14 Climate

14 Climate

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This theme on Africa’s Climate Futures explores the trends related to climate change. It focuses on Africa's unique position as a minor emitter of global carbon, yet a region disproportionately affected by the impact of climate change. We model Africa’s energy demand and carbon emissions, with fossil fuels and deforestation as major contributors, and then discuss strategies for mitigation and adaptation, including a global carbon tax.

The analysis here complements the separate theme on Africa’s Energy Futures. Energy production and carbon emissions are closely linked, and we use the same scenarios across the two themes. We use 2050 as a standard reference year to enable comparisons with global ambitions such as ‘getting to net zero by 2050’ and extend the forecast horizon to 2063 to allow for outcomes to align with the African Union’s Agenda 2063 long-term vision for Africa.

For more information about the International Futures (IFs) modelling platform used for our forecasts and scenarios and the environment and energy modules, please see the Technical page.

Summary

The theme begins with an overview of the current climate crisis, highlighting the unprecedented rise in global meteorological records and climate-related disasters over the past decade.

Next, we examine the disproportionate impact of climate change on Africa. Despite contributing minimally to global carbon emissions, the continent faces severe consequences due to its limited adaptive capacity. Climate change exacerbates Africa’s vulnerabilities, compounding natural disasters and socio-economic challenges.

We then analyse global carbon emissions, emphasising fossil fuel consumption as the main driver of rising temperatures and extreme weather. In 2024, emissions from fossil fuels reached an all-time high, with projections suggesting a peak in 2037/38 before declining. However, even this decline is unlikely to prevent a global temperature rise of 3 °C above pre-industrial levels by the century’s end.

Amidst these challenges, we explore Africa’s energy dilemma: the continent’s pressing need for economic growth and energy expansion versus the constraints of a limited global carbon budget. Even under a net-zero scenario, CO2 concentrations will continue rising due to historical emissions, underscoring the necessity of carbon capture and sequestration efforts.

Currently, Africa accounts for less than 5% of global fossil fuel emissions. On the Current Path, this share will rise to 9% by 2050 and 10.5% under a high-growth Combined scenario, which integrates ambitious improvements across eight sectors.

To address these challenges, we propose two strategic approaches alongside the rapid renewable energy transition explored in the Energy theme:

- Africa’s role as a global carbon sink – leveraging sequestration efforts.

- A global carbon tax – assessing four tax models and identifying the Differentiated Pay scenario as the most equitable, where contributions are based on income classification.

Integrating the Differentiated Pay model into the high-growth Combined scenario results in the Sustainable Africa scenario, which balances emissions reduction with economic growth. By 2050, Africa would emit 7.5% less carbon than on the Current Path while achieving an annual economic growth rate of 7.7% (compared to 4.3% under the Current Path). Despite these reductions, energy demand in 2050 would still be 30% higher, reaching 10.7 barrels of oil equivalent per capita by 2063.

Finally, we emphasise the need for further policy exploration, such as greater utilisation of municipal solid waste. The report concludes with a set of recommendations for decision-making to achieve sustainable development and climate resilience, highlighting the importance of global cooperation and support.

All charts for Climate

- Chart 1: Global yearly temperature anomaly, 1880-2024

- Chart 2: Greenhouse gas emissions by gas, 1853-2023

- Chart 3: Climate change impact on agricultural yields, precipitation and temperature, 2020-2063

- Chart 4: Africa’s climate disasters, 2014-2024

- Chart 5: CO₂ emissions for top 10 emitters vs the rest of the World, 2023-2063

- Chart 6: Land use by type, 2020-2063

- Chart 7: Water use vs supply, 2020-2063

- Chart 8: Africa's contribution to CO₂ emissions from fossil fuels, 1963-2063

- Chart 9: Africa’s CO₂ emissions, 2020-2063

- Chart 10: Carbon emissions from deforestation: Current Path vs Agriculture scenario, 2020-2063

- Chart 11: Global carbon tax scenarios

- Chart 12: CO₂ emissions in different Carbon tax scenarios, 2020-2063

- Chart 13: CO₂ concentration in atmosphere in different Carbon tax scenarios, 2020 vs 2063

- Chart 14: CO₂ emissions in different scenarios, 2020-2063

- Chart 14: Recommendations

In its landmark 2022 Global Land Outlook report, the UN Convention to Combat Desertification warns, 'At no other point in modern history has humankind faced such an array of familiar and unfamiliar risks and hazards, interacting in a hyper-connected and rapidly changing world.'

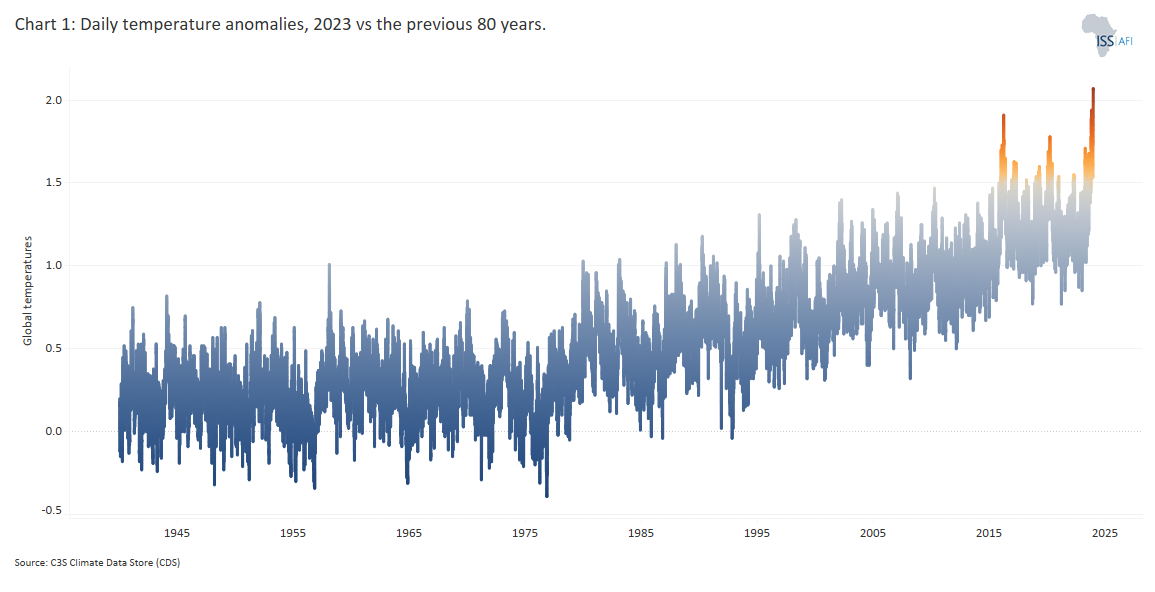

In early January 2025, the Copernicus Climate Change Service (C3S) confirmed that 2024 was the warmest year on record and the first calendar year with global surface air temperature exceeding the pre-industrial reference period (1850-1900) by 1.5oC. The daily temperature anomalies for 2024 compared to the previous 80 years, extracted from the C3S data server, are presented in Chart 1.

In addition to record-breaking temperatures, 2024 and the beginning of 2025 saw unprecedented extreme weather events across the globe, including prolonged heatwaves in North Africa, devastating wildfires in the Sahel, severe flooding in Southern Africa, and massive wildfires across the western United States, particularly in California and Oregon. In the words of the Secretary-General of the United Nations (UN): ‘The era of global warming has ended; the era of global boiling has arrived’.

The consequences of the climate crisis extend far beyond rising temperatures to widespread ecosystem collapse, more frequent and severe weather patterns and increased displacement of vulnerable communities. Scientists attribute a discernible surge in weather-related disaster frequency and losses in the past two decades to climate change. Since 1984, 11 640 weather-related disasters were recorded in the International Disaster Database (EM-DAT), of which 62% occured after 2004. The growing disaster losses trend highlights the intensification and acceleration of the challenges posed by climate change.

Concurrently, climate-induced displacement is also rising, with millions of people forced to relocate due to the adverse effects of changing weather patterns. According to the database of the Internal Displacement Monitoring Centre (IDMC) more than 240 million internal displacements occurred between 2013 and 2023 due to natural disasters (the vast majority due to storms and floods). 2022 proved particularly disruptive with 32 million people displaced in countries such as the Phillippines, Nigeria, India, China, Pakistan, Somalia, Bangladesh and Ethiopia due to flooding, storms and droughts.

The unfolding crisis underscores the widening gap between current global climate policies and the ambitious targets set by the 2015 Paris Agreement. This agreement sought to limit global temperature increases to below 2°C above pre-industrial levels, with a concerted effort to strive for a more ambitious 1.5°C limit. However, recent data suggests that the 1.5°C threshold has already been breached, signalling an urgent need for enhanced adaptation and mitigation measures.

Strengthening climate adaptation efforts is essential and should align with the Sendai Framework for Disaster Risk Reduction, which was adopted in 2015. This framework underscores the importance of reducing disaster risk and building resilience in the face of rising natural hazards, acknowledging the interconnectedness of climate change, disasters, and sustainable development. Additional frameworks, such as the Global Adaptation Goal (GAG) and the Adaptation Communication under the United Nations Framework Convention on Climate Change (UNFCCC), also provide avenues for enhancing international cooperation on adaptation strategies.

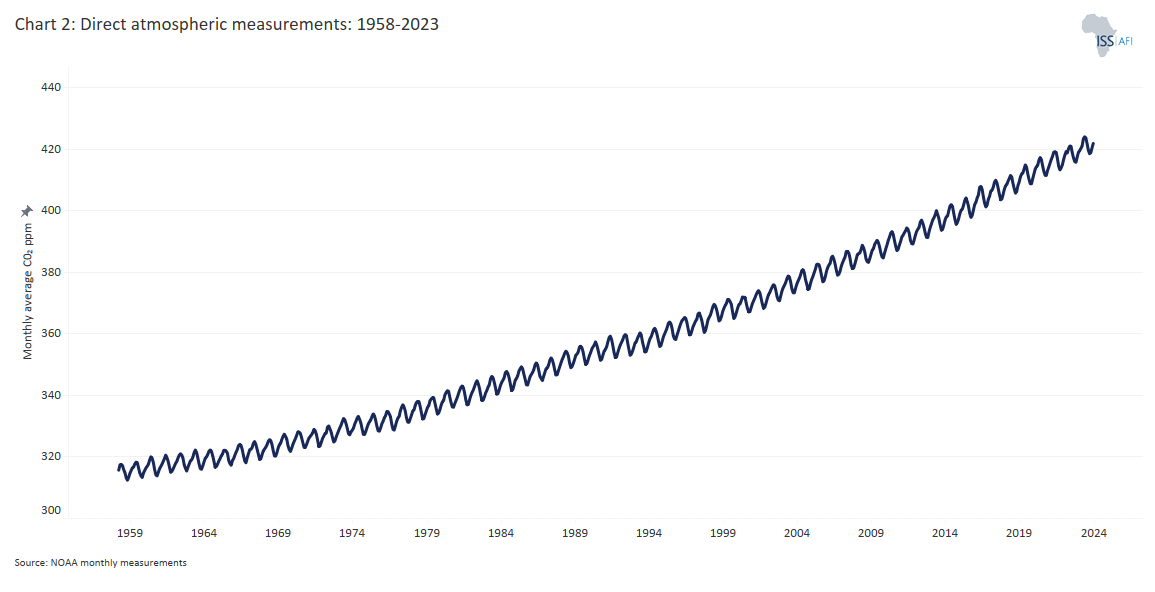

Yet, despite numerous frameworks and policies and the well-established understanding that a growing population and human-induced activities, notably fossil fuel burning and unsustainable land use practices, have been significant contributors to the climate crisis, global average concentrations of carbon dioxide (CO2) in the atmosphere have persistently risen year after year, reaching record high levels in 2024. The World Meteorological Organization (WMO) has warned that human activities have raised the CO2 content in the atmosphere by more than 50% from pre-industrial levels, warming the planet to the unprecedented levels observed today. In May 2024, CO2 in the atmosphere was recorded at 426.7 parts per million (ppm) over Hawaii’s Mauna Loa Observatory, a staggering increase from the 320 ppm recorded in 1960 and the pre-industrial levels of 280 ppm. The data in Chart 2 on direct atmospheric CO2 measurements from 1958 to 2024 is extracted from NOAA monthly measurements. These alarming trends underscore the urgent need for immediate and sustained action to mitigate rising temperatures and escalating climate disruptions.

