South Sudan

South Sudan

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This page provides an in-depth analysis of South Sudan’s current development challenges and prospects, using alternative sectoral scenarios to assess how different policy and investment choices could shape the country’s growth to 2043. It explores the individual and combined impact of eight sectors, including demographic, economic and infrastructure-related outcomes. The analysis highlights practical policy actions that could help South Sudan strengthen resilience, diversify its economy beyond oil and accelerate progress in livelihoods and service delivery.

For more information about the International Futures modelling platform we use to develop the various scenarios, please see the Technical page.

Summary

We begin this page with an introductory assessment of the country’s context, focusing on current population distribution, social structure, climate and topography.

- South Sudan is a landlocked country in East-Central Africa, bordered by Sudan, Ethiopia, Kenya, Uganda, the Democratic Republic of the Congo and the Central African Republic. Since gaining independence in 2011, it has faced repeated conflict and economic volatility that have constrained state-building and development, leaving it among the world’s poorest and most fragile countries. South Sudan now faces a critical need to consolidate peace, build stronger institutions and accelerate structural transformation by reducing dependence on oil and expanding productive employment to achieve more inclusive, resilient long-term growth.

This section is followed by an analysis of the Current Path for South Sudan, which informs the country’s likely current development trajectory to 2043. It is based on current geopolitical trends and assumes that no major shocks would occur in a ‘business-as-usual’ future.

- The population will increase from 11.5 million in 2023 to 18.2 million by 2043, while demographic trends point to a declining fertility rate, a rise in median age from 19.2 to 25.1 years and a growing ageing population, with the share of people aged 65 and older rising from 3.1% to 6.6% in the same period.

- The economy will expand steadily, with GDP growing by 4.1% from US$6.9 billion in 2027 to US$12.8 billion by 2043. This performance exceeds the average for low-income countries, indicating positive structural economic progress in the years ahead.

- GDP per capita will rise from US$1 476 in 2023 to US$1 940 by 2043, though this recovery will remain slow relative to peer-income groups.

- Poverty levels are expected to remain severe in South Sudan. The share of the population living in extreme poverty (below US$2.15 per day) will increase from 64.3% in 2023 to 73.2% by 2043. These high poverty rates are likely to be worsened by limited employment opportunities.

- Development challenges will persist, including high unemployment, widespread insecurity and underinvestment in key sectors such as healthcare, education and basic infrastructure. The Current Path emphasises the importance of effective structural reforms and well-targeted policy actions, aligned with the National Development Plan and peacebuilding priorities, to foster inclusive growth and strengthen socio-economic outcomes.

The following section compares progress on the Current Path with eight sectoral scenarios. These are Demographics and Health; Agriculture; Education; Manufacturing; the African Continental Free Trade Area (AfCFTA); Large Infrastructure and Leapfrogging; Financial Flows; and Governance. Each scenario is benchmarked to set an ambitious yet reasonable aspiration for that sector.

- The Demographics and Health scenario projects significant improvements in population health by 2043 compared to the Current Path. Life expectancy will increase to 75.5 years, compared to 73.4 years on the Current Path. Infant mortality rates will decline from 41.3 per 1 000 live births to 33.5 per 1 000 live births, and deaths from communicable diseases will fall as prevention, treatment and health-system coverage improve. This scenario underscores the increase in economic productivity among the working-age population resulting from improved health outcomes and reduced disease burden.

- In the Agriculture scenario, average crop yields will increase to 4.2 metric tons per hectare by 2043, up from 3.5 metric tons per hectare in the Current Path. This increase will boost total crop production to 10.5 million metric tons, narrowing the production deficit and helping lift an additional 519 000 people out of extreme poverty by 2043 compared to the Current Path.

- In 2023, young adults aged 15 to 24 years had, on average, completed five years of education. The Education scenario would raise the average years of schooling for this group to about 7.4.

- The manufacturing sector accounts for a small share of South Sudan’s economy, with activity centred on agro-processing and light manufacturing. The Manufacturing scenario will increase the share of manufacturing value added to 13.5% of GDP by 2043, a one percentage-point increase above the Current Path.

- In the African Continental Free Trade Area (AfCFTA) scenario, South Sudan's trade deficit as a percentage of GDP will fall from 22.9% in 2023 to 3% by 2043, compared to 4.2% on the Current Path. By 2043, South Africa’s GDP will be 13.7% higher, equivalent to an additional US$1.8 billion than on the Current Path. GDP per capita will also reach US$2.119 in the AfCFTA scenario, 9.1% above the Current Path, underscoring the significant gains from deeper regional and global trade integration.

- In the Financial Flows scenario, foreign direct investment (FDI) inflows to South Sudan will increase slightly to 0.6% of GDP by 2043, versus 0.5% on the Current Path. This incremental gain would lift the country’s FDI stock to around US$619 million, up from US$503 million under the Current Path. The stronger investment outlook translates into an economy that is 0.8% larger by 2043, with GDP per capita roughly 0.5% higher than in the baseline. Achieving these outcomes would require greater policy predictability, a more enabling regulatory environment and improved credit ratings—measures that would support faster growth and better living standards.

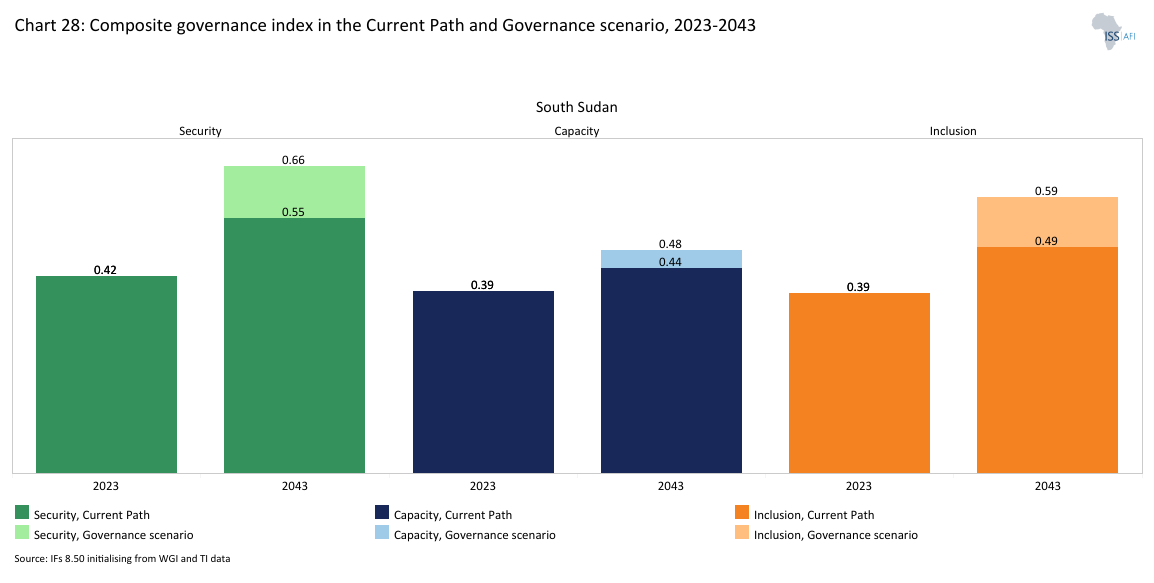

- By addressing insecurity, fragility and institutional weaknesses that continue to constrain development, the Governance scenario could reduce poverty by 3.2% and increase economic growth by 7.7% in 2043 relative to the Current Path. Improved security and stronger, more accountable institutions would bolster investor confidence and macroeconomic stability, supporting quicker, more resilient growth and pushing GDP per capita 5.2% higher than under the Current Path. While reforms are needed across many areas, prioritising state capacity, the rule of law and public financial management will be key to rebuilding trust, improving service delivery and unlocking South Sudan’s long-term economic potential.

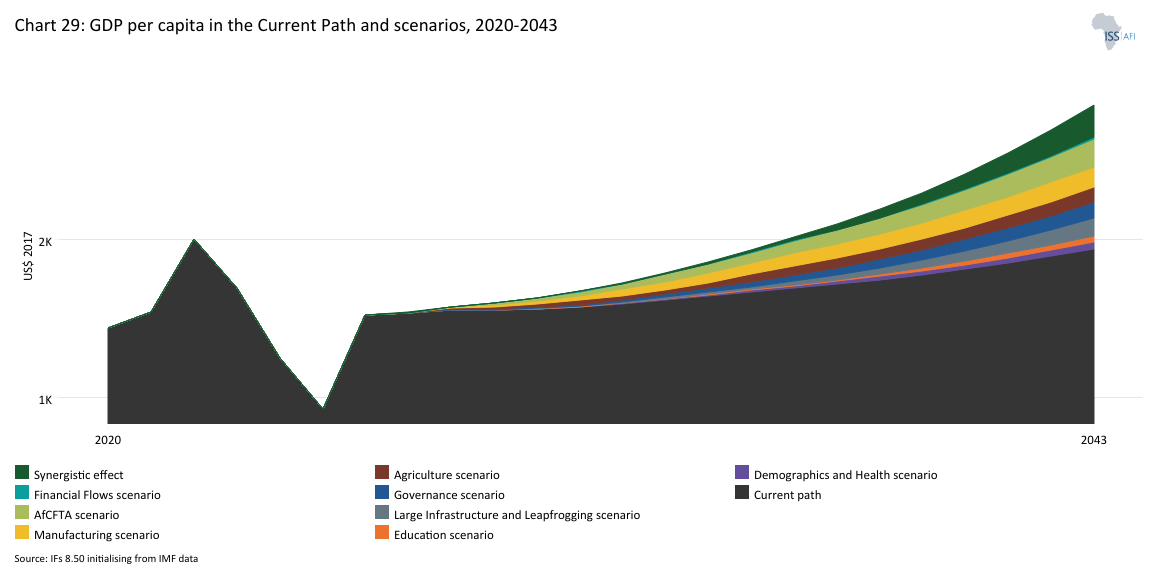

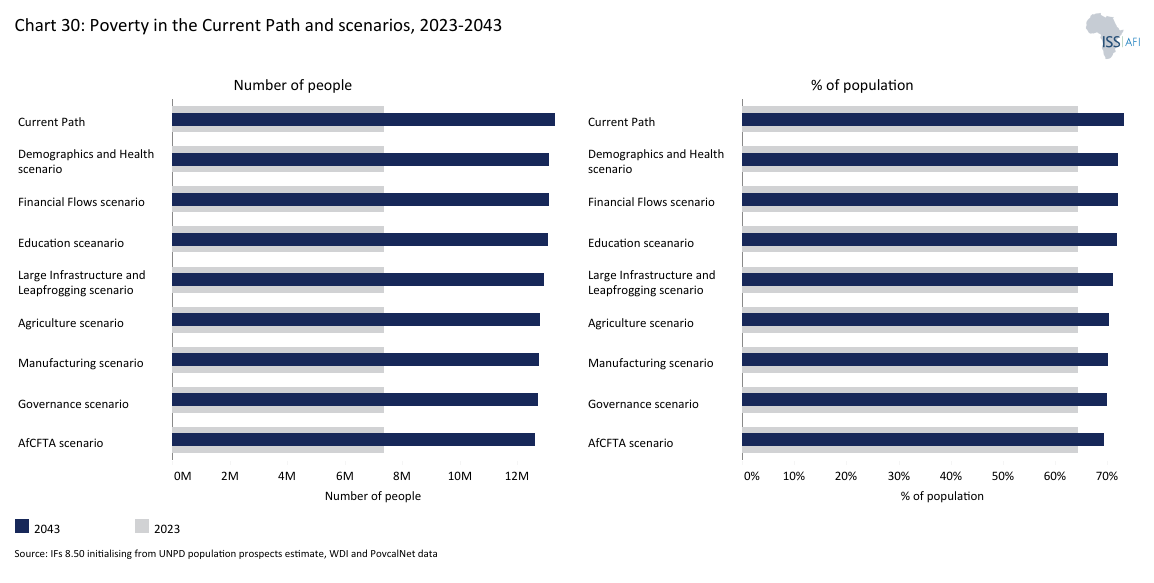

In the fourth section, we compare the impact of each of these eight sectoral scenarios with one another and subsequently with a Combined scenario (the integrated effect of all eight scenarios). In our forecasts, we measure progress on various dimensions such as economic size (in market exchange rates), gross domestic product per capita (in purchasing power parity), extreme poverty, carbon emissions, the changes in the structure of the economy, and selected sectoral dimensions such as progress with mean years of education, life expectancy, the Gini coefficient or reductions in mortality rates. Given the potential gains from deeper regional and continental trade integration for South Sudan, primarily through improved market access and lower trade costs, the AfCFTA scenario delivers the strongest results for reducing extreme poverty. The Governance, Manufacturing and Agriculture scenarios follow this. In addition, the AfCFTA scenario is projected to provide the highest GDP per capita, followed closely by the Manufacturing, Large Infrastructure and Leapfrogging scenarios.

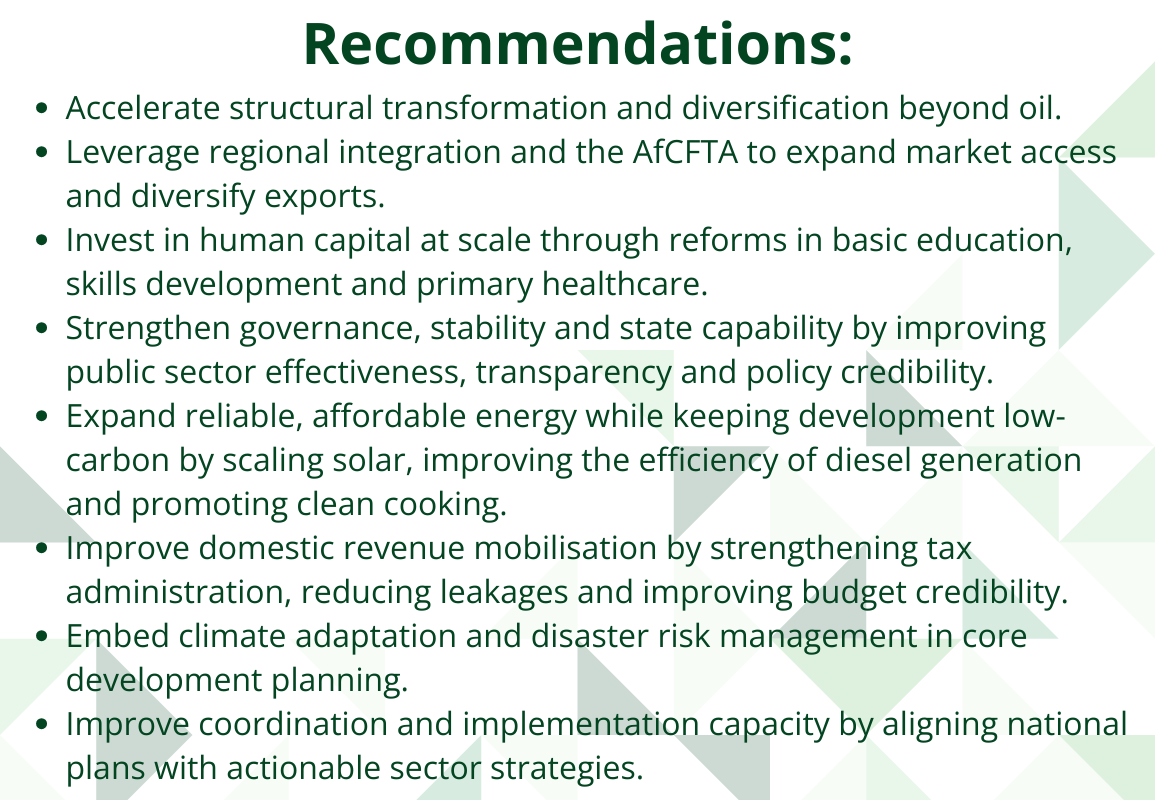

We end this page with a summarising conclusion offering key recommendations for decision-making. To achieve sustainable growth and reduce inequality, South Sudan needs to strengthen capable and accountable leadership, anchor decisions in evidence, and build institutions that promote transparency, inclusion and trust. Given the country’s fragility and heavy dependence on oil, this also requires stabilising the macroeconomy and improving security, while shifting toward a more diversified and trade-enabled growth path. Progress will depend on sustained investment in human capital (education, skills and health), basic infrastructure (roads, electricity and digital connectivity) and climate-resilient and renewable energy solutions, backed by effective public spending, stronger partnerships with communities and greater private-sector participation.

