additionally, conflict and population displacement increase the risk of unsafe and unhygienic childbirth conditions, further endangering both mothers and newborns.

On the Current Path, the infant mortality rate will rise further, reaching 51.7 deaths per 1 000 live births in 2030, before eventually falling to 39.2 deaths per 1 000 live births by 2043, a rate higher than recorded in 2017, an indication of retrogression that is expected to occur. At this rate, Sudan will become the country with the fifth-highest infant mortality among low-income countries in Africa. It means that Sudan will not achieve the SDG target of 12 deaths per 1 000 live births even by 2043, which can only be achieved by 2093 in the Current Path projections.

Under the Demographics and Health scenario, Sudan will reduce its infant mortality rate to 41.9 deaths per 1 000 births in 2030 and 25.1 deaths per 1 000 births by 2043. This will be 14 deaths fewer than in the Current Path and at par with the average of low-income countries in Africa by 2043. Although this does not meet the SDG target of 12 deaths per 1 000 births, it pushes Sudan close to it, emphasising the need for the country to invest in improving healthcare services and infrastructure.

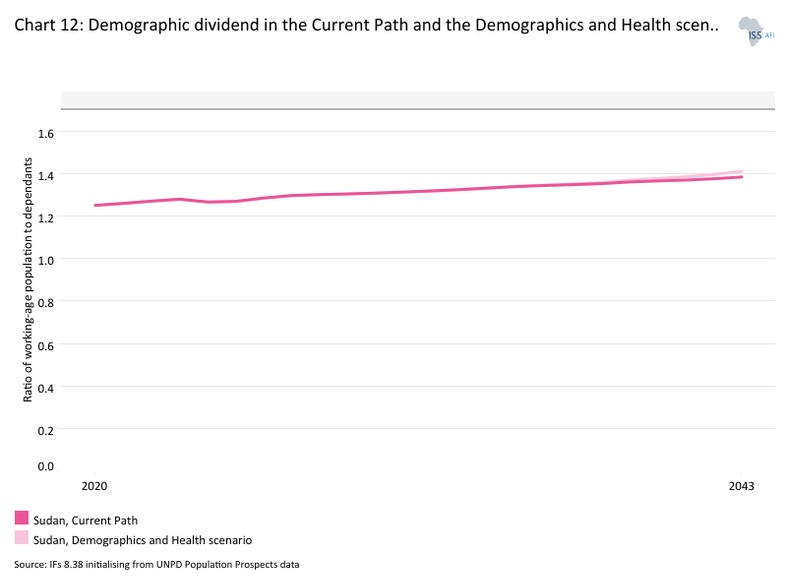

Chart 12 presents the demographic dividend in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The demographic dividend is the potential of economic growth generated by changes in the population structure. It generally materialises when the ratio of the working-age population to dependants is at least 1.7 to one, meaning that for every dependant, there are 1.7 persons of working age. When there are fewer dependants to care for, it frees up resources for investment in both physical and human capital. However, the growth in the working-age population relative to dependants does not automatically translate into rapid economic growth unless the labour force acquires the needed skills and is absorbed by the labour market. Without sufficient education and employment opportunities to harness their productive power, the growing labour force (especially in urban areas) could become increasingly frustrated by the lack of job opportunities, leading to social tension and even civil instability.

In 2023, the ratio of the working-age population to dependants in Sudan was 1.3 to one, which means that, on average, for every dependant in Sudan, there were only 1.3 persons of working age (15-64 years of age). This is slightly higher than the 1.2-to-one average for low-income countries in Africa. The high dependency rate in Sudan can be attributed to the high fertility rate, as discussed previously. On the Current Path, Sudan’s progress will lag and is unlikely to achieve the minimum ratio of 1.7 working-age persons per dependant required for the materialisation of the demographic dividend, even by 2043. Indeed, Sudan is likely only to achieve this minimum ratio by 2068.

