Somalia

Somalia

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This page explores Somalia’s long-term trajectory across key social, economic and governance dimensions. The assessment discusses current trends in population growth, economic performance, poverty and human wellbeing. The analysis also highlights how policy choices across sectors could shape Somalia’s future pathway.

For more information about the International Futures modelling platform we use to develop the various scenarios, please see the Technical page.

Executive Summary

We begin this page with an introductory assessment of the country’s context, focusing on current population distribution, social structure, climate and topography.

- Somalia is located in the Horn of Africa along the Gulf of Aden and the western Indian Ocean. With more than 3 000 km of coastline, the longest on mainland Africa, it occupies a strategically important position along major maritime trade routes. It borders Djibouti, Ethiopia and Kenya.

- The collapse of Siad Barre’s regime in 1991 led to the fragmentation of the central state and prolonged conflict. Since 2012, Somalia has operated as a federal republic under a Provisional Constitution, comprising the Federal Government and several federal member states. However, relations between federal and regional authorities remain contested, and the constitutional settlement is incomplete. Territorial fragmentation persists, most notably in Somaliland, which declared independence in 1991 and functions as a de facto state but lacks international recognition.

- Security remains the most immediate constraint on state consolidation. The federal government does not exercise full territorial control, and al-Shabaab continues to operate in parts of the countryside. International and regional support, therefore, remains central to the security sector, including African Union missions and bilateral training and assistance to Somali security forces.

- Somalia remains a low-income and institutionally fragile state. Poverty is widespread, the economy is largely informal, and public services remain limited and uneven. Although macroeconomic reforms enabled Somalia to reach the completion point of the Heavily Indebted Poor Countries Initiative in 2023 and secure significant debt relief, state capacity and revenue collection remain constrained.

- The population is predominantly Somali and organised around clan-based social structures that continue to shape politics and access to resources. Somali and Arabic are the official languages, and almost all Somalis follow Sunni Islam of the Shāfiʿī school. Pastoralism and agropastoralism remain central to livelihoods in the country’s largely arid environment.

- Somalia has recently sought deeper regional integration, joining the East African Community in 2023 and ratifying the African Continental Free Trade Area in 2025.

This section is followed by an analysis of the Current Path for Somalia, which informs the country’s likely current development trajectory to 2043. It is based on current geopolitical trends and assumes that no major shocks would occur in a ‘business-as-usual’ future.

- Despite decades of conflict and fragility, Somalia’s population more than doubled from 7.1 million in 1990 to 18.4 million in 2023 and is projected to reach 33.7 million by 2043. This is driven by persistently high fertility, which remains at 6.1 births per woman and is expected to remain well above replacement level. The population is overwhelmingly young, with nearly three-quarters under 30 and almost half under 15, a share that will decline only slightly by 2043. As a result, dependency ratios will remain structurally high, particularly in rural and nomadic areas, sustaining intense pressure on education, health systems and job creation, and reinforcing spatial inequality and development strain over the coming decades.

- Economic growth remains modest, uneven and structurally shallow, constrained by insecurity, weak institutions, dollarisation and heavy aid dependence that finances much of public spending. Although HIPC debt relief in 2023 reduced external debt, and GDP will rise from US$8.6 billion in 2023 to US$20.8 billion by 2043, the growth model remains externally supported and insufficiently diversified, limiting its ability to generate jobs, absorb demographic pressures or drive sustained structural transformation.

- Somalia’s GDP per capita, at US$1 466 in 2023, remains among the lowest in Africa and will reach only US$2 644 by 2043, still far below the average for its low-income peers. Persistent income gaps reflect rapid population growth, entrenched informality, weak human capital development and a narrow, low-productivity services base. Urbanisation, remittances and incremental stabilisation support modest gains, but without structural transformation and sustained job creation, significant improvements in living standards will remain challenging.

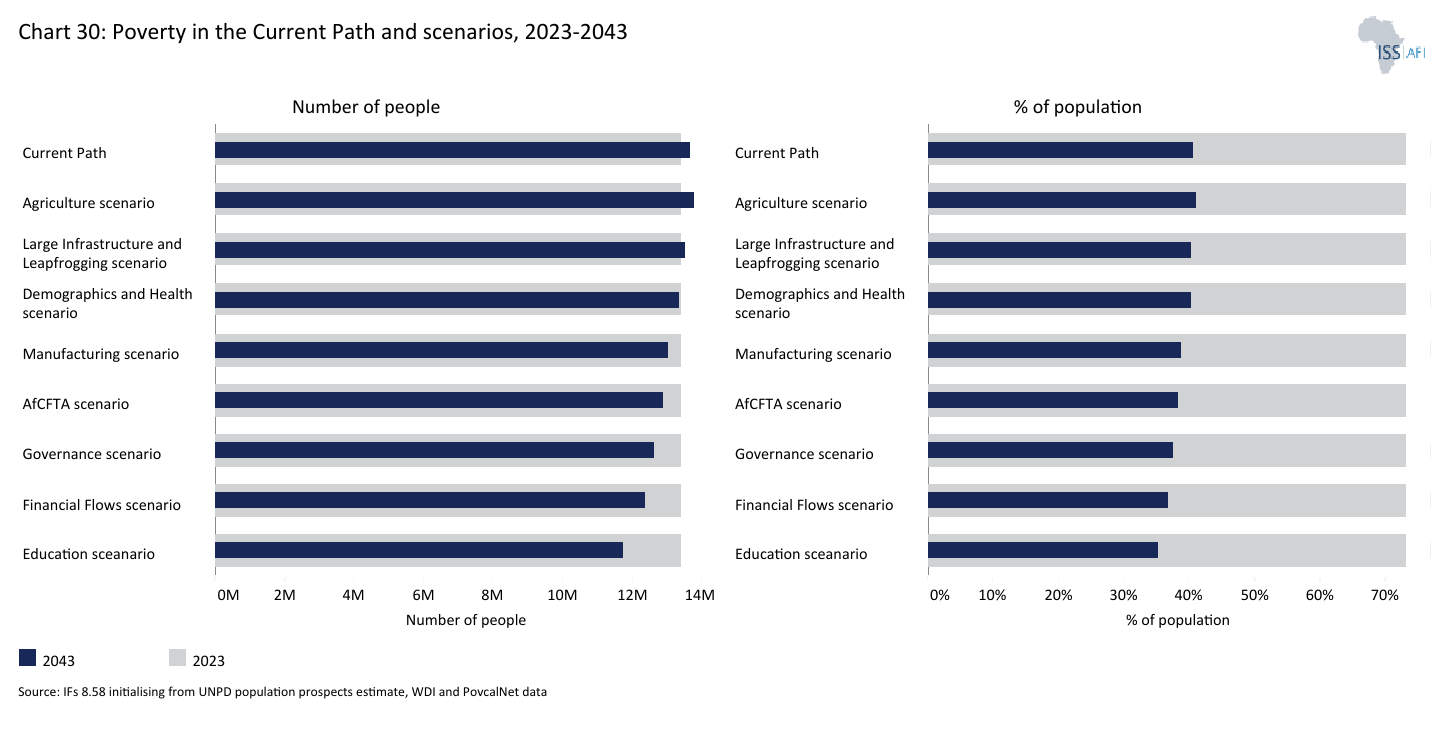

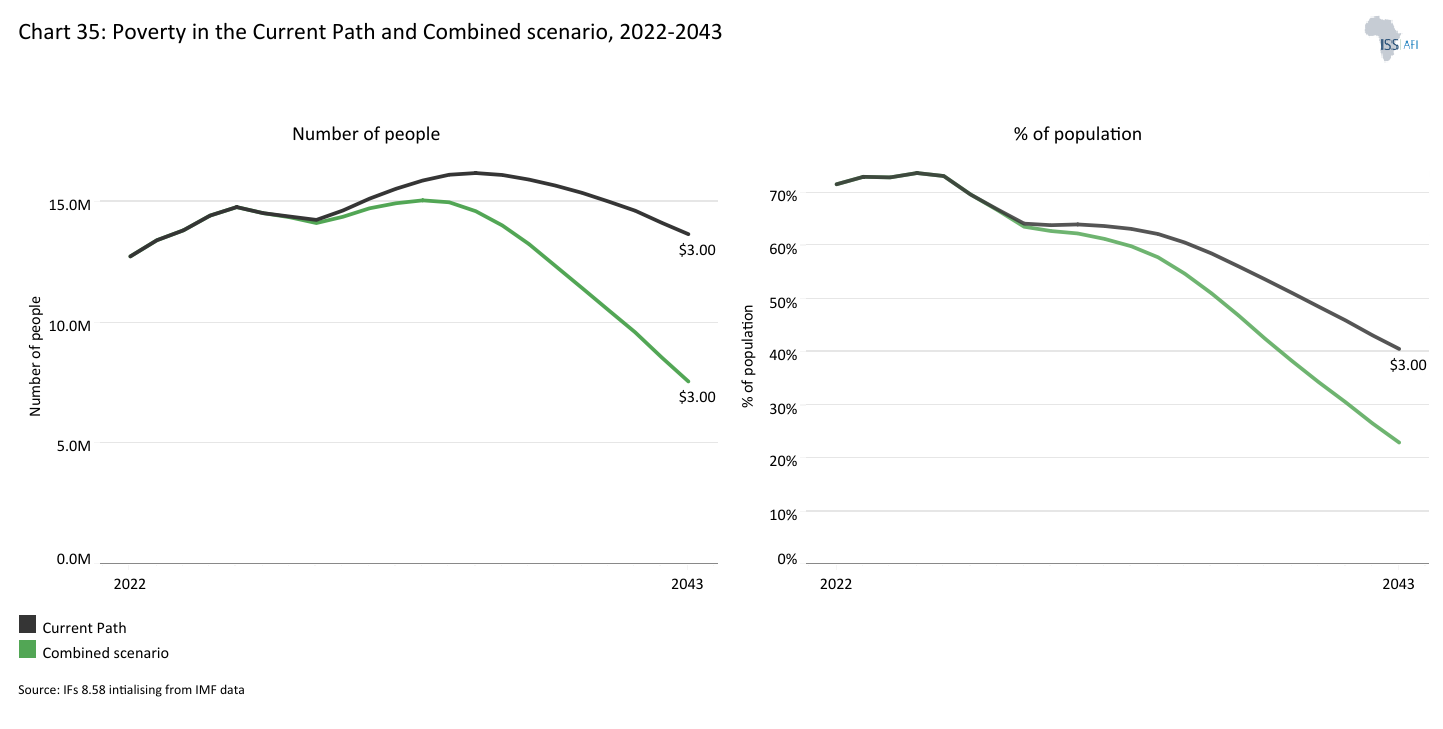

- Poverty in Somalia is widespread and structurally entrenched, with 54% of the population living below the national poverty line (US$2.06 per day) and little progress in recent years due to weak per capita growth and recurrent climatic shocks. Poverty is deepest among nomadic and rural communities and geographically concentrated in Central and Southern regions, although rapid urbanisation means most poor people now live in towns and cities. At the international poverty line for low-income countries at US$3.00 per day, 73% of the population (13.4 million people) were poor in 2023. On the Current Path, this rate will decline to 41% by 2043. However, the absolute number will increase to 13.7 million due to population growth. Multidimensional poverty is even more severe, affecting roughly two-thirds of the population and over 80% of nomadic groups, driven primarily by deficits in living standards and education.

- Since the mid-2010s, Somalia has rebuilt its national planning architecture, progressing from NDP 8 and NDP 9, which tied recovery to governance reform, macroeconomic stabilisation and debt relief, to the more ambitious National Transformation Plan 2025–2029 and the longer-term Centennial Vision 2060. The NTP serves as Somalia’s medium-term development framework, aimed at strengthening state institutions and governance while accelerating sustainable economic and social development. It prioritises building transparent and accountable governance systems, fostering macroeconomic stability and economic diversification, expanding critical infrastructure, investing in human capital and social services, and strengthening resilience to environmental and climate shocks, while mainstreaming gender equality and inclusion across development policies. This evolution reflects a gradual shift from a focus on stabilisation towards structural transformation, with greater emphasis on state capacity, federal coordination, human capital development and resilience. Implementation, however, remains constrained by limited administrative reach, uneven federal authority and persistent insecurity.

The next section compares progress on the Current Path with eight sectoral scenarios. These are Demographics and Health; Agriculture; Education; Manufacturing; the African Continental Free Trade Area (AfCFTA); Large Infrastructure and Leapfrogging; Financial Flows; and Governance. Each scenario is benchmarked to set an ambitious yet reasonable aspiration for that sector.

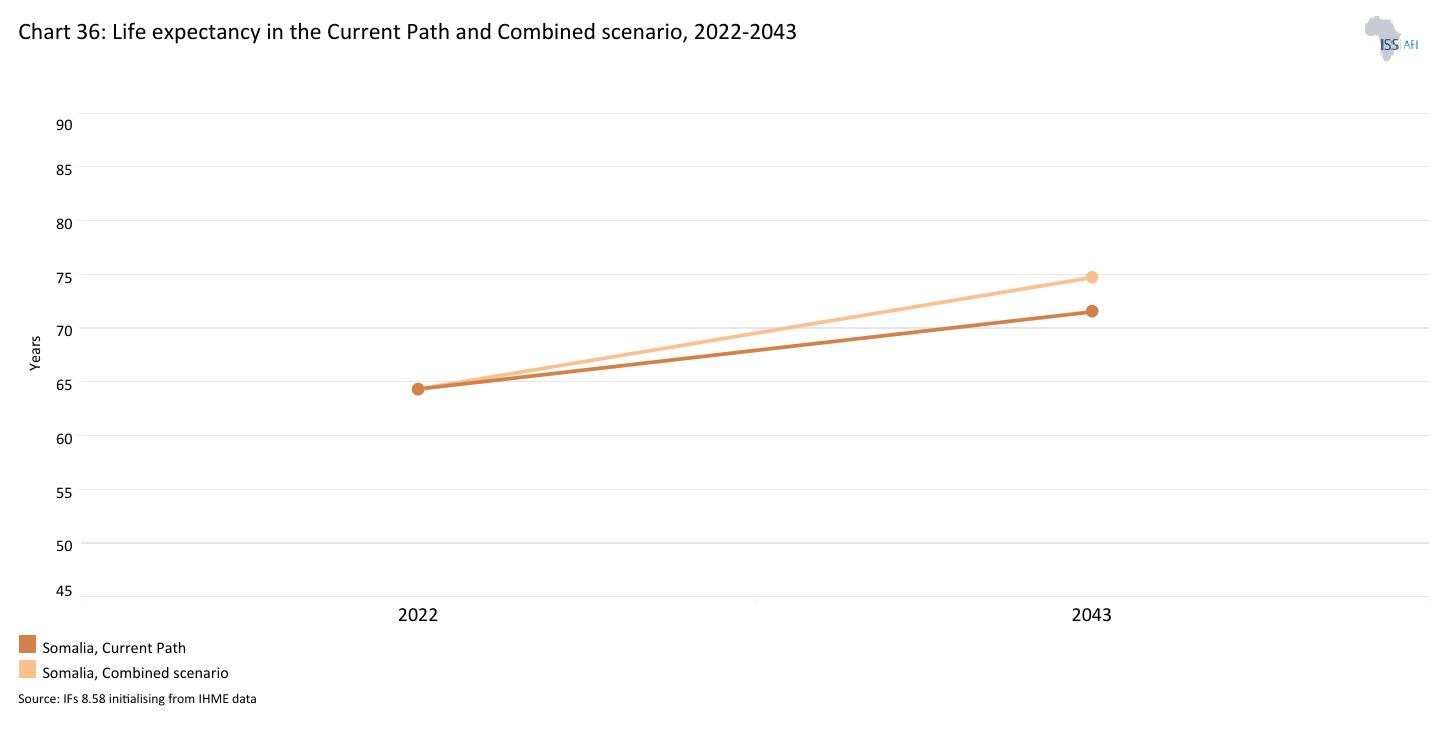

- In 2023, Somalia’s infant mortality rate stood at 62 deaths per 1 000 live births, more than double the Sustainable Development Goal target of fewer than 25 deaths per 1 000 live births by 2030. On the Current Path, the rate will decline to 31 deaths per 1 000 live births in 2043, indicating substantial improvement but still falling short of the global benchmark. Under the Demographics and Health scenario, however, infant mortality could fall further to 26 deaths per 1 000 live births, bringing the country close to achieving the SDG target. Life expectancy will improve from 65 years in 2023 to 74 years in 2043 (2 years more than the Current Path projection).

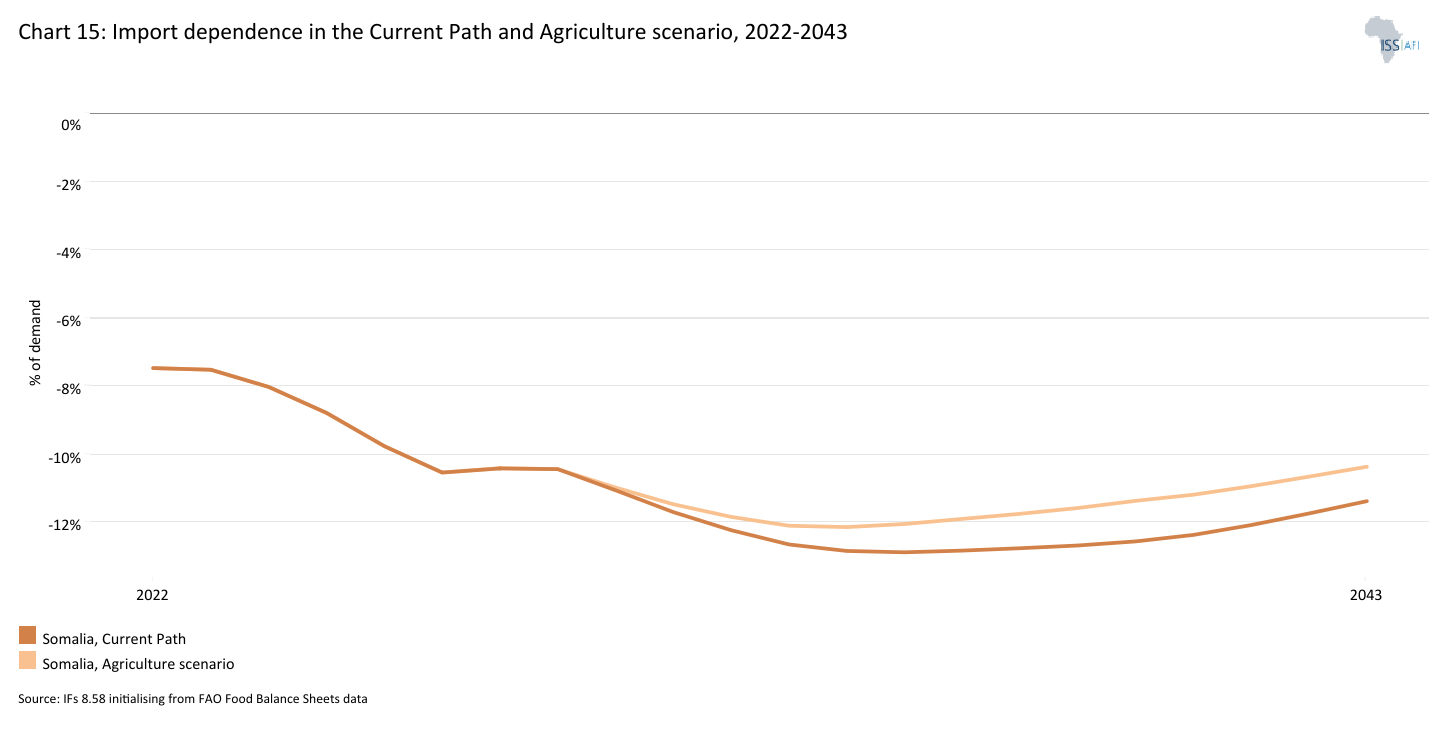

- In the Current Path, the agricultural trade deficit increases from almost 8% of demand in 2023 to 11.4% by 2043, reflecting rising food demand driven by rapid population growth and limited gains in domestic production. The Agriculture scenario will improve this outlook. Higher crop yields, expanded irrigation and reduced agricultural losses will slightly reduce reliance on imports. As a result, the agricultural trade deficit will decline to around 10.4% of demand by 2043. However, these gains are not sufficient to eliminate structural food import dependence. Continued population growth and climate vulnerability will continue to put pressure on domestic food systems. Without sustained productivity improvements and diversification beyond rain-fed agriculture, particularly through irrigation expansion, stronger livestock value chains and fisheries development, Somalia is likely to remain reliant on food imports over the next two decades.