All charts for South Sudan

- Chart 1: Political map of South Sudan

- Chart 2: Population structure in the Current Path, 1990–2043

- Chart 3: Population distribution map, 2023

- Chart 4: Urban and rural population in the Current Path, 1990-2043

- Chart 5: GDP (MER) and growth rate in the Current Path, 1990–2043

- Chart 6: Size of the informal economy in the Current Path, 2020-2043

- Chart 7: GDP per capita in Current Path, 1990–2043

- Chart 8: Extreme poverty in the Current Path, 2020–2043

- Chart 9: National Development Plan of South Sudan

- Chart 10: Relationship between Current Path and scenarios

- Chart 11: Mortality distribution in the Current Path, 2023 and 2043

- Chart 12: Infant mortality rate in Current Path and Demographics and Health scenario, 2020–2043

- Chart 13: Demographic dividend in the Current Path and the Demographics and Health scenario, 2020–2043

- Chart 14: Crop production and demand in the Current Path, 1990-2043

- Chart 15: Import dependence in the Current Path and Agriculture scenario, 2020–2043

- Chart 16: Progress through the education funnel in the Current Path, 2023 and 2043

- Chart 17: Mean years of education in the Current Path and Education scenario, 2020–2043

- Chart 18: Value-added by sector as % of GDP in the Current Path, 2023 and 2043

- Chart 19: Value-add by the manufacturing sector in the Current Path and Manufacturing scenario, 2020–2043

- Chart 20: Exports and imports as % of GDP in the Current Path, 2000-2043

- Chart 21: Trade balance in the Current Path and AfCFTA scenario, 2020–2043

- Chart 22: Electricity access: urban, rural and total in the Current Path, 2000-2043

- Chart 23: Cookstove usage in the Current Path and Large Infra/Leapfrogging scenario, 2020–2043

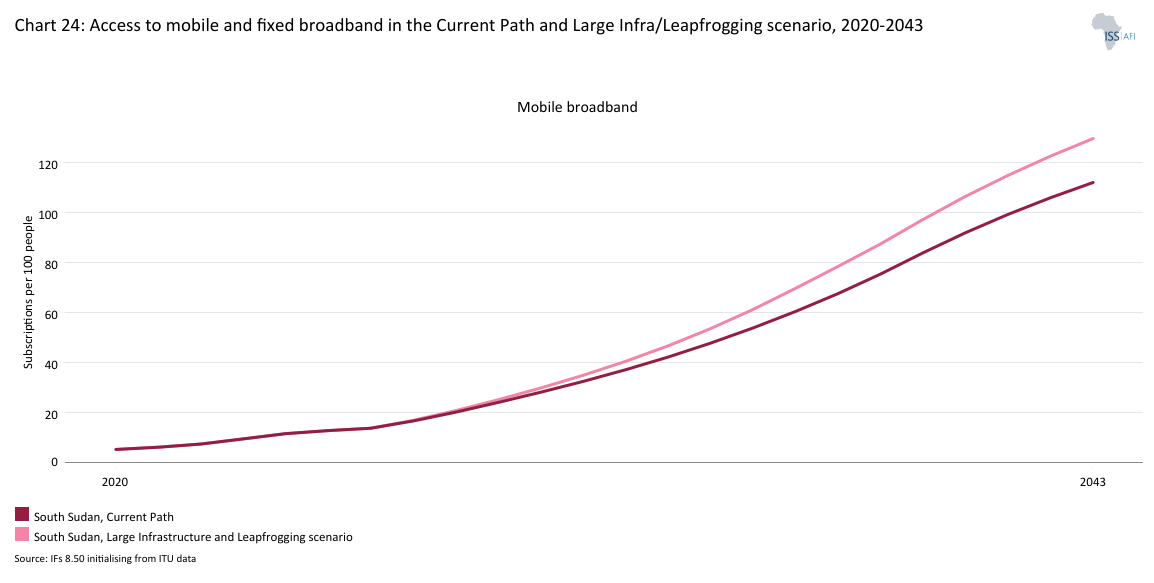

- Chart 24: Access to mobile and fixed broadband in the Current Path and the Large Infra/Leapfrogging scenario, 2020–2043

- Chart 25: FDI, foreign aid and remittances as % of GDP in the Current Path and in the Financial Flows scenario, 1990-2043

- Chart 26: Government revenue in the Current Path and Financial Flows scenario, 2020–2043

- Chart 27: Government effectiveness score in the Current Path, 2002-2043

- Chart 28: Composite governance index in the Current Path and Governance scenario, 2023 and 2043

- Chart 29: GDP per capita in the Current Path and scenarios, 2020–2043

- Chart 30: Poverty in the Current Path and scenarios, 2020–2043

- Chart 31: GDP (MER) in the Current Path and Combined scenario, 2020–2043

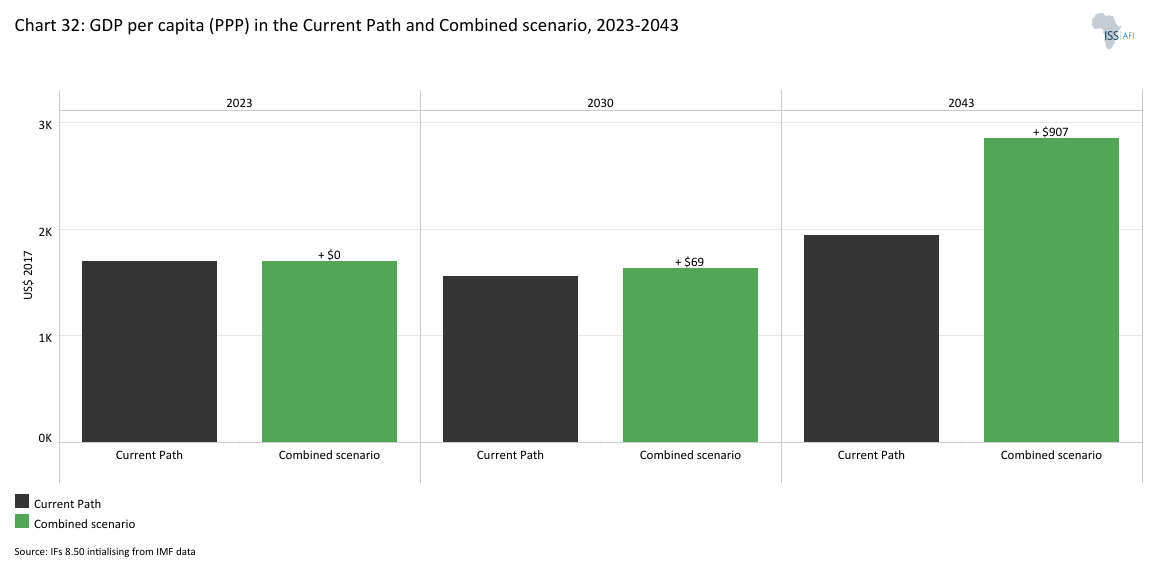

- Chart 32: GDP per capita in the Current Path and Combined scenario, 2023-2043

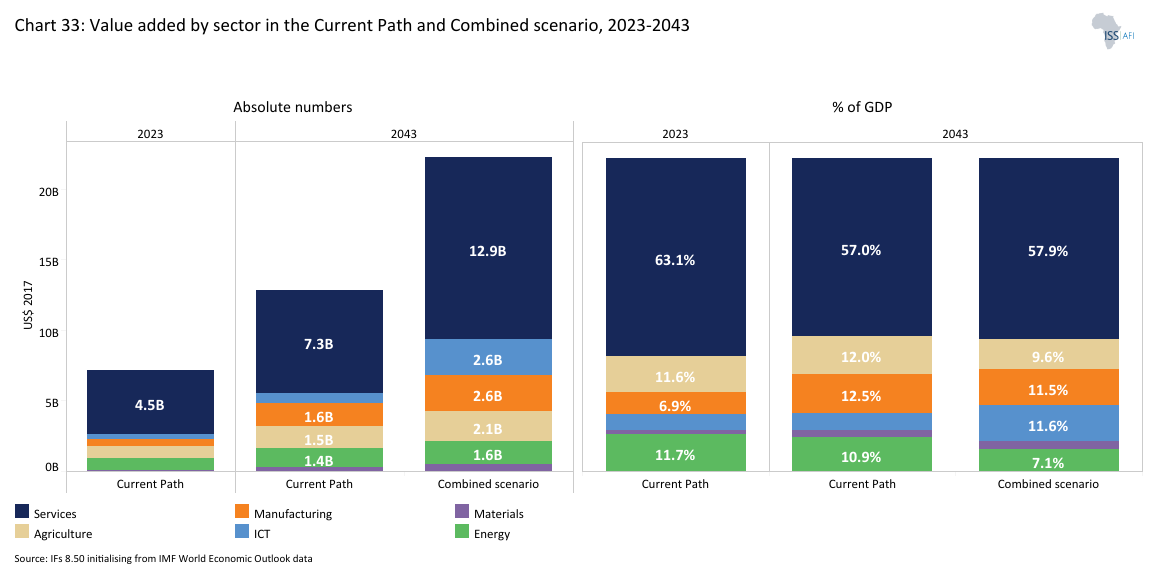

- Chart 33: Value-add by sector in the Current Path and Combined scenario, 2023 and 2043

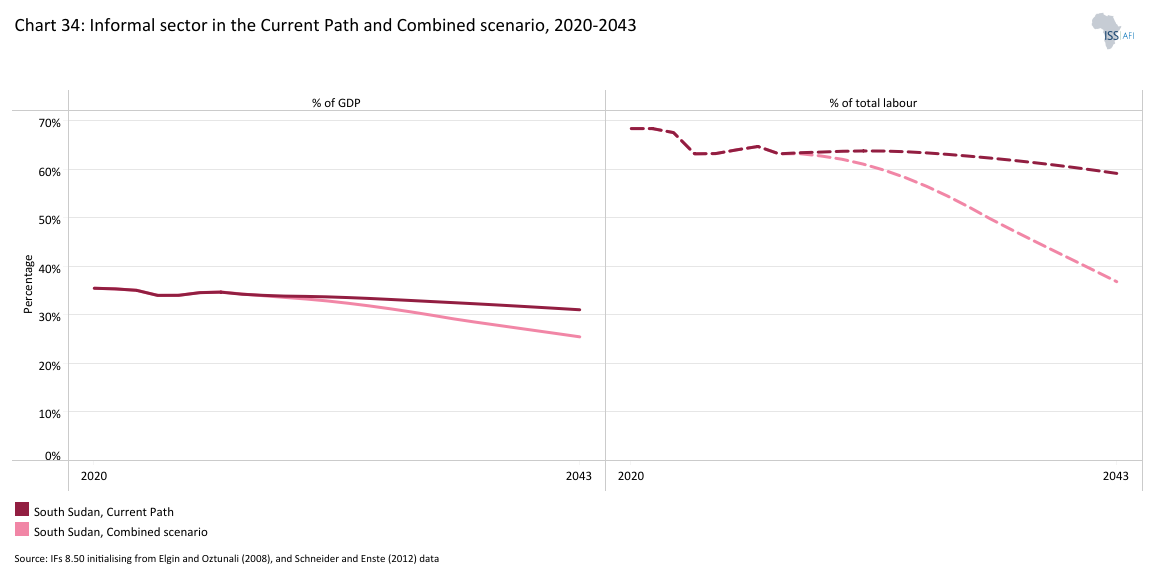

- Chart 34: Informal sector in the Current Path and Combined scenario, 2020–2043

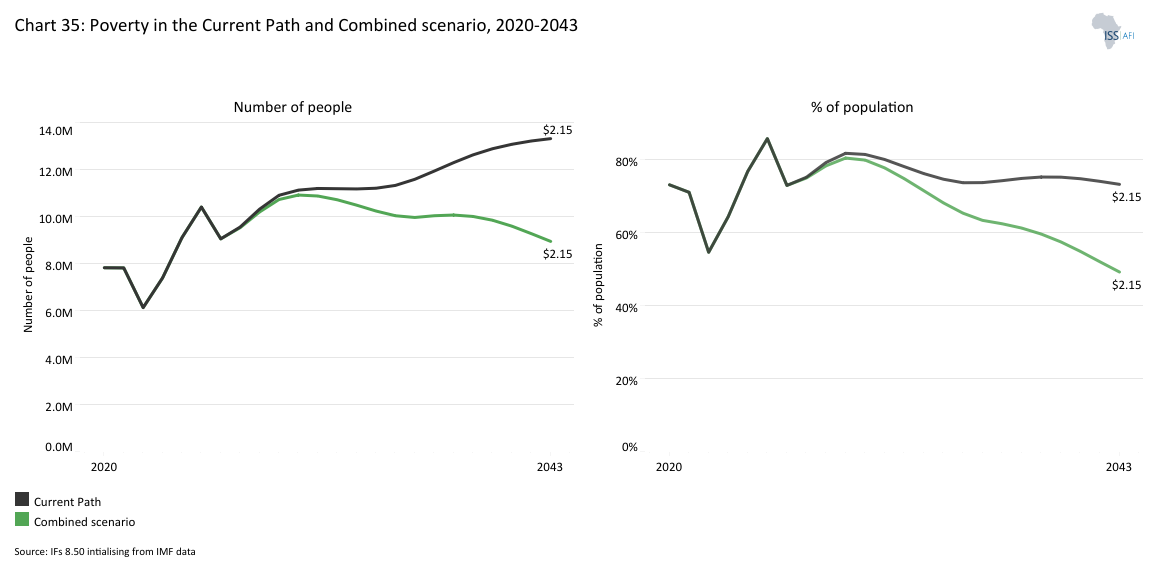

- Chart 35: Poverty in the Current Path and Combined scenario, 2023 and 2043

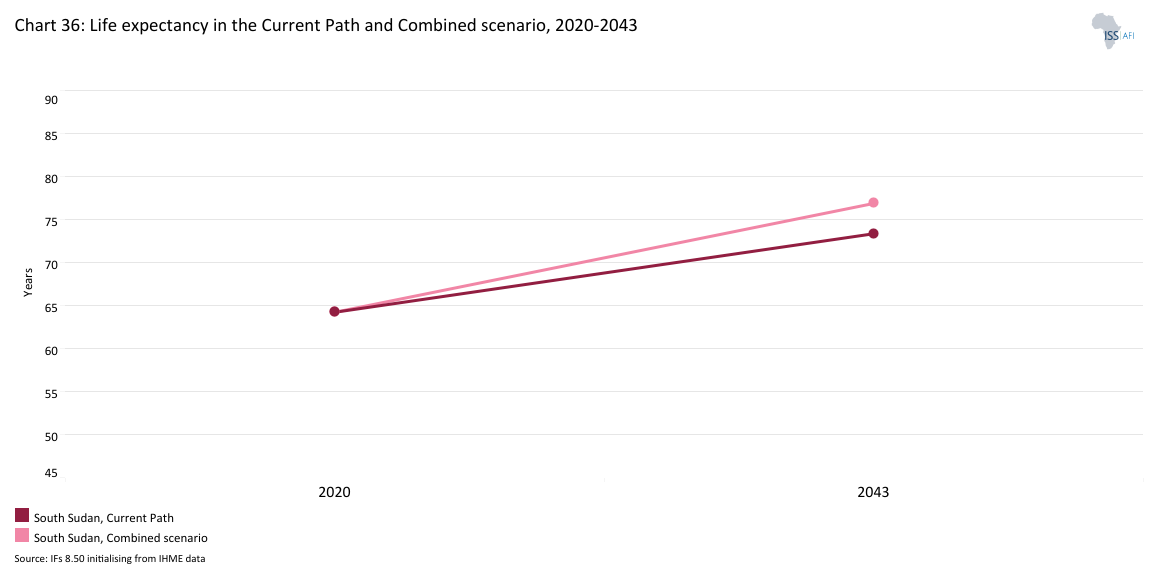

- Chart 36: Life expectancy in the Current Path and Combined scenario, 2020–2043

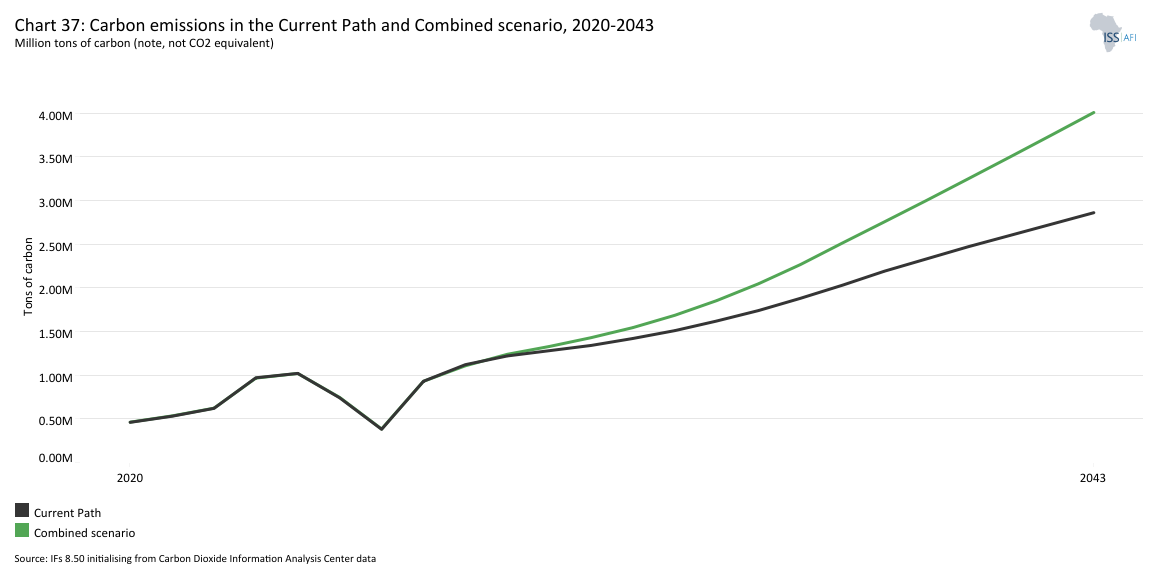

- Chart 37: Carbon emissions in the Current Path and Combined scenario, 2020–2043