The scenario also pushes the country close to the target such that, by 2043, the ratio of the working-age population to dependants will be 1.4 to one, slightly above the projections in the Current Path and almost on par with the average for its income-group peers in Africa. The growing size of the working-age population in Sudan can be a catalyst for growth if sufficient education and employment are generated to harness their productive power successfully. Otherwise, it could turn into a demographic 'bomb', as many people of working age may remain in poverty, potentially creating frustration, social tension and conflict. This means that Sudan needs to invest in educating its growing population and provide decent job opportunities, not to drag on growth.

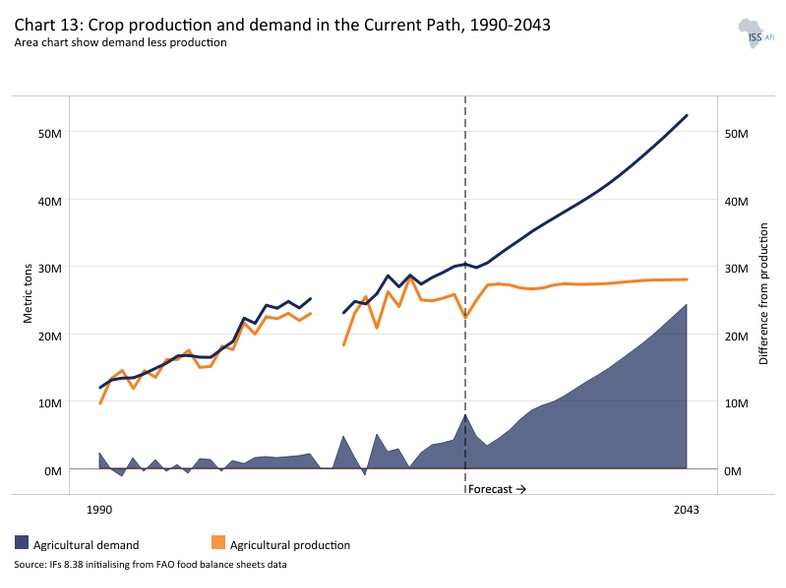

Chart 13 presents crop production and demand in the Current Path from 1990 to 2043.

The Agriculture scenario envisions an agricultural revolution that ensures food security through ambitious yet feasible increases in yields per hectare, thanks to improved management, seed, fertiliser technology and expanded irrigation. Efforts to reduce food loss and waste are emphasised, with increased calorie consumption as an indicator of self-sufficiency and prioritising it over food exports. Additionally, enhanced forest protection signifies a commitment to sustainable land use practices.

Visit the theme on Agriculture for our conceptualisation and details on the scenario structure and interventions.

Sudan was once the largest agricultural producer in Africa and the Middle East and has long been regarded as a potential “breadbasket” for the region and beyond. Agriculture remains the backbone of the Sudanese economy, with the majority of the population living in rural areas and depending on farming for both income and food security. The sector employs approximately 65% of the workforce and benefits from the country’s substantial agricultural resources, including an estimated 19.8 million hectares of arable land and access to 21% of the Nile’s water resources under regional agreements.

Sudan produces a wide variety of agricultural commodities, with cereals serving as the country’s primary staple crops. The main cereals include sorghum, millet and wheat. Sorghum is the most widely cultivated crop, followed by millet, which is predominant in regions such as Darfur and Kordofan. Wheat production is concentrated mainly in the Gezira and Northern states. In addition to staple crops, Sudan cultivates several cash crops that play a vital role in export earnings and rural livelihoods. These include cotton, sesame, groundnuts, sugarcane and sunflowers. Notably, sesame production has significantly improved household incomes in parts of Kordofan. Sudan also produces fruits and vegetables, such as watermelons, for both domestic consumption and export markets.