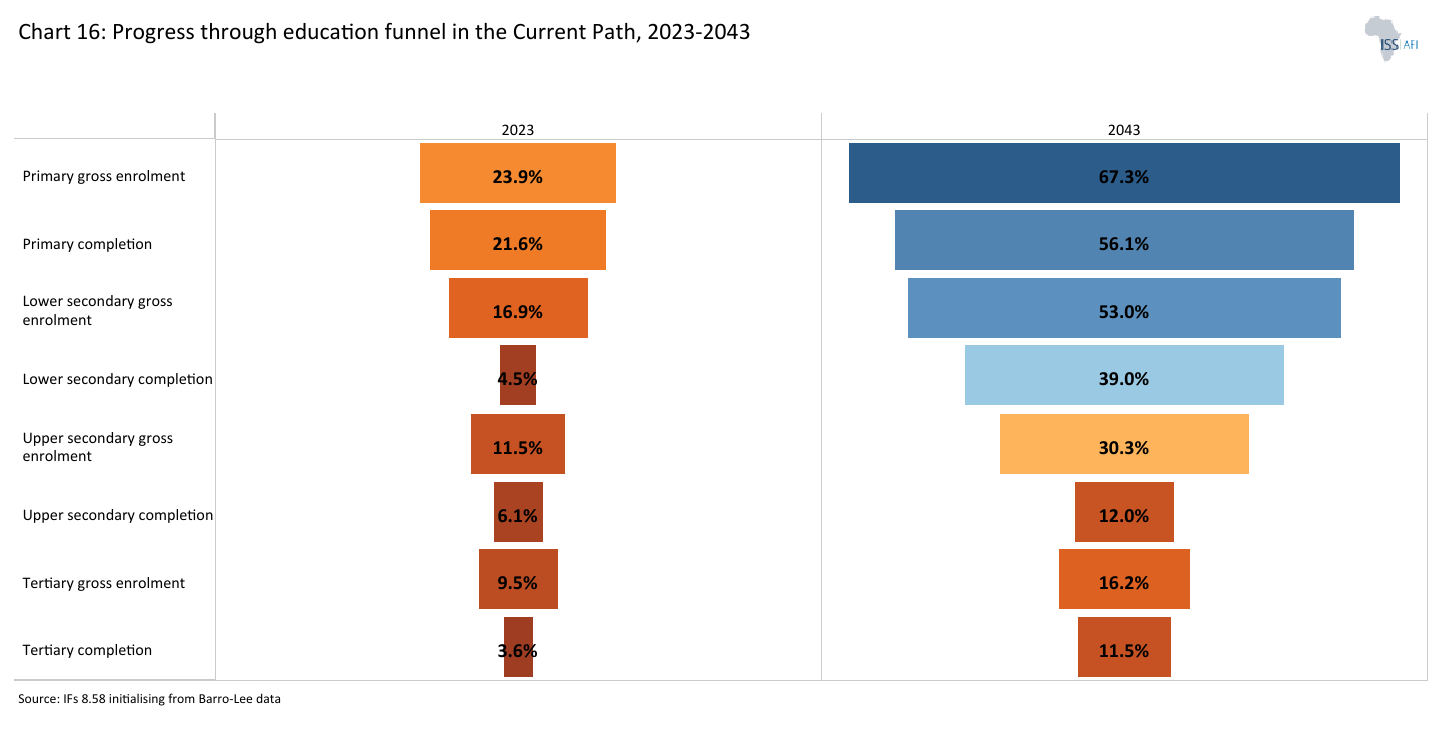

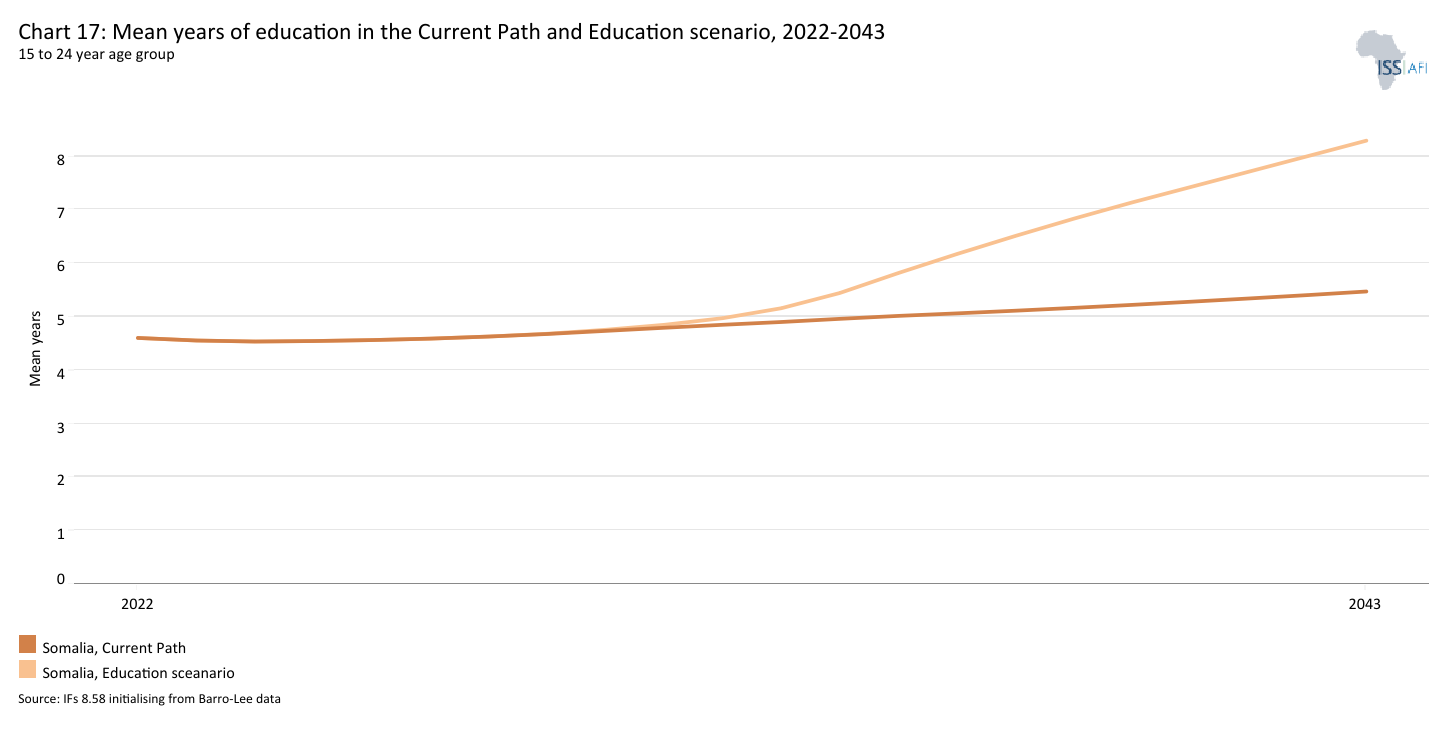

- Mean years of schooling for 15 to 24-year-olds increase only modestly on the Current Path, from 4.6 to 5.5 years by 2043, reflecting persistent bottlenecks across the pipeline. In the Education scenario, stronger intake, retention, vocational expansion, improved quality and gender parity will raise this to 8.3 years, signalling a more substantial shift in human capital accumulation. However, without parallel job creation and economic diversification, even accelerated education gains may struggle to translate into broad-based transformation.

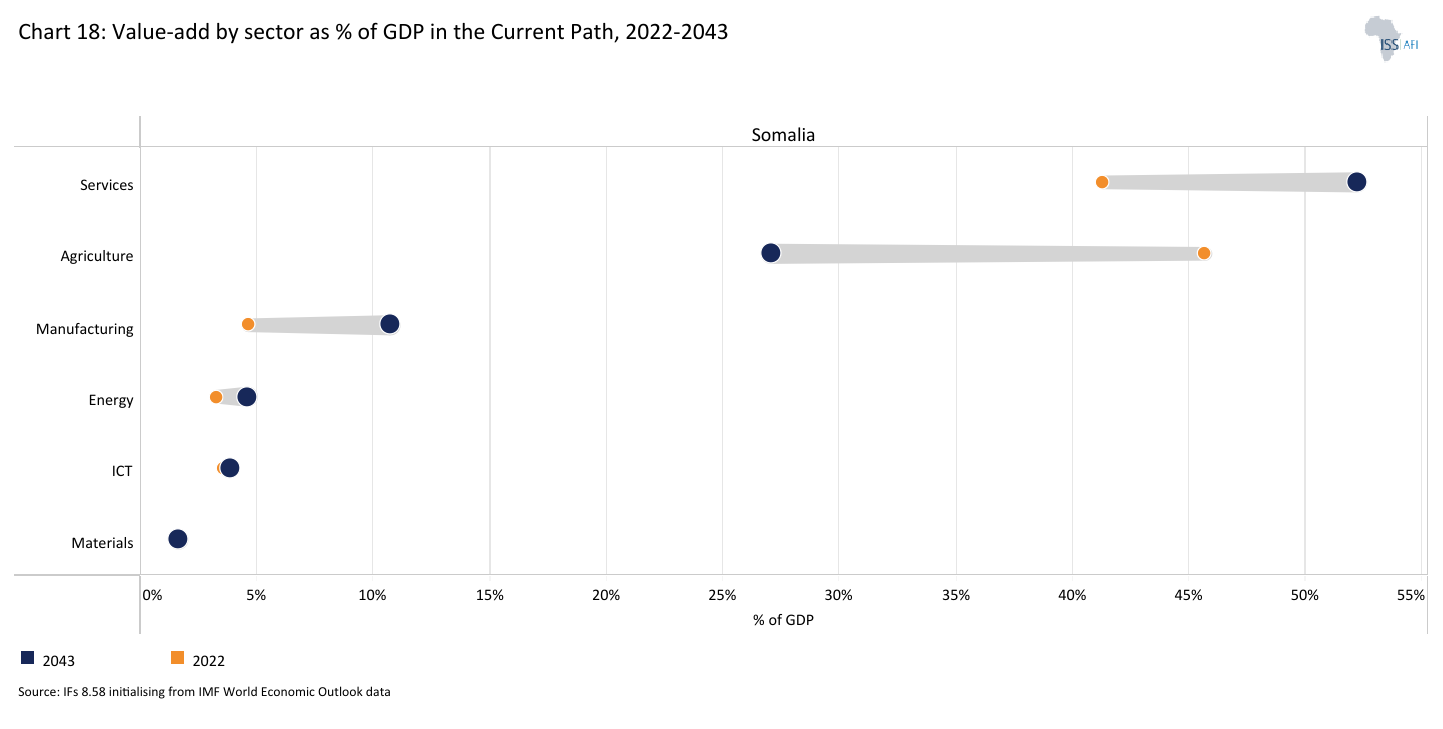

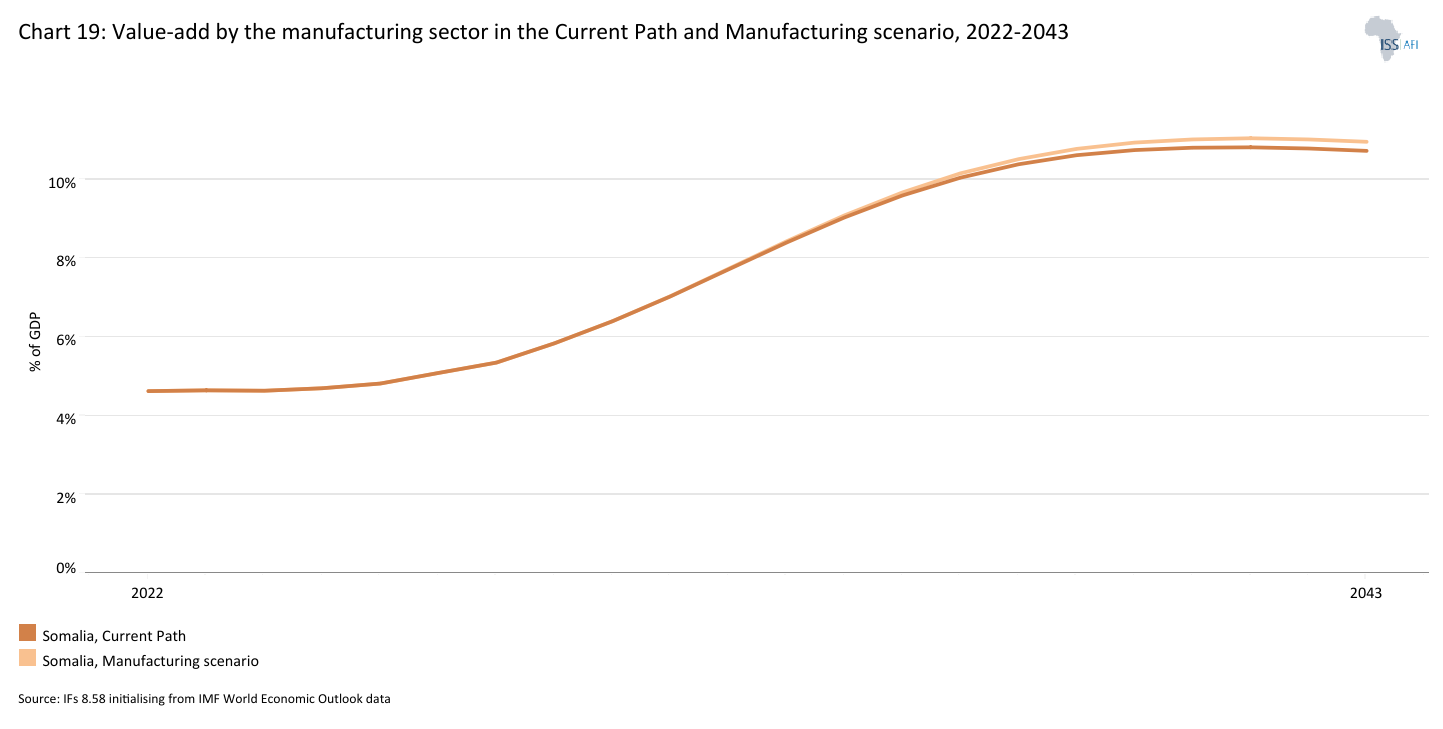

- By 2043, manufacturing value added will increase from approximately US$2.5 billion in the Current Path to US$2.7 billion in the Manufacturing scenario, an improvement of around US$200 million. While this reflects measurable industrial deepening in absolute terms, manufacturing’s share of GDP will remain at 11% in 2043. The limited impact highlights persistent structural constraints in Somalia. Industrial expansion remains closely tied to improvements in energy reliability, transport infrastructure, access to finance, skills development and institutional coherence. Without broader system-wide reforms in these enabling conditions, manufacturing growth does not generate strong backward and forward linkages or significant spillovers into higher-productivity employment.

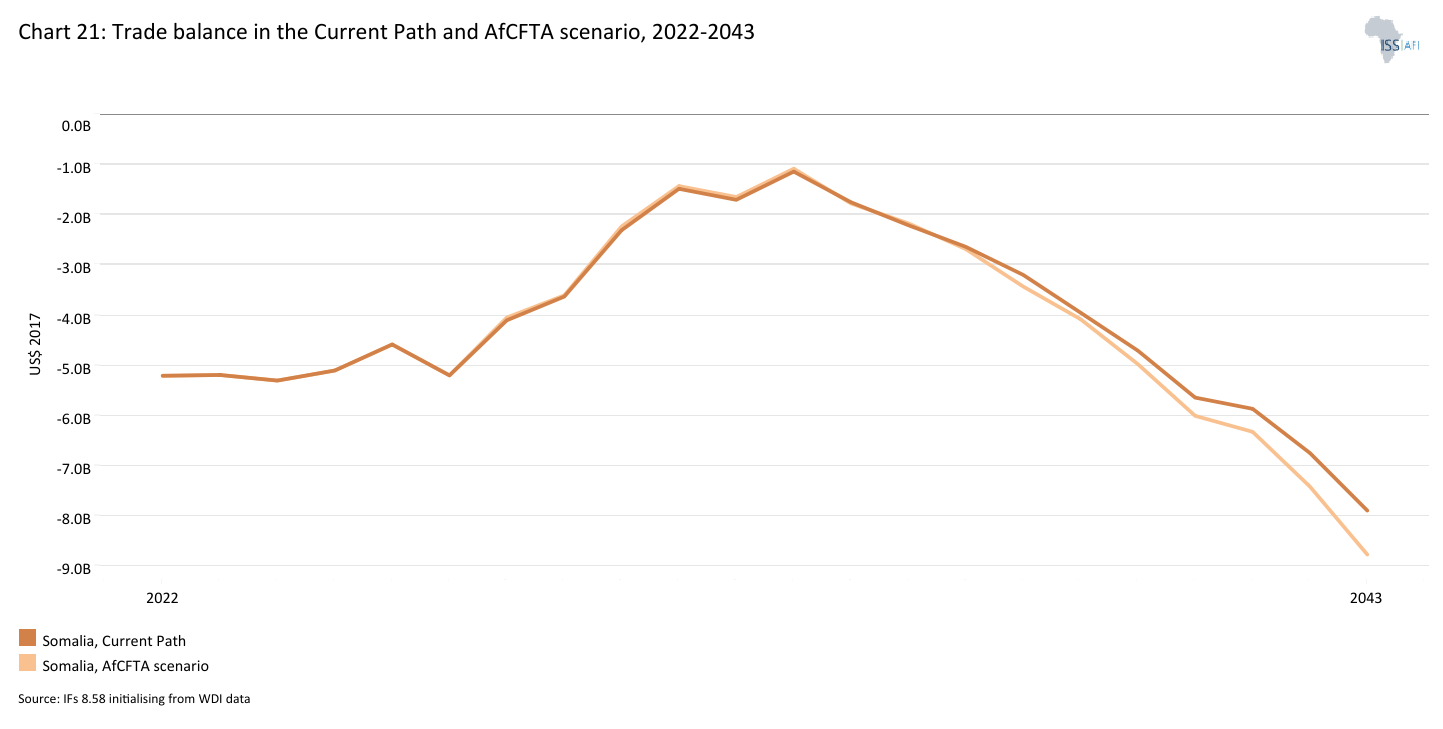

- Somalia’s trade deficit will decline significantly from 51.1% of GDP in 2023 to 19.4% by 2043 on the Current Path. In the AfCFTA scenario, the deficit will remain slightly higher at 20% of GDP in 2043. The limited gains reflect Somalia’s current trade structure. Exports are heavily concentrated in Gulf markets and dominated by low-value primary commodities, while the country remains highly dependent on imports of food, fuel and manufactured goods. As a result, reduced intra-African trade barriers do not immediately translate into large export gains. Over the longer term, however, AfCFTA could support the diversification of export markets and the development of the manufacturing and agro-processing sectors, provided complementary reforms strengthen domestic productive capacity and trade facilitation.

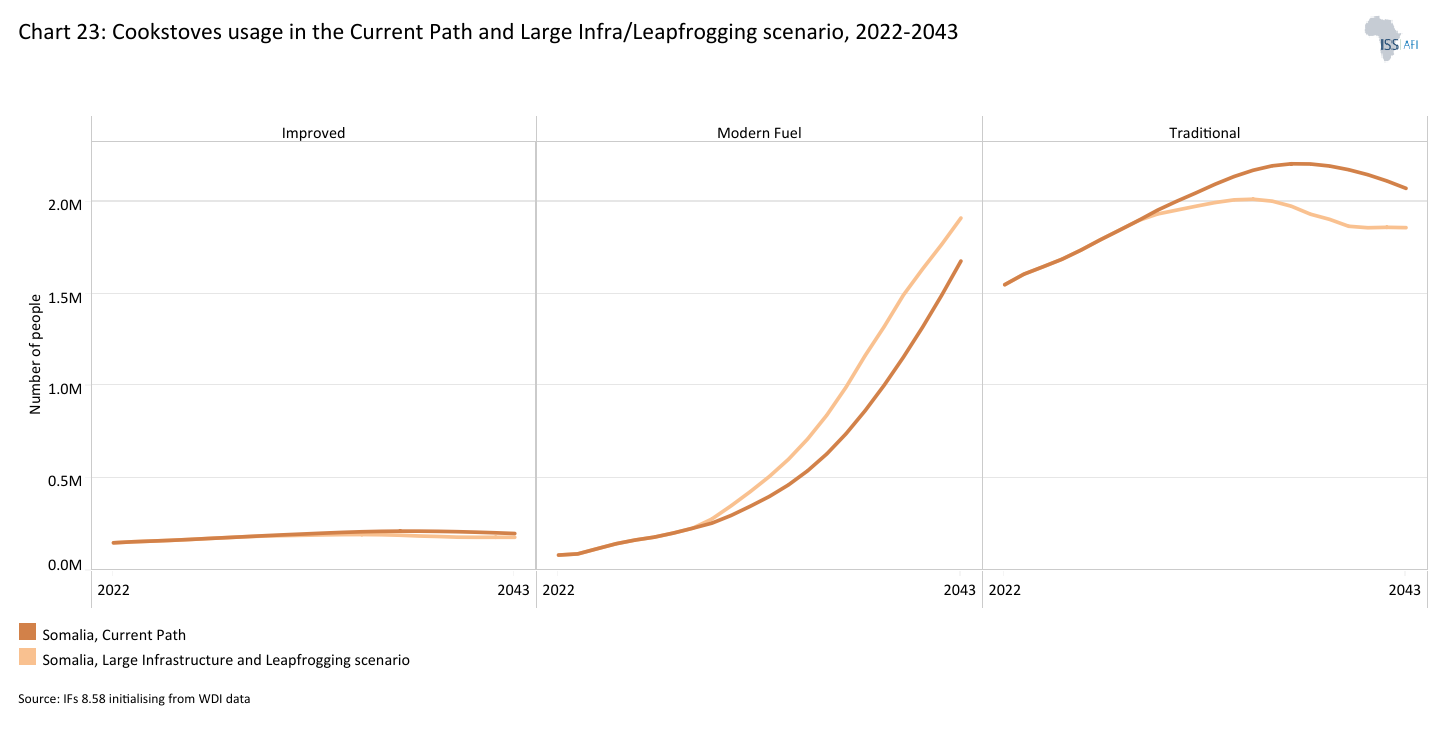

- In the Current Path, households using traditional cookstoves will increase from 1.6 million in 2023 to 2.1 million by 2043. In the Large Infrastructure and Leapfrogging scenario, the number of households using traditional cookstoves will be about 200 000 fewer than the Current Path forecast for 2043, indicating a modest acceleration in the shift away from biomass. This shift is reflected in modern fuel uptake. By 2043, 1.7 million people will use modern fuels in the Current Path, compared to 1.9 million in the Large Infrastructure and Leapfrogging scenario. The gains are tangible but limited.