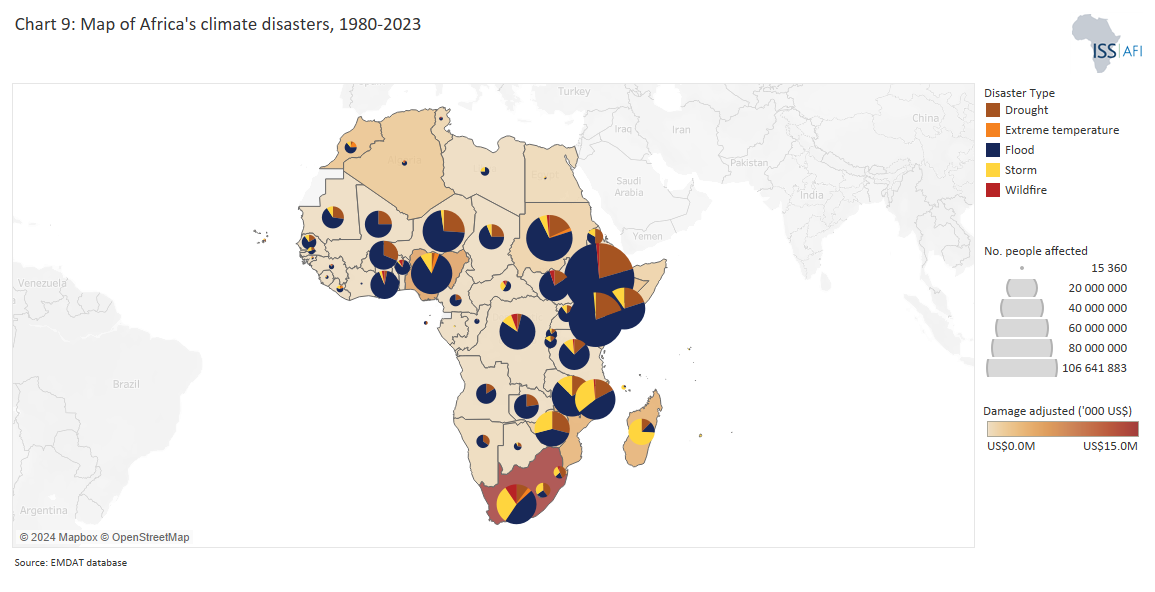

Africa has historically contributed little to the climate crisis but bears a disproportionate burden of severe climate change impacts. The continent grapples with escalating challenges, including rising temperatures, water stress, heat-related mortality, diminished food production, increased extreme weather events, climate-induced displacement, biodiversity loss, worsening air quality and the spread of climate-sensitive diseases. These impacts foster conflict and insecurity, reduce investor confidence and complicate governance in a region with many of the lowest infrastructure, health, education and human development indicators globally. According to the EMDAT database, since 1984, Africa has endured 1 865 climate-related disasters, accruing US$53 billion in direct financial losses and affecting an estimated 702 million people. In 2024 alone, Africa witnessed some of the most severe climate-related disasters, including widespread flooding in East Africa, which affected more than 700 000 people, and the worst drought in Southern Africa in a century, leaving 27 million people, including 21 million children, facing food insecurity.

Climate-related disasters now account for nearly 70% of all natural disasters, with extreme weather events increasing in frequency and severity. 2024 saw 73 devastating climate-related disasters on the continent, 40 of which were attributed to flooding alone, collectively impacting nearly 10 million people. Other extreme events included prolonged droughts in Southern Africa, cyclones along the southeastern coast, and heatwaves across North and West Africa, exacerbating food insecurity and displacement.

Compounding the crises is Africa’s high vulnerability to climate-related disasters. With almost 30% of the population living in absolute poverty, the continent grapples with systemic challenges that exacerbate the impact of any natural disaster. Limited infrastructure, slow economic growth and fragile governance exacerbate Africa’s climate risks. Governments in many African countries lack the agility and resources needed for effective disaster response. Political instability, logistical hurdles and corruption frequently delay aid and relief efforts, weakening community resilience.

The effect of climate change differs significantly across Africa. Chart 3 illustrates the anticipated impact on agricultural yields, precipitation changes and temperature anomalies by region from 2020 to 2063.

Further contributing to the high vulnerability rates is the continent's stark wealth disparity, particularly in Southern Africa, which has some of the highest inequality rates globally, with countries like South Africa and Namibia ranking among the most unequal in the world. Limited investment in critical infrastructure exacerbates vulnerabilities and increases exposure to hazards, leaving critical resources such as healthcare facilities and transportation networks unable to withstand the onslaught of climate-related disasters.

Many African nations are still struggling to recover from economic shocks induced by the 2008 financial crisis, the COVID-19 pandemic and escalating climate-induced infrastructure damages. Alarmingly, only 9% of the direct climate-related disaster losses incurred over the past four decades on the continent were insured, leaving governments, communities, and families without the necessary means to recover and rebuild in the aftermath of these disasters. This lack of financial protection pushes vulnerable communities into deeper poverty and increases their long-term risks. Ecosystem degradation and biodiversity loss further diminish the capacity to buffer against catastrophe. The subsequent deforestation and soil erosion escalate the risk of floods, amplifying the magnitude of their impact on vulnerable communities.

Chart 4 presents the number of climate-related disasters in Africa by type. Water-related disasters emerge as the continent's Achilles' heel, constituting 82% of all climate-related incidents. The precarious balance between too much water in the form of floods and too little during droughts underscores the urgent need for adaptation interventions.

South-east Africa is disproportionately exposed to severe weather events, including convective storms, tropical lows, cut-off lows and cyclones. The devastating impact of Cyclone Freddy (the longest-lasting and most intense[1The most ambitious transboundary project in Africa to fight desertification, land degradation and climate change is the Great Green Wall (GGW) initiative introduced in 2007 by the African Union. The project aims to restore 100 million hectares of degraded land, capture 250 million tons of CO2 and contribute to creating 10 million jobs by 2030. At the COP26 conference in 2021, the EU reconfirmed their commitment to the GGW with an additional annual commitment of US$ 700 million, pushing the global commitments to this programme to €19 billion.] tropical cyclone ever recorded), which caused widespread devastation in Mozambique, Malawi, Zimbabwe and Madagascar in 2023, and the 2022 devastating floods in the KwaZulu province of South Africa (caused by an intense cut-off low-pressure system) are worrying examples. The warming Indian Ocean along Africa’s east coast is fuelling the intensification of cyclones. As temperatures rise, intense weather events are becoming more frequent and destructive. The escalating exposure to such disasters will exacerbate existing vulnerabilities on the continent, further challenging the resilience of communities and countries alike.

The Horn of Africa, too, is particularly vulnerable to droughts, floods and disease outbreaks as years of conflict and instability have eroded community resilience. The region recently experienced one of the worst droughts recorded in history, and critically high food insecurity and conflict have contributed to large-scale internal displacement across the region. The 2023 estimate of 12.15 million internally displaced and almost 60 million food insecure people was a noticeable increase from the 37 million recorded in 2022. Climate projections differ in their forecasts for rainfall in the region. Still, there is agreement that the area is drying due to increased evapotranspiration and that a noticeable rise in the frequency of extreme events is highly probable. Given the high reliance on subsistence farming and the prominence of the agricultural sector, food insecurity and shortages will likely rise.

On the other side of the continent, large areas in the Sahel and West Africa risk transforming into a desert landscape. The susceptibility to desertification is especially noticeable in the Sahel, a transitional zone between the Sahara Desert to the north and the more fertile and moist regions to the south. Climate change will increase erratic rainfall patterns and prolonged droughts in this region, exacerbating existing socio-economic challenges in an area considered highly unstable. The region's exposure to climate change and the meagre adaptive capacity pose significant risks to human well-being. As with the Horn, increased population displacement is unfolding as arable land diminishes and pastoral communities face intense challenges to sustaining their livelihoods.

Climate change in Africa is significantly reshaping the landscape of diseases, affecting both infectious and non-communicable diseases. Rising temperatures and alterations in rainfall patterns are shifting the prevalence of diseases like malaria, dengue, measles, etc. Despite breakthroughs in vaccine development offering promise, the heightened risk in countries grappling with underlying socio-economic challenges and strained healthcare systems is apparent, as exemplified by the recorded disease outbreaks in the Horn of Africa in 2023. Disease outbreaks, including polio, meningitis, malaria, measles, dengue, cholera and anthrax, underscore the vulnerability of areas facing climate-induced health challenges.

Outbreaks of water-borne diseases, including cholera and diarrhoeal illnesses, are also likely to become more prevalent due to prolonged droughts and intense flooding impacting water quality and sanitation systems. A case in point is Malawi, where such conditions have escalated the risk of water-borne diseases, necessitating enhanced public health interventions in early 2023. South Africa also saw the outbreak of a severe Cholera epidemic in early 2023, as rising temperatures and failing sanitation and water management contributed to the disaster.

Climate change also affects respiratory health, particularly in urban areas marked by industrialisation and increased transportation activity. Elevated temperatures and shifting precipitation patterns contribute to ground-level ozone and particulate matter formation, exacerbating respiratory conditions.

Vulnerable population groups, such as the elderly, those with pre-existing health conditions and children, face an elevated risk of heat-related illnesses like heatstroke. In 2003, a heatwave cost the lives of 72 000 people in Europe, showing just how deadly the urban heat island effect can be and underscoring the need for targeted healthcare interventions and public health initiatives to safeguard the well-being of these populations. Heat-related illness and death are severely underreported in Africa and difficult to monitor. Still, a WHO study showed that heat-related deaths among the elderly in South Africa can climb from a baseline of two deaths per 100 000 to as many as 20 to 50 deaths per 100 000 by 2050. Rising temperatures also threaten African cities as urbanisation continues amidst poor planning a lack of housing regulations and insufficient use of heat-resistant building materials.

Economic progress and social development are tied to energy use, transportation and consumption. Achieving sustainable advancement becomes nearly impossible without acknowledging and mitigating the significant environmental impact associated with the cumulative effect of carbon emissions over time. It underscores the historical reliance of most countries on fossil fuels for their growth and development and the efforts that will be needed to decouple economic growth from carbon emissions including from fossil fuel combustion, deforestation, land use changes, waste management, manufacturing processes and land degradation. A growing global population inevitably increases energy, food and economic demands, and Africa is at the front of the queue.

Emissions can be calculated variously, such as by the economic sector (construction, transportation, energy, etc.), and methodologies and numbers differ between agencies and organisations. According to the Intergovernmental Panel on Climate Change (IPCC), around 86% of global carbon dioxide emissions in 2020 were due to fossil fuels and industry processes (70-75% directly from fossil fuel combustion and 10-15% from industrial processes). More than half of the world's greenhouse gas emissions in 2023 can be linked to just 36 fossil fuel and cement producers. The top five state-owned emitters are Saudi Aramco, Coal India, CHN Energy, National Iranian Oil Company and Jinneng Group. The top five investor-owned emitters are ExxonMobil, Chevron, Shell, TotalEnergies and BP.