Following South Sudan's secession and the consequent loss of most oil revenues, Sudan’s government has renewed its focus on agriculture as a key driver of economic recovery and diversification. This shift has revived the country’s long-standing aspiration to become a regional agricultural powerhouse. However, the agricultural sector faces severe challenges, many of which have been exacerbated by the ongoing conflict. Fighting in key agricultural regions—particularly Darfur, Kordofan and Gezira—has disrupted farming operations. Looting of agricultural machinery, seeds and fertilisers has further reduced productivity.

Additionally, unsustainable land use practices have contributed to soil erosion and declining soil fertility. Rain-fed agriculture continues to yield far below regional averages, while limited access to quality seeds, fertilisers and agrochemicals further constrains output. The lack of irrigation infrastructure, storage facilities and transportation networks compounds these problems, resulting in post-harvest losses and reduced market access. Moreover, rising input costs and restricted access to financial services have made farming increasingly unprofitable for smallholder farmers.

To address these challenges, several initiatives and partnerships have been launched to support Sudan’s agricultural recovery. The government has identified agriculture as a strategic sector for international cooperation, particularly with partners such as Iran, focusing on knowledge-sharing and capacity-building programs. Policy efforts aim to improve farmers’ access to seeds, fertilisers and agrochemicals through strengthened local production and distribution networks. Concurrently, projects are underway to rehabilitate irrigation systems and improve rural transport infrastructure, thereby enhancing farmers’ market access. International organisations have also supported the development of agricultural input markets and implemented interventions to mitigate the effects of conflict on production.

Total agriculture production in 1990 stood at about 13 million metric tons. Of this, about 10 million metric tons, representing almost 72%, were crops, with the remainder constituting meat production. In 2022, before the war, total agricultural production had grown to 32.1 million metric tons. Of this, crop production constituted about 80.6% (25.4 million metric tons), meat production 19.1%, and fish production constituted the remainder of the total production. However, the prolonged conflict in Sudan has had a devastating impact on food production, leading to a 46% decline in staple crop output in 2023. This was primarily due to mass displacement, restricted access to agricultural inputs and the destruction of critical farming infrastructure.

The total demand for agricultural products in Sudan has consistently exceeded total production. Total demand stood at about 16 million metric tons in 1990, of which 12 million metric tons, equivalent to 75%, were for crops. The remaining demand was for meat (3.9 million tons) and for fish (33 000 tons). Comparing this to the total production (about 13.5 million metric tons) in the same year means that Sudan had an excess demand for agricultural products of about 2.5 million metric tons. Since then, domestic demand has rapidly outpaced production, and by 2022, agricultural demand exceeded domestic production by 4.5 million metric tons, despite increased production. Of the total demand of 22.9 million tons, 82.2% was for crops (30 million tons). The remaining demand was mainly for meat (6.4 million tons), and the lowest demand was for fish (52 000 tons).

The conflict has plunged millions into food poverty and famine conditions. More than 19 million people—approximately 40% of Sudan’s population—are facing severe food insecurity, and the situation is projected to worsen further. Key grain-producing regions, including Darfur, Kordofan and Gezira, have been particularly affected, with some areas experiencing harvest losses of nearly 50%. The destruction of infrastructure, theft of farming assets and trade disruptions have made food increasingly scarce, while continued violence perpetuates a vicious cycle of hunger, displacement and instability.

Despite the projected increase in domestic production, reaching 33.8 million metric tons in 2030 and 37.8 million metric tons in 2043, it will not be enough to meet domestic demand that will rapidly grow to 42.6 million metric tons and 62.1 million metric tons in the same period, respectively. As a result, excess demand for agricultural products will reach 9.3 million metric tons in 2030 and 24.3 million by 2043. This indicates that Sudan faces the risk of food shortages in the future if drastic measures are not taken to revamp the agriculture sector to increase domestic production to meet its growing demand.