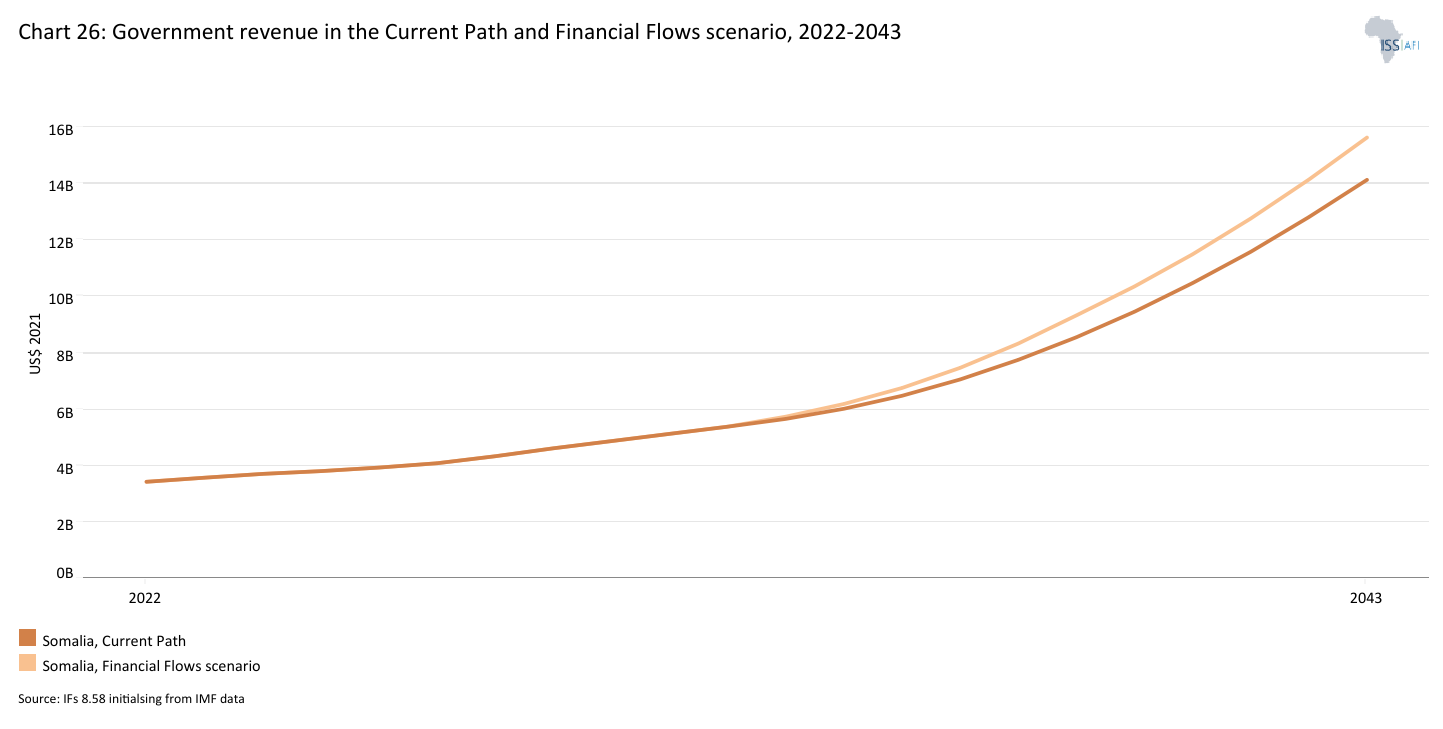

- Government revenue will increase from US$3.6 billion in 2023 to US$14.1 billion by 2043 on the Current Path. In the Financial Flows scenario, revenues will rise further to US$15.6 billion over the same period. As a share of the economy, government revenue stood at 35.2% of GDP in 2023 and will decline slightly to 34.8% by 2043 on the Current Path. In the Financial Flows scenario, improved financial inflows and strengthened fiscal capacity will raise government revenue to 37.3% of GDP by 2043.

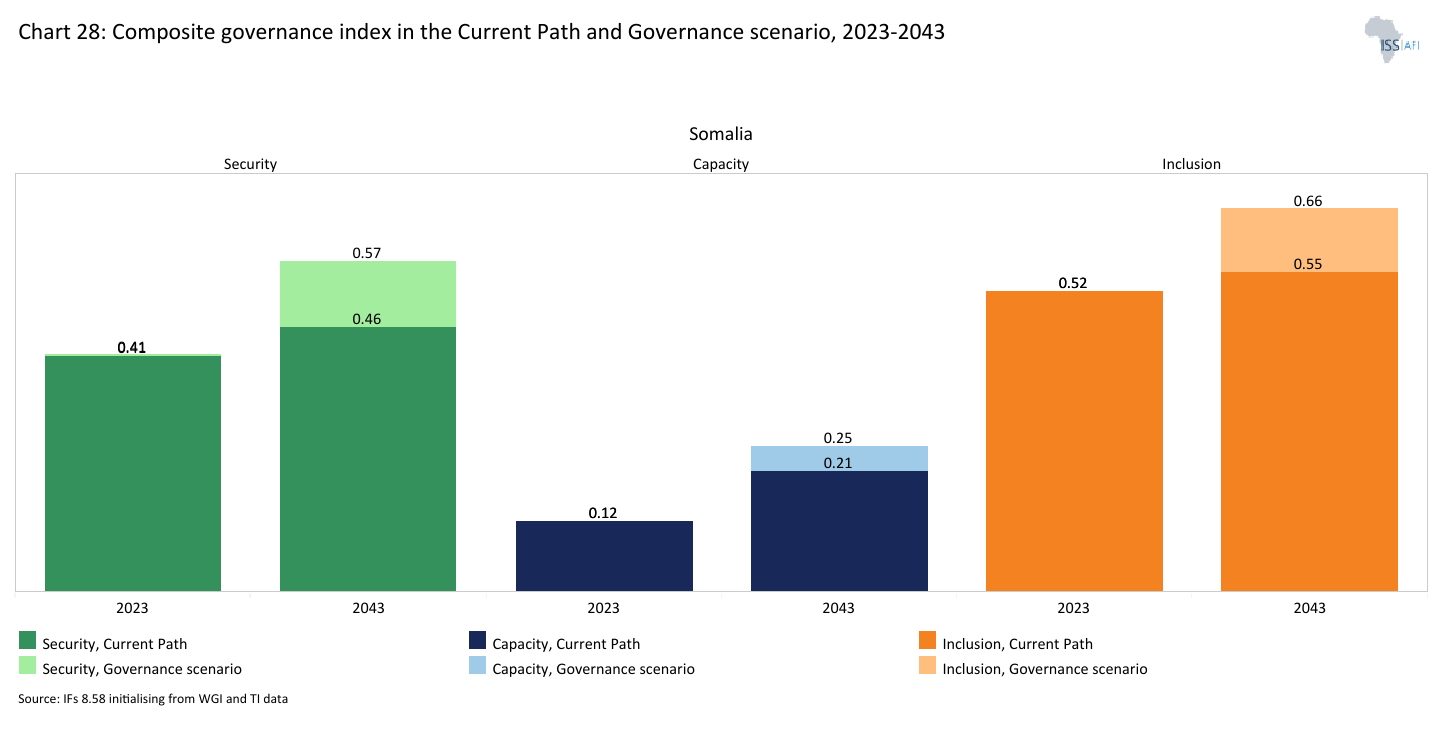

- Somalia’s governance performance remains weak but shows gradual improvement over time. The overall governance index will rise from 0.35 in 2023 to 0.41 by 2043 on the Current Path, while governance reforms will increase the score further to 0.49. Security remains a major challenge. Somalia’s security score of 0.41 in 2023 is well below regional averages (0.67 in East Africa and 0.63 for low-income Africa). Improvements are modest on the Current Path, reaching 0.46 by 2043, but reforms under the Governance scenario will raise the score more substantially to 0.57. State capacity is the weakest aspect of governance. With a score of 0.12 in 2023, it will improve only slowly to 0.21 by 2043 on the Current Path, and 0.25 in the Governance scenario, reflecting the long process of rebuilding core institutions after decades of state collapse. Inclusion performs comparatively better. The inclusion score will increase from 0.52 in 2023 to 0.55 by 2043 on the Current Path, and to 0.66 in the Governance scenario. However, broader political participation does not necessarily translate into stronger institutions or improved service delivery.

In the fourth section, we compare the impact of each of these eight sectoral scenarios with one another and subsequently with a Combined scenario (the integrated effect of all eight scenarios). In our forecasts, we measure progress on various dimensions such as economic size (in market exchange rates), gross domestic product per capita (in purchasing power parity), extreme poverty, carbon emissions, the changes in the structure of the economy, and selected sectoral dimensions such as progress with mean years of education, life expectancy, the Gini coefficient or reductions in mortality rates.

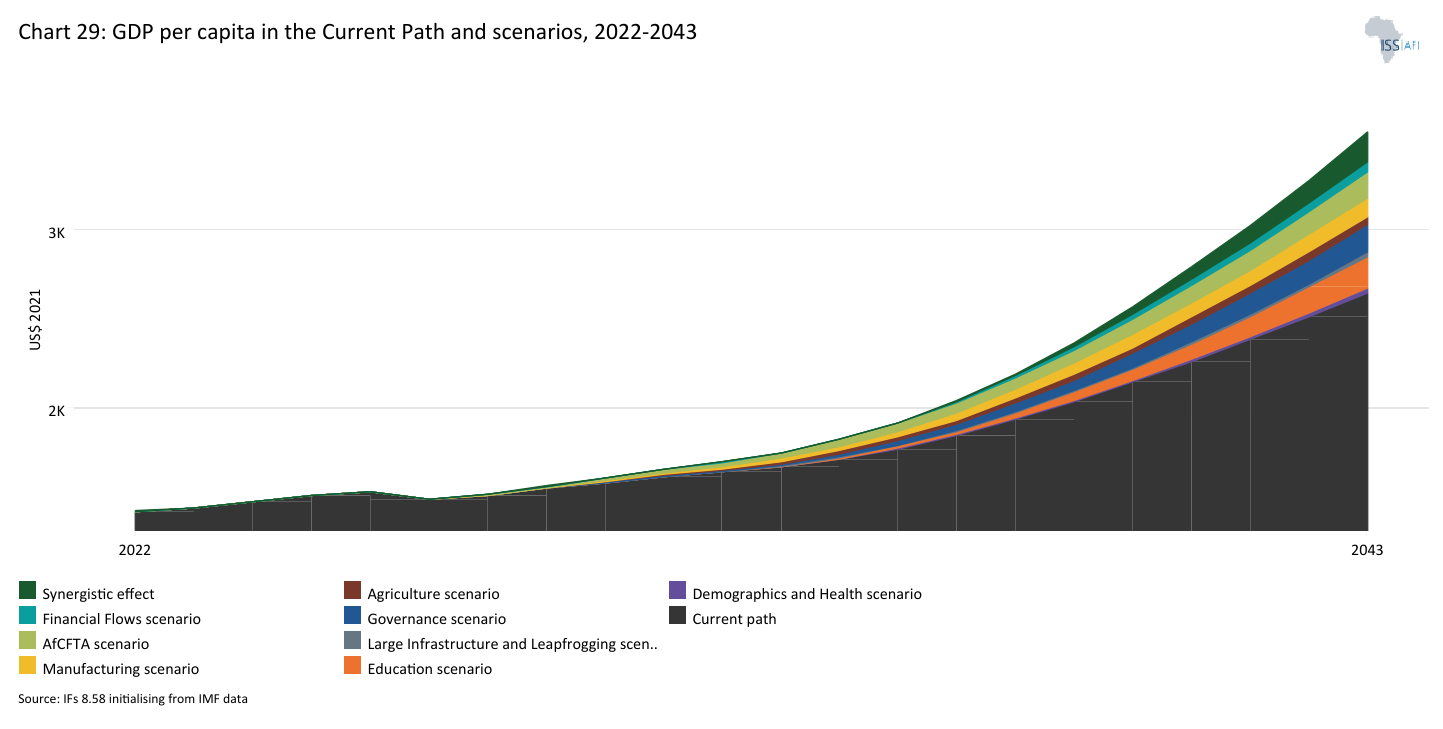

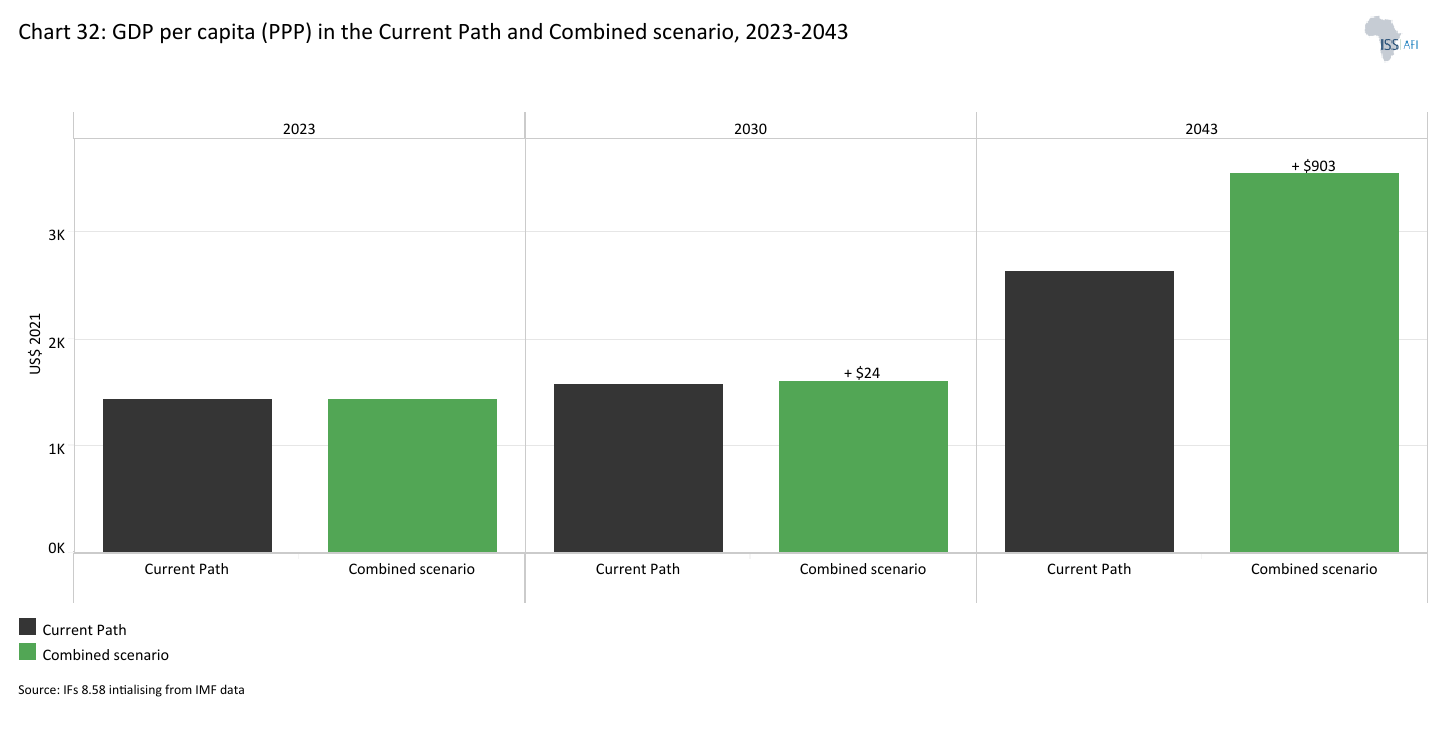

- Across individual scenarios, GDP per capita improves in every case relative to the Current Path, but the strongest gains come from Education (+US$182), Governance (+US$153) and AfCFTA (+US$142) by 2043. Education will deliver the largest uplift because Somalia’s human capital base is exceptionally low; even moderate improvements raise productivity, earnings and female labour force participation. Governance follows closely, reflecting how insecurity, weak institutions and regulatory uncertainty suppress investment and distort public spending. AfCFTA will generate meaningful gains by expanding market access and strengthening trade integration in a small, import-dependent economy. When reforms are combined, effects compound: coordinated implementation will add US$170 in synergy gains, lifting GDP per capita to US$3 547 by 2043, compared to US$2 654 on the Current Path. The evidence is clear, systemic reform outperforms isolated interventions.

- Poverty trends reinforce this conclusion. On the Current Path, the poverty rate will decline, but the absolute number of people in poverty will rise due to population growth. Under the Combined scenario, the poverty rate will fall from 73% in 2023 to 23% by 2043, reducing the number of people living below US$3.00 per day from a projected 13.7 million to 7.6 million, 6.1 million fewer than on the Current Path. Education will drive the strongest poverty reduction among single-sector scenarios, followed by Financial Flows and Governance, underscoring the interaction between human capital, institutional quality and income dynamics.