In this theme, our focus is on carbon emissions from fossil fuels (coal, oil and gas), unless indicated otherwise.

Among the three sources of fossil fuels, coal has the most significant carbon emissions. Natural gas produces lower carbon emissions and air pollution than coal and oil but releases methane (a potent greenhouse gas) and other non-CO2 pollutants. Methane is more than 80 times more potent than carbon dioxide as a greenhouse gas when considered over 20 years. As a result, even small methane emissions can have a significant climate impact. In 2021, natural gas production accounted for 40 million tons of methane emissions, roughly equivalent to the methane emissions generated by the entire oil industry.

According to the International Energy Agency (IEA), coal contributed almost 44% of global carbon emissions from fuel combustion in 2021, closely following oil at 32% and natural gas at 22%. However, whereas oil and coal can be loaded and transported in bulk over long distances, such as by ship, transporting natural gas in bulk over long distances requires a pipeline or by compressing and cooling it down to form liquefied natural gas (or LNG) prior to movement, which then has to be regasified again on the other side - an extremely energy intensive and costly process. Emissions increase if the LNG is mainly produced from shale gas that emits a substantial amount of methane, which increases during liquefaction and tanker transports, as is the case with the United States, now the world's largest exporter. According to Robert Howarth's writing in 2024

Shale gas production is quite energetically intensive, and the related carbon dioxide need to be considered in any full lifecycle assessment of the greenhouse gas emissions associated with LNG. Further, methane emissions from shale gas can be substantial. Since 2008, methane emissions from shale gas in the US may have contributed one-third of the total (and significant) increase in atmospheric methane globally.

Howarth’s analysis concluded that LNG is 33% worse in greenhouse gas emissions over 20 years than coal and is often not cost-competitive with other fossil fuels. Even 100 years after emission, the LNG footprint from methane equals or exceeds that of coal. The results of that study made the Biden administration reconsider increased LNG exports pending further analysis of the consequences.

Concerns regarding the impact of carbon emissions have led to a dramatic increase in renewables, particularly solar and wind. In its ‘Renewables 2024’ report, the IEA states that 510 gigawatts (GW) of renewable energy capacity was installed globally in 2023, increasing the installed base to about 3 600 GW, with solar photovoltaic (PV) accounting for three-quarters of worldwide additions.

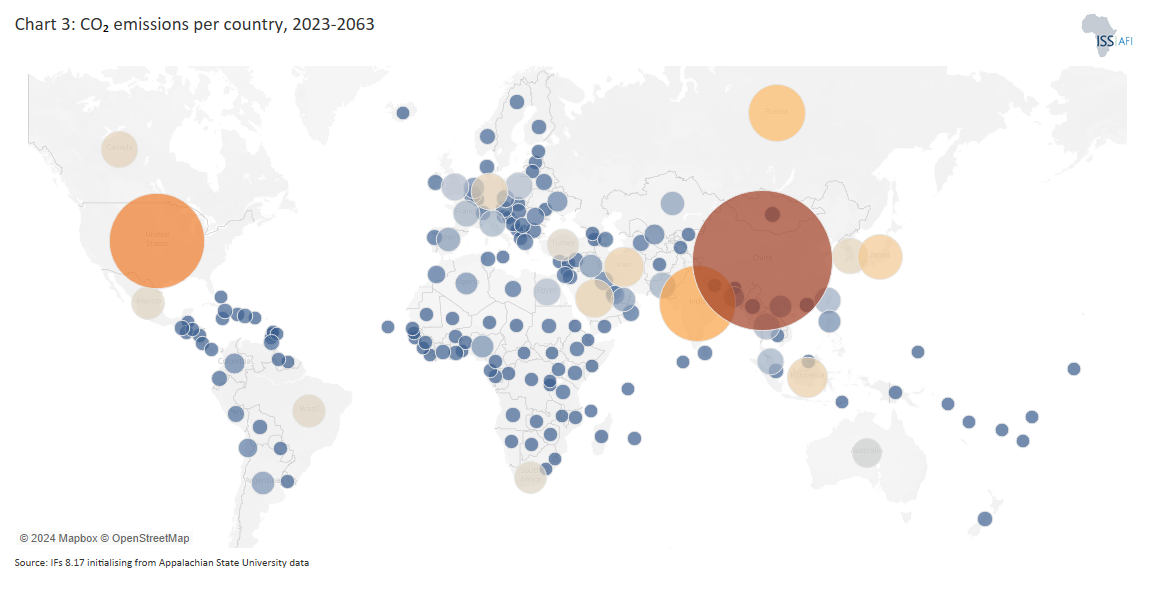

Chart 5 presents the progression of global carbon emissions from fossil fuels (i.e. excluding emissions from other sources such as deforestation and manufacturing) since 1990, with a forecast to 2063. In 2020, due to the significant economic slowdown caused by the COVID-19 pandemic, global emissions from energy combustion and industrial processes decreased by 5.8% compared to 2019. Then, as economic activities bounced back from the pandemic, emissions rebounded sharply. By 2023, CO2 from fossil fuels has surged to over five times the levels observed in 1960, reaching 36.1 billion tons of CO2 equivalent annually (the most ever recorded). The most significant contributors to these emissions are China, the USA, India, Russia, Japan, Indonesia, Iran, Germany, Saudi Arabia and South Korea. These top 10 global emitters collectively account for a substantial 69% of global fossil fuel emissions, 61% of the world's GDP and house 60% of the worldwide population.

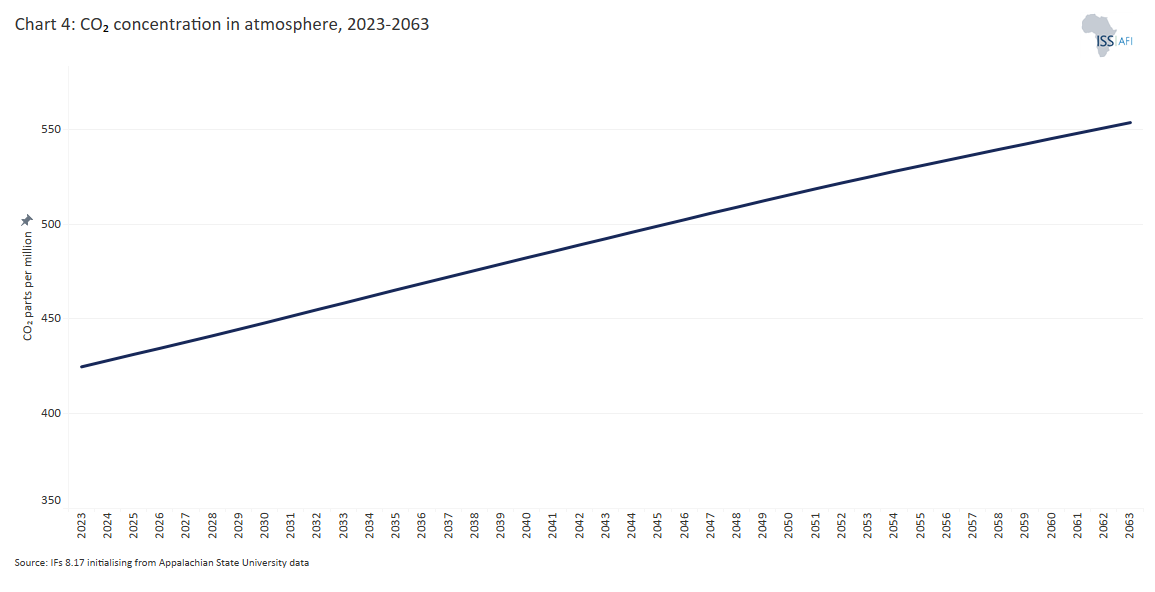

Despite gradual shifts in developed economies toward renewable energy sources, current mitigation efforts remain insufficient. As of 2024, atmospheric carbon dioxide (CO₂) concentrations have reached unprecedented levels, with a measured concentration of 427 parts per million (ppm) (Chart 2), a significant increase from pre-industrial levels of 280 ppm. Without a solid collective response and without a breakthrough in carbon sequestration technologies, atmospheric concentrations will accumulate, reaching 551 ppm by 2063 and 569 ppm by the end of the century. The Intergovernmental Panel on Climate Change Sixth Assessment Report states that atmospheric concentrations in 2050 should be around 330 to 400 ppm to keep the 1.5°C ambition alive. Such elevated atmospheric CO2 levels pose a significant risk, intensifying global warming and placing the world on a trajectory that can see global temperatures rise by at least 3°C above pre-industrial levels by the end of the century. It will intensify the adverse impacts on ecosystems, weather patterns and vulnerable communities particularly in Africa which has the least capacity to cope. Thus, 'the world has been locked into a path that will force us to focus on adaptation for survival.'[2Food and Agriculture Organization of the United Nations (FAO)] Without decisive action, the escalating trajectory of CO₂ concentrations will continue to drive severe climate-related challenges globally, potentially triggering critical tipping points.

The Current Path suggests an increase in carbon emissions from fossil fuels with a peak of 37.14 billion tons of CO2 equivalent per annum in 2037/8 and subsequent rapid decline back to 2020 emission levels in by 2049, aligning with various Nationally Determined Contributions (NDCs) and ongoing global initiatives to decarbonise economies. The plateauing and decline is primarily driven by expected emission reductions from China, the US, India and Europe. Still, the eventual rate of decline will be principally affected by what happens with carbon emissions from Africa, given its current low levels of development, energy deficits, high rate of addiction to fossil fuels compared to other regions, and rapidly growing population.

China, the largest carbon emitter globally, is rapidly shifting from fossil fuels to renewables, evidenced by a significant increase in low-carbon electricity generation, especially from wind and solar sources. The substantial investments in low-carbon technologies, such as solar, electric vehicles and batteries, reflect the nation's stance on domestic and international climate policies. While China's substantial reliance on coal for energy may keep emissions elevated in the coming decade, the surging investments in clean energy production and its NDC commitments will see the country emerge as a critical player in the global transition towards cleaner energy sources.

The United States, currently the world's second-largest greenhouse gas emitter, is experiencing a more gradual tardy reduction in emissions - the result of fluctuating commitments to climate policies. The country is heavily dependent on fossil fuels, and the significant setbacks caused by the first Trump administration, which withdrew from the Paris Agreement and dismantled key carbon reduction policies like the Clean Power Plan. According to a study by the Rhodium Group, President Trump's actions during those years are estimated to have contributed an additional 1.8 billion tons of CO2 into the atmosphere by 2035. The Biden administration subsequently made notable strides in recommitting to the Paris Agreement and investing in renewable energy infrastructure (most prominently with the introduction of the Inflation Reduction Act in 2022). The return of Trump to the White House in 2025 has already undone some of this progress. Already Trump signed an executive order to withdraw the US from the Paris Agreement for a second time. Looking ahead, the US appears to be placing emphasis on technological advancements within the petroleum and gas industries, such as green hydrogen production and carbon sequestration projects. However, these technologies are still in developmental stages and have not yet been proven at scale.

Compared with China, India and the US, the EU27 has the most comprehensive approach to combating climate change, including efforts to spur changes in consumer behaviour to cut emissions drastically. Other efforts include setting vehicle emission targets, defining requirements for building renovations, and adopting carbon pricing by expanding its market-driven emissions trading scheme at the heart of Europe’s decarbonisation plan. The result, the European Green Deal, embeds emission targets within the EU27 industrial policy. In the process, the EU has now legally enshrined its commitment to reduce emissions by at least 55% by 2030 compared to 1990 levels and achieve net-zero emissions by 2050.[3Vulnerability refers to a catch phrase that encompass socio economic vulnerability (inclusive of household composition, education, health status, basic service access, safety and security constraints and inequality)] Among other measures, the EU has started phasing in a carbon border adjustment mechanism (EU CBAM) since May 2023.