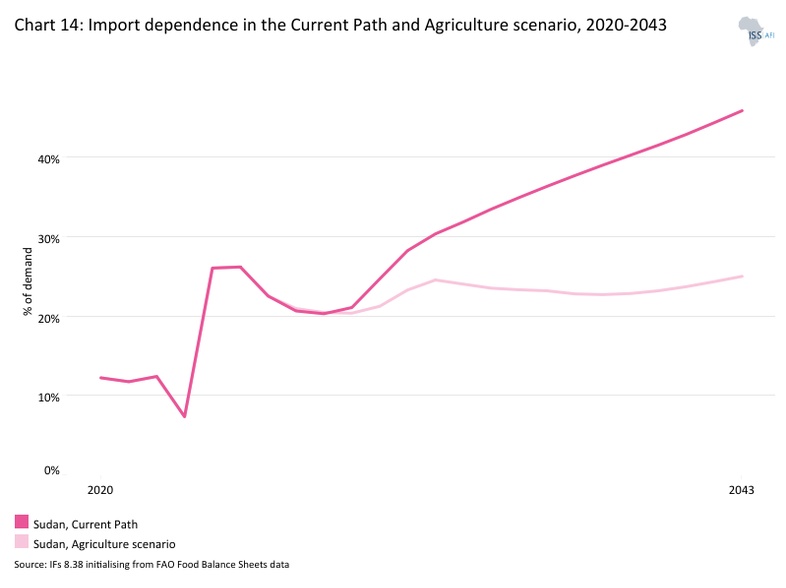

With total agricultural demand outpacing domestic production, Sudan is likely to continue relying on imports to meet its domestic demand. In 2022, Sudan’s net import of crops stood at 12.4% of total crop demand, exceeding the average of 7.9% for low-income countries in Africa. In the Current Path, net crop imports in Sudan will grow rapidly to 24.7% and 45.9% of total crop demand by 2030 and 2043, respectively. This suggests a growing level of national food insecurity in Sudan.

Chart 14 presents the import dependence in the Current Path and the Agriculture scenario, from 2020 to 2043.

In the Agriculture scenario, yields per hectare will increase to 2.2 metric tons by 2043, a 57% improvement compared to the Current Path projection and the average of low-income countries in Africa. Higher yields will boost crop production. In the Agriculture scenario, total crop production will rise to 45.3 million tons, almost 17.2 million metric tons, or 61.2%, more than the Current Path by 2043. The projected increases in crop production under the Agriculture scenario reduce the country's crop import dependency compared to the Current Path. By 2043, the net import of crops will decline to 25.0% in the Agriculture scenario, far below the projected Current Path average of 45.9%. This implies that, despite the devastating impact of the conflict on Sudan’s agriculture sector, the country still has the potential to reduce its food import and become food-sufficient if the conflict ceases and significant steps are taken to revamp the agricultural sector.

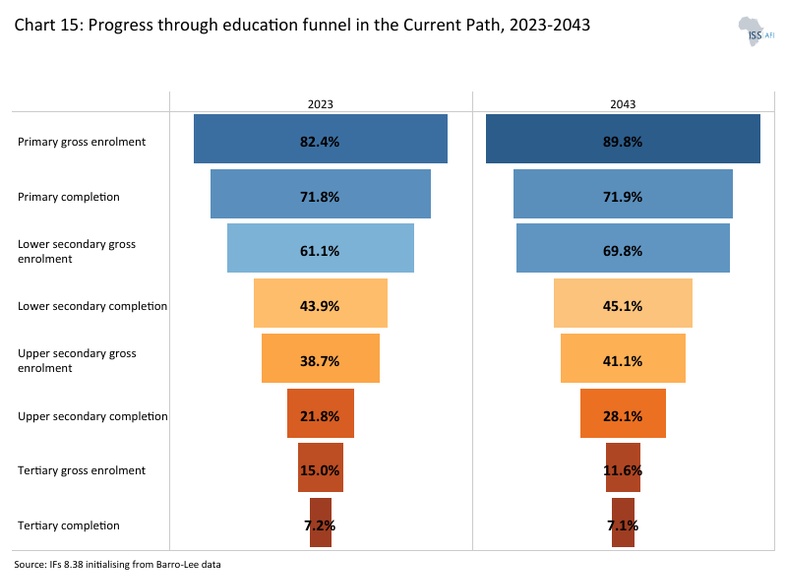

Chart 15 depicts the progress through the educational system in the Current Path, for 2023 and 2043.