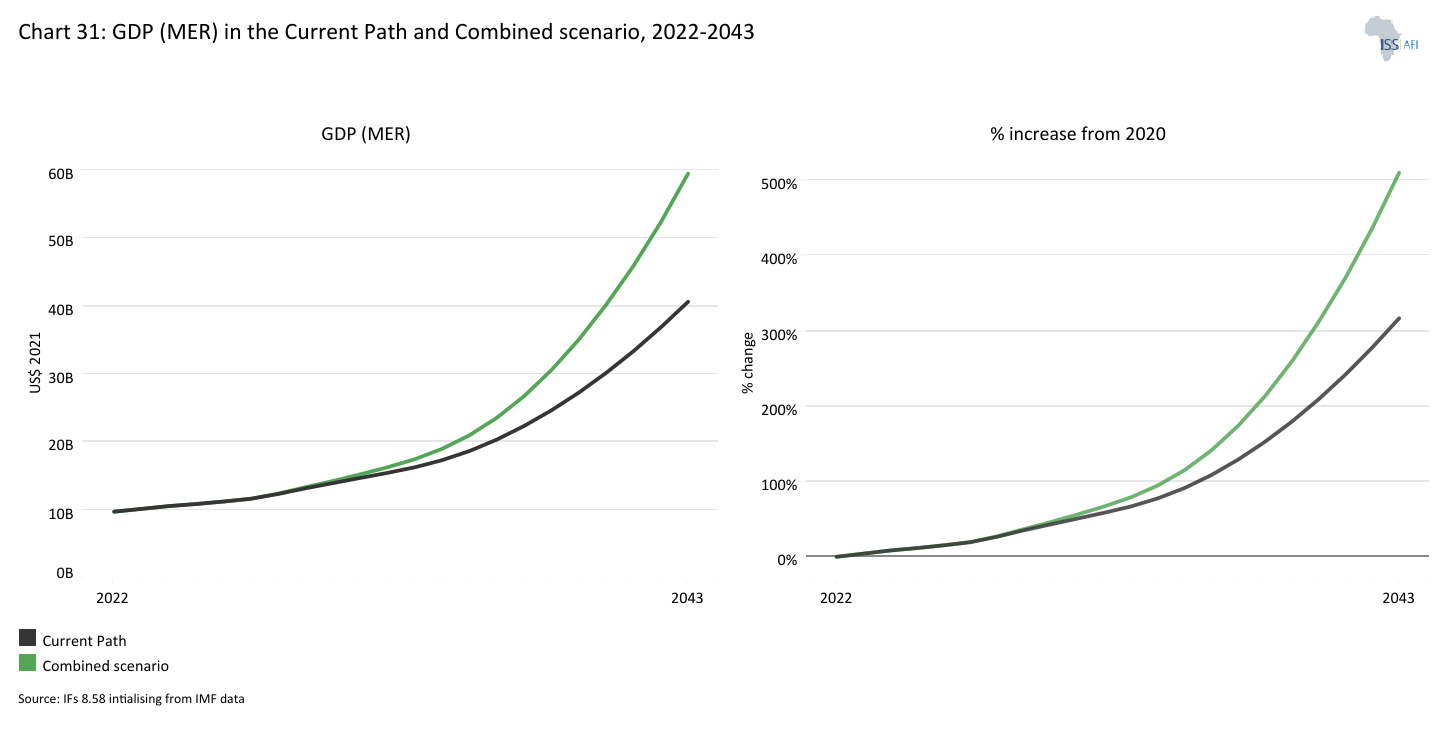

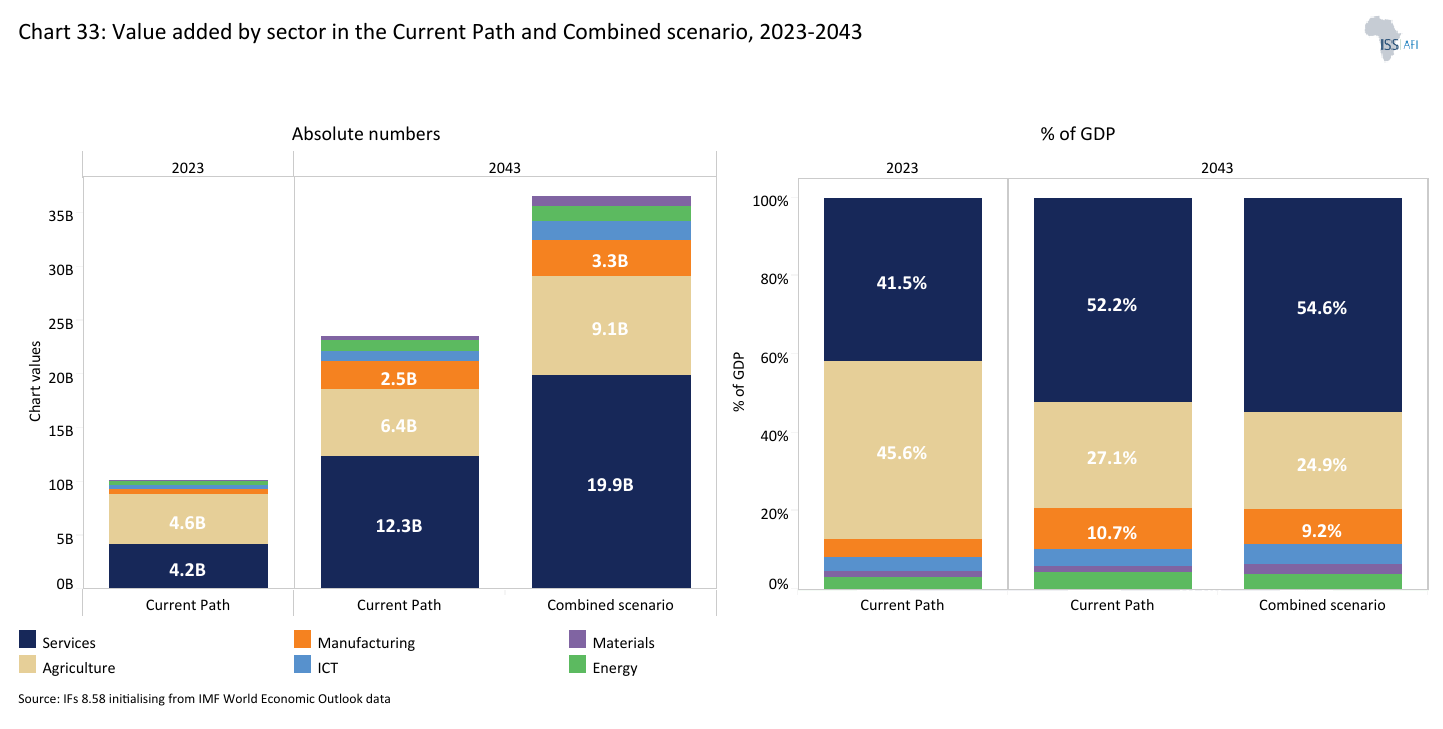

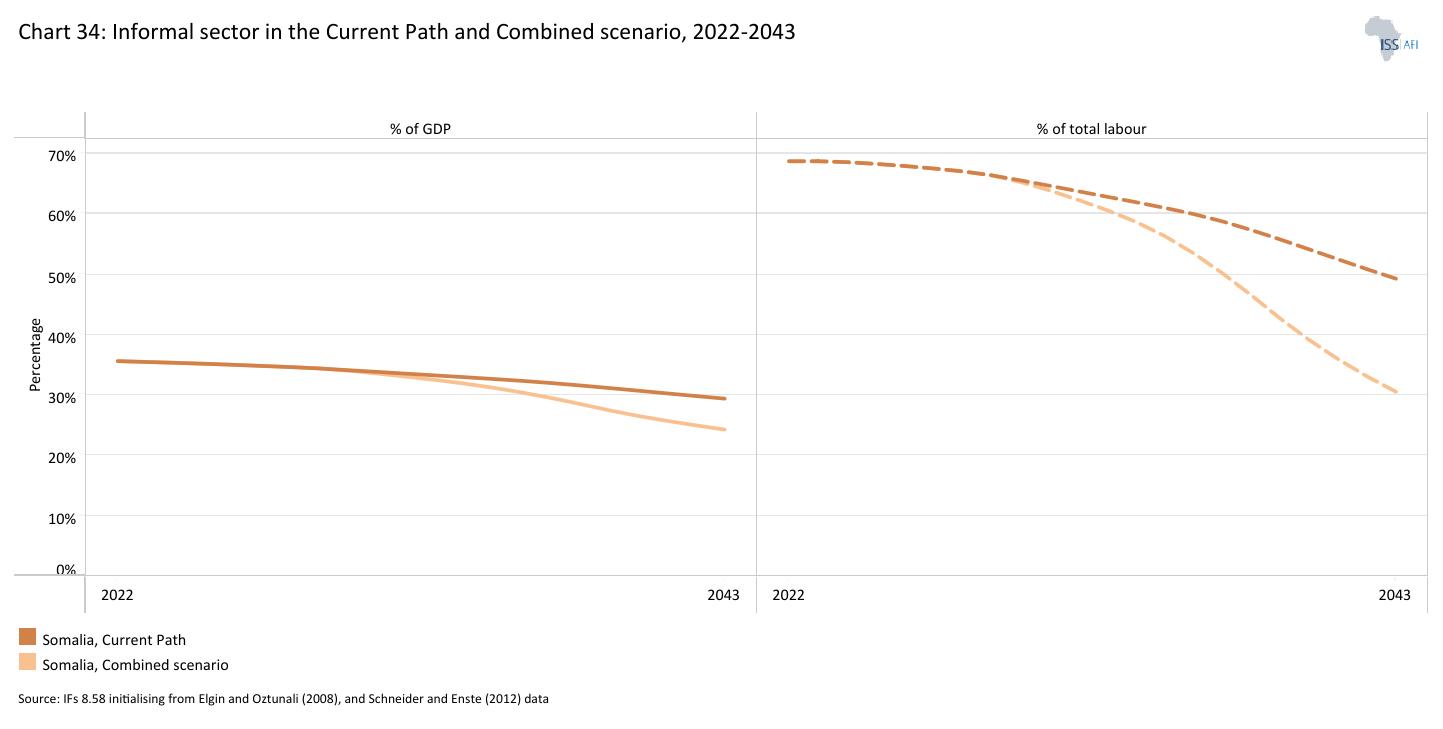

- GDP (MER) will rise to US$59.5 billion by 2043 in the Combined scenario, US$18.9 billion above the Current Path. The structure of the economy will shift, agriculture’s share will decline to 24.9%, while services will exceed 54% of GDP. Manufacturing will expand in absolute terms but will remain modest as a share of output, signalling a gradual rather than classic industrial take-off. Informality will fall sharply, with informal employment declining from 68.7% of the labour force in 2023 to 30.5% by 2043 under the Combined scenario, compared to 49.3% on the Current Path, indicating deeper formalisation and productivity gains.

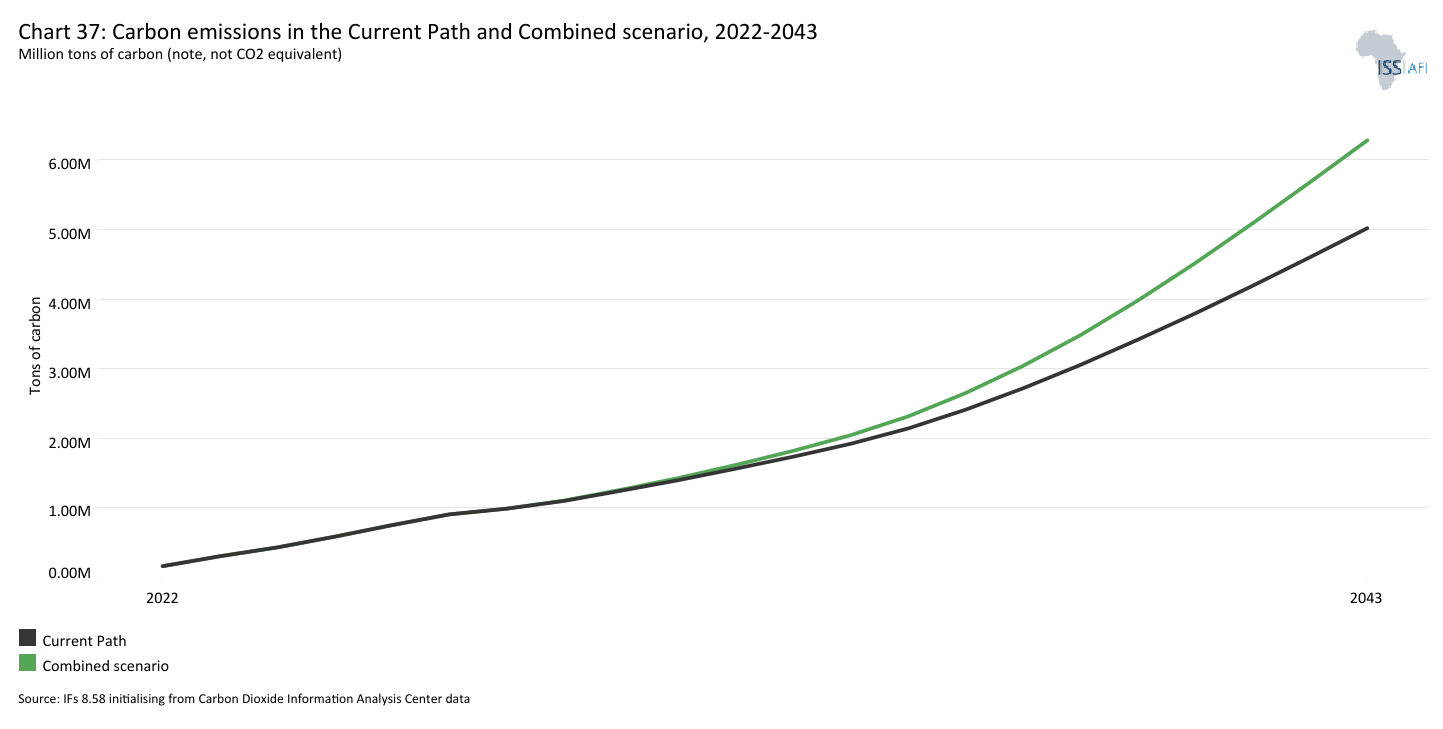

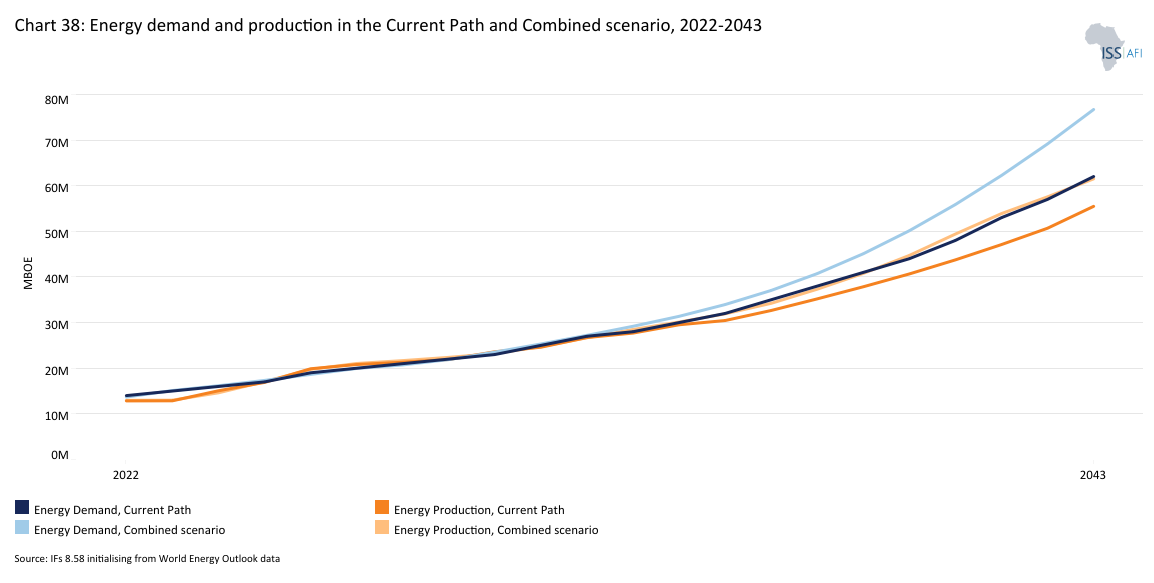

- Human development outcomes will also improve. Life expectancy will rise from 65 years in 2023 to 75 years by 2043 in the Combined scenario, three years higher than the Current Path. However, faster growth will bring higher energy demand and emissions. Carbon emissions will increase from 0.31 million tons in 2023 to 6.3 million tons by 2043 in the Combined scenario, above the Current Path, reflecting expanded industrial and infrastructure activity. Energy demand will grow faster than domestic production, putting upward pressure on supply unless generation capacity expands significantly.

- Overall, the modelling suggests that Somalia’s trajectory can shift meaningfully, but only through coordinated reforms that simultaneously strengthen institutions, human capital, trade integration, and infrastructure. Incremental progress is possible sector by sector. Structural transformation will require alignment across them.

We end this page with a summarising conclusion offering key recommendations for decision-making. Somalia’s development challenge is fundamentally one of fragility, low state capacity and limited structural transformation. Decades of conflict have weakened institutions, constrained service delivery and reduced the state’s ability to convert policy intent into implementation. At the same time, low human capital, rapid population growth, repeated climate shocks, a narrow export base and weak infrastructure continue to trap much of the economy in low-productivity activities. The result is a development trajectory in which progress remains possible, but slow, uneven and highly vulnerable to disruption. The analysis shows that Somalia is unlikely to achieve meaningful and sustained development through piecemeal reform. The Combined scenario reveals that substantial development improvements in economic growth, living standards and poverty reduction are achievable by 2043. Education and governance scenarios are among the most powerful levers for development in Somalia, generating the largest gains in GDP per capita while also accelerating poverty reduction. At the same time, Somalia must reduce structural economic vulnerabilities. Exports will remain heavily concentrated in livestock and reliant on a small number of Gulf markets, exposing the economy to demand shocks and policy changes. Diversifying trade through the African Continental Free Trade Area, alongside improvements in competitiveness, customs efficiency and trade logistics, can help broaden markets and strengthen resilience. More broadly, Somalia will need to diversify its economy by strengthening agriculture, agro-processing and manufacturing, supported by improvements in energy access, transport infrastructure and digital connectivity.

All charts for Somalia Development Futures

- Chart 1: Political map of Somalia

- Chart 2: Population structure in the Current Path, 1990–2043

- Chart 3: Population distribution map, 2023

- Chart 4: Urban and rural population in the Current Path, 1990-2043

- Chart 5: GDP (MER) and growth rate in the Current Path, 1990–2043

- Chart 6: Size of the informal economy in the Current Path, 2020-2043

- Chart 7: GDP per capita in Current Path, 1990–2043

- Chart 8: Extreme poverty in the Current Path, 2020–2043

- Chart 9: National Transformation Plan of Somalia

- Chart 10: Relationship between Current Path and scenarios

- Chart 11: Mortality distribution in the Current Path, 2023 and 2043

- Chart 12: Infant mortality rate in Current Path and Demographics and Health scenario, 2020–2043

- Chart 13: Demographic dividend in the Current Path and the Demographics and Health scenario, 2020–2043

- Chart 14: Crop production and demand in the Current Path, 1990-2043

- Chart 15: Import dependence in the Current Path and Agriculture scenario, 2020–2043

- Chart 16: Progress through the education funnel in the Current Path, 2023 and 2043

- Chart 17: Mean years of education in the Current Path and Education scenario, 2020–2043

- Chart 18: Value-added by sector as % of GDP in the Current Path, 2022 and 2043

- Chart 19: Value-add by the manufacturing sector in the Current Path and Manufacturing scenario, 2022–2043

- Chart 20: Exports and imports as % of GDP in the Current Path, 2000-2043

- Chart 21: Trade balance in the Current Path and AfCFTA scenario, 2020–2043

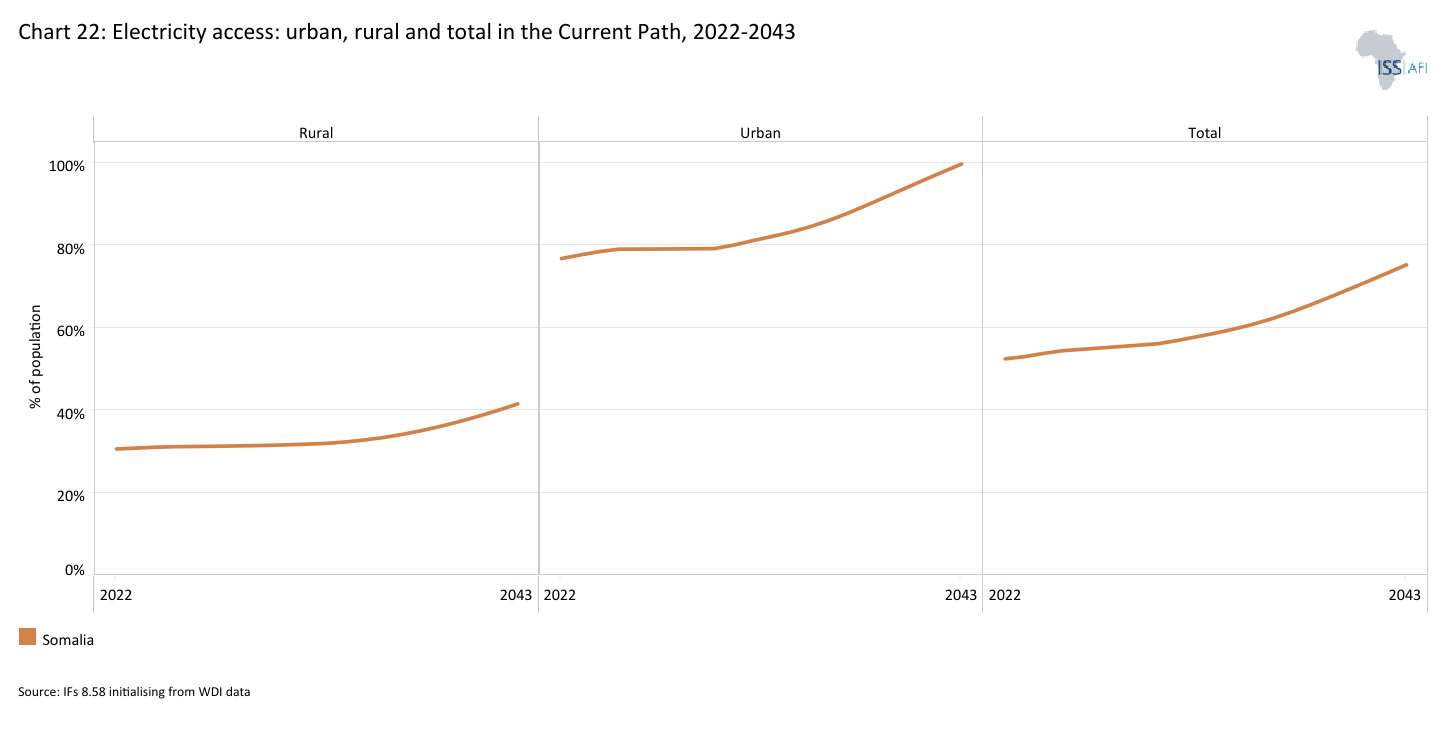

- Chart 22: Electricity access: urban, rural and total in the Current Path, 2000-2043