Emerging economies are contributing an ever-growing percentage to the global total emissions. With a rapidly growing population and expanding industrial sector, India is set to increase its carbon emissions significantly in the coming decades. The country's heavy reliance on coal for energy production and its ambitious development goals present a considerable challenge in mitigating greenhouse gas emissions. Despite efforts to diversify its energy mix and promote renewable energy sources, coal continues to dominate India's energy sector due to its affordability and accessibility.

India's industrial growth and urbanisation further contribute to rising emissions as manufacturing, construction and transportation sectors expand to meet the demands of a growing population and economy. Moreover, the country's reliance on fossil fuels for transportation and household energy needs adds to its carbon footprint. As a result, India may overtake the US to become the world's 2nd-largest carbon emitter by mid-century, with Russia in fourth position, followed by Indonesia.

A growing population and significant land use changes, including deforestation of its rainforests, drive Indonesia’s associated increased carbon emissions.

Nigeria will likely emerge at the 9th spot globally (and largest emitter from Africa) by 2050, followed by Egypt at number twelve. Iran, Japan, Canada, Turkey and Pakistan are all likely to be part of the top tier of countries that emit large volumes of carbon from fossil fuel use.

While Chart 5 depicts carbon emissions from burning fossil fuels, the contribution from land use management practices (deforestation, agriculture, soil erosion and changes in land use) is also important. Second to energy, the agriculture sector is responsible for most carbon emissions. Land use change and management (e.g. clearing forests or grasslands for agricultural fields) is a significant source of greenhouse gas emissions. In contrast, undisturbed and flourishing land ecosystems that serve as important carbon sinks. In addition to the substantial role of forests in carbon sequestration, grassy ecosystems (such as savanna and grasslands) store a significant amount of carbon in the soil, primarily within their extensive root systems and decaying organic matter. Grasses account for over half of the soil carbon content across tropical savannas, highlighting the need to avoid cultivating and tilling them.

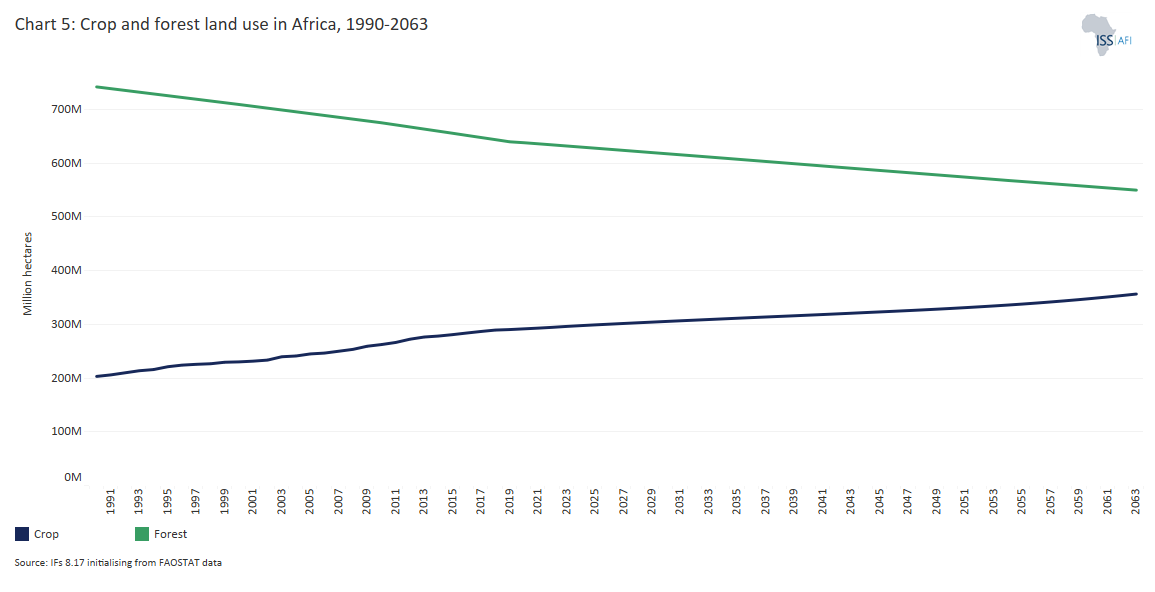

Globally, agricultural land is expanding, with a growing global population and increasing food needs. In Africa, crops, grazing and urban land have been expanding unabatedly at the cost of forests and grasslands. In the last three decades, 100 million hectares of forest have been cleared to make way for 66 million hectares of crop land[4internal displacement monitoring centre]. In the Current Path (Chart 6), forests in Africa will shrink by 14% from 2023 to 546 million hectares by 2063. Much of this will come as cropland in Africa expands from 301 million hectares in 2023 to 357 million hectares, while grazing land will grow from 876 million to 990 million hectares. As Africa’s population expands and urbanises, subsequent urban land will almost double from 37 million hectares in 2023 to 80 million hectares in 2063 (see the theme on Agriculture).

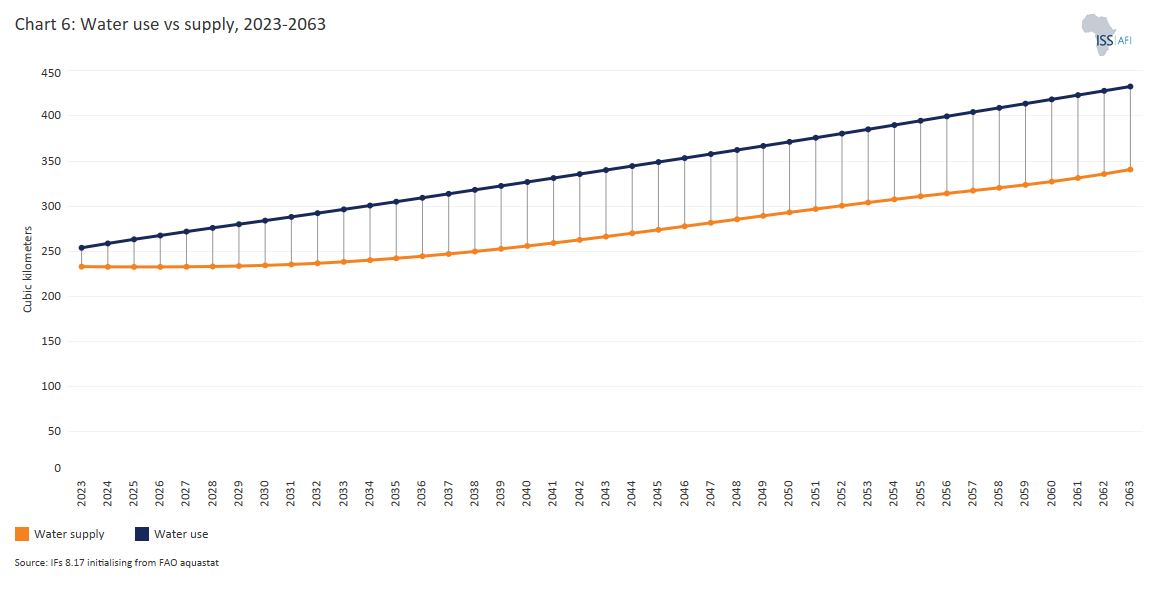

Another concerning trend is the increased annual water use resulting from a rapidly growing African population and improved agricultural land and food production. Annual water use exceeded supply in 21 African countries in 2023 (Chart 7). A growing population and intensified agricultural practices will lead to overexploitation of water resources, resulting in several interconnected challenges, such as water scarcity, competition for limited water supplies, environmental degradation and potential conflicts over water access. This worrisome projection underscores the urgent need for comprehensive water governance, cooperation and management strategies to address the growing demands of population expansion and intensified agricultural activities. The IPCC’s 6AR further emphasises the critical importance of sustainable water practices, highlighting the potential implications of climate change on water resources and the need for adaptive measures to ensure resilience in the face of evolving environmental conditions such as droughts.

Every African country needs proactive, climate-smart and science-based policies to mitigate the adverse effects of increased water use on ecosystems and communities. For example, water conservation measures such as rainwater harvesting and drip irrigation or investing in ecosystem restoration can significantly enhance resilience to climate change and mitigate water scarcity impacts.

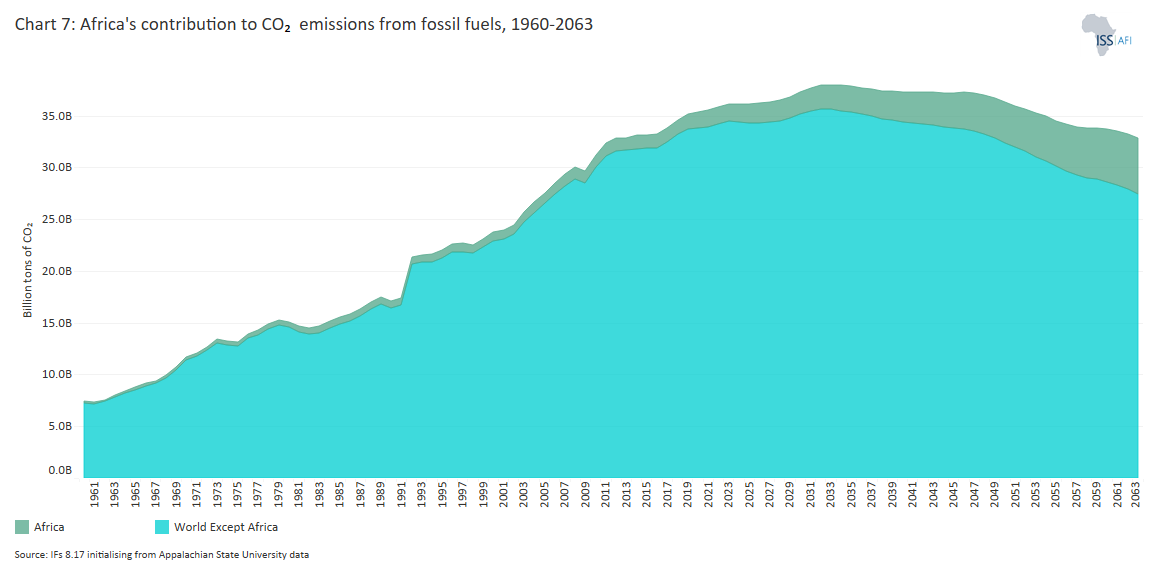

Africa is currently a minor carbon contributor, emitting less than 1.6 billion tons of CO2 equivalent from fossil fuel use constituting less than 5% of the associated global emissions. Yet, its fossil fuel dependency is growing rapidly, given efforts at electrification of a growing urbanising population, energy inefficiencies such as the lack of national grids and pipelines, and reliance on generators for electricity production.

Chart 8 presents the growing contribution of Africa’s carbon emissions from fossil fuels in the Current Path. As global emissions plateau and then decline, Africa’s contribution will climb from less than 5% in 2023 to 9% in 2050 and 12.5% in 2063. According to the Current Path, Africa will overtake fossil fuel-related emissions from the EU in 2034, India in 2052, and the US by 2061.

The picture changes when considering Africa’s development prospects in the Combined scenario, which combines ambitious improvements in development across eight sectors. The continent's contribution increases to 10.5% of the world's total in 2050 and 15% by 2063. The difference between the Current Path and the Combined scenario in 2050 is 341 million tons of CO2 equivalent, and the difference in 2061 is 638 million. The user can also select to display emissions from the Combined scenario.

