Bargaining on birthrights: the real resource race for Africa’s future

Africa’s land is becoming central to global competition over food, finance, carbon, data and luxury property, raising new sovereignty risks.

It is no secret that the African continent’s greatest assets are its real resources: its people, oceans and land.

The fundamental value of real resources is being remembered, by markets and governments alike, as conflicts in the Middle East and the Ukraine, alongside the insatiable demands of the artificial intelligence economy, remind investors and politicians that there is no digital or financial economy without energy, water and food—the necessities that power the bits, bytes and labour required to grow GDP numbers and stock market prices.

It is therefore no surprise that real resource prices have soared in recent months. Energy prices are projected to increase by 24% in 2026, gold and silver prices are setting records and fertiliser prices are set to surge by 31% this year.

Less reported, but just as important, is the steadily growing demand for African land to fuel data centres, food production, luxury escapes and ambitious carbon offsets.

This point warrants closer attention. As the prices of necessities and raw commodities—be they crops, minerals, oil or land—increase, so does the pressure and incentive to sell. Hungry populations need to be fed, and ambitious development projects require liquid capital.

Global markets, flush with stronger currencies and deeper pockets, bring demand ready to meet and match supply. Trade can be beneficial to both parties when they negotiate on equal footing. However, in a global economy where a few strong nations and regions can expand money supply with little to no consequence, while weaker currencies that attempt to keep up with the same monetary policy tricks suffer inflation or hyperinflation, a fundamental trade imbalance emerges and bargaining power is uneven from the start: soft money can buy hard assets at a significant discount. Seigniorage profits enable the holders of newly created money to purchase goods and services at prices below their true market-clearing value before sticky prices adjust and catch up with the adjusted monetary supply.

Seigniorage profits enable the holders of newly created money to purchase goods and services at prices below their true market-clearing value

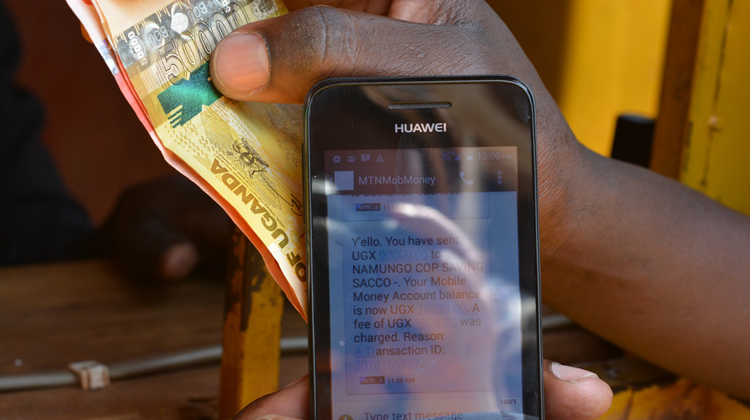

In the last seven months alone, the dollar supply has grown by US$7 trillion. This gives dollar holders a significant advantage in purchasing power in an increasingly competitive commodity market.

At the same time, African public debt repayments to foreign lenders are set to hit a “wall” as they exceed US$ 90 billion in 2026, as both Eurobonds and obligations to Chinese creditors come due. These repayments are due amid soaring debt repayment costs driven by the global commodity crunch and intensifying ground warfare conflicts, which are choking physical and fiscal economic flows.

This unequal purchasing-power dynamic becomes more acute when applied to the non-renewable subset of commodities that can only be sold once, especially land: farmland and mining rights, but increasingly also habitable land and housing.

Land, birthrights and ownership are key to Africa’s sovereign future. Land disputes and competition are global issues, central to generational, national, cultural and class conflicts. Africa, however, due to its yet-to-be-developed potential, is at the heart of the future of this conflict. According to the African Development Bank, 65% of the world's remaining uncultivated, arable land is located in Africa, making the continent a target for international capital acquisition—and land (or other hard asset) “grabbing”.

This phenomenon—African land being sold at seigniorage discount under duress—is playing out through different channels. The concern is not foreign investment itself, but the cumulative transfer of control over finite assets under unequal bargaining conditions.

Debt demands show how financial pressure can become a sovereignty risk. As unsustainable debt repayments come due, international creditors may seek collateral in the form of rights to infrastructure, or revenues therefrom. This could result in the loss of strategic sovereignty and future income streams for African nations.

Farms and food security create another pressure point. As food security and supply-chain sovereignty become national priorities worldwide, it is concerning that foreign investors are estimated to have acquired or leased roughly 560 000 km² of farmland in Africa since 2000, often through opaque deals criticised for their potential exploitation of local communities. Africa accounts for 47% of the total land area owned by foreign owners worldwide (followed by Asia at 33%), suggesting that in many places, physical colonisation has continued through fiscal colonisation.

Green grabs add a further layer to land competition. The new wave of debt-for-nature swaps and carbon offset schemes, which may involve foreign firms and government creditors taking stewardship or ownership of pristine African land, in exchange for debt forgiveness or capital injections, is facing criticism for what this may actually mean for African communities: lost ownership and usage rights over millions of hectares of their own land. In Kenya alone, land-based “voluntary” carbon projects cover over 5.4 million hectares, an area almost equivalent to the country’s total arable land.

Data demand is also beginning to reshape the land question. The race for artificial intelligence “compute” for nations and corporations is driving demand for prime land worldwide. Africa, with its relatively cheap and abundant land, is a target for data centre acquisitions. In South Africa, a single US-owned firm, Equinix, is buying ZAR890 million worth of land to build data campuses, an early signal of a possible trend of foreign ownership of both physical land and digital power within African borders.

Luxury land markets bring the same dynamic into cities and tourism destinations. Prime African property in sought-after cities and tourism destinations remains relatively cheap for stronger-currency nationals and corporations. In Cape Town, South Africa, foreign buyers now account for over 40% of property purchases above ZAR10 million, and up to 70% of all property purchases in some suburbs. In Kenya, communities and wildlife have been bought out and reportedly displaced by foreign hotel groups, while a 520-acre luxury Israeli-owned residential estate has raised further debate. In Zimbabwe, Chinese buyers are reshaping Harare’s property market. These trends raise substantial concerns about economic equality, displacement and social stability for residents.

Policymakers should thoroughly weigh the cumulative and compounding impact of individual transactions on future national and continental sovereignty

Together, these trends flash a warning about the long-term consequences of selling non-renewable, finite birthrights to foreign interests to meet short-term demands. Policymakers should thoroughly weigh the cumulative and compounding impact of individual transactions on future national and continental sovereignty. This requires greater transparency around land deals, stronger safeguards for community rights and a clearer distinction between short-term liquidity and long-term strategic control.

Image: GDJ/Pixabay

Republication of our Africa Tomorrow articles is only with permission. Contact us for any enquiries.