- Chart 23: Cookstove usage in the Current Path and Large Infra/Leapfrogging scenario, 2020–2043

- Chart 24: Access to mobile and fixed broadband in the Current Path and the Large Infra/Leapfrogging scenario, 2020–2043

- Chart 25: FDI, foreign aid and remittances as % of GDP in the Current Path and in the Financial Flows scenario, 1990-2043

- Chart 26: Government revenue in the Current Path and Financial Flows scenario, 2020–2043

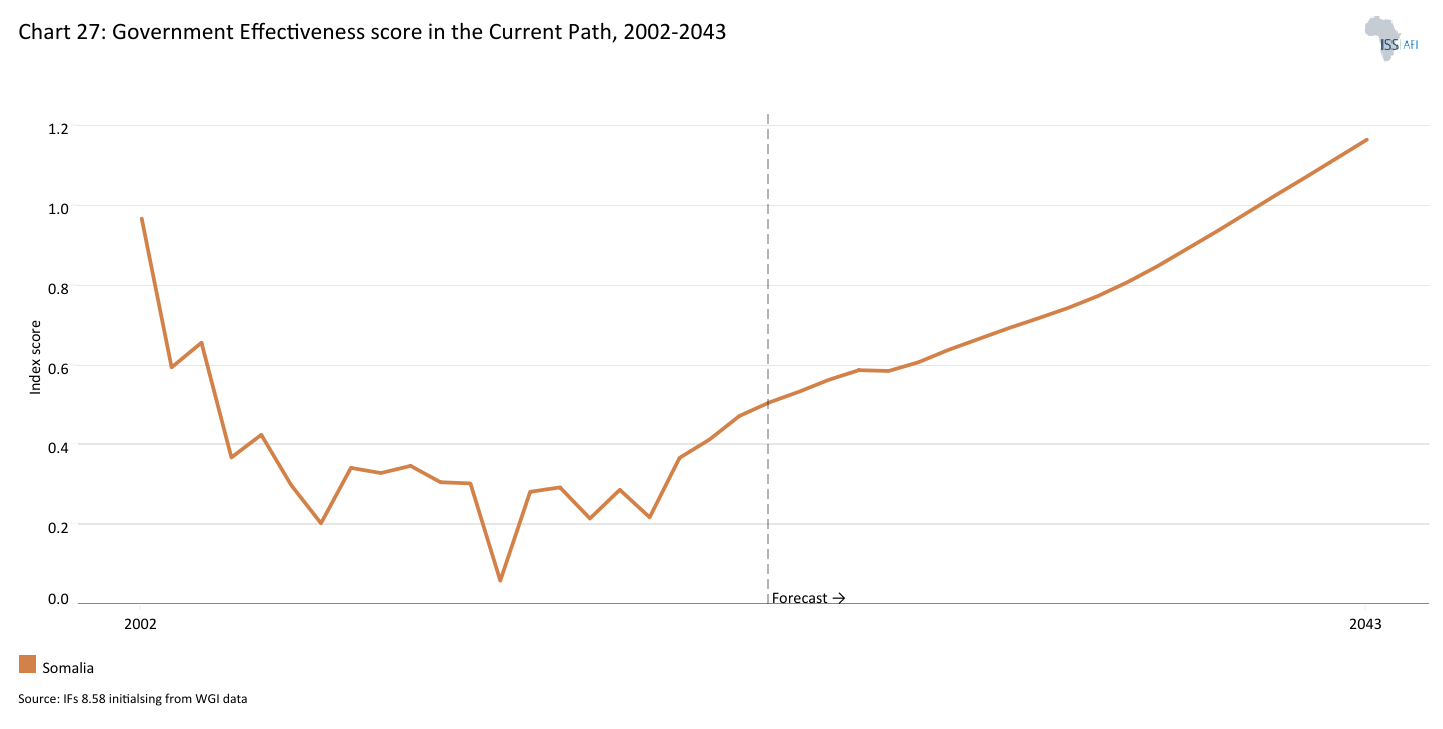

- Chart 27: Government effectiveness score in the Current Path, 2002-2043

- Chart 28: Composite governance index in the Current Path and Governance scenario, 2023 and 2043

- Chart 29: GDP per capita in the Current Path and scenarios, 2020–2043

- Chart 30: Poverty in the Current Path and scenarios, 2020–2043

- Chart 31: GDP (MER) in the Current Path and Combined scenario, 2020–2043

- Chart 32: GDP per capita in the Current Path and Combined scenario, 2023-2043

- Chart 33: Value-add by sector in the Current Path and Combined scenario, 2023 and 2043

- Chart 34: Informal sector in the Current Path and Combined scenario, 2020–2043

- Chart 35: Poverty in the Current Path and Combined scenario, 2023 and 2043

- Chart 36: Life expectancy in the Current Path and Combined scenario, 2020–2043

- Chart 37: Carbon emissions in the Current Path and Combined scenario, 2020–2043

- Chart 38: Energy demand and production by type in the Current Path and Combined scenario, 2020-2043

- Chart 39: Policy recommendations

Chart 1 is a political map of Somalia.

The Federal Republic of Somalia is located in the Horn of Africa and occupies a strategic position along the Gulf of Aden and the western Indian Ocean. It shares borders with Djibouti to the northwest, Ethiopia to the west and Kenya to the southwest. With a land area of approximately 637 655 km², it is one of the larger countries in East Africa. Its coastline, stretching more than 3 000 kilometres, is the longest on mainland Africa and shapes both maritime opportunity and exposure to security risks along major shipping corridors.

Somalia gained independence in 1960 and was among the earliest post-colonial African states to hold competitive multiparty elections and experience a peaceful transfer of power. This transition was interrupted by a military coup in 1969, which centralised authority under Siad Barre. The regime’s collapse in 1991 led to the fragmentation of the central state and prolonged civil conflict. Since 2012, Somalia has operated under a Provisional Federal Constitution and an internationally recognised Federal Government. The country is structured as a federal system comprising the Federal Government of Somalia and several Federal Member States. However, the allocation of powers, fiscal arrangements and completion of the constitutional review process remain politically contested.

Territorial fragmentation is a significant issue in Somalia’s governance. The brutal civil war and the collapse of the central government led by Siad Barre resulted in the establishment of a self-declared independent breakaway state, Somaliland, in the northwest (capital: Hargeisa) in 1991. Somaliland functions autonomously but lacks international recognition. Meanwhile, Somalia, with its capital in Mogadishu, continues to exist as the internationally recognised Federal Republic to this day.

Tensions escalated in 2024 when Ethiopia signed a port access agreement with Somaliland, prompting diplomatic pushback and regional mediation, and again in December 2025 when Israel announced recognition of Somaliland, triggering condemnation from Somalia, regional states and the African Union.

Somalia’s political calendar has become more contentious. Presidential elections had originally been planned for 2026, before the current government’s mandate expired in May. But progress towards the vote had already stalled amid deep disagreements between the federal government, opposition actors, and key federal member states over the timing, format and constitutional basis of the process. In that context, parliament’s March 2026 approval of constitutional changes extended the terms of the president and lawmakers from four to five years and pushed the election timetable back by a year. The federal government has presented the move as part of a transition towards direct elections, but it has deepened disagreements with opposition actors and key federal member states over the timing, format and constitutional basis of the electoral process. Rather than resolving uncertainty, the amendments have heightened the risk of a delayed or disputed political transition, contested mandates and renewed instability. This also raised renewed concerns about the credibility of the process and the orderly transfer of authority.

Somalia’s physical geography has long influenced its economic and social organisation. Much of the country is arid or semi-arid, characterised by low and highly variable rainfall. Beyond the northern highlands and the more fertile Juba and Shabelle river corridors, extensive flat plateaus and dry savannah dominate the landscape. These environmental conditions have historically favoured mobility as a strategy for managing climatic risk. Pastoralism and agropastoralism remain central to livelihoods, while clan-based social structures continue to shape political representation, dispute resolution and access to resources.

Somalis dominate Somalia's population, organised into clans tracing descent from common male ancestors, subclans and larger families. The Sab (Rahanweyn and Digil) are southern farmers and agropastoralists. Daarood inhabit the northeast, Ogaden and the Somalia–Kenya border. Hawiye live along the middle Shabelle and in the south-central areas. Isaaq occupy central and western northern Somalia. Dir reside in the northwest with southern dispersions, while Tunni hold the Marca-to-Kismaayo coast. Bagiuni, Swahili fishing communities, live along the coastal strip and nearby islands near Kenya.

Key minorities include trade-oriented Arab communities, mainly of Yemeni origin, and Somali Bantu, concentrated along the fertile Jubba and Shabelle river valleys, where they play a central role in irrigated agriculture. Many Somali Bantus descend from populations brought to the region through the nineteenth-century slave trade and have historically faced social marginalisation within Somalia’s clan-based hierarchy. A small Italian community also remains from the colonial period.

Somali, a Cushitic Afro-Asiatic language, serves as the primary official language and is widely understood across the country despite regional dialects. Arabic is the second official language, spoken mainly in northern regions and coastal towns. English and Italian, reflecting colonial legacies, are also widely used, particularly in higher education, while Swahili is spoken in parts of southern Somalia.

Almost all Somalis follow the Shāfiʿī school within Sunni Islam. Key Muslim orders (ṭarīqa), such as the Qādirīyah, Aḥmadīyah and Ṣaliḥiyah, exert significant influence.

Classified as a low-income country, Somalia remains among the most institutionally fragile states globally. A young and rapidly expanding population places sustained strain on public services, infrastructure and employment creation. Poverty is both widespread and persistent, with one of the highest extreme poverty rates in Africa and only modest gains in per capita income from a very low starting point. Much of the economy operates informally, limiting productivity, narrowing the tax base and constraining the state’s capacity to finance essential services and long-term investment.

State capacity has improved in selected areas, particularly those monitored by the IMF and World Bank, but remains uneven. Public financial management reforms enabled Somalia to reach the completion point of the Heavily Indebted Poor Countries Initiative (HIPCI) in December 2023, securing approximately US$4.5 billion in debt relief and strengthening macroeconomic credibility. However, fiscal gains have not translated uniformly into governance effectiveness. Revenue collection remains concentrated in the capital, Mogadishu; institutional performance varies across federal member states; and service delivery in sectors such as water, electricity, health and education is uneven and heavily reliant on private providers and external partners.

Security remains the most immediate constraint on state consolidation. The federal government does not exercise full territorial control, and al-Shabaab continues to influence or administer parts of the countryside, limiting the reach of state institutions. External assistance has therefore been central to rebuilding the security sector. For example, AU and UN missions, including the African Union Mission in Somalia (AMISOM) and its successor the African Union Transition Mission in Somalia (ATMIS), have supported counter-terrorism operations and the gradual transfer of security responsibilities to Somali forces. Regional and international partners, including Ethiopia, Turkey, the EU, the UK and the United States, have also provided training, equipment and logistical support to Somali security forces. In August 2024, the AU Peace and Security Council endorsed the establishment of a new AU-led and UN-authorised mission, the African Union Support and Stabilization Mission in Somalia (AUSSOM), underscoring the continued role of international and regional assistance. Establishing a unified command structure and sustainable national security architecture remains essential for long-term stability.

Somalia is a member of the Intergovernmental Authority on Development (IGAD) and formally joined the East African Community in December 2023. It acceded to the African Continental Free Trade Area (AfCFTA) in 2023 and ratified the agreement in 2025, reinforcing its stated commitment to deeper regional and continental economic integration after decades of fragmentation.

Finally, data constraints remain significant. Decades of conflict weakened national statistical systems, resulting in modelled population estimates, limited subnational economic data and uneven administrative reporting. These limitations require cautious interpretation of trends and careful triangulation when assessing Somalia’s development trajectory.

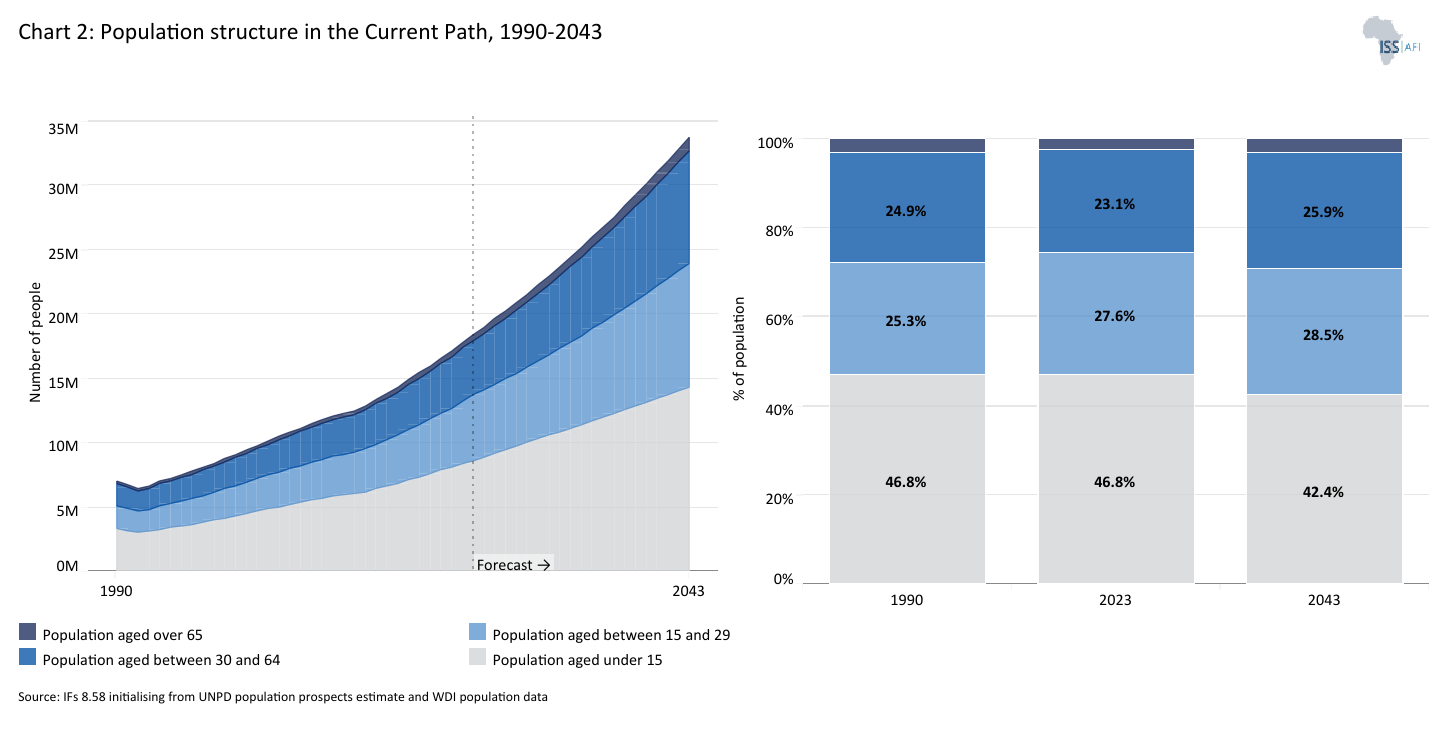

Chart 2 presents the Current Path of the population structure, from 1990 to 2043.

Somalia has not conducted a full national population census since 1975, meaning population trends over the past five decades have relied largely on estimates. The current Somali Population and Housing Census (SPHC), launched in 2023, marks a significant institutional milestone. The census project timeline outlines:

- March 2022 – December 2025: Pre-census activities

- January 2026 – October 2027: GIS development and cartographic mapping

- October – December 2028: Development of enumeration instruments and field testing

- January 2029 – December 2029: Enumeration, data processing and release of results

While the SPHC will eventually provide a national demographic baseline, existing estimates already offer valuable insight into Somalia’s population trajectory.

Despite prolonged civil conflict and state fragility, Somalia’s population has more than doubled over the past 33 years, from approximately 7.1 million in 1990 to 18.4 million in 2023. In 2024, the country ranked 24th in Africa and 68th globally in terms of population size. On the Current Path, the population will reach 33.7 million by 2043, making Somalia the 22nd most populous country on the continent.

This sustained population expansion is driven primarily by persistently high fertility, which remains among the highest globally. In the early 1990s, women had, on average, more than seven children each. The total fertility rate has declined gradually since then, but remained high at 6.1 births per woman in 2023. On the Current Path, it is expected to fall further to 4.6 births per woman by 2043. This will still exceed the replacement rate of 2.1, ensuring ongoing population growth and exerting sustained pressure on development outcomes in the coming decades.

Like many countries in sub-Saharan Africa, Somalia's population is predominantly young. In 2023, nearly three-quarters of the population was under 30, and almost half were children under 15. This means that a large portion of the population is dependent on the workforce to provide for its needs. On the Current Path, the population under 15 years will decline gradually, but will still constitute 42% of the population by 2043. The share of older persons (65 and above) has been stable at 3% over time, and is projected to remain 3% by 2043. The structure of Somalia’s population is typical of countries with high fertility rates and low life expectancy.

The dependency ratio, which compares children (under 15 years) and elderly (over 64 years) to the working-age (15-65 years) population, remains high at 97% and will continue to place sustained pressure on education systems, health services and job creation. These pressures are also unevenly distributed, with dependency ratios markedly higher in rural (131%) and nomadic (121%) areas than in urban (106%) areas. This suggests that support burdens are particularly acute outside cities, with implications for poverty, service provision and regional inequality.

Somalia’s demographic profile intersects with broader structural constraints on development. Around 75% of young people face unemployment, alongside limited educational attainment and restricted access to health services. These conditions compound the pressures created by a youthful, dependent population, constraining livelihoods, weakening economic prospects and limiting the country’s ability to translate demographic change into inclusive growth.

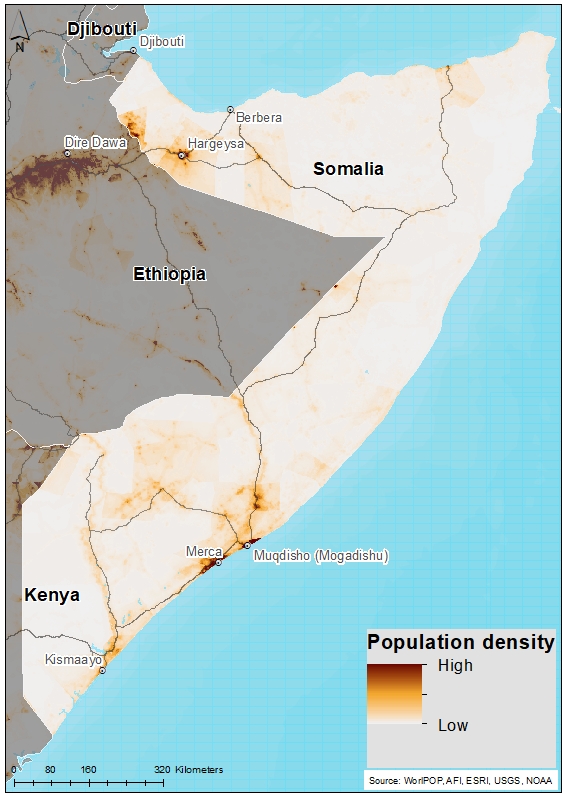

Chart 3 presents a population distribution map for 2023.

In 2023, Somalia had an average population density of 29 people per square kilometre, ranking 39th on the continent. Population distribution across the country is highly uneven, shaped by the interaction of climate conditions, livelihood systems, mobility patterns and fragmented governance.

Much of Somalia is arid to semi-arid, with highly variable rainfall patterns across space and time, which limits the feasibility of stable livelihoods and more permanent settlements. Higher population concentrations are found along the Juba and Shabelle river valleys, where irrigated agriculture supports more reliable livelihoods than in surrounding dryland areas. Historically, nomadic and pastoralist livelihoods have played a central role in shaping low-density settlement patterns, with seasonal mobility responding to the availability of pasture and water across extensive rangeland systems. Although the share of fully nomadic households has declined over time, mobility remains a defining feature of rural livelihoods, which still account for over 60% of the population.