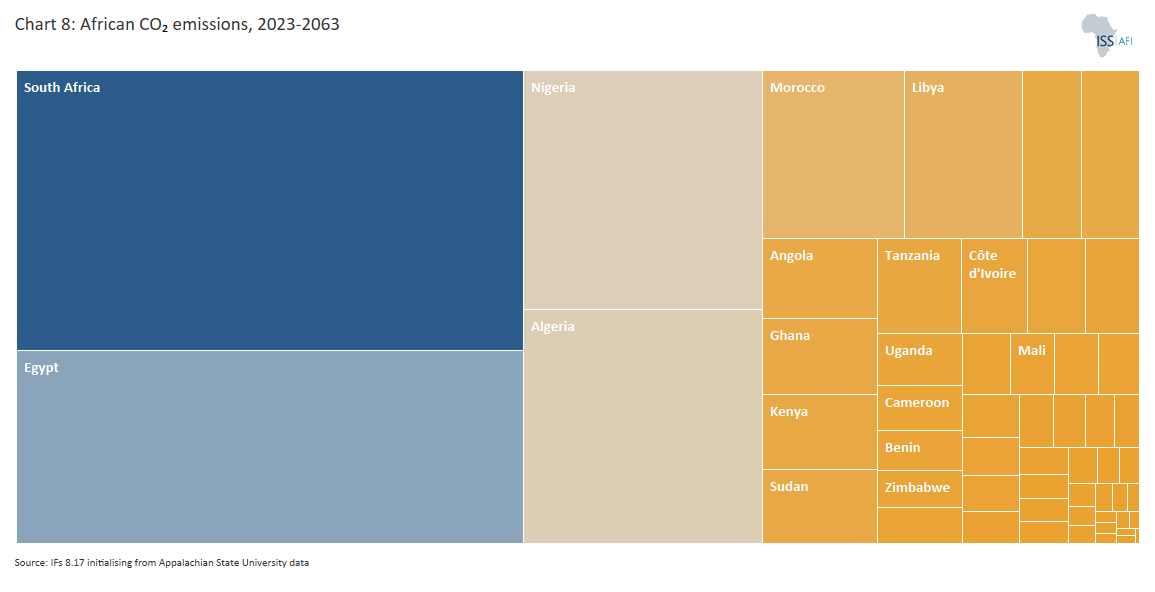

Four countries are responsible for 66% of the continent's fossil fuel carbon emissions. In 2023, South Africa was the largest emitter with 28% of Africa’s total emissions, followed by Egypt (17%), Algeria (11%) and Nigeria (11%) (Chart 9).

By 2050, South Africa will contribute only 11% of the continent's carbon emissions on the Current Path having reduced its reliance on coal for electricity, while Egypt’s share will decline to 15%. Nigeria will then be the continent's largest fossil fuel emitter, contributing 17%, while Algeria will contribute 6%. Other countries that will see rapid increases in carbon emissions are Ethiopia, DR Congo, Mozambique, Tanzania, Uganda, Cote d’Ivoire, Morocco and Sudan. These portions are unchanged when compared to emissions in the Combined scenario.

Nigeria, characterised by its rapid population growth and abundant oil and gas resources, has struggled to fulfil its NDC commitments and, by 2063, will have emerged as the continent's most extensive and the world’s fifth-largest fossil fuel carbon emitter, contributing 2.4% to global emissions from fossil fuels. It moves to the fourth spot in the Combined scenario, contributing 2.8% to global emissions from fossil fuel use. Instead of being responsible for 17% of Africa’s emissions, its share will be 20%. The country will then significantly challenge regional and international efforts to combat climate change.

South Africa, currently the largest emitter of carbon from fossil fuel use on the continent, is also one of the most coal-dependent countries globally. South Africa has committed to decarbonising its industry, reflected in its Nationally Determined Contributions (NDC). In line with these commitments, the Current Path suggests a gradual decrease from 125 million tons of carbon from fossil fuels in 2023 to 34 million by 2050 on the Current Path, and 354 million in the Combined scenario. South Africa will then have dropped from Africa’s largest fossil fuel carbon emitter to the third largest. It will be at the same ranking in 2063.

A growing dependence on natural gas characterises North Africa and the region struggles in decoupling economic growth from that dependence. Despite endeavours to diversify and embrace cleaner energy sources, finding the proper equilibrium between economic development and environmental sustainability is a challenge in Egypt, Algeria and Libya. The Ukraine-Russia war has heightened the importance of gas, with the EU turning to these countries, amongst others, for additional supplies. The Climate Action Tracker (CAT) also shows that to date, Egypt’s NDC targets, climate policies and actions are wholly insufficient and akin to a 4°C global trajectory. Its expanding fossil gas production overshadows its recent investments in renewable energy. In the Combined scenario, Egypt will emerge as Africa’s 2nd most extensive and the world’s 8th-largest fossil fuel carbon emitter, responsible for 1.8% of global fossil fuel emissions by 2063. All other African countries except South Africa will contribute less than 1% to global carbon emissions from fossil fuels.

Conversely, Morocco NDC targets associated policies align with a 1.5°C world after making commitments to halt the development of new coal-fired power plants while ramping up renewable investment. There are smaller countries, such as Seychelles, with a high per capita dependency on imported fossil fuels. Still, their annual emissions come from a shallow base, and these countries are amongst the smallest emitters globally.

Therefore, the success of reducing carbon emissions from the growing African continent hinges on only a few countries, notably Nigeria, Egypt, South Africa, Algeria, Ethiopia, Tanzania, Morocco, Côte d’Ivoire, DR Congo and Uganda. Their actions will determine how much Africa contributes to global emissions. Most other African countries would contribute very little to global emissions and will probably primarily invest resources in sustainable adaptation efforts.

Addressing the cause of climate change and acknowledging the need to adapt to its impact requires a comprehensive global approach and commitment focusing on adaptation (making people, infrastructure and economies safer) and simultaneous aggressive mitigation efforts (reducing carbon in the atmosphere).

There has been a proliferation of international, regional and national efforts to address the unfolding climate crisis, and the imperative for aggressive mitigation efforts is well-established and understood. Countries are adopting diverse carbon strategies to curb emissions and promote environmental responsibility. These strategies include investments in renewable energy (to speed up the energy transition), setting ambitious emission reduction targets (as outlined in the various country National Determined Contributions - NDCs) implementing carbon pricing mechanisms such as carbon taxes and emission trading systems as well as investing in the environment for sequestration.

The intent of the Paris Agreement is to limit global average temperature rise to below 2°C above pre-industrial levels and pursue ambitious efforts to limit it to 1.5°C. The Agreement requires that aggressive net-zero greenhouse gas emissions are achieved by mid-century, meaning removing as much carbon from the atmosphere as is being emitted. Our analysis does not, however, deal with Direct Air Capture (DAS) technologies which, according to some, would provide a technological solution since the associated efforts are still unproven at the required scale. According to IEA Executive Director, Fatih Birol, for example, the potential for DAC technologies to capture and store enough carbon emissions from the atmosphere at a sufficient scale to allow for ongoing oil and gas production is a fantasy. The implication is that more than 85% of emission reductions must come from cutting fossil fuel use and the balance from carbon capture, relying on natural systems.

To have a 50% chance of keeping global warming within 1.5°C relative to pre-industrial levels, a recent update of the IPCC Sixth Assessment Report finds that the world’s remaining carbon budget as of January 2023 was 250 GtCO2, equivalent to around six years of current CO2 emissions. For a 50% chance of the 2oC, the budget is around 1 200 GtCO2. These budgets underscore the need for rapid and deep emissions reductions.

Using data from the IPCC's 6AR, various studies and scenarios offer estimations of the CO2 concentration range in 2050 for a 1.5oC limit of 330 to 400 ppm. Even in a net-zero scenario, CO2 concentrations will continue to rise for several decades due to the stock and long residence time of historical atmospheric emissions, emphasising the importance of additional carbon capturing and sequestration efforts. In the Current Path, even amidst a decrease in annual global carbon emission, carbon ppm concentrations would continue to increase since the stock of CO2 in the atmosphere continues to grow, albeit slower, to around 518 ppm by mid-century and 547 by 2063. The additional contribution from the Combined scenario compared to the Current Path is relatively small at 4 ppm by 2063 given Africa’s limited emissions within a global context.

The implication is that instead of limiting global warming to 1.5oC above the pre-industrial level, the earth will be almost 3oC warmer in 2050. However, it is important to remember that this is a long-term average to be considered over twenty or thirty years, not a single event. Nevertheless, recent data highlight the importance of additional carbon storage and sequestration efforts (sequestration focuses on the initial capture of carbon, and storage involves the retention of this carbon over the long term) and the necessity of aggressive adaptation financing and investment.[5Carbon Capture and Storage (CCS) investments are still relatively small but growing rapidly. Investment in CCS almost doubled in 2023, reaching a record US$11.33 billion. CCS have the most potential when applied to industrial ‘point’ processes before carbon reaches the atmosphere, such as cement, steel, pulp and paper, chemicals and natural gas processing (accounting for around 25% of global energy-related CO2 emissions), but it is expensive. CCS technologies have, on the one hand, been applauded, mainly by the oil and gas industry, for their innovation and ability to decarbonise heavy emitting industries, while on the other hand, heavily criticised as a greenwash attempt in what many fear will only extend the fossil fuel era instead of ending it. Still, capacity has grown by 44% between 2022 and 2023 and as of September 2023, there were 39 large-scale CCS facilities worldwide in operation, with 20 in construction and another 98 in an advanced development phase. Most of these projects are in North America and are part of the US petroleum and gas industry. The IEA forecasts that CCS capacity could increase in the coming decades, reaching 1.5 gigatons of CO2 per year by 2030 and potentially exceeding 5.6 gigatons by 2050, most from point capture from cement production and power generation. The Agency subsequently set out a range of policy recommendations for CCS development and deployment. The Chair of the Energy Transitions Commission believes that CCS could capture or store about 4 Gt of CO2 a year by 2050.]

Against this background, the following sections explore two strategic and complementary approaches for Africa to pursue in addition to the rapid transition to renewables modelled elsewhere on this website. These are: Africa’s role as a global carbon sink (as part of sequestration) and the potential of a global carbon tax to reduce emissions through incentivising high emitters.

Forest regeneration and the retention of savanna and grassland areas can play a critical role in reducing carbon emissions in Africa and globally through sequestration and storage, given that deforestation and land-use changes contribute a sizeable chunk of between 11% and 20% of global greenhouse gas emissions. They can also provide a potential trade-off in respect of a global carbon tax, discussed further below.

Nature stores significant amounts of carbon in the Earth's soils. Soil health is closely linked to carbon preservation, and efforts to reduce soil erosion are crucial in maintaining the effectiveness of carbon sequestration processes. Soil erosion and poor farming practices threaten this natural carbon sink, as they can lead to the degradation of soil quality and the release of stored carbon into the atmosphere.

Photosynthesis, the process by which plants absorb carbon dioxide and convert it into biomass, is a natural mechanism for capturing and storing carbon. Deforestation and poor land management practices disrupt this process by reducing the number of trees, grass and other plants available to absorb carbon dioxide. It diminishes the Earth's natural capacity for carbon sequestration and releases stored carbon when, for example, trees are cut down or burned. Protecting, conserving, restoring, replanting and managing these carbon sinks are thus vital in mitigation and sustainability efforts. Forests, in particular, act as a significant carbon sink, removing an estimated 2.6 billion metric tons of carbon dioxide from the atmosphere annually. However, Africa is under constant threat due to its growing population that needs cheap, low-technology fuels and land for agriculture. Land expansion in agriculture accounts for up to 90% of deforestation globally, including in Africa. Next to South America (68 million hectares) Africa experienced the highest deforestation in 2000-2018 (49 million hectares). The leading cause of forest loss in Africa is cropland expansion, particularly in the Congo Basin, home to the world’s second-largest tropical rainforest and its most significant carbon sink.