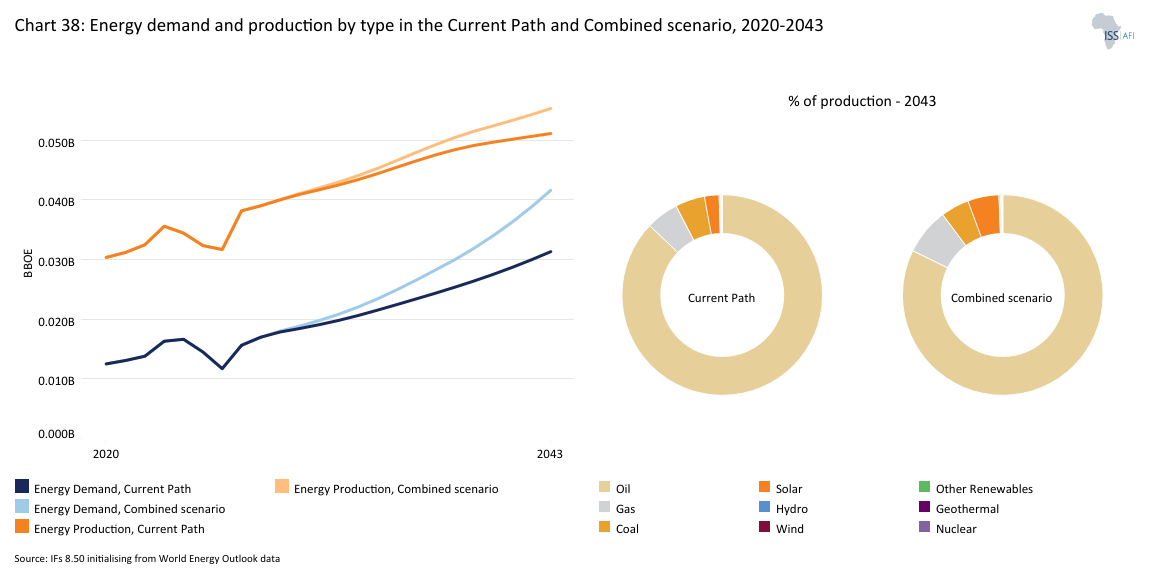

- Chart 38: Energy demand and production by type in the Current Path and Combined scenario, 2020-2043

-

Chart 39: Policy recommendations

Chart 39: Policy recommendations

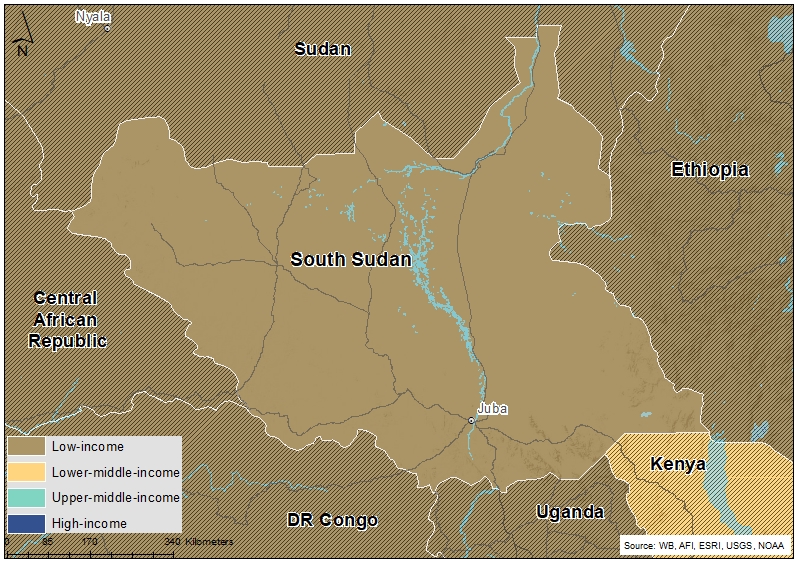

Chart 1 is a political map of South Sudan.

South Sudan, officially the Republic of South Sudan, is the 18th-largest country in Africa, and the 42nd-largest in the world, with a surface area of about 644 329 km². It is one of the sixteen landlocked countries in Africa, situated in the eastern region of the continent. South Sudan shares borders with Sudan to the north, Ethiopia to the east, Kenya to the southeast, Uganda to the south, the Democratic Republic of the Congo to the southwest and the Central African Republic to the west.

South Sudan gained independence from Sudan on 9 July 2011. This independence followed Africa’s longest civil war (1983-2005), which killed and displaced millions of people. The 2005 Comprehensive Peace Agreement not only ended that war but also established autonomy and a pathway to secession.

South Sudan’s independence followed an overwhelming 98.8% of voters supporting secession in the January 2011 referendum, making South Sudan the world’s newest nation and Africa’s 54th country. However, since its independence, South Sudan has struggled to establish a stable system of governance and has faced persistent challenges, including widespread corruption, political infighting and communal violence. The country ranked 180 out of 180 countries in Transparency International’s 2023 Corruption Perceptions Index, underlining the governance crisis that development efforts must confront.

In 2013, a civil war broke out between forces loyal to President Salva Kiir and those supporting his then-Vice President, Riek Machar. What began as a political power struggle quickly escalated into an ethnic conflict, causing immense suffering, widespread violence and mass displacement. Several peace agreements, most notably the Revitalised Agreement on the Resolution of the Conflict in South Sudan (R-ARCSS), signed in 2018, and the formation of a Transitional Government of National Unity (TGoNU) in 2020, have sought to restore stability and establish a power-sharing government. The transitional period was extended (from February 2025 to February 2027) to give more time for the government to implement provisions in the R-ARCSS and prepare the country for elections. Despite positive steps, the peace process faces challenges, such as the unification of armed forces and the delayed drafting of a permanent constitution.

Despite multiple peace deals, implementation lags, and unification of forces continues, constitutional reforms remain incomplete. Communal clashes and insecurity persist, and the Fragile States Index has consistently ranked South Sudan among the most fragile states (3rd in 2024). Furthermore, the country is in a severe humanitarian crisis. In 2025-2026, roughly 7.5 to 7.7 million South Sudanese face high levels of acute food insecurity (IPC Phase 3+), with some areas experiencing catastrophic conditions. Driven by chronic conflict, climate disasters like floods, and economic crises, this situation leaves millions reliant on dwindling humanitarian aid.

Beyond conflict, South Sudan’s physical environment also profoundly shapes its development prospects. South Sudan is a land of incredible diversity, combining within its boundaries much of the physical, social and economic variation seen throughout Africa as a whole. Its terrain is remarkably diverse, encompassing vast plains, swamps and tropical forests. The country experiences a tropical climate, with hot conditions year-round. The dry season from December to February brings intense heat and minimal rainfall, followed by a rainy season from June to September, which is cooler and more humid.

Climate variability, severe droughts and floods already cripple agriculture and infrastructure, a trend likely to worsen with ongoing climate change. Building climate resilience (as emphasised in Agenda 2063 and Sustainable Development Goal 13) is thus a key development priority. The central and northern regions are dominated by the sudd, one of the world’s most extensive wetlands. Yet, water management is a critical concern, given the country’s heavy dependence on the Nile River. Despite these environmental constraints, South Sudan possesses rich natural resources, including oil and fertile land that supports agriculture and livestock.

South Sudan is one of the world’s most oil-dependent economies. Oil has provided about 90% of government revenue and nearly all export earnings. This reliance makes the country extremely vulnerable to shocks. In 2024, for example, conflict in Sudan shut a pipeline carrying approximately 70% of South Sudan’s oil exports, causing a fiscal crisis. In essence, oil revenues initially helped unite warring factions in pursuit of independence, but later created perverse incentives that undermined governance reforms.

The total population of South Sudan was estimated at 11.5 million in 2023, predominantly African cultures that tend to adhere to Christian or animist beliefs. Juba is the capital and largest city of South Sudan. English is the official language, but Arabic and several indigenous languages, including Dinka, Nuer, Bari and Zande, are also widely spoken. The country’s rich ethnic and cultural diversity is reflected in its vibrant traditions, music, art and community practices, which continue to play an essential role in daily life and national identity. In terms of education, only about 35% of adults are literate, reflecting the toll of conflict on education.

South Sudan is a member of several key regional organisations, including the East African Community (EAC), the Intergovernmental Authority on Development (IGAD) and the African Union (AU). Joining the EAC in 2016 signalled South Sudan’s commitment to regional economic integration, although full integration (for example, under the standard market protocols) is ongoing. These regional ties are viewed as avenues to bolster trade, infrastructure links and peace–aligning with the AU’s Agenda 2063 aspiration for an ‘integrated, prosperous and peaceful’ continent.

This complex backdrop frames South Sudan’s current development trajectory and the potential impact of various sectoral interventions, as explored in the sections that follow.

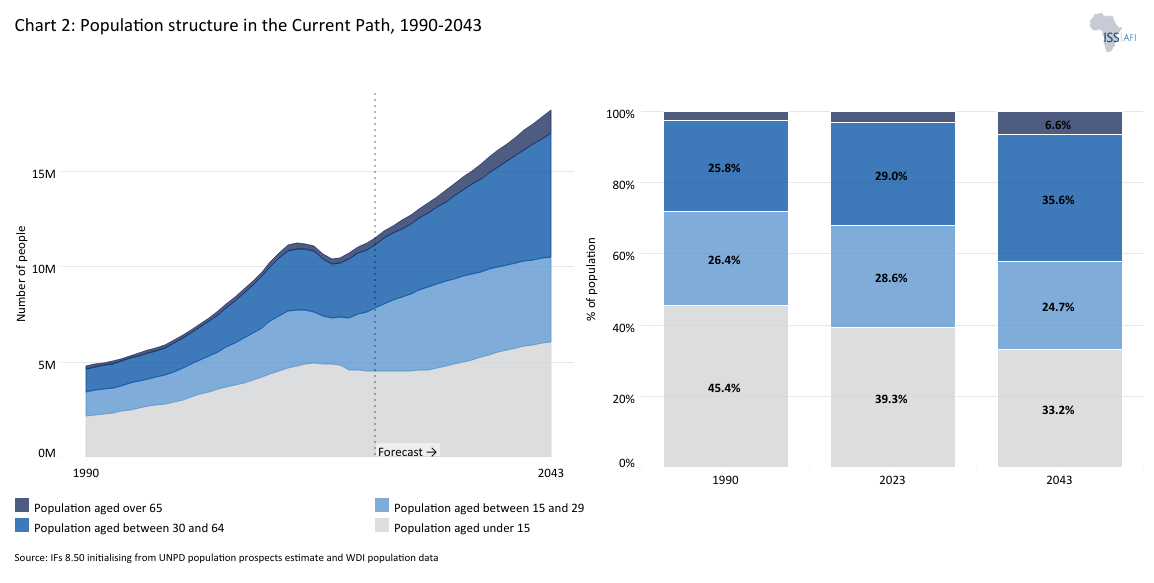

Chart 2 presents the Current Path of the population structure from 1990 to 2043.

A country’s population characteristics are fundamental to shaping its long-term social and economic trajectory. Demographic factors such as population size, age structure, fertility rates, migration patterns and levels of urbanisation directly influence labour markets, service delivery, governance capacity and social cohesion.

Analysing South Sudan’s demographic structure is particularly critical, as the country’s youthful population, high fertility rates, widespread displacement and uneven access to education and healthcare present both significant challenges and potential development opportunities. These demographic dynamics provide insight into South Sudan’s development prospects, informing policy choices on human capital investment, economic growth and stability.

South Sudan’s population remains among the youngest in the world, with a median age of just 19.2 years in 2023, compared to the averages of 20.4 and 31.9 years, respectively. This youthful demographic profile reflects persistently high fertility rates and a rapidly growing population, shaped by decades of conflict, limited access to education and healthcare, and constrained economic opportunities. On the Current Path, South Sudan's median age will increase to 25.1 years by 2043.

In 2023, South Sudan had an estimated fertility rate of 3.9 children per woman and a total population of approximately 11.5 million. The working-age population (15–64 years) accounted for 57.6% of the total population, slightly higher than the average of 54.5% observed among low-income countries in Africa. If this working-age population is supported through adequate education and skills development and effectively absorbed into the economy, it has the potential to boost productivity, stimulate economic growth and contribute to the demographic dividend. However, in the absence of sufficient employment opportunities and investment, this potential may remain underutilised, increasing pressure on public services and constraining inclusive economic growth.

As of 2023, South Sudan’s unemployment rate was estimated at around 12.5%, indicating that roughly 1 in 8 working-age individuals actively seeking employment remained unemployed. This labour market challenge is compounded by the country’s low level of human capital. In the same year, South Sudan ranked last out of 193 countries on the Human Capital Index, with a score of 0.39, reflecting significant constraints in education, skills and health outcomes that limit workforce productivity.

By 2043, the country’s population will grow to approximately 18.2 million. Its average total fertility rate will decline to 3.1 births per woman, far above the 2.1 replacement rate required to maintain population size without immigration. However, South Sudan is significantly impacted by the war in Sudan, especially from a vast and growing number of refugees, which has introduced uncertainty to these forecasts.

South Sudan’s youth bulge (15–29 year-olds as a share of adults) at approximately 47% in 2023 is among the highest globally, often associated with instability if not matched with economic opportunities. On the Current Path, this figure will decline to 36.9% by 2043. In addition to the need for greater spending on education, health services, and job creation, a large number of young adults can drive positive political change in a country through youth activism; however, they can also sow the seeds of socio-political instability in the absence of economic opportunities.

Children under the age of 15 constitute approximately 39.3% of the total population (significantly higher than the world average of 25.1% in 2023), placing significant pressure on already overstretched public services, particularly in education, health and social protection. The elderly population aged 65 years and above remains relatively small, accounting for just 3.1% of the population, reflecting lower life expectancy.

South Sudan’s limited provision of healthcare, combined with widespread poverty, recurrent violence and a high burden of communicable diseases, continues to constrain life expectancy, which remains well below the global average for both men and women. In 2023, life expectancy in South Sudan was estimated at 66.5 years, slightly lower than the African average of 67.3 years and significantly below the global average of 74.2 years in the same year.

On the Current Path, the proportion of children under 15 years will decline to 33.2% of the total population by 2043, while the share of the elderly aged 65 years and above will more than double, rising to 6.5% compared to 2023. This shift reflects gradual improvements in life expectancy, which will increase to 73.4 years by 2043.

As the population structure evolves, South Sudan will need to prepare for future demands on its social protection and health systems. However, child- and youth-focused investments will remain paramount for the next two decades. The country’s slow demographic transition underscores the need for targeted policy interventions that accelerate fertility declines, improve youth outcomes, and expand opportunities for productive employment. The country’s ability to shift towards a more balanced age structure and unlock a demographic dividend will depend on sustained progress in economic growth and peacebuilding.