Over the past decade, these traditional settlement systems have been increasingly disrupted by overlapping climate and conflict shocks. The country hosts one of the world’s largest internal displacement crises. By the end of 2024, conflict and violence had left around 3.1 million people living in internal displacement. Climate shocks have increasingly compounded and intensified displacement dynamics across the country. Since late 2021, Somalia has experienced one of the most severe droughts in decades, driven by multiple failed rainy seasons that devastated pastoral and agropastoral livelihoods. The drought triggered additional large-scale displacement, with well over a million people forced to move by early 2023, and its socioeconomic impacts have continued to reverberate beyond the peak crisis. From 2023 onwards, drought impacts have been compounded by extreme climatic volatility, including severe El Niño-related flooding, exposing millions of people to consecutive climate shocks.

Alongside climate stress, conflict and communal violence remain significant displacement triggers. In early 2023, clashes around Laascaanood led to the internal displacement of at least 150 000 people and pushed about 100 000 refugees into Ethiopia, many of whom arrived in remote and drought-affected areas. An estimated 316 000 new internal displacements linked to conflict and violence were reported in Somalia in 2024, less than half the number recorded in 2023, when fighting escalated sharply in the Sool region. This decline reflects an overall reduction in large-scale fighting and violence against civilians, despite continued military operations against Al-Shabaab and episodes of communal violence, including land-related conflicts in Gedo in July and October. By the end of 2024, an estimated 3.1 million people remained internally displaced due to conflict and violence, while disasters displaced more than 733 000.

Beyond internal displacement, Somalia remains one of the region’s major refugee-origin countries, with substantial Somali refugee populations in Kenya, Ethiopia and Yemen. Many have spent decades in exile, often in camp settings, reflecting a protracted refugee situation in which large refugee populations remain displaced for extended periods. As a result, entire generations of Somalis have grown up outside their country of origin. Host governments, including Ethiopia, have introduced measures to improve access to education, livelihoods and local integration, though constraints remain. Return movements from neighbouring countries occur periodically but remain modest relative to internal displacement. Nevertheless, returnees intersect with existing settlement pressures, particularly in urban and peri-urban areas. Population mobility in Somalia, therefore, operates across both internal and cross-border dimensions, further complicating spatial planning, service delivery and governance.

In response, the government has taken steps to strengthen institutional frameworks, including ratifying the Kampala Convention in 2019 and establishing a Durable Solutions Unit within the Ministry of Planning, Investment and Economic Development. Still, displacement pressures remain closely linked to insecurity, environmental stress and long-standing marginalisation, particularly in southern regions. In September 2024, the federal government adopted the National Solutions Pathways Action Plan for 2024–2029, outlining a framework to advance longer-term solutions for internally displaced persons and returnees. The plan focuses on expanding access to basic services, livelihood and employment opportunities, housing and tenure security, and social support systems. It builds on the earlier National Durable Solutions Strategy (2020–2024) and is aligned with broader national development priorities and the Sustainable Development Goals.

These spatial dynamics are further complicated by contested authority and state legitimacy. This includes Somaliland’s 1991 declaration of independence and its limited international recognition, as well as Puntland’s autonomous status within Somalia’s federal system, which has periodically been marked by tensions with the Federal Government over constitutional authority, governance arrangements and resource control. These issues gained renewed international salience in 2025, amid Israel’s announcement recognising Somaliland and debates at the United Nations Security Council, where concerns were raised that external engagement with Somaliland outside Somalia’s constitutional framework could undermine the country’s territorial integrity and regional stability.

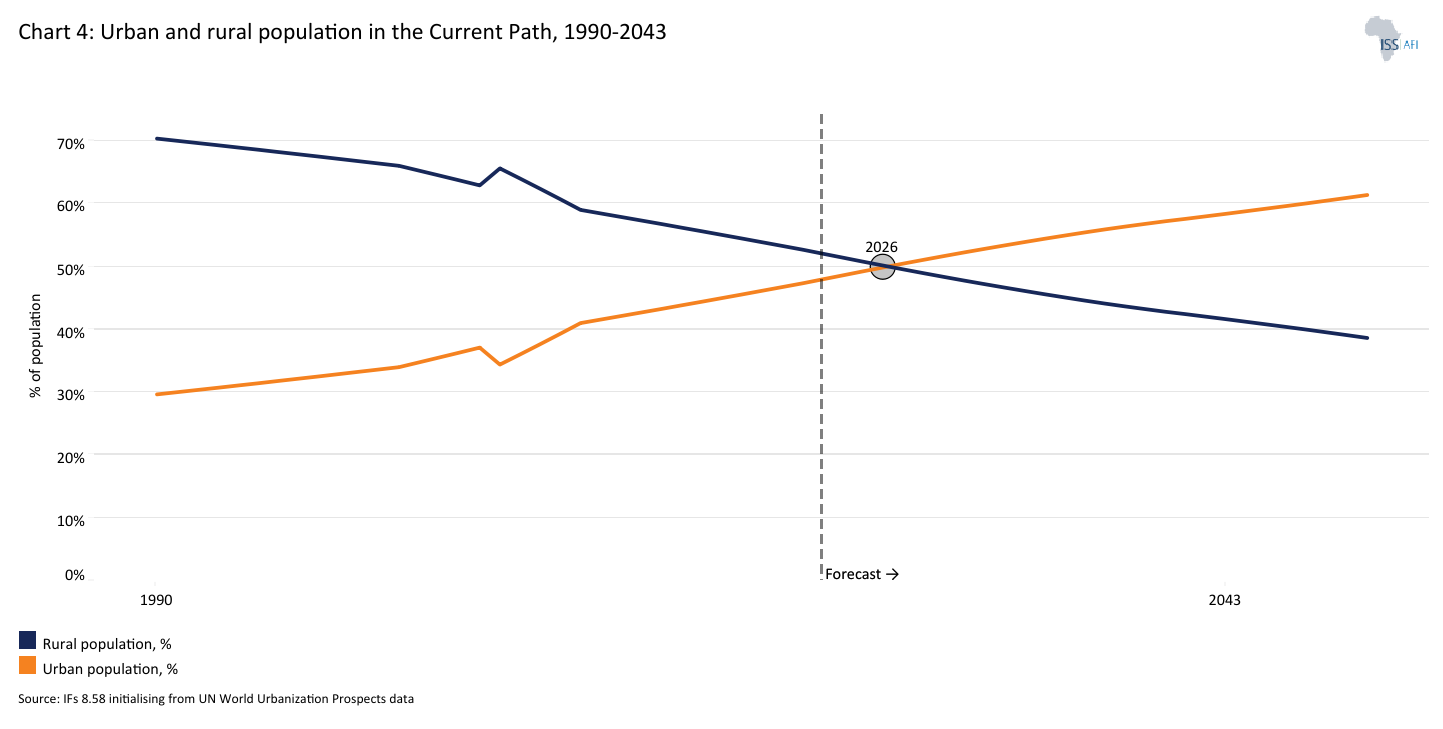

Chart 4 presents the urban and rural population in the Current Path, from 1990 to 2043.

Somalia is urbanising rapidly, and consistently faster than its low-income African peers. However, this urban expansion has been driven less by ‘classic’ structural transformation and instead by protracted conflict, climate shocks and large-scale internal displacement.

The urban population increased from 29.7% in 1990 to 48% in 2023, now ranking fifth among its low-income African peers and above the group average of 33.2%. On the Current Path, Somalia is expected to remain more urbanised than its peers, with the urban share rising to 58.4% by 2043, compared to a peer-group average of 42.8%.

Cities such as Mogadishu, Bosaso, Baidoa and Hargeisa are absorbing a disproportionate share of the displaced population. Much of this growth has taken the form of informal settlement, characterised by insecure land tenure, spatial segregation, weak service provision and high exposure to eviction. Nearly half of Somalia’s urban population lives in slum conditions, reflecting limited access to durable housing, improved sanitation and secure tenure. Municipal governance capacity remains extremely limited, shaped by fragmented authority, weak fiscal autonomy and minimal planning reach, while core urban services are predominantly delivered through private, informal or humanitarian systems.

As a result, Somali cities function as dense hubs of population and economic activity without corresponding institutional depth, inclusive labour markets or effective regulatory frameworks. Urban land has emerged as a central arena of political and economic contestation, reinforcing inequality, elite capture and social exclusion. Taken together, Somalia’s urbanisation reflects a distress-driven and structurally informal trajectory that is reshaping the country’s political economy, concentrating both opportunity and risk in cities that increasingly operate as de facto sites of governance in the absence of a consolidated social contract.

According to the World Bank, managing urbanisation is therefore central to Somalia’s development and stability, yet the country’s political and administrative realities render conventional urban policy approaches largely unworkable. While cities have benefited from committed local leadership and adaptive governance practices, these actors operate with limited tools and face persistent resistance and institutional constraints. Consequently, Somalia is not yet positioned to implement standard, state-centric urban development models. Instead, a transitional approach is required, one that works pragmatically within existing hybrid systems, avoids overburdening weak institutions and incrementally strengthens coherence, complementarity, credibility and capacity across formal and informal governance arrangements, including through regulated third-party service delivery models where appropriate.

Recent government strategies explicitly recognise the need to move beyond crisis management towards more durable and development-oriented responses to displacement and urbanisation. The National Transformation Plan (NTP 2025-2029) embeds urban-relevant priorities within its four pillars—including targeted infrastructure development, service delivery expansion, economic diversification and climate resilience—with an emphasis on strengthening institutional capacity, public sector efficiency and sustainable urban ecosystems as enablers of inclusive growth and stability in rapidly expanding cities. Complementing this, the Solutions Pathways Action Plan (2024–29) provides a practical framework for addressing displacement in urban and peri-urban areas, focusing on supporting local integration and improving access to basic services, livelihoods, and land and housing for displaced populations and host communities. The plan seeks, where feasible, to better align displacement responses with subnational planning processes and service delivery systems, recognising existing capacity constraints and institutional fragmentation. Together, these strategies point to an effort to move beyond short-term humanitarian responses towards more integrated, place-based approaches to displacement and urban governance. However, delivery continues to be shaped by weak capacity, fragmented authority and ongoing insecurity.

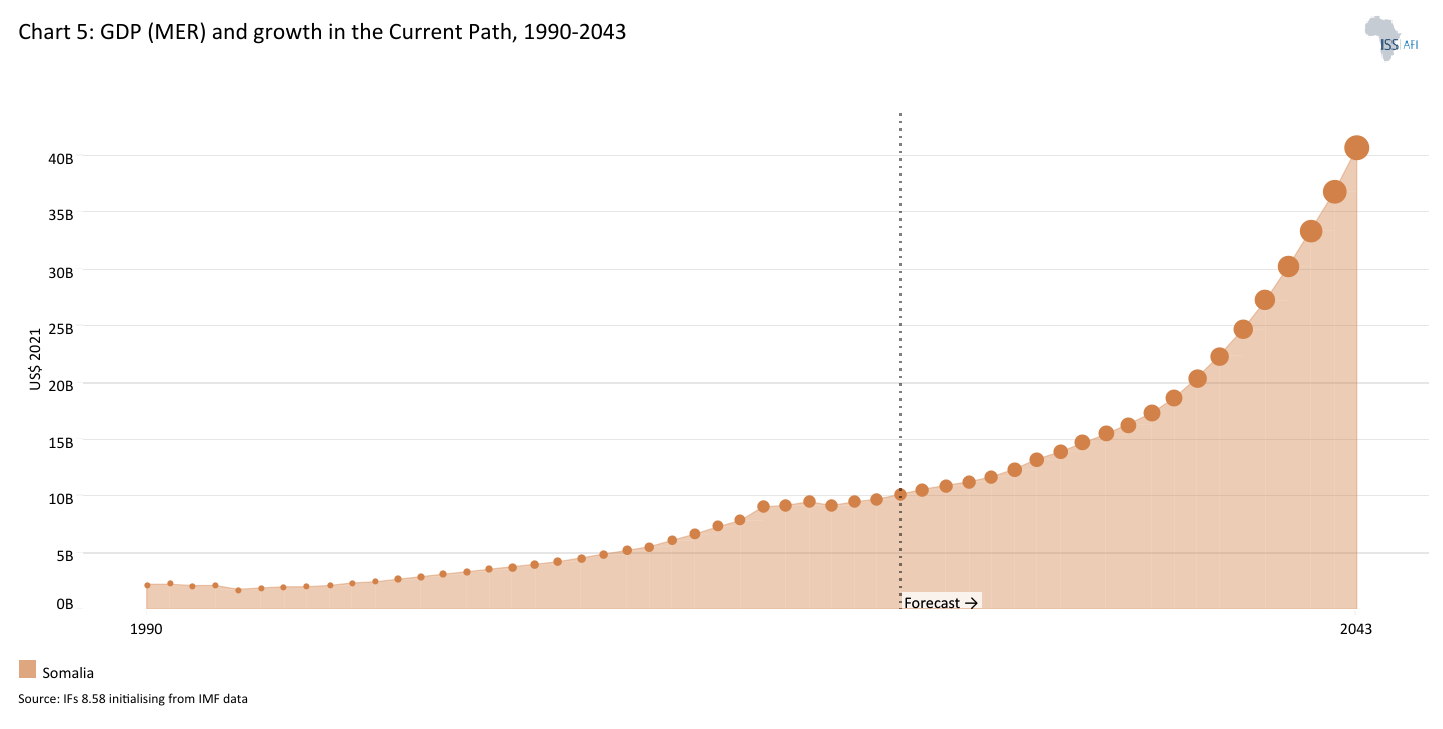

Chart 5 presents GDP in market exchange rates (MER) and growth rate in the Current Path, from 1990 to 2043.

Somalia’s economic trajectory reflects prolonged disruption followed by gradual but fragile recovery. GDP growth remained weak throughout the 1990s and early 2000s, shaped by state collapse, insecurity and the absence of formal economic institutions. From the late 2000s, activity began to recover as urban-based private-sector-led services expanded, including trade, telecommunications, transport and construction. Growth remained modest and uneven, concentrated in major urban centres and driven primarily by private adaptation rather than structural transformation.

Agriculture underpins the economy, contributing over 70% of GDP and employing over 80% of the labour force. Yet productivity remains low and highly exposed to climatic shocks. Recurrent drought, insecurity and climate-related disruptions constrain productivity and deter long-term investment. The economy operates within a de facto dollarised system that facilitates transactions despite weak monetary institutions but limits policy flexibility and domestic financial deepening.

Aid continues to play a central role in macroeconomics. External grants finance a substantial share of public expenditure, development projects and service delivery due to very limited domestic revenue mobilisation. While this support has helped stabilise public finances and sustain basic services, it also underscores the state’s fiscal vulnerability and dependence on external partners.

Completing the Heavily Indebted Poor Countries (HIPC) Initiative in 2023 marked an important milestone, sharply reducing external debt and restoring access to concessional finance. However, debt relief alone does not alter the underlying growth model. Somalia’s expansion remains services-led and externally supported, with limited structural transformation.

In 2023, Somalia’s GDP stood at US$8.6 billion, up from US$1.9 billion in 1990, reflecting an average growth rate of 4.9% over this period. By 2043, the economy will reach US$20.8 billion in the Current Path, implying a faster average growth rate of 7.4% between 2024 and 2043. However, Somalia’s economy remains vulnerable, externally supported and insufficiently diversified to absorb demographic pressures or deliver sustained structural transformation.

Overall, Somalia’s economy has stabilised and resumed growth, but it has not yet transitioned onto a path of diversified, productivity-driven development. The central question over the next two decades is whether macroeconomic stabilisation and incremental urban expansion can translate into structural transformation, job creation and resilience, or whether growth will remain narrow, shock-prone and externally anchored.

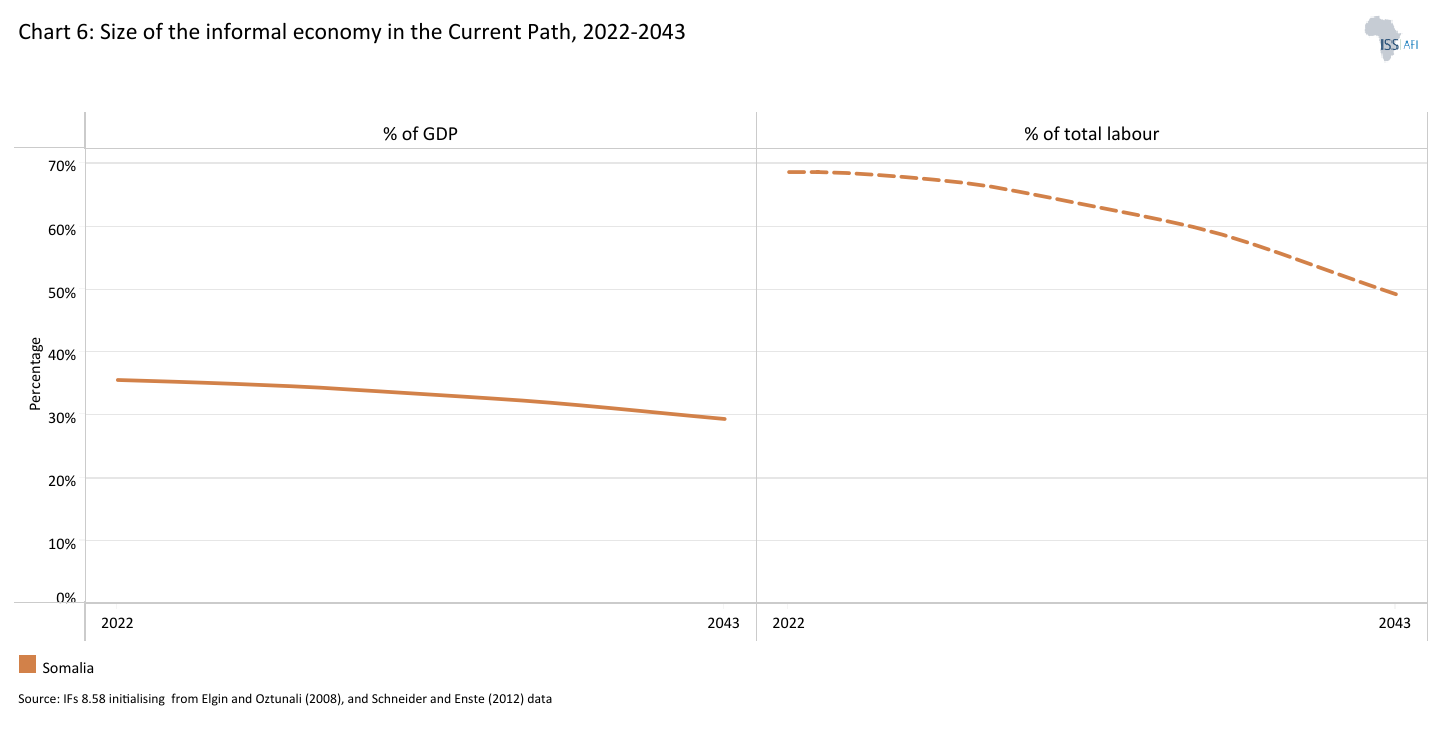

Chart 6 presents the size of the informal economy as per cent of GDP and per cent of total labour (non-agriculture), from 2020 to 2043. The data in our modelling are largely estimates and therefore may differ from other sources.

Somalia’s economy is predominantly informal, with a large share of the labour force concentrated in subsistence agriculture and pastoral livelihoods. This economic structure exposes households and output to significant vulnerability, given the heavy dependence of these sectors on rainfall and open grazing systems. Structural constraints are compounded by weak physical and digital infrastructure, including limited transport connectivity and communications networks, which continue to impede business activity, market integration and productivity. Persistent gender inequality further constrains economic potential, as social norms and unequal access to education and employment limit women’s participation in the labour market, reducing overall labour supply and human capital development.

Informality is not confined to low-productivity or rural activities but extends across most sectors of the economy. Very high rates of informal employment also prevail in health and social services, finance and insurance, and information and communication activities, where the vast majority of workers operate outside formal employment arrangements.

In 2023, the informal economy accounted for 36% of the country’s GDP, ranking 11th-highest on the continent. By 2043, it will decline to 29%, roughly at par with the average for low-income countries in Africa (28%). The informal economy, excluding the agriculture sector, employed 69% of total labour in 2023, with a projected decline to 49% by 2043.

While the informal economy provides an essential safety net for Somalia’s large and growing working-age population, it also constrains productivity, limits policy effectiveness and slows structural transformation. High levels of informality reduce access to better wages, social protection and redistributive mechanisms, while weakening the state’s ability to regulate and support economic activity. Although recent reforms signal progress towards formalisation, including the 2019 Company Act, the 2023 Investors and Investments Protection Law and the rollout of the Somali Business Registration System, their impact remains limited. Institutional fragility, governance weaknesses, overlapping federal and state mandates, persistent insecurity and the continued reliance on informal and clan-mediated arrangements undermine regulatory predictability and transparency. As a result, Somalia remains one of the most challenging environments for formal business activity and sustained private investment, despite incremental reform efforts.