The Congo Basin spans six Central African countries and should be at the heart of global climate action. It absorbs 4% of the world’s CO2 emissions, with its peatlands alone storing an estimated 30 billion metric tonnes of carbon – the equivalent of three years’ worth of global fossil fuel emissions. The region, however has lost 30% of its forest cover since 2001, mainly in DR Congo which is home to more than half of the Congo Basin’s rainforest area. While illegal logging was outlawed in 2002, enforcement remains weak due to resource constraints and, in some cases, the complicity of officials in the hardwood trade.

Urgent action is required to halt deforestation in the Congo Basis since forests are shrinking at an alarming rate of 1 to 5% per year. Due to unregulated logging and mining, up to 30% of forest cover has been lost since 2000. Mining, logging and agricultural expansion are accelerating forest loss, with Chinese and European companies implicated in illegal deforestation—often with the collusion of local officials. Elsewhere, countries like Mozambique, one of the world’s poorest nations, are also severely impacted, losing an estimated 267 000 hectares of forest annually.

Recognising these threats, international policies like the 2024 EU Deforestation Regulation (EUDR), aim to buttress reforestation. Under EUDR, importers of commodities like coffee, cocoa, soy, palm, cattle, timber and rubber - and products that use them - must be able to prove their goods did not originate from deforested land or else face hefty fines. However, the efficacy of these measures is not fully established.

In addition to soil erosion and deforestation, desertification represents another significant challenge to carbon sequestration efforts. The process depletes the ability of arable land to retain carbon, contributing to the degradation of natural ecosystems. An estimated 45% of Africa’s land area is affected by desertification, particularly in the Sahel region. In response, the African Union launched the Great Green Wall (GGW) initiative in 2007 to combat desertification, land degradation and climate change. The project aims to restore 100 million hectares of degraded land, capture 250 million tons of CO₂, and create 10 million jobs by 2030. At COP26 in 2021, the European Union reaffirmed its commitment to the GGW with an annual pledge of €700 million, bringing total global commitments to €19 billion.

Already the Agriculture scenario includes a reasonable forest protection multiplier to constrain the expansion of cropland. The multiplier is introduced over a 40-year period in 17 African countries.[6Congo, Zambia, Angola, CAR, Nigeria, São Tomé, Senegal, Sierra Leone, Ghana, Benin, Eswatini, Gambia, Guinea, Malawi, Burkina Faso, Togo, Madagascar.] Chart 10 compares the carbon emission from deforestation in the Agriculture scenario with the Current Path which, by 2063, equates to 1.2 billion tons of CO2 equivalent less carbon in the atmosphere. That reduction represents 4.7% of global carbon emissions from fossil fuels in 2063 and translates into 2.6 ppm less CO2. The latter is more than half the additional concentration associated with the Combined scenario (3.5 parts per million) compared to the Current Path in 2063.

Africa needs to monetise its role as a global carbon sink, especially as deforestation and land degradation threaten its ability to absorb emissions. One way to do this would be to explore the potential of a global carbon tax that could not only fund the continent’s more rapid transition to renewables but also support large-scale reforestation and conservation efforts critical for maintaining its carbon sequestration capacity. However, such a proposal faces opposition from high-emitting economies reluctant to commit to mandatory carbon pricing, fearing economic slowdowns and competitiveness concerns. On the other hand, there is growing international support from climate advocacy groups, multilateral institutions like the World Bank and IMF, and emerging economies that see a global carbon tax as a fair mechanism to hold historic polluters accountable while financing sustainable development in the Global South.

The matter of a carbon price is raised regularly. It would likely be implemented through carbon taxes or emissions trading systems, also known as cap and trade systems.

Carbon taxes assign a fixed cost to carbon emissions to incentivise businesses and individuals to adopt cleaner technologies and sustainable practices. The revenue generated is then channelled into initiatives such as renewable energy projects (to speed up the energy transition) or climate change adaptation (to safeguard communities and infrastructure). Emissions trading systems or cap and trade systems set an emissions allowance (or permit) for an industry or sector, allowing companies to trade permits. While emission trading systems have proven effective, they can cause “carbon leakages” where industries move to regions with less stringent environmental regulations, resulting in a shift in emissions rather than a genuine reduction. The associated responses can compromise the effectiveness of carbon reduction efforts and have unintended ecological consequences. Despite widespread support and publicity, only 39 carbon tax initiatives have been implemented globally, covering a meagre 6% of global greenhouse gas emissions. Of the world’s top 10 emitters, only Japan has adopted a carbon tax. Emission Trading Systems cover 19% global emission. Collectively these two instruments cover 24% of global emissions. The most recent report from the World Bank, State and Trends of Carbon Pricing 2024, indicates that while a carbon price covers 24% of global emissions, only 1% is at the recommended price range which is sufficient to curb emissions in line with the Paris goals.

According to the World Bank’s Carbon pricing dashboard, carbon prices in Europe range from US$0.77 per metric ton in Ukraine to as much as US$132 in Switzerland. Globally, carbon prices ranges between US$0.46 per metric ton to US$167. Some countries in the Global South like South Africa, Uruguay, Argentina and Chile have also set a carbon price, with Uruguay having the highest price worldwide at US$167 per metric ton of CO2. Subnational emissions trading systems are also present in some US states (e.g. California, Oregon, Washington and Massachusetts).

A 2023 study on the emission trading pilot areas in China showed outsourcing of carbon emissions or carbon leakage in pilot areas to non-pilot areas where less stringent environmental laws persist. This phenomenon was also observed in the EU emission trading system (EU ETS), prompting the proposal of a Carbon Border Adjustment Mechanism (CBAM) to ensure that imported goods face a comparable carbon cost to domestically produced goods, preventing a competitive disadvantage for EU businesses and incentivising global partners to adopt emission reduction measures. The EU CBAM (legislated as part of the EU’s Green Deal) aims to align the amount of carbon involved in industries within and outside the EU and will impact specific carbon-intensive goods (steel, aluminium, fertilisers, electricity, hydrogen and cement) from 2026 onward. The initial price is at 2.5% of the carbon price per ton which will increase to 100% of that generated in the production of the goods by the end of 2034.

Concerns have been expressed about the potential harm that CBAM may inflict on several African economies, specifically the risk to industries in low- and middle-income countries, as they may lack the resources to decarbonise production. Some, such as South Africa, are considering taking the EU to the World Trade Organisation.

What is clear from the above is that the complex, different and fragmented approaches to carbon pricing internationally. Many countries responsible for contributing to high greenhouse gas emissions are not taxing carbon emissions or pricing them at very low rates. There is, therefore, growing support (backed by institutions such as the World Bank and the IMF) for a uniform (global) carbon tax framework to drive emission reductions worldwide. An international framework would be more transparent and improve emission reduction efficiency and effectiveness. A single carbon tax framework will also be less complex. Still, it must be flexible enough to consider countries' economic structures, incorporate precise compensation mechanisms to address potential disparities and diverse national circumstances and include technical and financial assistance provisions for developing countries. A global carbon tax at scale could also assist Africa’s energy transition.

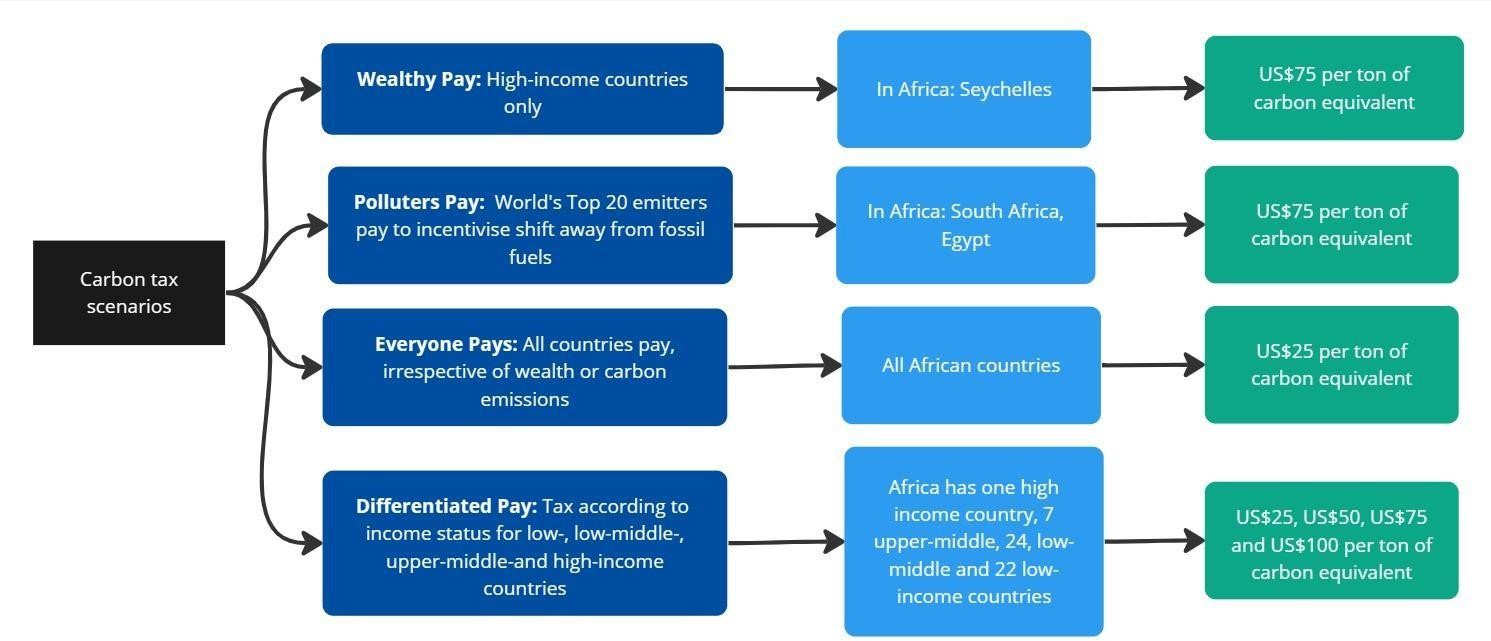

To implement these ambitions, we explore four illustrative carbon tax scenarios, summarised in Chart 11. As reference we use the International Carbon Price Floor (an IMF proposal) of a minimum carbon price ranging from US$25 to US$75 per metric ton of CO2, but apply the price to a ton of carbon (equivalent to 3.67 tons of CO2), meaning that the rates used in the scenarios are significantly lower than those proposed by the IMF.

In the Wealthy Pay scenario, we argue that present-day developed countries obtained their wealth through an enormous environmental impact and should be taxed accordingly. The carbon tax for high-income countries is introduced at US$75 per metric ton of carbon (or US$20.43 per ton of CO2) and phased in over ten years from 2027. Since China (the world’s largest carbon emitter) is on the cusp of graduating to high-income status ranks, it is included among the high-income countries and the tax phased in over 15 years from 2030. The only African country affected is Seychelles, but the impact is minimal due to its low carbon emissions (2nd-smallest carbon emitter in Africa).