When the ratio of the working-age population (15-64 years of age) to dependants (children and the elderly) is 1.7 to one or higher, countries often experience more rapid growth, known as the demographic dividend, provided the workforce is appropriately skilled and absorbed into the labour market. In 2023, South Sudan’s ratio of working-age persons to dependants was 1.4 to one. On the Current Path, South Sudan is likely to only enter a potential demographic window of opportunity around 2053.

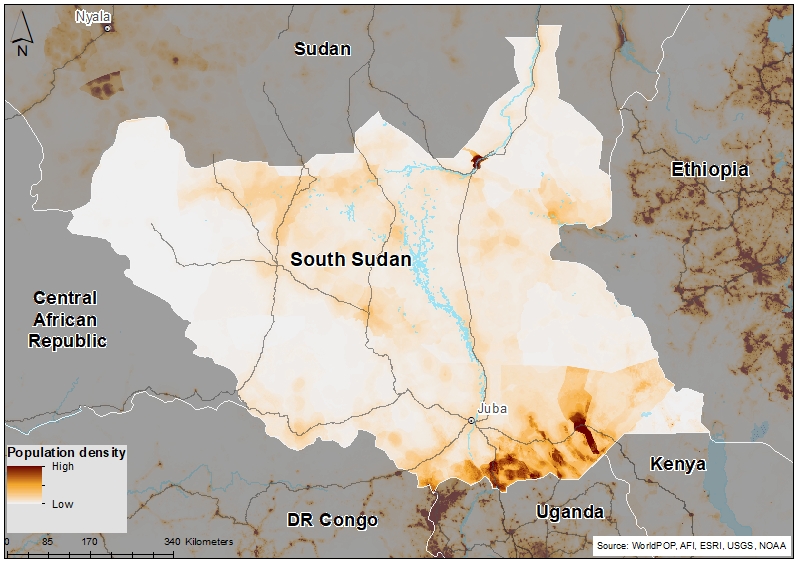

Chart 3 presents a population distribution map for 2023.

South Sudan’s population is relatively low in density, but settlement patterns are highly uneven, with the highest concentrations in and around major urban centres such as Juba, the capital. Much of the country’s territory remains sparsely populated due to ongoing challenges related to conflict, displacement and environmental constraints, including seasonal flooding and limited infrastructure.

In 2023, population density was 0.18 people per hectare, well below the averages for low-income African countries (0.46) and the continent (0.50). This distribution reflects the effects of humanitarian pressures and slow urbanisation linked to protracted insecurity and repeated population movements. These factors continue to shape settlement patterns in South Sudan, reinforcing the concentration of people in areas that are accessible and relatively secure.

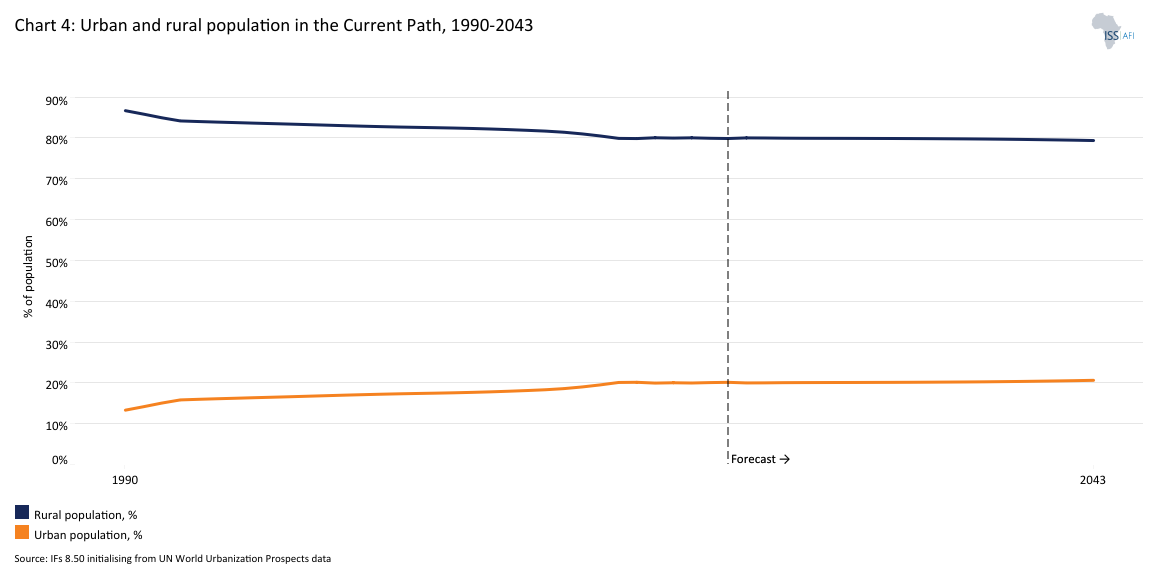

Chart 4 presents the urban and rural population in the Current Path, from 1990 to 2043.

South Sudan’s urbanisation rate is very low; the population is mainly rural, at 79.5% in 2023, above the averages of 67.3% and 55.7% for low-income African countries and Africa, respectively. This makes the country one of the least urbanised in the Horn, East and Central Africa (HECA) region. This persistent rural majority reflects limited structural transformation and slow urbanisation, in contrast to the broader trends across low-income African countries. Between 1990 and 2023, the rural share of South Sudan’s population declined by just 7.2 percentage points, a far slower shift than the 12.4 percentage point drop seen on average among its income peers.

On the Current Path, the rural population is only expected to decline by approximately 0.2 percentage points to 79.4% by 2043. This means the urbanisation rate only marginally increases from about 20.5% in 2023 to 20.6% by 2043. Thus, South Sudan will remain largely rural across the Current Path forecast horizon.

The predominance of the rural population has important implications for South Sudan’s development strategy and the allocation of public investment. It underscores the need to prioritise rural livelihoods, agricultural transformation and the expansion of basic service delivery beyond urban centres. Key interventions will include strengthening rural infrastructure (particularly roads, irrigation and market connectivity), supporting productive and climate-resilient agriculture, and scaling up education and health services in underserved areas. In the absence of faster urbanisation and structural transformation, a sustained focus on rural development will remain essential to promote inclusive growth, enhance human capital and accelerate poverty reduction.

In addition to forced urban migration driven by armed conflict and its effects, rural-to-urban migration is driven by the search for employment opportunities and education, as well as 'push factors' such as poverty, food insecurity, crop failure, land shortage and lack of cattle.

With proper planning, urbanisation can play a pivotal role in driving economic growth and development by accelerating the provision of a range of services (e.g., education and health), fostering entrepreneurship and boosting productivity. In addition, adequate and appropriate urban planning is essential to mitigate the impacts of climate change, such as flooding.

However, if poorly managed, urbanisation can exacerbate structural challenges, fueling unemployment, urban poverty and rising demand for health services, sanitation and housing. It can also accelerate the growth of informal settlements and contribute to environmental degradation. In South Sudan, these risks are already evident: in 2022, an estimated 94% of urban residents lived in slums.

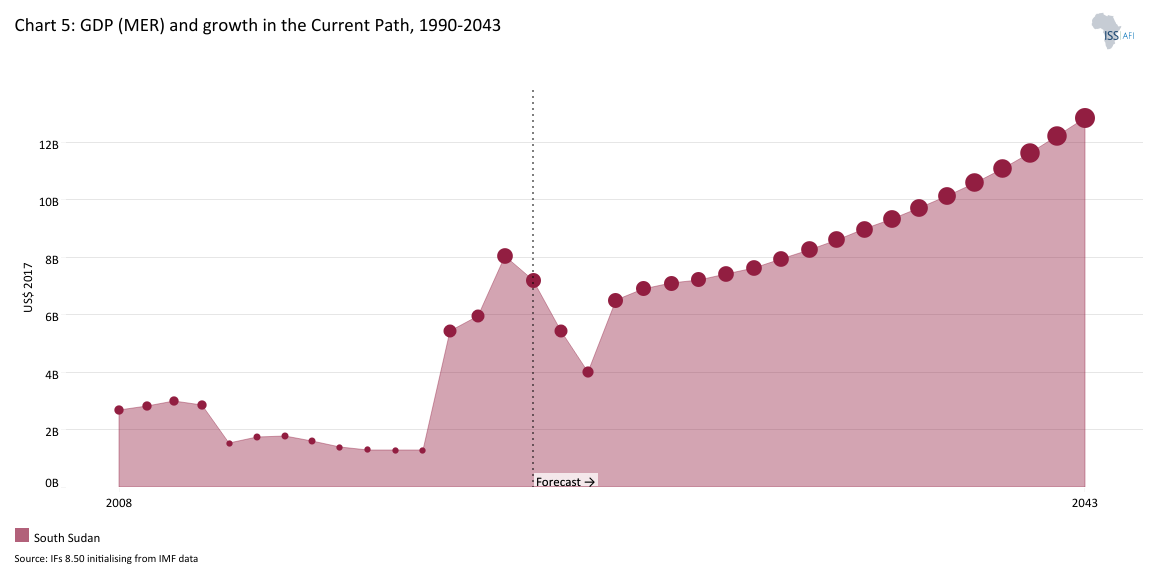

Chart 5 presents GDP in market exchange rates (MER) and growth rate in the Current Path from 1990 to 2043.

South Sudan’s economy remains heavily dependent on oil production and continues to be constrained by political instability and the enduring legacy of conflict. As a result, the country has experienced a highly volatile growth path since independence. In 2023, GDP at market exchange rates (MER) was estimated at US$7.2 billion, marking a strong rebound from the severe contraction during the civil conflict. In 2017, GDP fell to US$1.3 billion, reflecting the scale of economic disruption between 2013 and 2018.

The country’s GDP growth rate over the past decades has alternated between deep recessions and rapid expansions, driven by conflict-related shocks, intermittent oil production shutdowns and intermittent peace efforts. Between 2019 and 2023, the country experienced relatively rapid economic growth, averaging 23.8% per annum.

This recovery is linked to improved security following the 2018 Revitalised Peace Agreement and the gradual reactivation of oil exports, which account for the majority of government revenue and export earnings. While the post-2018 period saw a return to positive growth, the country still faces significant challenges in consolidating these gains. In 2023, South Sudan’s real GDP growth rate was negative, underscoring persistent structural weaknesses, including limited economic diversification, weak infrastructure and ongoing humanitarian needs.

Oil exports account for approximately 90% of government revenue and a significant share of the country's GDP. Revenues are shared with Sudan through pipeline and transit agreements. However, the country’s reliance on oil exposes it to fluctuations in global prices and disruptions in production due to insecurity.

To reduce vulnerability to oil price shocks and production disruptions, the government is pursuing a diversification agenda centred on agriculture, fisheries, forestry and the expansion of small-scale manufacturing and value addition. With vast arable land, water resources, and a youthful population, South Sudan has significant development potential if peace and stability are maintained. However, realising this potential will require overcoming significant structural constraints, including severe infrastructure gaps, persistent food insecurity and ongoing political fragility. South Sudan’s natural resource endowment, strong social resilience and ongoing peace efforts position it for gradual economic transformation toward a more stable and prosperous future.

Looking ahead on the Current Path, South Sudan is forecast to maintain moderate GDP growth averaging around 4.1% per annum between 2027 and 2043, but the outlook is contingent on continued political stability. The country’s GDP will reach US$12.8 billion by 2043, below the average expected for low-income countries in Africa. This underscores the need for targeted policies to foster private-sector-led growth, enhance agricultural productivity, and improve infrastructure resilience.

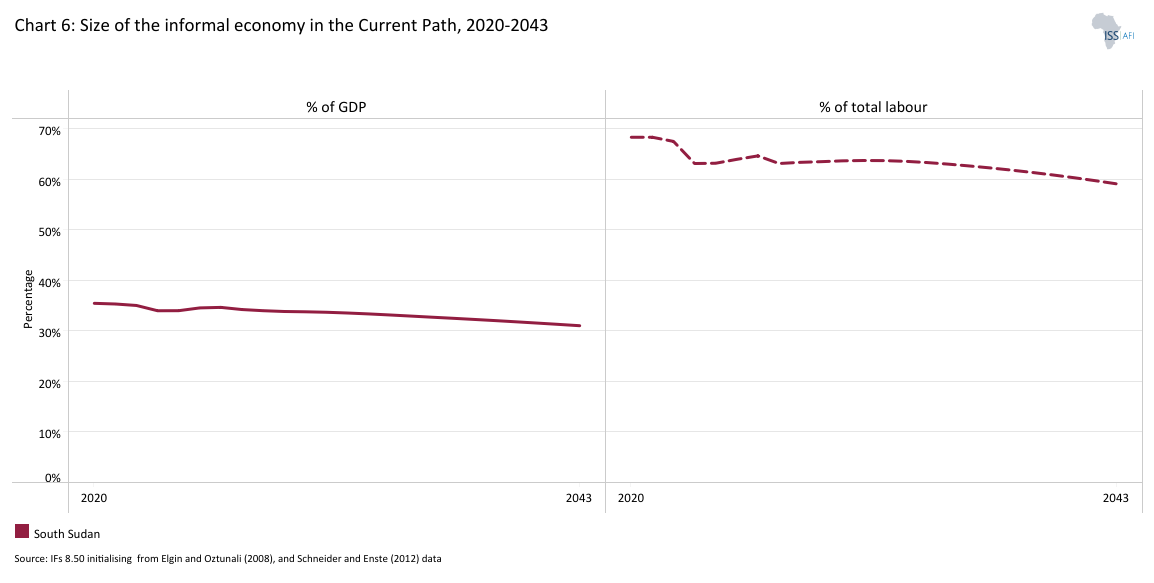

Chart 6 presents the size of the informal economy as per cent of GDP and per cent of total labour (non-agriculture), from 2020 to 2043. The data used in our modelling are essentially estimates and may therefore differ from other sources.

The informal economy comprises activities that have market value and would add to tax revenue and GDP if they were recorded. Countries with high informality face a host of development challenges, including low revenue mobilisation, higher poverty, lower per capita incomes, greater inequality and weaker productivity investment. Therefore, high levels of informality tend to constrain economic growth but often serve as a survival sector in poor countries.

In South Sudan, informal economic activities are more than just a means of survival; they are central to the lives of South Sudanese people. They also reflect quiet determination and strong community organisation. Because formal institutions are often weak or unstable, markets, trade routes and small farming or service businesses become spaces where communities manage their own affairs and support one another. Through these activities, people also show resistance by building independence from armed groups and exploitative authorities.

In many regions of South Sudan, people avoid high taxes imposed by the government, form mutual support groups and establish informal cooperatives to maintain trade. These actions have helped limit elite control and protect people’s independence in daily lives. In South Sudan, the informal sector has also helped rebuild relationships between divided communities. Traders, transport workers and producers from diverse ethnic groups often rely on one another, fostering trust through mutual exchange.

Despite its importance, South Sudan's informal sector has experienced a slight decline in its share of GDP over time. In 2023, the informal economy accounted for approximately 34% of South Sudan's GDP, down from about 35.5% in 2020. Despite this reduction, South Sudan's informal economy remains above the 2023 averages of 31.9% for low-income countries in Africa and 26.9% for the continent as a whole.

With nearly 80% of South Sudanese residing in rural areas and relying on subsistence agriculture for their livelihoods, the informal economy has helped South Sudan reduce extreme poverty. In 2023, an estimated 63.1% of the total labour force (non-agriculture) was informally employed, and women constituted 51% of the total labour force in the informal economy.

The informal sector’s share of GDP will further decline to 31% by 2043, and informal employment to 59.1%. This suggests a slow but steady shift in the economy's structure. Productivity in informal work remains substantially lower than in the formal sector, as evidenced by the wide gap between the informal share of employment and its contribution to GDP. High informality under the Current Path underscores the need to improve the business climate and develop skills to transition workers into the formal sector.

While the informal economy provides an important safety net for South Sudan’s large and growing working-age population, it also hinders productivity growth, weakens the tax base and complicates the implementation of effective economic policies. Reducing informality would enable more workers to access better wages, stronger protections and the benefits of redistribution. South Sudan, therefore, needs to shrink the informal economy with minimal disruption by lowering barriers to business registration, tackling corruption and expanding access to education and finance.

Without such reforms, the informal sector is likely to remain a significant component of South Sudan’s non-agricultural labour market for the foreseeable future.