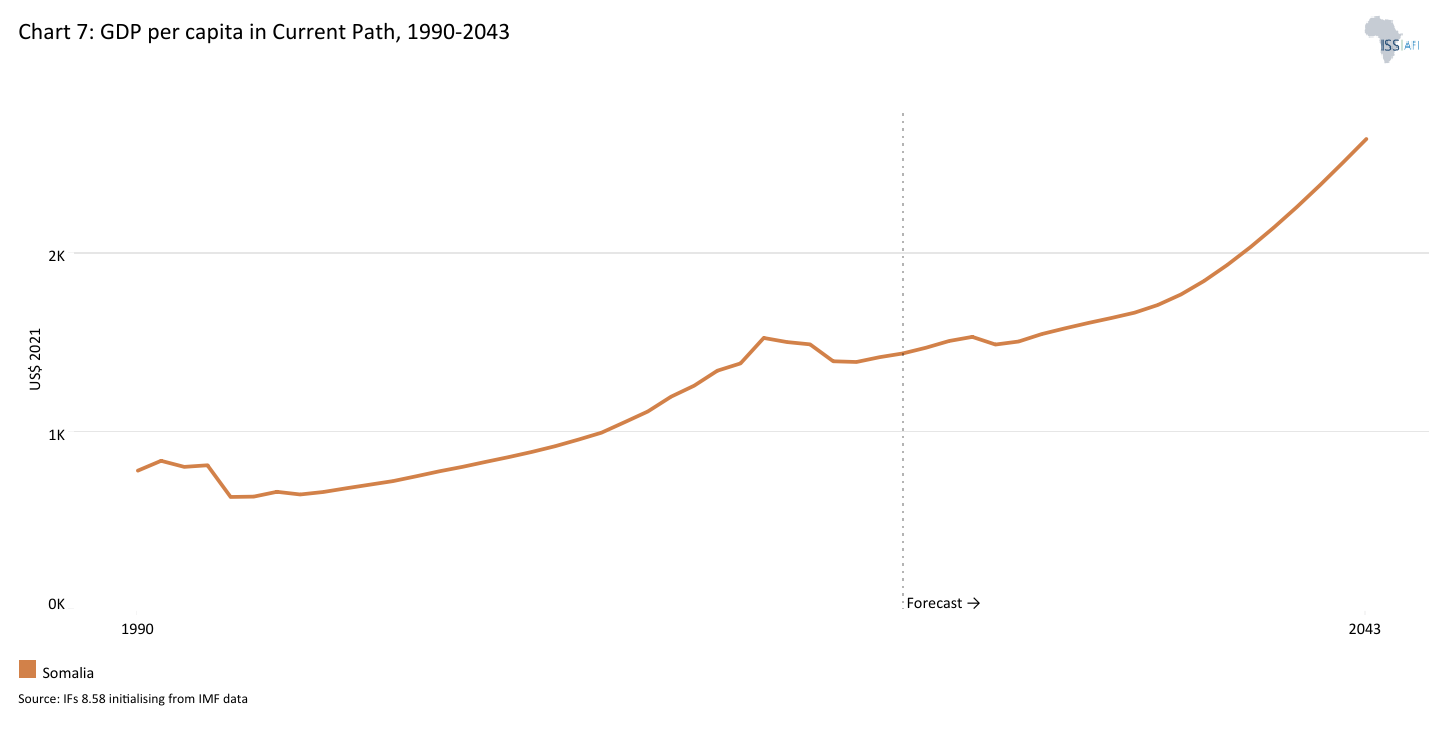

Chart 7 presents GDP per capita in the Current Path, from 1990 to 2043, compared with the average for the Africa income group.

Somalia’s GDP per capita, measured in purchasing power parity (PPP), constant 2021 US dollars, reflects a long-term pattern of disruption and slow recovery. In 2023, Somalia’s GDP per capita stood at US$1 466, the fourth-lowest on the continent. By 2043, GDP per capita will reach US$2 644, which would improve Somalia’s relative position slightly to 46th out of 54 African countries. Even with this increase, income levels would remain well below the projected average of its low-income African peer group, estimated at US$5 117 in 2043, and the country is therefore likely to continue facing a substantial income gap relative to comparable economies over the next two decades.

This reflects underlying structural constraints that limit the pace of income growth, including high population growth, persistent informality, low productivity and the dominance of consumption-driven, services-led activity. While urbanisation, remittances and incremental macroeconomic stabilisation support continued growth, these factors alone are insufficient to trigger a decisive income take-off in the absence of industrialisation, productivity gains or large-scale employment creation.

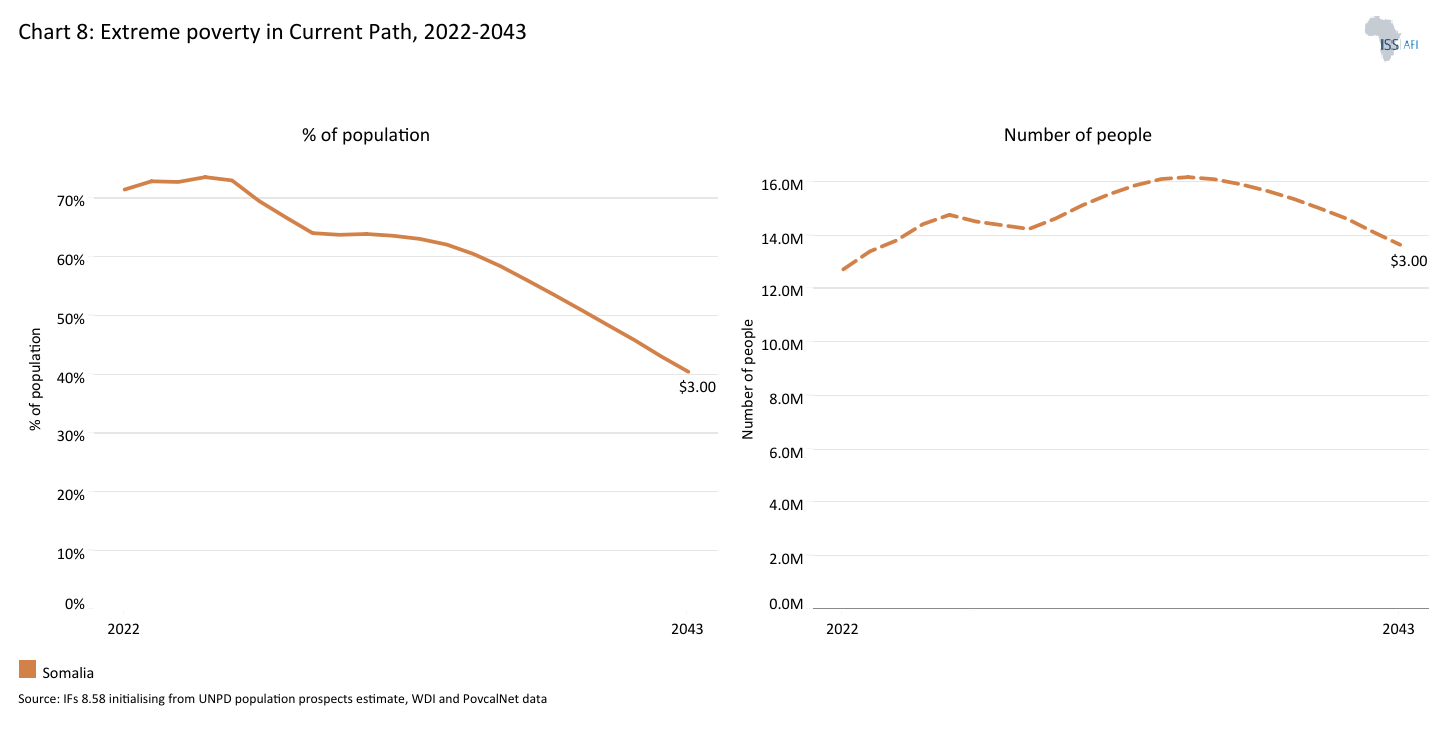

Chart 8 presents the rate and number of extremely poor people in the Current Path from 2020 to 2043.

In 2024, the World Bank updated the poverty lines to 2021 constant dollar values as follows:

- The previous US$2.15 extreme poverty line is now set at US$3.00, also for use with low-income countries.

- US$3.65 for lower-middle-income countries, now US$4.20 in 2021 values.

- US$6.85 for upper-middle-income countries, now US$8.30 in 2021 values.

Poverty in Somalia remains widespread, persistent and structurally entrenched. Half of the population (54%) lives below the national poverty line (US$2.06 per day), and there was no progress between 2017 and 2022. This stagnation reflects weak per capita consumption growth and repeated exposure to shocks, particularly climatic shocks. While national poverty rates appear stable, this masks important underlying deterioration in rural and nomadic areas. Poverty is unevenly distributed across geography and livelihood systems, with the highest rates among nomadic households (78%) and lowest in urban areas (46%).

Using the international extreme poverty line of US$3.00 per day, Somalia had the seventh-highest poverty rate among its peer group in 2023. At this poverty threshold, around 73% of Somalians (equivalent to 13.4 million people) were living in poverty. On the Current Path, this rate will decline to 41% by 2043. However, the absolute number of people increases to 13.7 million due to population growth.

Monetary poverty only tells part of the story. In addition, the global Multidimensional Poverty Index (MPI) measures acute multidimensional poverty by measuring each person’s overlapping deprivations across 10 indicators in three equally weighted dimensions: health, education and standard of living. The MPI complements the international poverty rate by identifying who is multidimensionally poor and by showing the composition of multidimensional poverty. The headcount or incidence of multidimensional poverty is often several percentage points higher than that of monetary poverty. This implies that individuals living above the monetary poverty line may still suffer deprivations in health, education and/or standard of living.

In 2024, Somalia released its first National Multidimensional Poverty Index (MPI) using 2022 household data, establishing a baseline for assessing non-monetary deprivation. The findings reveal that multidimensional poverty is both widespread and severe. Approximately two-thirds of the population experience overlapping deprivations, and those classified as poor are, on average, deprived in more than half of the weighted indicators used to assess wellbeing. Poverty is significantly higher outside urban areas. While 62% of urban residents are multidimensionally poor, the incidence rises to 74% in rural areas and 82% among nomadic populations.

Regional disparities are equally stark. In some regions, such as Bakool and Hiraan, multidimensional poverty affects over 90% of the population, whereas in others, including Awdal and Lower Shabelle, it records substantially lower rates. The pattern of deprivation points to structural deficits in living standards and education as the main drivers of multidimensional poverty. Nationally, the most pervasive gaps concern cooking fuel availability and overcrowding, alongside serious shortfalls in education. Among nomadic communities, education is the dominant contributor, driven especially by low years of schooling and poor school attendance.

Poverty dynamics are also closely linked to fragility. Recurrent droughts and floods erode assets and destabilise pastoral and agricultural livelihoods. Conflict disrupts trade, displaces communities and weakens institutional capacity. The labour market remains dominated by informality, limiting income stability and productivity gains. Social protection systems are expanding but remain insufficiently scaled to cushion repeated shocks. As a result, many households fluctuate between vulnerability and crisis.

Somalia’s National Transformation Plan (NTP) 2025–2029 places poverty eradication at the centre of its development agenda, embedding it within a broader commitment to resilience, equity and inclusion. The Plan moves beyond narrow income-based approaches by strengthening social protection systems, expanding adaptive safety nets and improving social care services to shield vulnerable households from shocks and chronic deprivation. It recognises that breaking poverty cycles requires sustained investment in human capital, particularly through expanding access to education, skills development and nutrition support.

The NTP also treats inclusion as a structural imperative. Women’s economic empowerment, youth employment and entrepreneurship, and the institutional integration of persons with disabilities are positioned as core pillars of transformation. By aligning vocational training with labour market demand, promoting access to finance, addressing gender-based barriers and reforming legal and governance frameworks, the Plan seeks to expand productive participation across society.

Chart 9 depicts the National Transformation Plan of Somalia.

Since the mid-2010s, Somalia has progressively re-established a national development planning framework after decades of state collapse and fragmented governance. The National Development Plan 8 (2017–2019) marked the first substantive post-conflict effort to articulate national priorities and achieve the Sustainable Development Goals (SDGs).

This was followed by the National Development Plan 9 (2020–2024). It functioned not only as a development strategy but also as an interim poverty-reduction strategy and as a vehicle for macroeconomic reform. NDP 9 underpinned improvements in public financial management and supported Somalia’s progress towards debt relief under the Heavily Indebted Poor Countries Initiative. The Plan was structured around four pillars: politics, security and rule of law, inclusive economic growth and social development, reflecting an understanding that economic recovery required parallel progress in governance and stability. To strengthen oversight and accountability under the NDP 9, the Ministry of Planning, Investment and Economic Development commissioned the National Integrated Monitoring and Evaluation Framework to provide a unified approach for tracking, assessing and reporting on the implementation of NDP-9 programs, policies and projects across government.

From 2025, Somalia transitions from the NDP cycle to the National Transformation Plan (NTP) (2025–2029), signalling an ambition to move beyond stabilisation towards more transformative development outcomes. The NTP reframes national priorities around governance reform, economic transformation, human capital development and climate resilience. It places stronger emphasis on the role of state institutions, at both federal and subnational levels, in coordinating service delivery, investment and reform. The Plan reflects greater macroeconomic confidence following debt relief and improved engagement with international partners. However, its implementation remains constrained by limited administrative capacity, uneven authority across the federal system and persistent insecurity.

In parallel, the launch of Somalia’s Centennial Vision 2060 introduces a longer-term horizon. Announced following President Hassan Sheikh Mohamud’s re-election in 2022 and formally launched in 2025, the Vision outlines a 35-year strategic trajectory to 2060, the centenary of independence. The Vision aims to steer Somalia towards sustained political stability, stronger economic resilience and broader social inclusion. It is designed to anchor national priorities within a shared long-term framework, reinforce core national values, encourage locally driven solutions, and ensure that reforms and investments remain aligned with enduring national interests.

The credibility of this planning architecture depends on reliable data. Since the collapse of the central government in 1991, Somalia has operated without a coherent and functioning national statistical system. As state institutions disintegrated, so too did the infrastructure for producing and managing official data. The governing statistics law dates from 1970 and no longer reflects Somalia’s federal structure. In practice, data production became fragmented, donor-driven and often undertaken in parallel by non-state actors, with weak coordination across ministries and federal entities.

This prolonged data vacuum constrained evidence-based policymaking. Administrative systems remained underdeveloped, statistical units within ministries were weak or inconsistent and ad hoc surveys substituted for institutionalised data systems. Capacity shortages, limited financing, fragile IT infrastructure and uneven methodological standards further undermined the credibility and comparability of official statistics.

A decisive institutional shift occurred with the enactment of the 2020 Statistics Law, which established the Somalia National Bureau of Statistics as an Independent Government Body and clarified its coordination mandate across the federal system. This legal reset marked the beginning of rebuilding statistical authority as part of broader state reconstruction. The Second National Strategy for the Development of Statistics (2024–2029) consolidates this effort. It focuses on operationalising the new law through regulations and codes of practice, modernising administrative data systems to reduce over-reliance on costly surveys, institutionalising data quality standards and investing in ICT and geospatial infrastructure. It also recognises the political realities of a federal system and seeks to strengthen coordination, harmonisation and trust across institutions. The significance of these reforms extends beyond technical data improvements. Credible statistics are essential for development planning, fiscal management, service delivery and accountability. Without reliable data, national plans cannot be monitored, performance cannot be measured and public trust cannot be built.

The eight sectoral scenarios as well as their relationship to the Current Path and the Combined scenario are explained in the Technical page. Chart 10 summarises the approach.

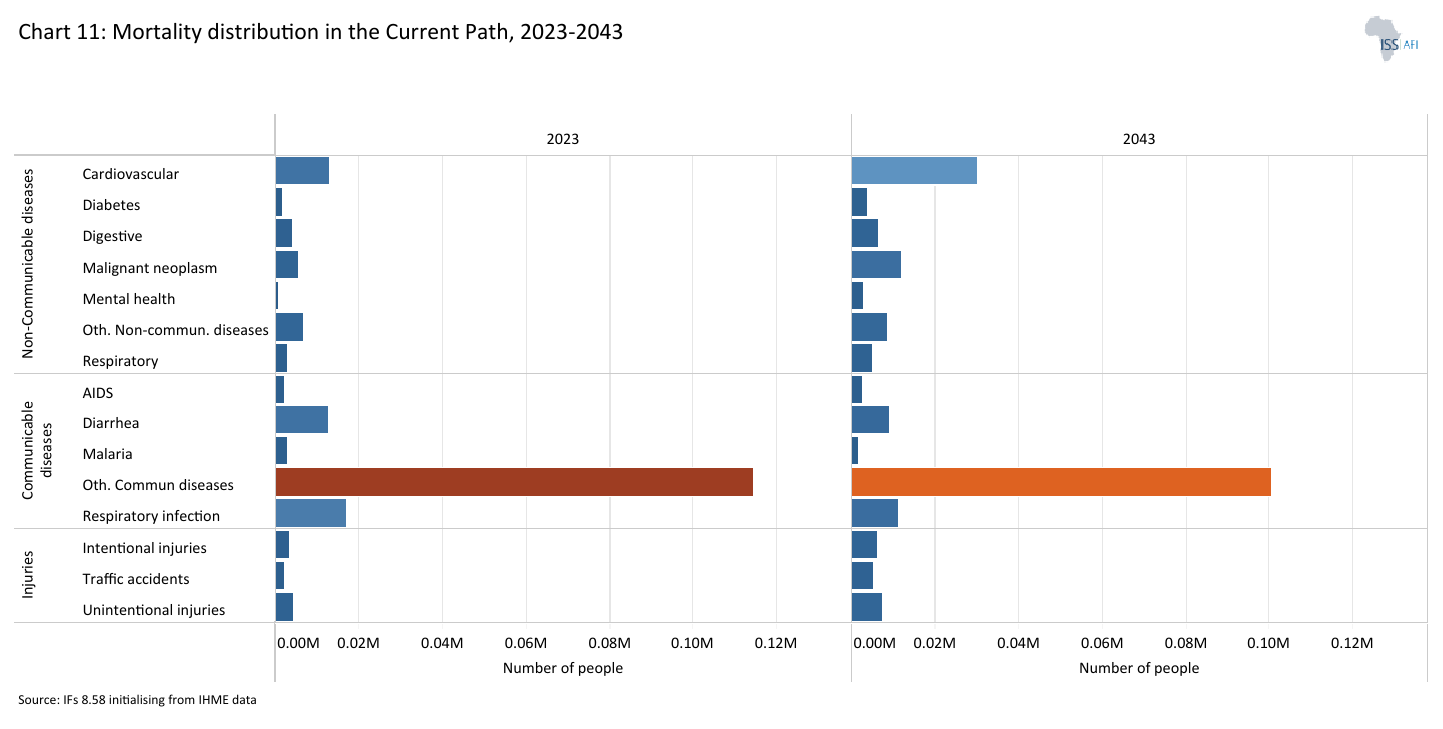

Chart 11 presents the mortality distribution in the Current Path for 2023 and 2043.

The Demographics and Health scenario envisions ambitious improvements in child and maternal mortality rates, enhanced access to modern contraception, and decreased mortality from communicable diseases (e.g., AIDS, diarrhoea, malaria, respiratory infections) and non-communicable diseases (e.g., diabetes), alongside advancements in safe water access and sanitation. This scenario assumes a swift demographic transition, supported by increased investments in health and water, sanitation, and hygiene (WaSH) infrastructure.

Visit the themes on Demographics and Health/WaSH for more details on the scenario structure and interventions.

Somalia’s health outcomes remain among the weakest globally, with high maternal and child mortality and widespread malnutrition. Access to basic care is limited for large segments of the population, and health service provision is overwhelmingly dependent on external assistance, with donor financing accounting for around 95% of total health expenditure. This heavy reliance on external funding leaves the system highly exposed to external shocks and geopolitical factors, and recent reductions in international support have placed growing pressure on the continuity and quality of essential health and nutrition services. A 2025 survey by the Somali NGO Consortium highlights the scale of disruption caused by the suspension of US aid to Somalia. More than 60% of NGOs operating in the country reported receiving stop-work orders. The suspension has led to widespread interruptions across critical sectors, including health, nutrition, WASH, food security, education and protection, alongside staff layoffs and unpaid leave.

Additionally, the health workforce is critically overstretched, with a severe shortage of trained professionals and pronounced urban–rural imbalances driven by insecurity, internal migration and outward emigration. Health facilities are unevenly distributed and often poorly equipped, with many facilities non-operational or failing to meet basic infection prevention standards. These weaknesses are compounded by persistent shortages of medicines and supplies, alongside procurement and transport challenges that are further exacerbated by insecurity.