In the Polluters Pay scenario, the 30 largest polluters in 2023 pay a carbon tax of US$50 per metric ton of carbon equivalent (or US$13.62 per ton of CO2), phased in over ten years from 2027. The scenario places a carbon tax on countries responsible for 88% of the world’s emissions in 2023.

In the Everyone Pays scenario, the responsibility for reducing carbon emissions is shared across all nations, reflecting the collective responsibility of combating climate change at US$25 per ton of carbon equivalent emissions (or US$6.81 per ton of CO2). The tax is phased in over ten years, starting in 2027. However, a recent study by the WTO stresses that low-income countries would adversely be affected by such a Carbon Price Floor and that even a low-carbon price would impact production decisions and reduce real income in these countries.

In the Differentiated Pay scenario, income classification determines the carbon tax. In this scenario, high-income countries pay US$100 per ton of carbon equivalent (or US$27.25 per ton of CO2) while upper-middle-income countries pay US$75/ton. The taxes are phased in over ten years, starting in 2027. Lower-middle-countries pay US$50/ton, and low-income countries pay US$25/ton. In both these cases, the taxes are phased in over a more extended period of 15 years. In 2024, Africa had one high-income country, eight upper-middle-income countries, 23 lower-middle-income countries and 22 low-income countries.

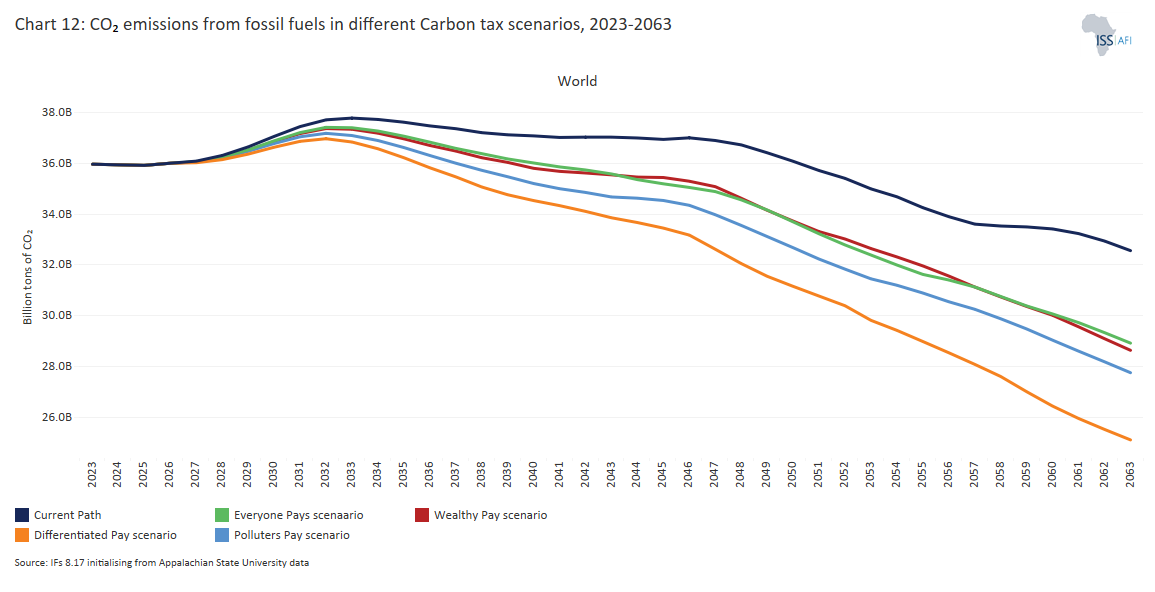

Compared to the Current Path scenario, all carbon price interventions substantially reduce fossil fuel-related carbon emissions (Chart 11), reducing the accumulated CO2 in the atmosphere (Chart 12), albeit to levels still on par with an RCP4.5 world.

The Differentiated Pay scenario significantly affects carbon emission reductions (14% below the 2050 Current Path and 26% lower in 2063). This is followed by the Polluters Pay and Wealthy Pay scenarios, which have similar results. The Everyone Pays scenario has the lowest impact. It is important to remember that the prices used in these illustrative scenarios are significantly below those recommended by the IMF in its International Carbon Price Floor.

The Differentiated Pay scenario leads to a swift decline in emissions, evident from 2034. By 2050, CO2 equivalent emissions decline from 36 billion tons to 31.2 billion tons. However, implementing such a differentiated carbon tax will require careful management. The impact on each country under a carbon tax regime hinges on its ability to navigate the transition effectively, invest in clean energy alternatives (modelled in the next section) and implement policies that foster economic resilience and sustainability.

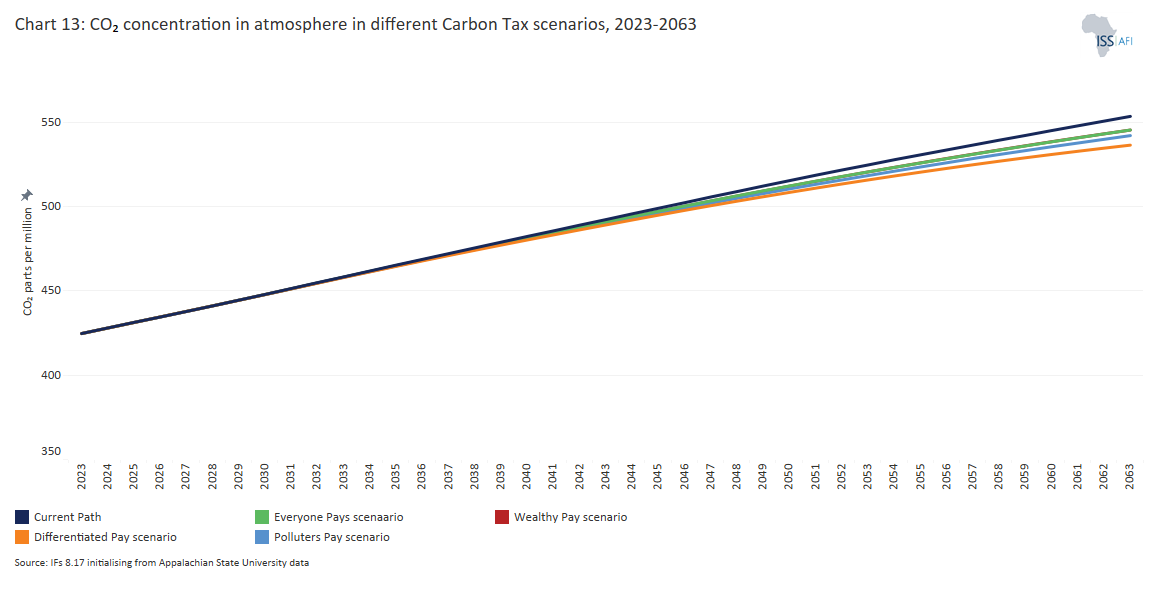

Chart 13 shows the impact of the four carbon tax scenarios on CO2 concentration in the Earth's atmosphere.

The Differentiated Pay scenario aligns with the Paris Agreement, which established the principle of common but differentiated responsibilities. It also aligns with the Just Energy Transition initiative and advocates for a collective global responsibility in addressing climate change. It recognises that all governments are responsible for tackling environmental destruction worldwide, but not equally. This acknowledgement stems from the understanding that earlier industrialised economies have historically contributed more to the climate crisis. In this context, requiring richer countries to pay a more significant tax reflects a commitment to addressing historical disparities and ensuring a fair distribution of the financial responsibility for mitigating climate change.

The result of the Differentiated Pay scenario is that atmospheric carbon dioxide levels could be 3.4% lower in 2063 than the Current Path, with up to 0.2oC lower average global temperature. Higher prices, as recommended by the IMF, would have a much more significant effect.

A carbon tax is only one of several policies, tools and measures to tackle the global climate crisis. It would need to be complemented by measures such as carbon sequestration and a swift energy transition, particularly in the more significant global emitters. Implementing a global carbon tax framework has challenges, but it addresses the potential social and economic effects of carbon emissions on vulnerable communities. However, by embedding fairness and efficiency, a global carbon tax can become a cornerstone of effective climate governance — as long as Africa is active and the world’s top polluters pay their bills.

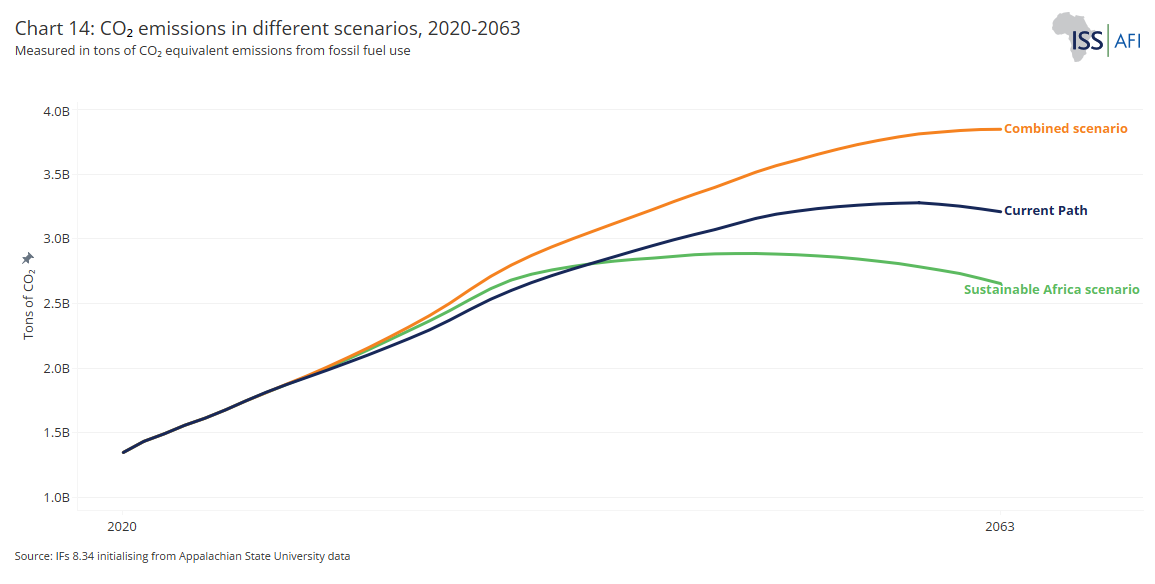

We now combine the Differentiated Pay and Combined scenarios into a single scenario, the Sustainable Africa scenario, and compare the summary impact on emissions and development outcomes.

Chart 14 presents Africa’s CO2 equivalent emissions from fossil fuel use in the Current Path, the Combined and the Sustainable Africa scenarios. The impact of the Differentiated Pay carbon tax is significant, with CO2 equivalent emissions below even the Current Path. The user can change the regions to select the World or any African country.

The impact of the suite of policies to improve energy efficiency and constrain carbon emissions is evident when considering that Africa will release 7.5% less carbon from fossil fuels in the Sustainable Africa scenario in 2050 compared to the Current Path and 17.6% less in 2063 while economic growth averages 7.7% per annum compared to 4.3% in the Current Path.

The reader is reminded that the fulfilment of the Sustainable Africa ambitions would see a 2050 African economy that is 79% larger than the Current Path. GDP per capita would be 61% higher, and only 105 million Africans would live in extreme poverty instead of 341 million. Africa’s total economy would grow roughly two percentage points more rapidly than in the Current Path. The differences are even more impressive by 2063.

However, because of the various mitigation policies, energy demand would only be 30% higher in 2050. Instead of energy demand equivalent to 6.4 barrels of oil equivalent per person, African per capita demand would be 10.7 barrels by 2063.