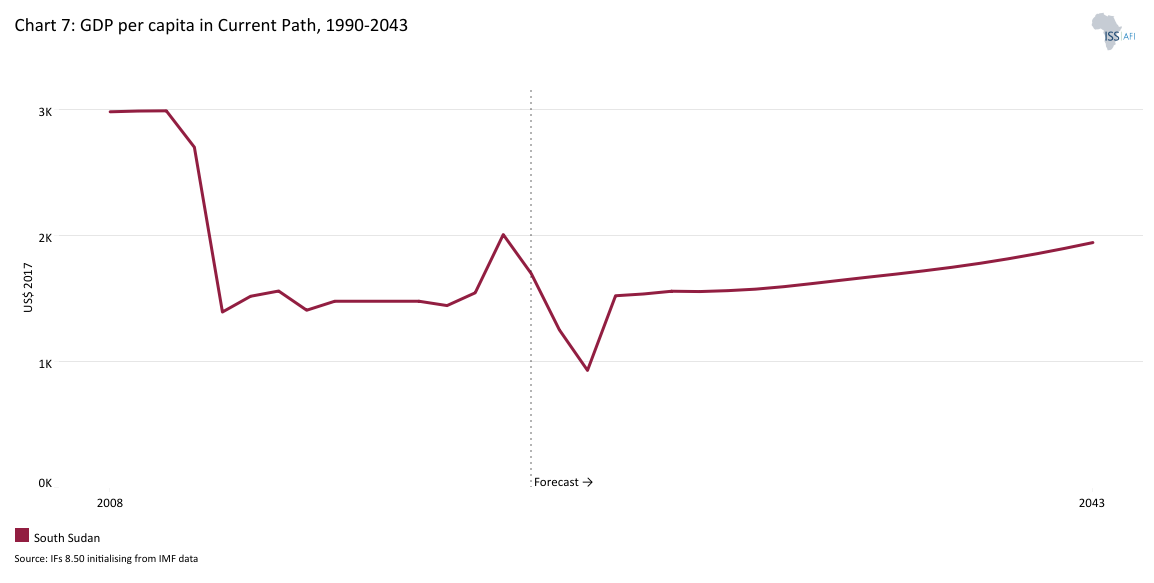

Chart 7 presents GDP per capita in the Current Path, from 1990 to 2043, compared with the average for the Africa income group.

In 2014, South Sudan was reclassified from lower-middle-income to low-income status after a steep decline in GNI per capita (Atlas method), the indicator used by the World Bank for income group classification. Over the same period, GDP per capita (PPP) dropped from about US$2 697 in 2011 to roughly US$1 557 in 2014, highlighting the scale of the contraction. Since then, South Sudan has remained a low-income economy, reflecting persistently weak per capita income and ongoing macroeconomic fragility. This reclassification demonstrates the country’s prolonged political challenges and the disruption of its main growth and revenue base, the oil sector, which continues to dominate exports and fiscal resources.

In 2023, GDP per capita in South Sudan stood at about US$1 476, slightly below the African low-income group average of around US$1 879. Looking ahead, the Current Path forecasts that South Sudan’s GDP per capita will increase to US$1 940 by 2043. This recovery remains lower than that of the income peers group, whose average GDP per capita will nearly double to US$2 985 by 2043.

The widening divergence highlights the ongoing constraints facing South Sudan, including limited economic diversification, weak institutions and the slow pace of structural reforms. Without more effective measures to address these constraints—such as improving fiscal management, promoting private-sector-led growth, and fostering greater political stability—South Sudan is likely to continue lagging behind its income peers in broad-based improvements in living standards.

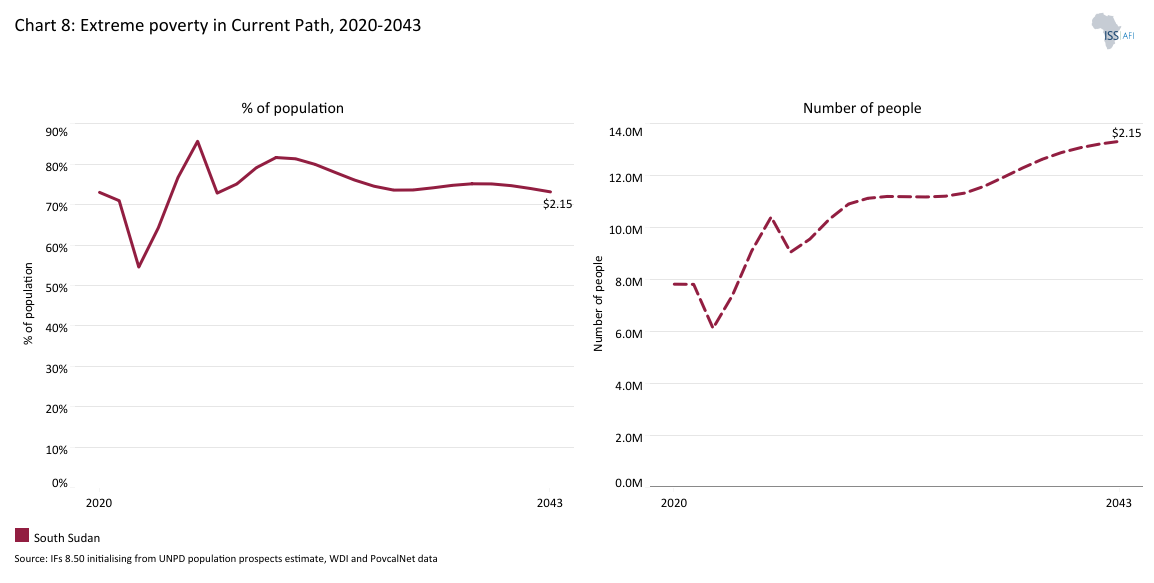

Chart 8 presents the rate and number of poor people in the Current Path from 2020 to 2043.

In 2022, the World Bank updated the poverty lines to 2017 constant dollar values as follows:

- The previous US$1.90 extreme poverty line is now set at US$2.15, also for use with low-income countries.

- US$3.20 for lower-middle-income countries, now US$3.65 in 2017 values.

- US$5.50 for upper-middle-income countries, now US$6.85 in 2017 values.

- US$22.70 for high-income countries. The Bank has not yet announced the new poverty line in 2017 US$ prices for high-income countries.

As a low-income country, South Sudan uses the international monetary poverty line of US$2.15 per person per day. Using this benchmark, the country’s poverty rate was 64.3% in 2023—equivalent to roughly 5.9 million people—well above the average rate of around 45% for low-income African countries. On the Current Path, poverty will rise to 81.4% by 2030 and then decline to 73.2% by 2043. Although the rate will decrease from 2030, the absolute number of South Sudanese living in extreme poverty will increase from 9.8 million in 2030 to 11.1 million by 2043 as the population grows.

On its current development trajectory, South Sudan is likely to struggle to reduce poverty due to a combination of prolonged conflict and insecurity, weak economic performance, limited job creation and heavy dependence on subsistence livelihoods and humanitarian support. These pressures are compounded by high inflation, macroeconomic instability and disruptions to markets and basic services, which constrain household incomes and undermine resilience. According to the Global Inequality Update 2024, published by the World Inequality Lab, the top 10% of the South Sudanese population capture over 62% of the country's wealth. In contrast, the bottom 50% of the population captured less than 5% of South Sudan's national income. This implies that growth alone, without inclusive targeted policies, will not address poverty and inequality.

Monetary poverty provides only a partial view of the situation. The global Multidimensional Poverty Index (MPI) offers a broader perspective by assessing acute poverty through overlapping deprivations across 10 indicators, divided into three equally weighted dimensions: health, education and standard of living. The MPI complements the international poverty line of US$2.15 a day by identifying who is multidimensionally poor and by showing the composition of multidimensional poverty. The headcount or incidence of multidimensional poverty is often several percentage points higher than that of monetary poverty. This implies that individuals living above the monetary poverty line may still suffer from deprivations in health, education, and/or the standard of living.

According to the 2022 Global MPI report, 91.9% of the population in South Sudan was multidimensionally poor in 2010, with an additional 6.3% classified as vulnerable to multidimensional poverty, compared to the international monetary poverty rate of 35.8% at US$2.15 per day in the same year.

Chart 9 depicts the National Development Plan of South Sudan.

South Sudan's national development plan has evolved over several years to address shifting economic, political and social challenges. The first national development plan, the South Sudan Development Plan (SSDP) 2011–2013, was effective immediately after independence (2011). It was primarily a state-building and service-delivery framework, aimed at laying the foundations for governance, economic recovery and human development in the new country. Its organising logic was structured around four pillars: governance, economic development, social and human development, and conflict prevention and security. The plan also emphasised building national systems for budgeting, implementation and monitoring and evaluation—recognising institutional weakness as a key constraint.

The 2013 conflict and subsequent instability fundamentally reshaped national development planning. As violence intensified and displacement expanded, planning priorities shifted away from long-term development and toward stabilisation, emergency service delivery and humanitarian response.

Against the backdrop of the protracted conflict and the 2018 Revitalised Peace Agreement, South Sudan adopted the National Development Strategy (NDS) 2021–2024 in late 2018. The strategy centred on consolidating peace, restoring basic services and supporting economic recovery in a context of continued fragility. It also sought to align national priorities with the Sustainable Development Goals (SDG) and the African Union’s Agenda 2063, consistent with development planning trends in other low-income and conflict-affected settings. Additionally, the NDS served as a platform for donor coordination and institutional strengthening.

In September 2025, the government unveiled the South Sudan Development Plan (SSDP) 2026–2036, marking a clear shift from shorter planning cycles to a 10-year national development framework. Reporting around the launch frames the SSDP as a structured roadmap aimed at stability, resilience and sustainable development. However, with national elections on the horizon (postponed to 2027 under the peace agreement) and the SSDP just launched, South Sudan has a narrow window to solidify peace and chart a new course.

The eight sectoral scenarios as well as their relationship to the Current Path and the Combined scenario are explained in the Technical page. Chart 10 summarises the approach.

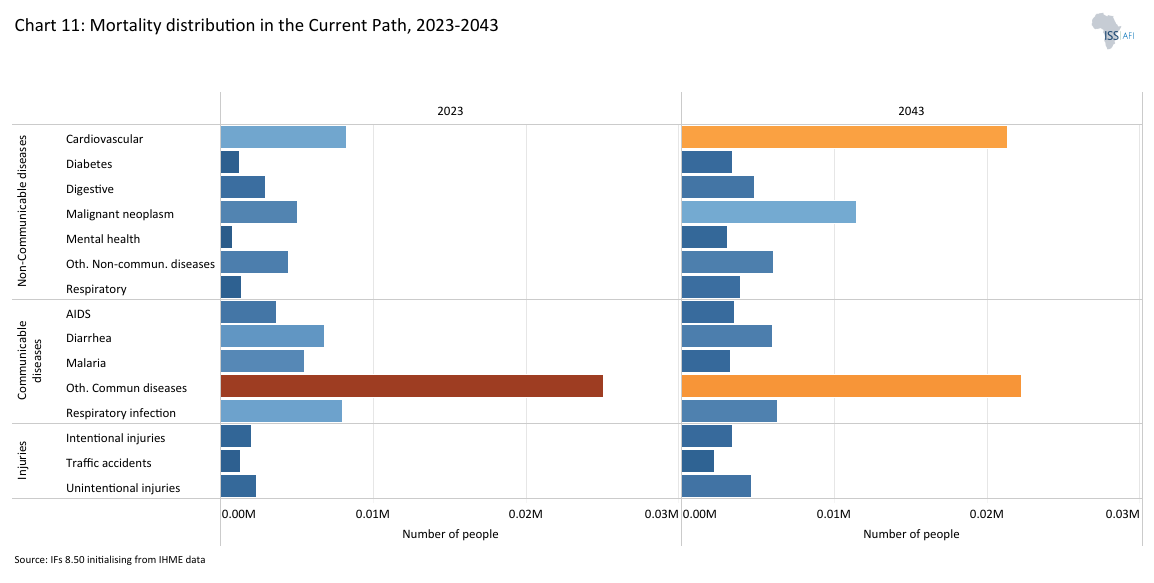

Chart 11 presents the mortality distribution in the Current Path for 2023 and 2043.

The Demographics and Health scenario envisions ambitious improvements in child and maternal mortality rates, enhanced access to modern contraception, and decreased mortality from communicable diseases (e.g., AIDS, diarrhoea, malaria, respiratory infections) and non-communicable diseases (e.g., diabetes), alongside advancements in safe water access and sanitation. This scenario assumes a swift demographic transition, supported by increased investments in health and water, sanitation, and hygiene (WaSH) infrastructure.

Visit the themes on Demographics and Health/WaSH for more details on the scenario structure and interventions.

There is a close relationship between population size and health. A country's health status affects fertility, mortality and morbidity rates, while rapid population growth increases the demand for essential resources, including nutrition and healthcare.

South Sudan faces significant health and demographic challenges shaped by population dynamics, a fragile healthcare system, prolonged conflict and displacement, and challenging socioeconomic conditions. The Government of South Sudan’s Ministry of Health has consistently described the health system as severely constrained. Widespread insecurity and the looting of health supplies and assets, including the closure of health facilities, have significantly reduced health service delivery in most states. However, recent surveys conducted in certain parts of the country indicate that nearly 80% of the population reported having access to healthcare, a finding widely attributed to the strong presence of humanitarian actors providing health services. Still, a range of indicators remains particularly poor.

Key challenges include persistently high levels of morbidity and mortality, especially among vulnerable groups such as mothers and newborns, alongside limited coverage of essential health services and uneven quality of care. Mortality distribution is influenced by a combination of communicable diseases (CDs) and non-communicable diseases (NCDs).

Communicable diseases (including malaria, respiratory infections and diarrhoeal diseases) accounted for the majority of deaths, about 67% of total mortality in 2023. CDs typically dominate in younger populations, and, as a result, South Sudan will undergo its epidemiological transition by 2039, when deaths from NCDs exceed those from CDs, seven years later compared to the average for low-income Africa. By 2043, NCDs will account for about 57% of mortality, a 6 percentage-point increase compared to 2039.

At a disaggregated level, cardiovascular and lower respiratory infections were major contributors to death in South Sudan. Cardiovascular disease remains the leading cause of death among the elderly. The lack of adequate healthcare access, particularly in rural areas, worsens the effects of these illnesses. Inadequate sanitation, unsafe drinking water and limited access to proper hygiene are major factors contributing to deaths from diarrhoeal diseases, particularly among children.

South Sudan remains far from having universal access to water, sanitation and hygiene (WASH). Only around 20% of the population had access to safely managed water, and only 10% had access to safely managed sanitation in 2023.

Service delivery is often inefficient and inequitable due to geographic barriers and insecurity, and is further constrained by shortages of equipment, medicines, skilled staff and basic infrastructure. Poor hygiene and malnutrition continue to worsen health outcomes, with rates of acute malnutrition continuing to exceed the WHO emergency thresholds.

An assessment by the IPC in 2025 shows that millions of people, including an estimated 2.1 million children under five and about 1.2 million pregnant and breastfeeding women, require treatment for acute malnutrition. An estimated 70% of acute malnutrition cases are concentrated in the five states of Jonglei, Northern Bahr el Ghazal, Upper Nile, Unity and Warrap.

Disease outbreaks, limited access to health services and poor WaSH conditions are compounding the already critical malnutrition situation. These persistent nutrition challenges act as long-term barriers to human capital formation and economic productivity. Chronic food insecurity and weak service delivery erode people’s physical and cognitive development, reducing their ability to engage productively in the economy.

These systemic pressures are compounded by recurring disease outbreaks (including cholera and other epidemic-prone illnesses), recurrent flooding and large-scale population displacement, leaving the health system in a near-continuous state of response and recovery. At the same time, gender-based violence, including intimate partner violence and conflict-related abuse, remains widespread across many communities, while access to even basic services for the clinical management of rape is minimal.