Within this context, the mortality profile in 2023 was dominated by communicable diseases, reflecting the high prevalence of preventable and treatable conditions in a setting characterised by weak health system capacity and limited access to safely managed water and sanitation. Conflict, displacement and overcrowded living conditions further amplify transmission risks and disrupt access to preventive and curative care. Routine immunisation coverage in Somalia was low for many years, remaining below 50% for extended periods. More recent estimates, however, indicate significant progress, with around 70% of children fully vaccinated by 2024.

Looking ahead, communicable diseases are projected to remain the leading cause of mortality through to 2043, even as deaths from non-communicable diseases (NCDs) increase markedly. In 2023, the leading causes of death were “other communicable diseases” including respiratory infections, cardiovascular diseases, diarrhoeal diseases and cancers. By 2043, other communicable diseases will remain the leading cause, while cardiovascular diseases and cancers rise to second and third place, respectively, overtaking respiratory infections and diarrhoeal diseases, which fall to fourth and fifth.

These shifts reflect an intensifying dual burden of disease, in which persistent infectious mortality coexists with a growing challenge of chronic conditions, placing increasing strain on an already fragile health system. Managing this transition will require sustained efforts to reduce preventable infectious disease deaths while simultaneously strengthening the system’s capacity to detect and treat NCDs.

In the near term, reducing infectious disease mortality remains critical. Priority interventions include expanding access to basic and preventive services, strengthening routine immunisation and maternal and child health programs, improving infection prevention and control standards in health facilities, and reinforcing community-based health delivery in displacement-affected and hard-to-reach areas. Sustained investment in WaSH services, nutrition support and early disease detection will also be key to reducing preventable deaths in a context of recurrent shocks and population displacement. Without progress on these fronts, gains in health outcomes are likely to remain fragile.

At the same time, the rising burden of NCDs will require targeted health system strengthening. Priorities include improving access to early diagnosis and basic screening, progressively integrating NCD prevention and treatment into primary health care, and strengthening disease surveillance and health information systems to support planning and resource allocation. Complementary public health efforts, including addressing malnutrition, reducing tobacco use and promoting physical activity, will also be important in moderating the long-term growth of NCDs.

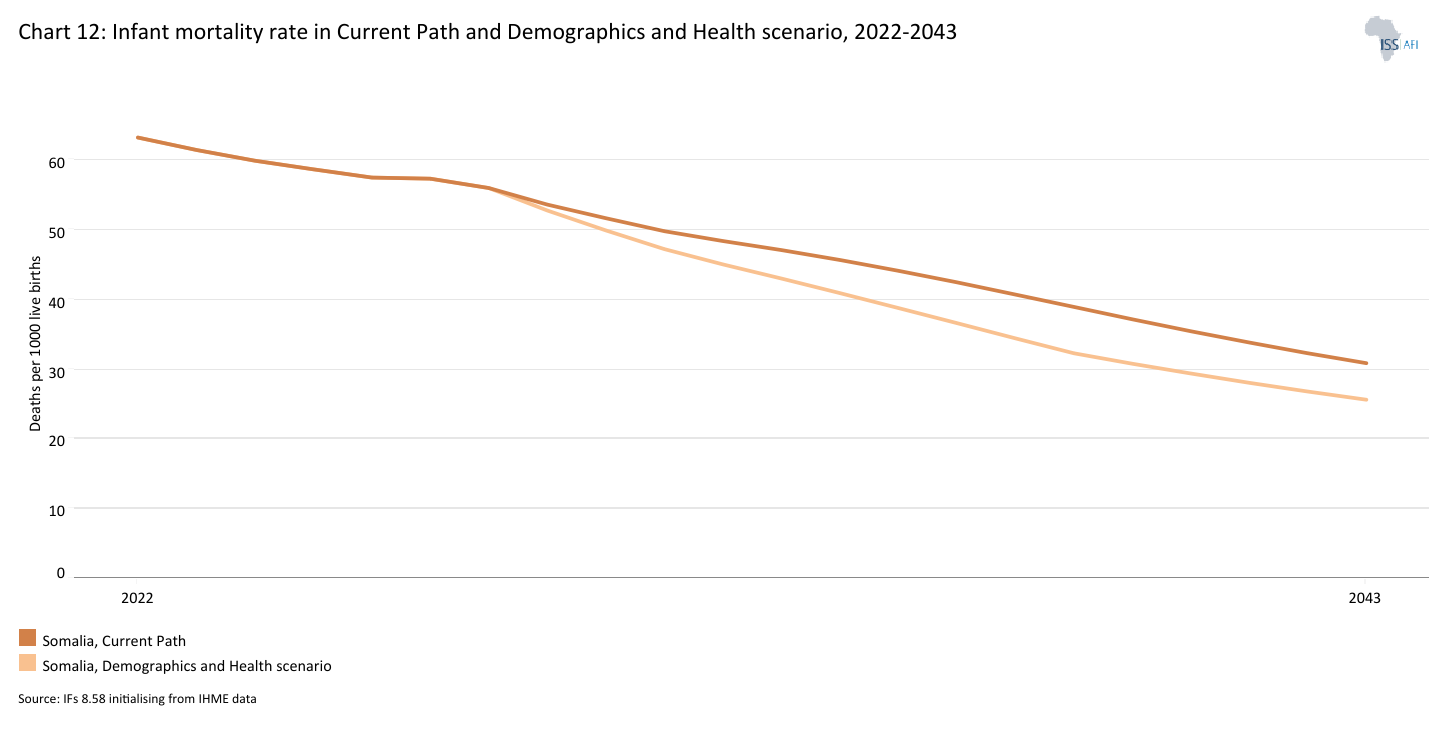

Chart 12 presents the infant mortality rate in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The infant mortality rate is the probability of a child born in a specific year dying before reaching the age of one. It measures the child-born survival rate and reflects the social, economic and environmental conditions in which children live, including their health care. It is measured as the number of infant deaths per 1 000 live births and is an important marker of a country's overall health system quality.

Somalia continues to face extremely high levels of maternal and newborn mortality. UNICEF 2019 estimates indicate that around four in every 100 children die within the first month of life, and nearly eight in 100 do not survive to their first birthday. Approximately one in 20 women of reproductive age dies each year from complications related to pregnancy or childbirth.

Limited access to, and utilisation of, maternal and newborn health services contribute significantly to these outcomes. The 2020 Somalia Demographic and Health Survey shows that only about one-third of births take place with the assistance of skilled health personnel, and a similar share of women receive antenatal care from a trained provider during their most recent pregnancy. Postnatal care coverage is particularly weak, with nearly nine in ten mothers not receiving a check-up within the first two days after childbirth. Service availability is also uneven: a 2016 national assessment found that Basic Emergency Obstetric and Neonatal Care services were available in fewer than half of urban health facilities and only one-fifth of rural facilities. Essential Newborn Care was offered in less than a third of urban facilities and just over one in ten rural facilities.

In 2023, Somalia’s infant mortality rate stood at 62 deaths per 1 000 live births, more than double the Sustainable Development Goal target of fewer than 25 deaths per 1 000 live births by 2030. On the Current Path, the rate is projected to decline to 31 deaths per 1 000 live births in 2043, indicating substantial improvement but still falling short of the global benchmark. Under the Demographics and Health scenario, however, infant mortality could fall further to 26 deaths per 1 000 live births, bringing the country close to achieving the SDG target.

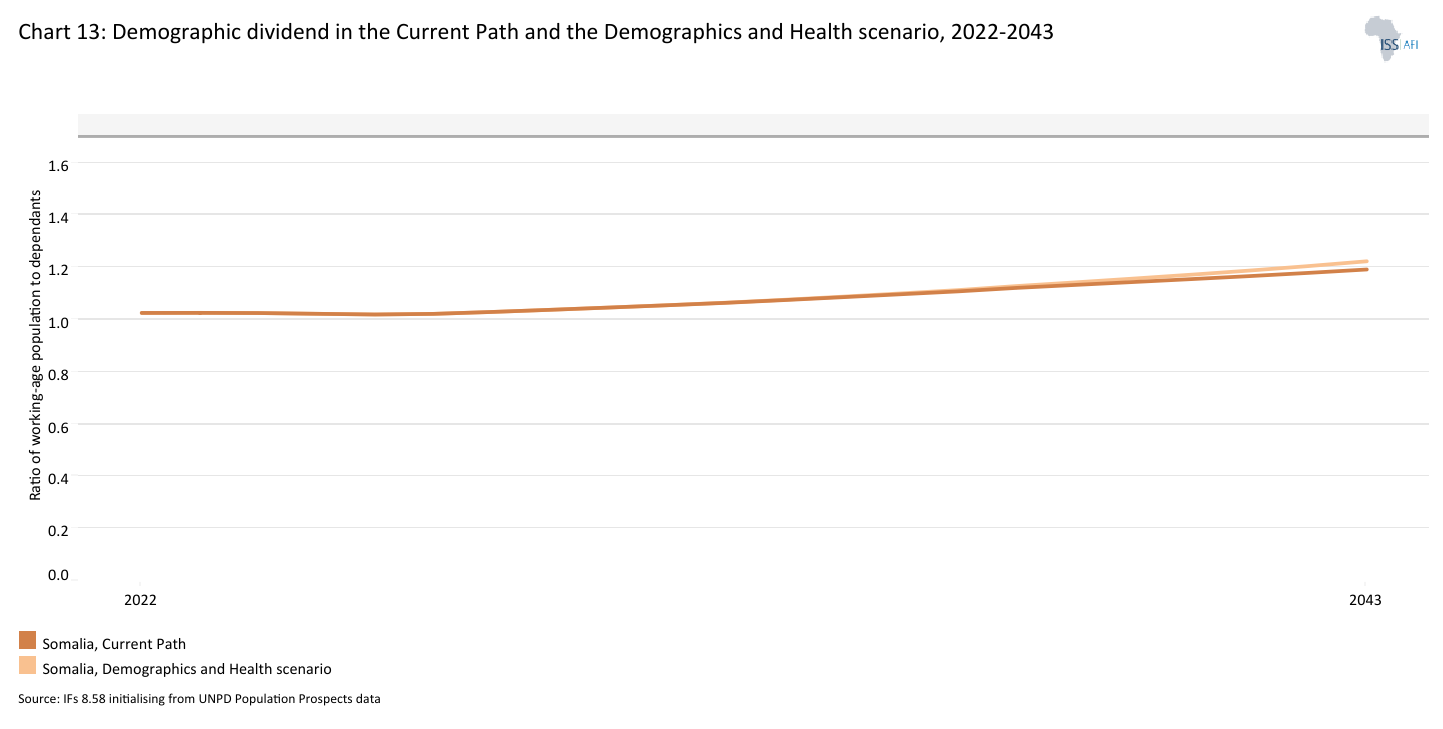

Chart 13 presents the demographic dividend in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

The demographic dividend, which refers to economic growth resulting from changes in a country's population structure, is influenced by factors such as declining fertility rates and improvements in health and education. With fewer dependants (children under 15 and adults over 65) to support, families and governments can allocate more resources to savings, education, infrastructure and economic development, driving accelerated growth.

The demographic dividend is attained when the ratio of working-age persons (15–64 years of age) to dependants is at least 1.7:1. However, attaining the demographic dividend does not automatically translate into economic growth. Realising the potential demographic dividend depends on simultaneous policy-driven improvements in employment, governance and basic service provision.

In Somalia’s case, persistently high fertility and rapid population growth mean that this transition will unfold slowly under the Current Path. In 2023, the ratio of working-age individuals to dependants stood at approximately 1.03, indicating that for every 1 dependent person (children under 15 or elderly over 65), there were approximately 1.02 people of working age (15–64). This implies that the economic burden of supporting non-workers was relatively low, which is a key requirement for economic acceleration. Although fertility is projected to decline over time, the reduction will be slow. As a result, the dependency burden will ease only marginally, with the demographic dividend ratio rising to 1.19 working-age persons per dependant by 2043 under the Current Path, and slightly higher to 1.22 under the Demographics and Health scenario.

Even under the Demographics and Health scenario, which reduces infant mortality, expands access to family planning and strengthens overall health outcomes, improvements in the age structure remain incremental. Demographic shifts operate over decades, and the large youth cohorts already born will continue to move through the dependency cycle before substantially altering the overall ratio.

Somalia is projected to reach a ratio of 1.7 working-age persons per dependant only towards the end of the 2060s, more than a decade later than the projected average of 2052 for low-income Africa. This delayed window has significant implications. For the next several decades, demographic momentum will continue to exert pressure on public services, education systems and labour markets, even as gradual gains in human capital materialise.

The policy implication is clear. Somalia cannot rely solely on demographic change to unlock growth and must balance immediate priorities with sustained long-term investments. Accelerating fertility decline through expanded access to family planning and greater investment in girls’ education is essential to reducing dependency pressures. At the same time, the country must manage immediate strains on employment, service delivery and human capital while advancing longer-term structural transformation, including stronger institutions, economic diversification and broader inclusion.

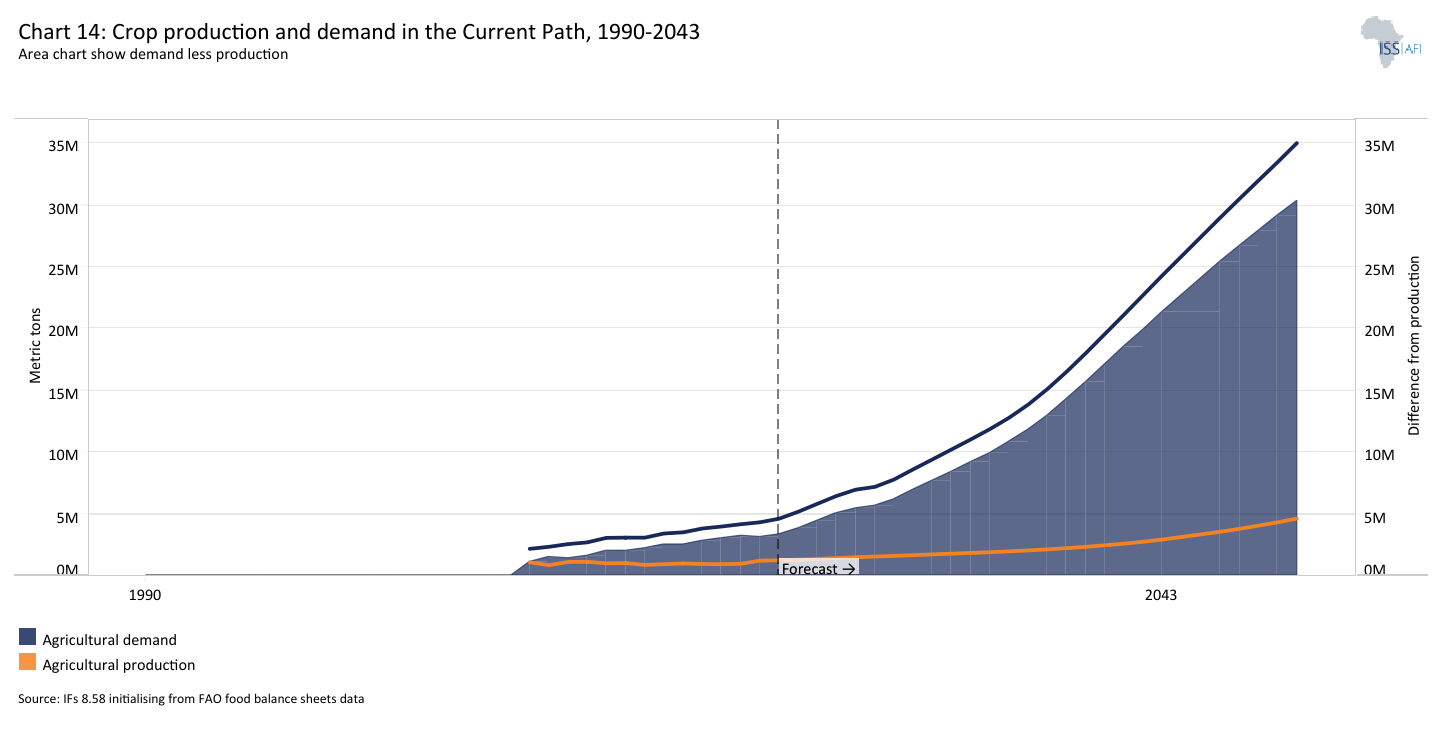

Chart 14 presents crop production and demand in the Current Path from 1990 to 2043.

The Agriculture scenario envisions an agricultural revolution that ensures food security through ambitious yet feasible increases in yields per hectare, driven by improved management, seed, fertiliser technology and expanded irrigation. Efforts to reduce food loss and waste are emphasised, with increased calorie consumption as an indicator of self-sufficiency and prioritising it over food exports. Additionally, enhanced forest protection demonstrates a commitment to sustainable land-use practices.

Visit the theme on Agriculture for our conceptualisation and details on the scenario structure and interventions.

A thriving agriculture sector is crucial to long-term peace and development in Somalia. Crop and livestock production together account for more than 70% of GDP and employ more than 80% of the labour force. Within this, livestock is the dominant subsector, contributing roughly 45% of GDP and underpinning around 80% of foreign currency earnings. An estimated 70% of Somalis depend directly or indirectly on livestock-related activities along the value chain, whether through herding, trading, processing or transport.

Despite its potential, the crop sector underperforms relative to its pre-conflict levels and its current potential. The country has an estimated 8.9 million hectares of arable land, significant groundwater reserves and three major river systems, the Shabelle, Jubba and Dawa, which together stretch roughly 2 500 kilometres. Agro-pastoral systems dominate much of rural life, particularly in the fertile river valleys of the south. Agricultural production is concentrated in southern Somalia, where soils are relatively fertile and river-based irrigation is available.

Maize is one of the country’s most important staple crops. It is primarily cultivated in Lower Shabelle and serves as a key source of household nutrition and livestock feed. However, domestic maize production remains far below national requirements. Yields are relatively low due to limited irrigation infrastructure, erratic rainfall, poor access to improved seeds and fertilisers, and high post-harvest losses. Annual output is estimated at 75 000 to 80 000 metric tons, while demand exceeds 1.2 million tons.

Fodder production remains underdeveloped but a vital part of Somalia’s livestock economy, which is the country’s largest contributor to GDP. However, a feed deficit of around 34%, driven by recurring droughts, overgrazing and rangeland degradation, continues to constrain productivity and raise livestock mortality during dry periods. Expanding the cultivation of drought-tolerant fodder crops, particularly in irrigated areas of Lower Juba and Lower Shebelle, offers significant scope to strengthen resilience and improve output.

Environmental degradation represents a significant constraint on Somalia’s development trajectory. The causes of degradation are estimated at 38% of the land area affected by biological decline, and a further 34% by water-driven soil erosion, meaning that more than 70% of already degraded land is under significant ecological stress. Only about 14% of the overall land remains unaffected by degradation. These patterns reflect the country’s heavy reliance on natural resources and its growing vulnerability to degradation driven by overgrazing, deforestation and unsustainable land use. Somalia has taken constructive steps in response, including its commitment under SDG 15 to achieve land degradation neutrality, alongside reforestation and soil conservation initiatives. Stronger land-use planning, improved environmental data systems, consistent monitoring and better coordination across sectors and levels of government are essential. Without strengthened land governance and sustained resource management, ecological decline will continue to erode food security, slow poverty reduction, and heighten risks to long-term stability.

Climate change is compounding Somalia’s structural vulnerabilities and intensifying pressure on its food systems. Longer and more frequent dry spells are reducing water availability, degrading rangelands and causing repeated livestock and crop losses. Between 2021 and 2023, the country experienced its worst drought in nearly four decades, following successive failed rainy seasons. The shock affected more than half the population, depleted key water sources, destroyed pasture, caused large-scale livestock losses and triggered widespread displacement. Recent initiatives, such as the Ugbaad climate-resilient agriculture program, signal a shift towards more adaptive water management, drought-resistant inputs and ecosystem restoration. While these interventions are important, their impact will depend on scale, coordination and sustained implementation.

These climate shocks interact with conflict, economic fragility and environmental degradation to disrupt production and weaken resilience. As a result, food insecurity remains chronic. In 2023, around 1.9 million people in Somalia were facing severe levels of food insecurity, classified as crisis or worse under the Integrated Food Security Phase (IPC) classification, the highest number recorded since the Global Report on Food Crises began in 2016. Acute malnutrition also remained alarmingly high, with an estimated 1.8 million children under five affected.

Against this backdrop, crop demand will rise steeply under the Current Path from 4.63 million metric tons in 2023 to 24.35 million metric tons by 2043, mainly due to rapid population growth. Production will increase, but at a far slower rate, from 1.26 to 2.94 million metric tons in the same period. Accordingly, the crop production deficit will widen from roughly 3.37 million metric tons to 21.41 million metric tons. This trajectory depicts severe food insecurity and tends to have negative implications for macroeconomic stability.

Chart 15 presents the import dependence in the Current Path and the Agriculture scenario, from 2020 to 2043.