Africa needs to develop much more rapidly (modelled in the Combined scenario), which will inevitably increase emissions given its young and growing population and current low levels of energy use. In addition to application to cement and fertiliser production plants, reducing illegal gas flaring in countries such as Nigeria, Algeria, Angola, Cameroon and Egypt should play an essential role. However, due to the associated costs and technical barriers, the widespread deployment and adoption of carbon capture and storage technologies in Africa is still in its infancy. Nigeria and South Africa, as Africa’s largest carbon emitters, have the potential to become players in the carbon capture and storage markets, with South Africa currently having several pilot projects in the coal power sector.

Several scenarios on this website already include interventions to promote sustainability. For example, the Agriculture scenario includes interventions for forest protection (examined separately above). The Demographics and Health scenario includes greater contraceptive use in high fertility countries, which, by reducing population size, constrain total emissions. Better Governance and Education inevitably improve the effectiveness of mitigation and adaptation policies while raising awareness of the importance of keeping emissions in check. Numerous interventions that are part of the Large Infrastructure and Leapfrogging scenario improve the adaptive capacity of African populations through the provision of electricity and roads, as well as investing in and scaling up renewable energy production while simultaneously constraining coal production and exports.

On the other hand, regional trade (the AfCFTA scenario), the Manufacturing scenario, better Health and WaSH (although improved water and sanitation are also critical adaptive components) and more inward Financial Flows all increase emissions since they result in a larger African economy with more energy needs. Even improved Gender relations have this effect.

The Sustainable Africa scenario then complements the Combined scenario by including the Differentiated Pay global carbon tax set out in a previous section. The results indicate that although it will not be easy, Africa can embark upon a sustainable growth path to its own and global benefit, but it would need the rest of the world to create space for its carbon emissions while implementing a carbon tax and assisting the energy transition to renewables in exchange for its role as a global carbon sink. The analysis done in the Energy theme estimates that Africa would need up to 10% of global emissions from fossil fuels by 2050 and 14% in 2063.

Creating fuels from municipal solid waste is a significant opportunity that should get more attention than is provided with the hype around the need to reduce fossil fuels and increase non-fossil energy sources. In 2012, the world generated over 1.3 billion tons of municipal solid waste annually, which is expected to double by 2025. Most are generated in high-income countries, but low- and middle-income countries are experiencing the fastest growth. Only about 20% of municipal solid waste is collected and appropriately treated, while the rest is dumped in landfills, burned openly or littered. Informal waste picking and recycling sectors are widespread but often operate in unsafe and unhealthy conditions. Due to rapid urbanisation, Africa is likely to see an increase in projected urban waste of up to 200% in the next decade, of which 30 to 70% is organic waste (i.e. made up of food waste or biomass) that is not only non-recyclable but also produces methane (CH4), a potent greenhouse gas, on decomposition. Research published in Waste Management indicates that up to one ton (equivalent) of CO2 can be saved per ton of waste combusted rather than sent to landfill due to the potency of CH4 as a greenhouse gas. In 2016, Africa produced 174 million tonnes of municipal solid waste, projected to reach 269 million by 2030. According to UNEP, Africa generates an average of 0.72 kg of municipal solid waste per person per day, with only about half collected and the rest often dumped in landfills, burned openly or littered.

One approach would be to explore the design of small-scale, decentralised waste-to-energy plants. The downscaling of the Fischer-Tropsch synthesis in a remote context, with priority given to low capital costs, simplicity and energy self-sufficiency, offers a potential pathway in this regard.[7C L Tucker, Waste to Fuel: Designing a cobalt-based catalyst and process for once-through Fischer-Tropsch synthesis operated at high conversion, PhD Thesis, at the Department of Chemical Engineering, University of Cape Town, 2022.]

Because of its limited ability to adapt to climate change, Africa will suffer more than any other region from climate change impacts despite having contributed little to the cause of this problem. Decisive leadership and an effective executive system capable of averting a global crisis are sorely needed. Today, geopolitics and domestic politics intertwine, leading to an uncertain future with devastating outcomes and consequences for many, particularly in Africa. Sustainable solutions and adaptation are becoming increasingly urgent. We examine many of these challenges in the theme Africa in the World.

Our findings highlight the complex nature of Africa's transition away from fossil fuels, presented in the separate theme on Energy. Contrary to the rapid shifts proposed by UNEP and others, our analysis suggests a more gradual phasing out in Africa, starting with coal, then reducing oil and eventually gas beyond 2050. That transition is moving fast in many advanced economies such as Europe, North America, Japan and China. It is much slower in developing countries, particularly in Africa, which requires substantial support from wealthier nations to establish a feasible transition to renewables and carbon emission pathways, such as through some of the proceedings that could come from a global carbon tax. For Africa, climate finance is the critical enabler of the global energy transition and must be at the top of the COP agenda.

To date, little has come of previous initiatives such as the 2021 Glasgow Financial Alliance for Net Zero (GFANZ) that were to bring US$130 trillion to bear on the climate crisis or the Just Energy Transition Partnerships (JET-Ps) that was initiated at COP26. The flagship JET-Ps in South Africa and Indonesia have barely raised one-tenth of what is required, and those in Vietnam and Senegal have not fared much better. COP27 subsequently introduced a loss and damage fund that aims to provide financial assistance to nations most vulnerable and impacted by the effects of climate change, but it is still unfunded. Rather than the promises from the developed countries who promoted both, China is powering ahead in spending on renewables.

The question is: Who will finance the significant investments required for gas and oil in Africa as other regions gradually move away from fossil fuels? The world needs decisive action to shift Africa from its current fossil fuel dependency. In addition to carbon sequestration, this theme examined the implementation of a global carbon tax, an essential response component.

Adaptation efforts must catch up to mitigation efforts globally and in Africa. Efforts to adapt to climate change must prioritise the protection of communities, ecosystems and economies from its adverse effects. Our report underscores the importance of enhancing resilience through various means—be it poverty alleviation, conflict prevention or healthcare improvements—alongside modifying infrastructure (land use planning, climate-smart practices, climate-resilient infrastructure), being more efficient with natural resources (e.g. water and land use management) and formulating policies that enable societies to respond effectively to evolving climatic conditions (aid support, investments, early-warning systems, etc.) to withstand climate challenges better. This becomes particularly complex when accounting for concurrent crises like poverty, undernutrition, and civil conflict. Africa’s best response to the emerging threat of climate change is to pursue a sustainable development pathway, as reflected in the Sustainable Africa scenario.

Adopting diverse carbon reduction strategies globally, including carbon taxes and cap-and-trade systems, reflects a commitment to environmental stewardship. However, geopolitical tensions, notably between China, the US and the EU, pose significant challenges to these efforts. On the one hand, the competition for green energy leadership could create a ‘race to the top’, spurring green investment, innovation and international climate action. On the other hand, the rising tensions undermine cooperation and fragment the green energy market, and the election of Donald Trump as the 47th US President means that the US is, again, stepping away from climate action. Geopolitics tensions undermine collaboration across ideological divides. With China dominating almost all clean technology supply chains, policymakers must square the imperative to reduce dependencies with adequate cooperation to meet decarbonisation goals.

Carbon pricing mechanisms like the EU's Emissions Trading System offer a flexible approach to reducing greenhouse gas emissions. In addition, carbon offset programs enable entities to counterbalance their carbon footprint by investing in projects that mitigate emissions but remain controversial. Industries worldwide, particularly the aviation sector, have prominently embraced this approach through reforestation, renewable energy projects and energy efficiency initiatives. Still, the system is prone to greenwashing and shifting of responsibilities.

The impact on vulnerable populations and the risk of carbon leakages mar the effectiveness of these systems and could inadvertently shift emissions to less regulated regions. As a result, for the EU, the Carbon Border Adjustments Mechanism (CBAM) is a mechanism that levels the playing field for imports and domestic products. It intends to align industries within and outside the EU and impact specific carbon-intensive goods from 2026 onward. However, concerns have been raised regarding the potential harm to industries in low- and middle-income countries that will need more resources to decarbonise their production. Without careful consideration, CBAM will increase global inequalities and proactive measures are required to ensure that carbon strategies are practical and globally equitable. UNCTAD notes that African countries need expanded access to foreign currencies through central bank swaps and enhanced resilience during external crises through standstill rules on debtors’ obligations, such as climate-resilient debt clauses. This, the Conference notes, would allow a halt in debt repayments, providing some breathing space for crisis management.

Moreover, integrating adaptation measures across sectors, including healthcare, agricultural practices, transportation, infrastructure resilience, social services, urban planning, etc, is imperative. Strengthening Africa’s healthcare infrastructure, establishing robust disease surveillance systems, facilitating widespread access to vaccines, incorporating climate-resilient city design and fostering international collaboration are indispensable steps in building adaptive resilience across the region.

The preceding analysis emphasises the urgency of addressing both the causes and effects of climate change in Africa and the need for a concerted global effort to support the continent's transition to a low-carbon future. Such a response must be multifaceted and include mitigation strategies, adaptation efforts and financial investments tailored to the continent's unique context. Central to that approach would be a trade-off between Africa’s role as a carbon sink and the opportunities offered via a global carbon tax.

Africa’s climate strategy must leverage its natural carbon sink potential, accelerate the clean energy transition, secure climate finance and implement fair global carbon policies. A differentiated carbon tax, strong domestic policies and international support can help Africa balance economic growth with climate resilience, ensuring a sustainable and equitable future.

- Strengthen Africa’s role as a global carbon sink

-

- Protecting, restoring and expanding forests, wetlands, peatlands and grasslands is a priority for enhancing carbon sequestration.

- Implement and enforce stronger anti-deforestation policies to curb illegal logging and land degradation.

- Secure international financing and investment for large-scale reforestation and conservation projects.

- Expand initiatives such as the Great Green Wall to combat desertification and restore degraded land.

- Implement a fair and effective global carbon tax

-

- Establish a differentiated global carbon tax system where contributions are based on income classification.

- Use carbon tax revenues to finance renewable energy projects, climate adaptation and resilience-building initiatives in developing countries.

- Ensure that all significant emitters participate in the carbon tax framework to prevent carbon leakage and maintain global competitiveness.

- Advocate for fair trade policies to prevent measures like the CBAM from unfairly penalising African economies.

- Accelerate the transition to renewable energy

-

- Scale up investments in solar, wind, hydro, geothermal and SMNR energy to reduce dependency on fossil fuels.

- Using decentralised renewable solutions, improve energy efficiency and expand electricity access to underserved communities.

- Secure climate finance and technology transfer agreements to facilitate Africa’s clean energy transition.

- Develop and implement comprehensive carbon reduction strategies

-

- To incentivise emissions reductions, adopt carbon pricing mechanisms, including carbon taxes and emissions trading systems.

- Promote climate-smart agriculture and sustainable land-use practices to minimise deforestation and soil degradation emissions.

- Explore innovative waste-to-energy solutions, such as converting municipal solid waste into biofuels, to reduce methane emissions.

- Strengthen climate finance and global cooperation

-

- Ensure that wealthy nations meet their climate finance commitments to fund adaptation and mitigation efforts in Africa.

- Fully operationalise and finance the Global Loss and Damage Fund to support countries most affected by climate change.

- Expand access to green investment funds, debt relief mechanisms and concessional financing to enable sustainable development.

- Encourage regional cooperation among African nations to implement joint climate strategies and share technological advancements.

- Enhance adaptation and resilience efforts

-

- Invest in climate-resilient infrastructure, including flood defences, drought-resistant agriculture and sustainable urban planning.

- Strengthen early warning systems and disaster response mechanisms to protect vulnerable communities from climate-induced disasters.

- Support capacity-building programs to equip African governments with the skills and knowledge to implement effective climate policies.

- Align climate policies with Sustainable Development Goals

-