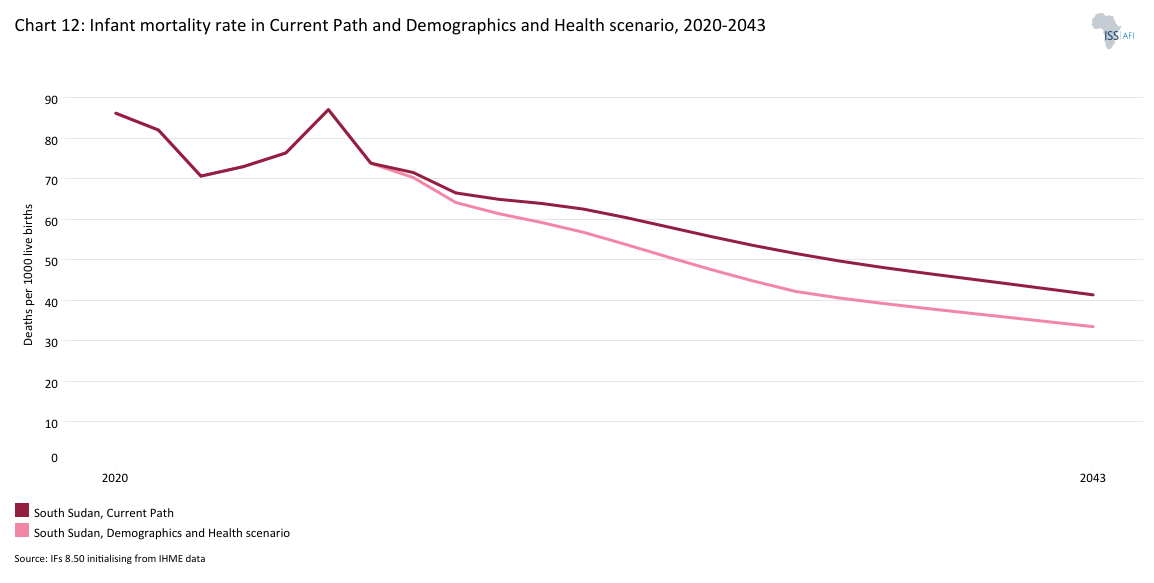

Chart 12 presents the infant mortality rate in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The infant mortality rate is the probability of a child born in a specific year dying before reaching the age of one. It measures the child-born survival rate and reflects the social, economic and environmental conditions in which children live, including their health care. It is calculated as the number of infant deaths per 1 000 live births and is an important marker of a country's overall health system quality.

Infant mortality remains one of the most serious public health challenges in South Sudan and is a strong indicator of the country’s broader health, social and economic conditions. The rate has declined significantly but remains very high by global standards, with 73 deaths per 1 000 live births in 2023, compared to an average of 43.4 for low-income countries in Africa in the same year. This wide gap underscores the persistent structural barriers to improving child survival in South Sudan. Despite some gradual improvements since 2018, progress has been slow and uneven, primarily due to persistent conflict, weak health systems, widespread poverty and recurring humanitarian crises.

A significant proportion of infant deaths in South Sudan occur during the neonatal period, the first 28 days of life. As of 2023, the country's neonatal mortality rate was estimated at 32.5 deaths per 1 000 live births, about 44% of the total infant mortality, and six percentage points above the average for low-income countries in Africa in the same year. This highlights the critical risks surrounding pregnancy, childbirth and immediate newborn care. Many women give birth at home without skilled health personnel, often due to long travel distances to health facilities, poor transport infrastructure, insecurity and the cost of services.

Beyond the newborn period, preventable infectious diseases are a leading cause of infant mortality. Malaria remains endemic and is a significant cause of death in infants, especially during the rainy season. Pneumonia and diarrhoeal diseases also account for a large share of deaths, often exacerbated by delayed care-seeking and limited access to effective treatment. These illnesses are closely linked to poor living conditions, including overcrowding, unsafe drinking water, inadequate sanitation and low immunisation coverage in some areas.

In the Demographics and Health scenario, the infant mortality rate will decline more rapidly after 2025. By 2030, the rate will fall to 59.2 per 1 000 live births, about 5 fewer than in the Current Path. By 2043, the scenario will achieve a rate of 33.5 per 1 000, representing a 19% reduction compared to the Current Path outcome. These health improvements align with SDG3 (Good Health & Well-being) targets, reducing child mortality and improving maternal health.

The scenario demonstrates that coordinated policy efforts targeting immunisation, improved reproductive health, maternal health and effective health system strengthening can substantially lower infant mortality. However, even with these improvements, South Sudan’s rate will remain above the average for low-income African countries, highlighting the scale of the challenge.

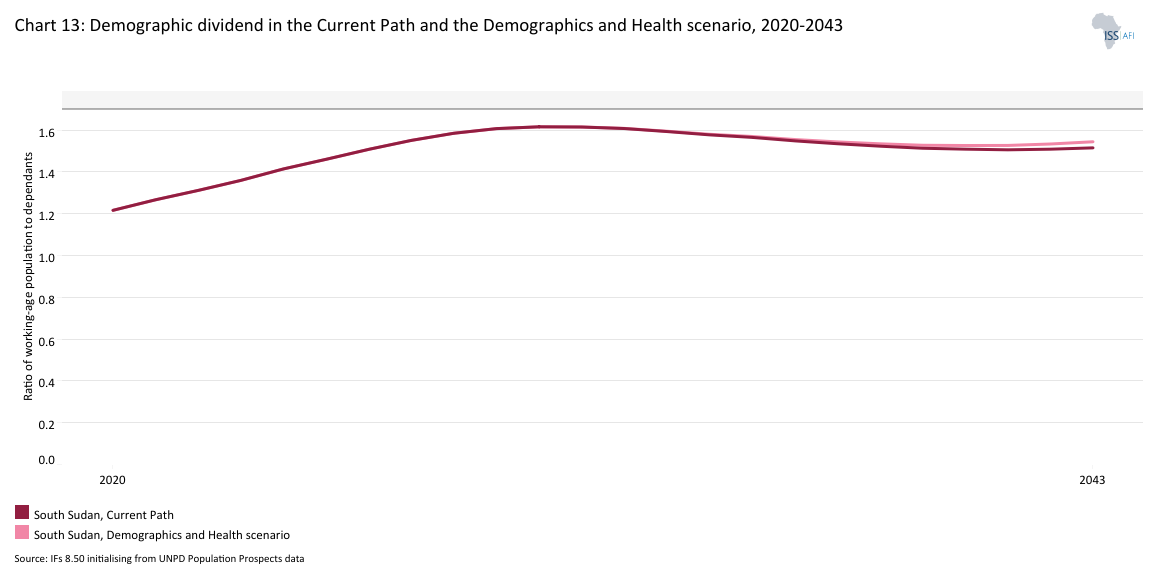

Chart 13 presents the demographic dividend in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The dividend is the window of economic growth opportunity that opens when the ratio of working-age persons to dependants rises to 1.7 to one and higher.

The demographic dividend, which refers to potential economic growth resulting from changes in a country's population structure, is influenced by factors such as declining fertility rates and improvements in health and education. With fewer dependants to support, families and governments can allocate more resources to savings, education, infrastructure and economic development, driving accelerated growth.

South Sudan’s demographic structure is much younger and has not entered its demographic window of opportunity. In 2023, the working-age-to-dependants ratio was about 1.4:1, meaning there was roughly 1.4 working-age persons for every dependant. On the Current Path, this ratio will increase to just about 1.52 by 2043. This implies that South Sudan will enter its first demographic window of opportunity after 2043 (by 2053, when the ratio will reach 1.7:1) if it follows the Current Path trajectory.

In the Demographics and Health scenario, which assumes improved access to modern contraception, reduced under-five and maternal mortality, and expanded access to safe water and sanitation, the demographic transition will accelerate slightly. In this scenario, the working-age-to-dependant ratio will increase to 1.54 in 2043, marginally above the Current Path.

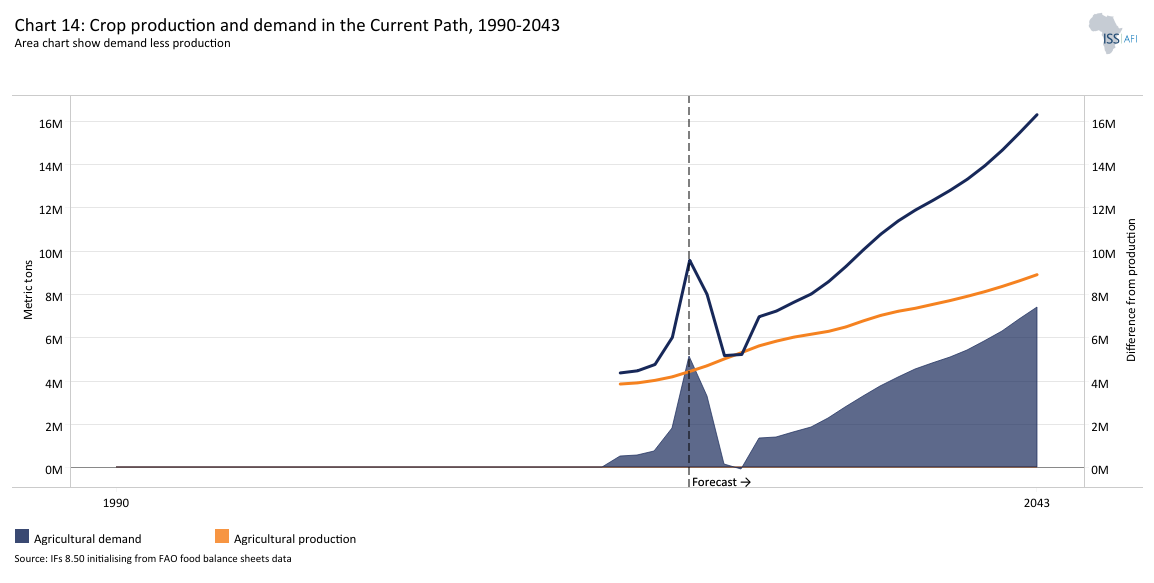

Chart 14 presents crop production and demand in the Current Path from 1990 to 2043.

The Agriculture scenario envisions an agricultural revolution that ensures food security through ambitious yet feasible increases in yields per hectare, driven by improved management, seed and fertiliser technologies, and expanded irrigation. Efforts to reduce food loss and waste are emphasised, with increased calorie consumption as an indicator of self-sufficiency and prioritising it over food exports. Additionally, enhanced forest protection demonstrates a commitment to sustainable land-use practices.

Visit the theme on Agriculture for our conceptualisation and details on the scenario structure and interventions.

Agriculture is a fundamental component of South Sudan’s economy, providing livelihoods for the majority of the population and accounting for a significant share of GDP and employment. Approximately 80% of rural households in South Sudan depend primarily on agriculture for their livelihoods. Nearly two-thirds of working women and one-third of working men are employed in the agriculture sector. Hence, gains in this sector directly impact incomes and poverty.

The sector is characterised by predominantly rain-fed, smallholder-based production, with crops such as sorghum, maize, millet and groundnuts forming the dietary staple. Despite its centrality, agriculture faces persistent structural constraints, including limited access to modern inputs, inadequate infrastructure, recurrent insecurity and vulnerability to climate shocks such as drought, flooding and land degradation. High transport costs, insufficient storage infrastructure and limited market access contribute to high post-harvest losses and volatile returns, deepening rural vulnerability and food insecurity.

These challenges have constrained productivity growth and limited the sector’s capacity to meet the food needs of a rapidly growing population. Furthermore, the ongoing influx of refugees and returning citizens from Sudan is further straining the already fragile sector. As a result, food insecurity and malnutrition in South Sudan remain very high.

The country has an extensive agricultural resource base; approximately 50% of its arable land is prime agricultural land, nearly five times the agricultural land per capita of Kenya, Uganda, or Ethiopia. Yet only 4.3% is currently being cultivated. Chart 14 shows that the gap between crop production and demand in South Sudan has widened steadily over the past three decades and will continue expanding through 2043. In 2023, crop production stood at 4.4 million metric tons, while domestic demand reached 9.6 million metric tons, resulting in a deficit of 5.2 million metric tons. This absolute gap has grown substantially since 2019, when production and demand were more closely aligned. The 2023 shortfall reflects both population growth and the slow pace of productivity gains in the sector, reinforcing South Sudan’s reliance on food imports and humanitarian assistance to meet consumption needs.

The baseline projection from 2023 onwards indicates that this structural imbalance will persist and deepen, with demand expected to reach 16.3 million metric tons by 2043, while production is projected at 8.9 million metric tons. The implied shortfall of 7.4 million metric tons by 2043 highlights the scale of the challenge facing the country’s food and nutrition security.

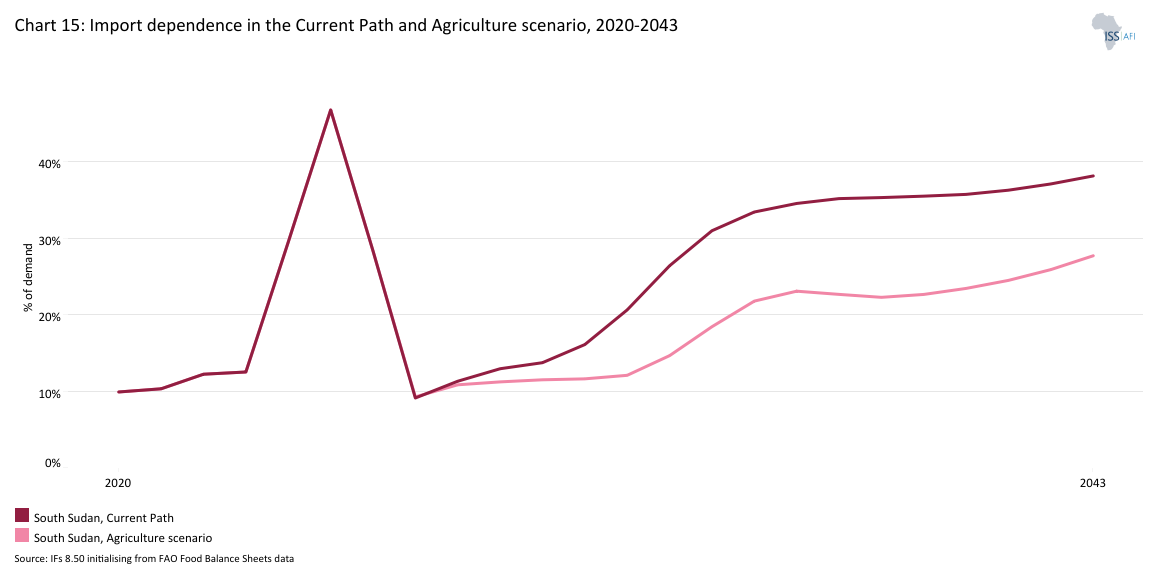

Chart 15 presents the import dependence in the Current Path and the Agriculture scenario, from 2020 to 2043.

South Sudan has abundant prime arable land, approximately 31.9 million hectares, but only 4.3% (about 2.8 million hectares) is currently cultivated. An estimated 38 100 hectares are equipped for irrigation, but only 18 480 hectares are actually irrigated, meaning only 48.5% of the equipped area is utilised, with the majority using surface water. This indicates the country’s underutilised agricultural potential, while it depends on imports to meet domestic food demand.

Before independence and in the years that followed, South Sudan’s cereal import bill, particularly for maize, sorghum and wheat, increased sharply as domestic output stagnated relative to demand. For example, between 2008/09 and 2014/15, the cereal trade balance dropped from a surplus of 49 000 tons to a deficit of 249 000 tons. The country imports large volumes of its cereals from neighbouring countries such as Uganda, Kenya and Sudan. This trend reflects a structural deficit in local cereal supply but also strong regional integration through cross-border trade.

In 2023, South Sudan’s import dependence for crops—measured as net imports as a share of total crop demand—stood at 14.1%, reflecting a significant reliance on external markets for food security. In the Current Path, import dependence will rise steadily over the forecast period, reaching 44.7% by 2043.

South Sudan’s long-term agricultural planning, as set out in the Comprehensive Agriculture Master Plan (CAMP), highlights the pressing need to reduce the dependence on food imports by boosting domestic productivity, scaling climate-resilient farming systems and strengthening value chains. At the same time, the country’s regional commitments, particularly through the Intergovernmental Authority on Development’s (IGAD) drought resilience and sustainability framework, emphasise more innovative water management, increased investment in resilience and stronger cross-border market connections. The Agriculture scenario models a package of interventions, including expanded irrigation, improved crop yields, enhanced storage and better rural infrastructure, to boost domestic production and food system resilience. Chart 15 shows that these interventions increase crop production, thereby slowing the growth of import dependence compared to the Current Path.

By 2043, import dependence in the Agriculture scenario will reach 32.8%, which is 11.9 percentage points lower than the Current Path. This would be transformative in a country where 3 in 4 households are food insecure today. The outcome, therefore, demonstrates the impact of targeted agricultural reforms on improving food security and resilience to external shocks.