The Education scenario represents reasonable but ambitious improvements in intake, transition, and graduation rates from primary to tertiary levels and better quality of education at primary and secondary levels. It also models substantive progress towards gender parity at all levels, additional vocational training at the secondary school level, and increases in the share of science and engineering graduates.

Visit the theme on Education for our conceptualisation and details on the scenario structure and interventions.

The education system can be likened to a long funnel through which children enter at the primary level and exit upon completing tertiary education. However, in Sudan, as in many sub-Saharan African countries, the funnel is leaky, with numerous cracks along the way. While many children enter the system at the mouth of the funnel, only a few complete the entire journey from primary to secondary and eventually to tertiary education. Even before the current conflict, educational enrolment rates in Sudan were significantly lower than those of comparable African countries. This situation has been severely worsened by the ongoing conflict, leading to a profound crisis.

The education system has been decimated at all levels as a result of the ongoing war. More than 19 million school-aged children have experienced disruptions in their education, with only 20% of schools currently operational. Many educational facilities have been destroyed, repurposed as shelters or occupied by armed groups. Even before the conflict, the education sector suffered from chronic underfunding, inadequate infrastructure and political instability. Today, widespread poverty and soaring inflation have rendered schooling unaffordable for many families, while teachers often go months without pay, further undermining the sector’s capacity.

Several policies and initiatives have been introduced to address these challenges. Plan International advocates for safe and inclusive access to education in conflict zones. At the same time, UNESCO has launched programs to reopen schools, improve teaching quality and mobilise resources for system-wide recovery. In addition, the Global Partnership for Education (GPE) has funded a US$41.9 million program to support 3 000 schools, enhance remote learning opportunities and provide remedial programs for vulnerable children. Efforts are also underway to integrate technology into education, although these are constrained by limited infrastructure.

Despite these interventions, the education sector continues to face severe obstacles. The destruction and repurposing of schools due to ongoing violence have displaced millions of students and teachers. High poverty levels and rising living costs have made education increasingly inaccessible, while many teachers have abandoned their posts because of unpaid salaries and unsafe working conditions. Girls are particularly at risk of dropping out of school due to child marriage, domestic labour responsibilities and safety concerns. Digital learning efforts are further hindered by low internet penetration and low computer ownership.

In 2022, the gross enrolment rate for primary school students in Sudan was 82.1%, a significant improvement from 60% in 2001, but still well below the average of 106.3% for low-income countries in Africa. Comparing this to the net enrolment rate of 63.6% in the same period leads to two important conclusions. First, a significant number of school-age children in Sudan are out of school (as reflected in the low net number). Secondly, many classrooms in Sudan are likely to be crowded with older students (as reflected in the high gross number).

In the Current Path, Sudan's gross enrolment rates will reach 83.3% and 89.8% in 2030 and 2043, respectively. In the same period, the net enrolment rate will be 64.0% in 2030 and 67.4% by 2043. At this rate of progress, the country will still lag behind the average of its income-group peers in Africa. The gross primary completion rate stood at almost 70.5% in 2023, above the average of 59.1% for low-income countries in Africa, indicating that a sizable number of children who enrolled did not complete the last grade of primary school in Sudan. On the Current Path, Sudan’s progress in ensuring more children complete primary school will be slower, reaching 72.7% in 2030, slightly below the average of 73.5% for its income peers in Africa. By 2043, the primary completion rate in Sudan will rise to 71.8%—still below the average for African low-income countries at 83.2%.