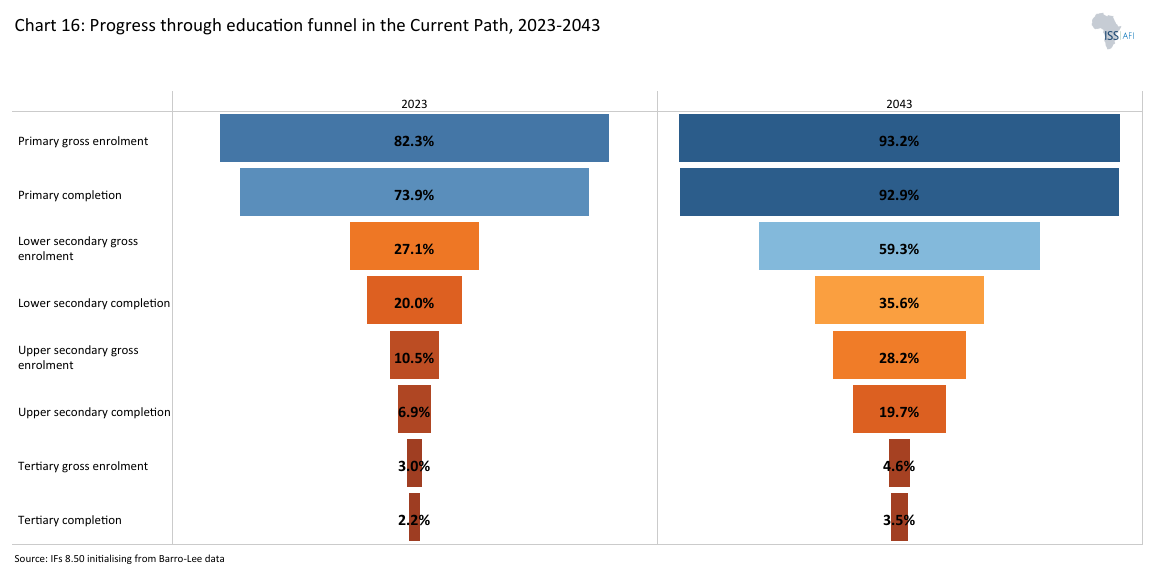

Chart 16 depicts the progress through the educational system in the Current Path, for 2023 and 2043.

The Education scenario represents reasonable but ambitious improvements in intake, transition, and graduation rates from primary to tertiary levels, as well as better-quality education at the primary and secondary levels. It also models substantive progress towards gender parity at all levels, additional vocational training at the secondary school level, and increases in the share of science and engineering graduates.

Visit the theme on Education for our conceptualisation and details on the scenario structure and interventions.

Education is a fundamental human right and a catalyst for broader development. Realising this right requires countries to guarantee universal and equal access to inclusive, equitable, high-quality education and lifelong learning, free of cost, and to ensure no one is left behind, regardless of gender, disability or socioeconomic status. As a public good, education places primary responsibility on the state, which serves as the duty-bearer and steward of the system.

South Sudan faces acute barriers to education access, with one of the world's highest shares of out-of-school children. Nearly three in five children have never attended school or have dropped out.

The country’s education system follows a formal pathway of eight years of primary education, four years of secondary education, and tertiary education, under a competency-based curriculum set out in the General Education Act (2012). The system comprises roughly 8 000 primary schools, 120 secondary schools and 12 universities. Yet, it is under severe strain: an estimated 4.75 million school-aged children, including 472 452 internally displaced children, must be served by limited infrastructure and capacity. As a result, the sector is marked by low participation beyond the early primary grades, weak learning conditions and a persistent mismatch between schooling outcomes and labour-market needs.

According to the 2023 Education Cluster Mid-Year Report, 3.4 million children aged 3-17 require education support, with over 42 000 teachers needed to meet the demand. Prolonged conflict and displacement—compounded by the recent COVID-19 pandemic—have intensified these pressures. In 2020, school closures alone kept an estimated 2.8 million learners at home, causing widespread disruption to learning.

Chart 16 shows that primary-level access remains the widest point in the education funnel. In 2023, gross enrolment at the primary level was 81.9%, and will improve to 93.3% by 2043. This expansion reflects a gradual return to near-universal access, though enrolment still trails the average for low-income African countries, where primary gross enrolment reached 107% in 2023. Primary completion rates in South Sudan have improved notably, rising to 73.9% in 2023 and projected to reach 92.9% by 2043. The narrowing gap between enrolment and completion at this stage signals significant progress in reducing primary-level dropout.

The transition to lower-secondary education remains a persistent challenge. Lower-secondary gross enrolment was 27.1% in 2023, less than half the rate of primary completion. This will rise to 59.3% by 2043. South Sudan’s projected lower-secondary enrolment will still fall below the average of 71.7% for low-income African countries. The completion rate remained low at 20% in 2023 and will reach 36% by 2043. The widening gap between lower-secondary enrolment and completion highlights ongoing barriers to progression, including limited school capacity, economic hardship and frequent disruptions to learning caused by insecurity.

Progression to upper secondary is even more constrained. In 2023, upper-secondary gross enrolment stood at 10.6%, with completion at 6.9%. By 2043, these figures will rise to 28.3% and 19.7%, respectively. These rates are well below income peers group averages, where upper-secondary enrolment was 45.5% in 2023, and completion will reach 31.6% in 2043. The steep attrition between lower and upper secondary, as well as between enrolment and completion within upper secondary itself, reflects structural constraints such as inadequate school infrastructure, insufficient numbers of qualified teachers and the high indirect costs of schooling for families.

Low completion and transition rates at lower- and upper-secondary levels sharply limit the number of South Sudanese students eligible for tertiary education, leading to weaker educational outcomes and, ultimately, reduced human capital accumulation. Tertiary gross enrolment was just 3% in 2023 and will increase to 4.6% by 2043. Completion rates at this level are the lowest in the education system, rising from 2.2% to 3.5% over the same period. For comparison, low-income Africa averages for tertiary enrolment and completion will reach 15.8% and 10.1%, respectively, by 2043. The limited access to higher education reflects not only supply constraints but also weak transition rates from upper secondary and intense competition for the few available places.

Education expenditure in South Sudan is among the lowest in sub-Saharan Africa. In 2023, education spending was estimated at US$162.4 million, representing approximately 2.3% of GDP—slightly below the income-peers average of 2.9%. This limited allocation constrains investments in school construction, teacher training and learning materials, and impedes efforts to expand access and improve quality at all levels of the system.

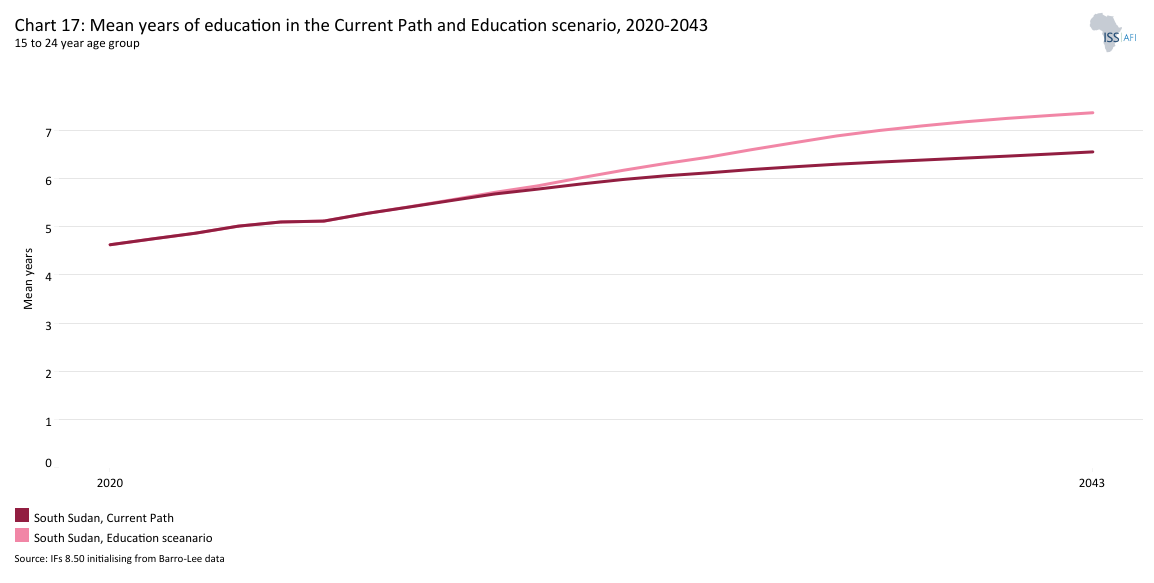

Chart 17 presents the mean years of education in the Current Path and in the Education scenario, from 2020 to 2043, for the 15 to 24-year age group.

The average years of education among the adult population aged 15 to 24 years is a valuable indicator of how the stock of knowledge in society is changing. In South Sudan, the mean for this cohort remains very low compared to the income peers group average: it stood at 5 years in 2023, about one year below the average for low-income African countries.

With low educational attainment among youths, adult literacy of approximately 35% and secondary net attendance of around 10-15%, South Sudan’s education challenges are substantial. The Education scenario, aligned with SDG4 (Quality Education), envisions a considerable push to increase enrollment and completion at all levels. In the Education scenario, average years of schooling will rise to 7.4 years by 2043, compared to 6.6 on the Current Path, laying the foundation for sustained economic growth beyond 2043 through a more skilled workforce.

This scenario also includes an ambitious push to close persistent gender gaps in attainment. In 2023, young men averaged 1.3 more years of education than young women.

Under South Sudan’s Revitalised Transitional Government of National Unity (RTGoNU), established in February 2020, renewed focus on education has been accompanied by periodic leadership changes in the Ministry of General Education and Instruction and repeated commitments to reform. Priorities have increasingly centred on making schools safer and more functional, and on addressing longstanding gaps in infrastructure, teaching quality and learning materials. Strengthening system management to ensure improvements are sustained over time.

In the Education scenario, education expenditures will account for 3.1% of GDP in 2043, compared to 2.4% on the Current Path. In this context, the increase in mean years of education reflects the government's renewed focus on educational reform, bringing South Sudan closer to the average of its income peers.

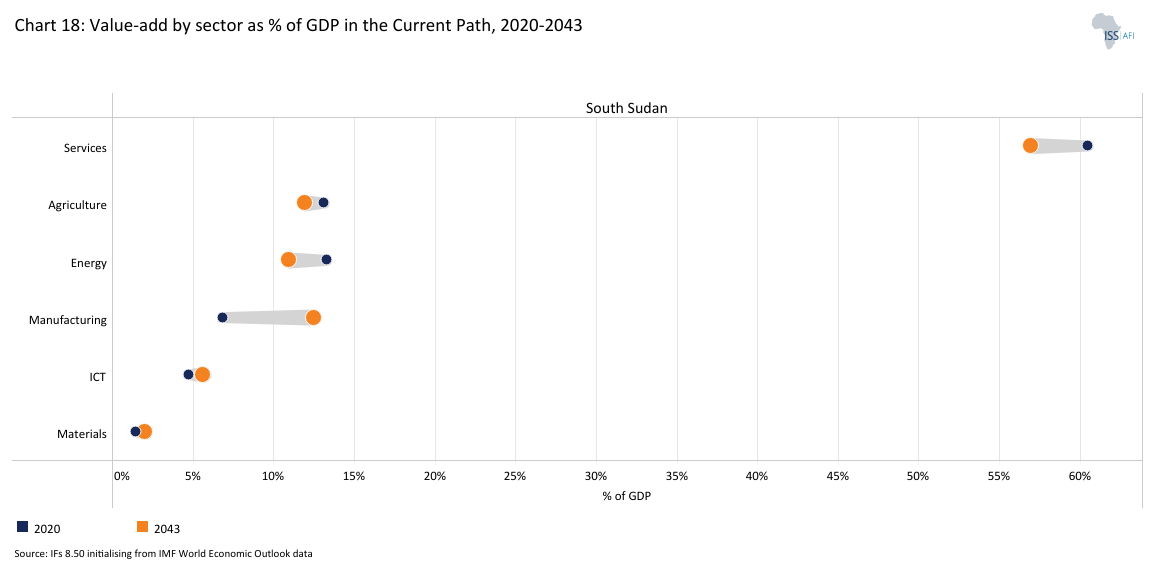

Chart 18 presents the value-added by sector as a share of GDP in the Current Path, for 2023 and 2043.

In the Manufacturing scenario, reasonable but ambitious growth in manufacturing is envisaged through increased investment in the sector, research and development (R&D) and improved government regulation of businesses.

Visit the theme on Manufacturing for our conceptualisation and details on the scenario structure and interventions.

South Sudan’s manufacturing sector is small, underdeveloped and strongly constrained by factors such as the long-running civil war, an infrastructure deficit, limited capital and a skills shortage. The industry is dominated by micro, small and informal firms engaged in light production, such as basic agro-processing, beverages, workshops, and the development of construction materials. Industrial value chains are minimal, with production channelled mainly toward local markets rather than exports.

A defining feature of South Sudan’s manufacturing landscape is its high dependence on imports. Most manufactured and processed goods consumed domestically, including pharmaceuticals, machinery and consumer goods, are imported, reflecting limited domestic industrial capacity.

As a result, South Sudan’s manufacturing sector contributes only a modest share to overall economic output. In 2023, the manufacturing sector contributed just 6.9% of GDP, compared to the average of 9.6% for its income peers group. South Sudan’s manufacturing sector ranked 40th in Africa in 2023. On the Current Path, the sector’s contribution will increase to around 12.5% of GDP by 2043, slightly below the forecast average of 16.1% for low-income African countries in the same year.

While opportunities exist, especially in agro-processing and the development of construction materials, manufacturing is unlikely to expand significantly without sustained improvements in energy, infrastructure, stability, and investment.

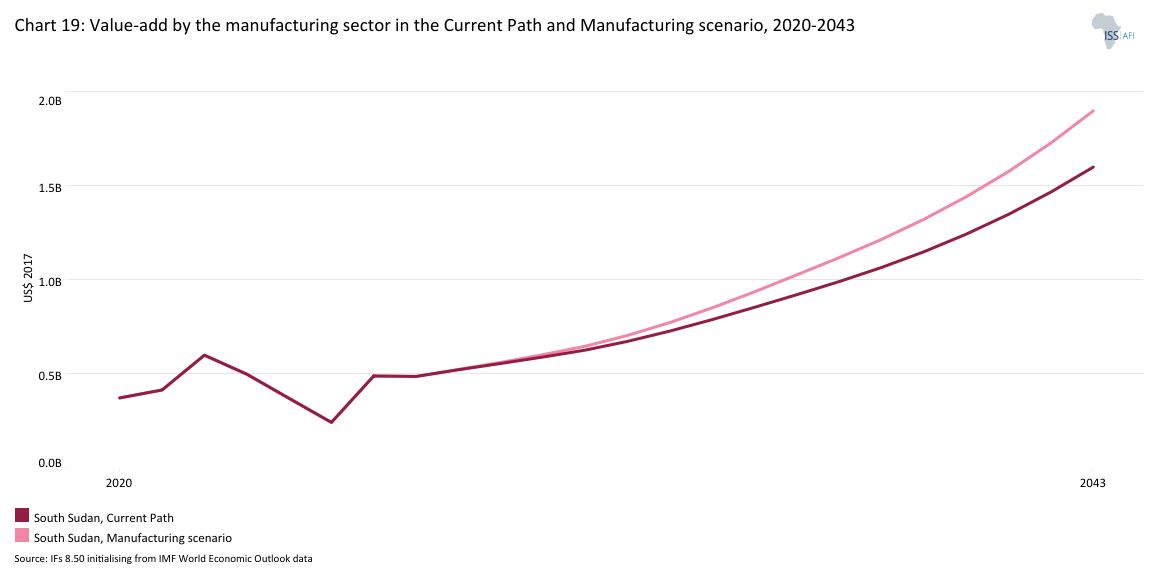

Chart 19 presents the contribution of the manufacturing sector to GDP in the Current Path and in the Manufacturing scenario, from 2020 to 2043. The data is in US$ and % of GDP.

In 2043, the manufacturing sector value-added in the Manufacturing scenario will reach 13.5% of GDP (equivalent to nearly US$1.9 billion), which is 1.0 percentage point higher than the Current Path projection of 12.5%. Despite these gains, the manufacturing share of GDP in both scenarios remains below the regional average for low-income Africa, which is projected at 16.1% by 2043. This suggests that, while targeted interventions can accelerate industrial growth, South Sudan will need sustained policy focus to address structural hurdles, including infrastructure, energy and skilled labour shortages.

With oil and subsistence farming currently dominating the economy, manufacturing expansion is crucial to diversify exports and generate jobs for urban youth. The Manufacturing scenario complements the AfCFTA implementation by enabling South Sudan to produce goods for regional markets, moving beyond raw commodity exports.

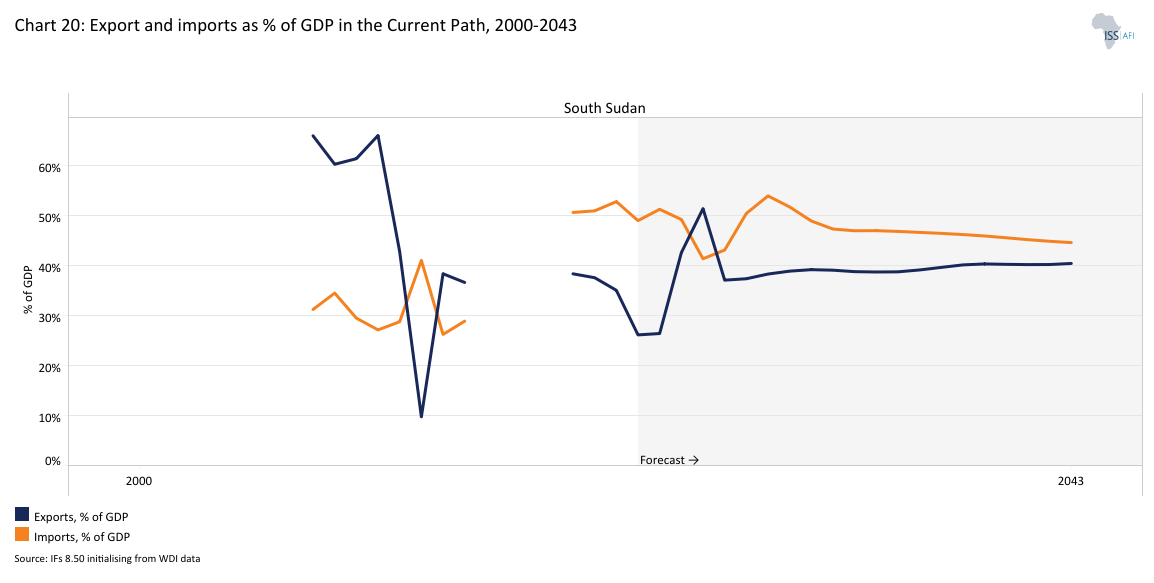

Chart 20 depicts exports and imports as a percentage of GDP, from 2000 to 2043, in the Current Path.

The AfCFTA scenario represents the impact of fully implementing the African Continental Free Trade Agreement by 2034. The scenario increases exports across manufacturing, agriculture, services, ICT, materials and energy. It also includes improved multifactor productivity growth from trade and reduced tariffs for all sectors.

Visit the theme on AfCFTA for our conceptualisation and details on the scenario structure and interventions.

South Sudan’s economy is characterised by a high degree of trade openness (measured as a share of total trade to GDP) and significant volatility in trade flows, concentrated in primary exports. The volatility is mainly due to its over-reliance on oil exports for foreign exchange while importing a wide range of manufactured commodities.

At the regional level, South Sudan is a member of several regional integration blocs, including the East African Community (EAC), which it joined in October 2016, the Common Market for Eastern and Southern Africa (COMESA) and the Intergovernmental Authority on Development (IGAD). However, it has not yet ratified the Tripartite Free Trade Area (TFTA) Agreement, launched in 2015 by the EAC, COMESA and the Southern African Development Community (SADC) to merge the three blocs into a larger free trade area.

South Sudan is also a signatory to the African Continental Free Trade Area (AfCFTA), although ratification is still pending. Ratifying the AfCFTA would broaden access to larger and more diversified markets, supporting South Sudan’s diversification agenda and strengthening resilience to terms-of-trade volatility and global supply chain shocks.

In the multilateral system, South Sudan currently holds observer status at the World Trade Organisation (WTO), having formally applied for membership on 5 December 2017. A WTO Working Party, responsible for overseeing and advancing the accession process, was subsequently established on 13 December 2017.

In 2023, South Sudan’s total trade (defined as the sum of exports and imports) amounted to 75.2% of GDP, substantially higher than the 46.9% average for its income-peer group. On the Current Path, total trade will rise further to 85.1% of GDP by 2043, remaining well above the estimated average for Africa’s low-income countries (69.4%). This high trade-to-GDP ratio largely reflects South Sudan’s oil-dependent export base and its heavy reliance on imports of goods and services, reinforced by the small scale of domestic manufacturing and limited import substitution.

At a disaggregated level, South Sudan’s exports accounted for 26.2% of GDP (equivalent to nearly US$1.9 billion) in 2023, underscoring its firm reliance on external trade. The country's export composition is highly concentrated on mineral fuels (crude oil), accounting for over 85% of total exports. This dependence reflects the underdeveloped state of domestic value chains and leaves the economy exposed to external shocks, complicating efforts to achieve more stable, sustainable growth.

South Sudan must develop an industrial strategy that strengthens domestic production while expanding non-oil export opportunities, so that diversification goes hand in hand with meeting basic needs such as food, affordable energy and essential services. As a resource-dependent economy, South Sudan faces a high risk of over-reliance on a narrow set of primary exports, leaving growth and public revenues exposed to external shocks. Expanding productive capacity and diversifying the export base are therefore central to building a more resilient economy, especially at South Sudan’s early stage of development, where structural transformation and value addition can generate jobs, raise incomes and reduce vulnerability over time.

A country’s export basket concentration can be assessed by looking at the combined share of a country’s top five export products. A higher combined share indicates a more concentrated export profile, whereas a lower share signals a more diversified export base. In 2023, South Sudan’s top five exports–crude petroleum (82.2%), refined petroleum (4.4%), forage crops (4%), gold (3.9%) and scrap iron (2.1%)–together represented 96.6% of total export earnings. The primary destinations for South Sudan’s exports were China, Singapore, the United Arab Emirates, Germany and Uganda.

South Sudan’s imports accounted for 49% of GDP (equivalent to US$3.5 billion) in 2023, almost double its export share. The top five imported products were cement (39%), knit men’s suits (34.9%), other edible preparations (32.3%), knit T-shirts (28.5%) and raw iron bars (28.1%). These imports mostly originated from Uganda, the United Arab Emirates, Kenya, China and the United States, respectively.

On the Current Path, South Sudan's total trade (imports plus exports) as a percentage of GDP will increase to 85.1% in 2043. The exports share will increase significantly to 40.9% of GDP, while the import share will decline marginally to 44.6% by 2043.

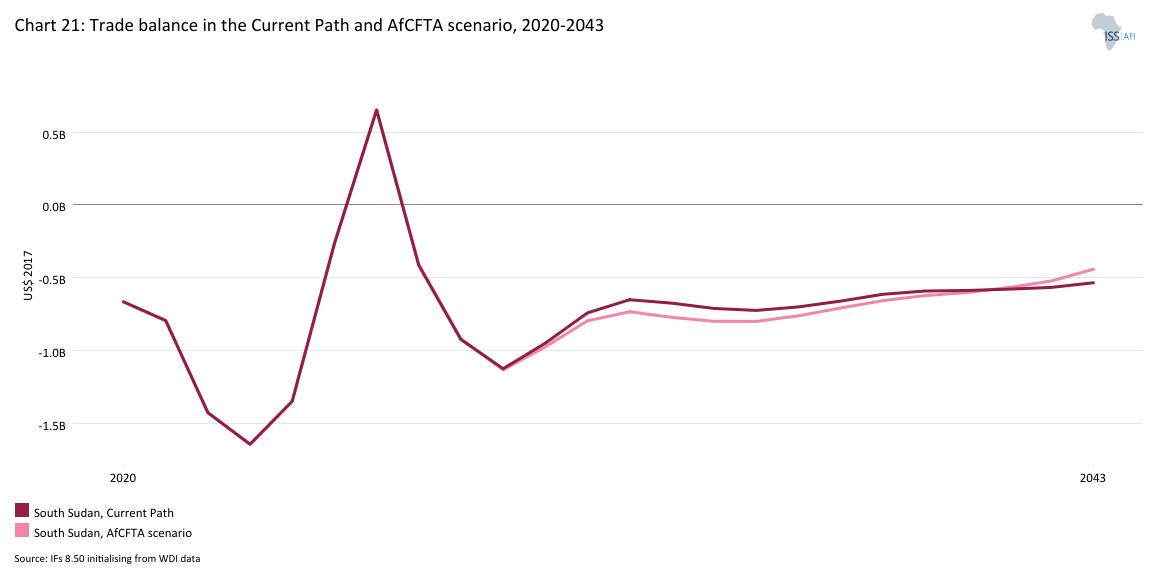

Chart 21 presents the trade balance in the Current Path and in the AfCFTA scenario, from 2020 to 2043 as a percentage of GDP.

South Sudan’s trade balance, expressed as a percentage of GDP, reflected persistent deficits throughout the 2020s, underscoring the country’s structural reliance on imports and exposure to external shocks. In 2023, the trade deficit stood at 22.9% of GDP, highlighting considerable external imbalances amid fragile domestic conditions. On the Current Path, the deficit will remain elevated through the remaining 2020s before gradually narrowing over the long term, reaching nearly 4.2% of GDP in 2043. This trajectory signals a gradual but incomplete adjustment in the country’s external position.

The AfCFTA scenario will reduce South Sudan’s trade deficit to around 3% of GDP in 2043, representing a 1.1 percentage point reduction relative to the Current Path. Total trade will also edge down slightly to 84.9% of GDP, driven by a modest decline in import dependence, as imports fall to about 44% of GDP, compared with 44.6% on the Current Path in the same year.

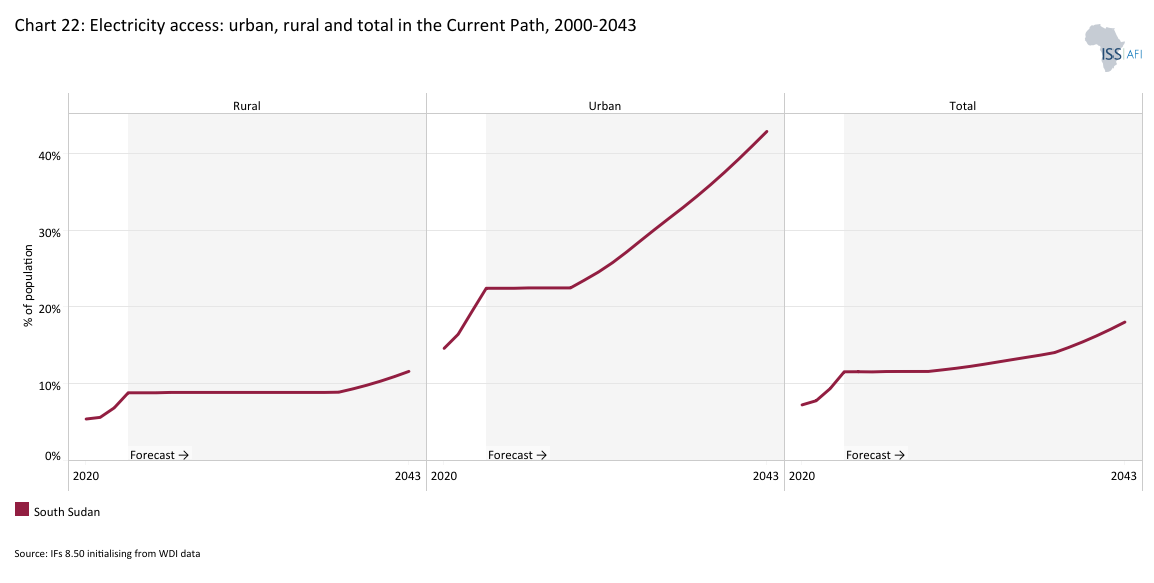

Chart 22 presents the Current Path of access to electricity for urban, rural and the total population from 2000 to 2043.

The Large Infrastructure and Leapfrogging scenario involves ambitious investments in road and renewable energy infrastructure, improved electricity access and accelerated broadband connectivity. It emphasises adopting modern technologies to enhance government efficiency. It incorporates significant investments in major infrastructure projects, such as rail, ports and airports (other infrastructure), while highlighting the positive impacts of renewables and ICT.

Visit the themes on Large Infrastructure and Leapfrogging for our conceptualisation and details on the scenario structure and interventions.

South Sudan's infrastructure faces a massive deficit. Decades of conflict and insecurity have damaged physical assets, disrupted construction and maintenance, displaced communities, and reduced the state’s ability to plan and deliver public investment. These pressures are compounded by weak governance and recurrent climate shocks, especially flooding, which repeatedly destroy roads, bridges and public facilities, thereby increasing the cost of rebuilding. The result is an infrastructure system that is not only limited in coverage but also fragile, expensive to operate and highly vulnerable to seasonal and security-related disruptions.

More than 98% of South Sudan’s road infrastructure remains unpaved and poorly maintained, resulting in highly seasonal road access. During the rainy season, large sections become impassable, cutting off rural communities from markets, health services and education, and sharply increasing the cost of moving goods and people.

Electricity access is one of the most binding constraints in South Sudan, with only 8.4% of the population having access to electricity in 2022, compared to the average of about 38.2% for low-income African countries. The country is among the least electrified in the world, with a total installed capacity of 30MW and no interconnected transmission grid.

Urban access to electricity is significantly higher than rural access, at an estimated 15% in 2022. However, this was still far below the 71.6% average for Africa’s low-income countries in the same year. Rural access remains extremely low at 1.7%, compared with the peer-group average of 21.5%. This stark disparity underscores the country’s predominantly rural demographic and the limited reach of electrification efforts outside major towns.

Urban areas have experienced notable gains in electricity access since independence (10.8%), mainly due to focused reconstruction efforts and donor-supported projects in major cities. However, rural electrification has lagged, constrained by high distribution costs, security risks and a lack of public and private investment. By 2043, urban access will rise to 42.9%, while rural access will reach only 11.6%. As a result, the urban-rural access gap will widen from 13.3 percentage points in 2023 to 31.3 percentage points in 2043. Total electricity access will reach 29.2% by 2043, well below the forecast average of 59.5% for low-income African countries in the same year.

Low electrification further restricts digital (ICT) usage, especially in rural areas where charging devices, powering mobile towers, and operating businesses consistently is difficult. As a result, digital technologies have not yet been able to scale to substantially offset the country’s physical infrastructure gaps.

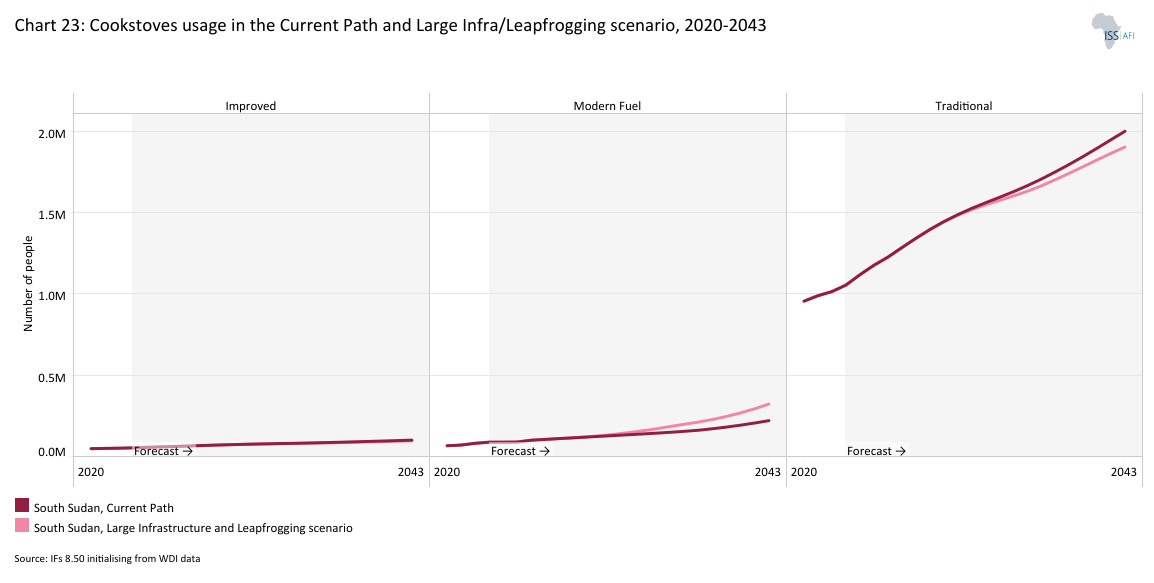

Chart 23 presents the number of people using cookstoves in the Current Path and in the Large Infrastructure and Leapfrogging scenario, from 2020 to 2043.