Djibouti

Djibouti

Feedback welcome

Our aim is to use the best data to inform our analysis. See our Technical page for information on the IFs forecasting platform. We appreciate your help and references for improvements via our feedback form.

This report analyses Djibouti’s current development path and prospects, examining how various sectoral interventions could shape the country’s economic and social landscape through to 2043, the end of the third ten-year implementation plan of the African Union's Agenda 2063. The analysis is grounded in scenario modelling and explores eight key sectors. In addition to evaluating the effects of each sectoral scenario individually, the report assesses the combined impact of these interventions on Djibouti’s long-term growth and development trajectory. The report concludes by summarising the key findings and offering policy insights to support Djibouti in pursuing a more inclusive, resilient and sustainable future. It underscores the importance of coordinated, multi-sectoral reforms to unlock the country’s long-term economic and social potential.

Visit the Technical section for additional information on the International Futures (IFs) modelling platform, which serves as the analytical foundation for this report's scenario simulations.

Executive Summary

This page begins with an introductory assessment of the country’s context, examining current population distribution, social structure, climate and topography.

- Djibouti is a small, lower-middle-income country located at a strategic maritime chokepoint in the Horn of Africa, with development anchored in its role as a regional logistics and trade hub. The country is highly urbanised, with over 60% of the population concentrated in Djibouti City, and faces severe climate and water constraints.

The introduction is followed by an analysis of the Current Path for Djibouti, which informs the country’s likely baseline trajectory to 2043. It is based on prevailing macroeconomic factors and assumes that no major shocks will occur in a ‘business-as-usual’ future.

- Djibouti’s population is transitioning toward a working-age-dominant structure, creating potential for a demographic dividend, contingent on job creation and skills development. The total population will grow from approximately 1.17 million people in 2024 to almost 1.5 million people by 2043.

- Urbanisation is nearing saturation, rising modestly from 79% in 2024 to 80.5% by 2043, with future pressure driven by absolute urban population growth rather than shifts in rural-urban migration.

- Gross domestic product (GDP) at market exchange rates (MER) will grow from US$4.25 billion in 2024 to US$13.13 billion by 2043 (6.1% annually), below the 8–10% target set in Vision 2035.

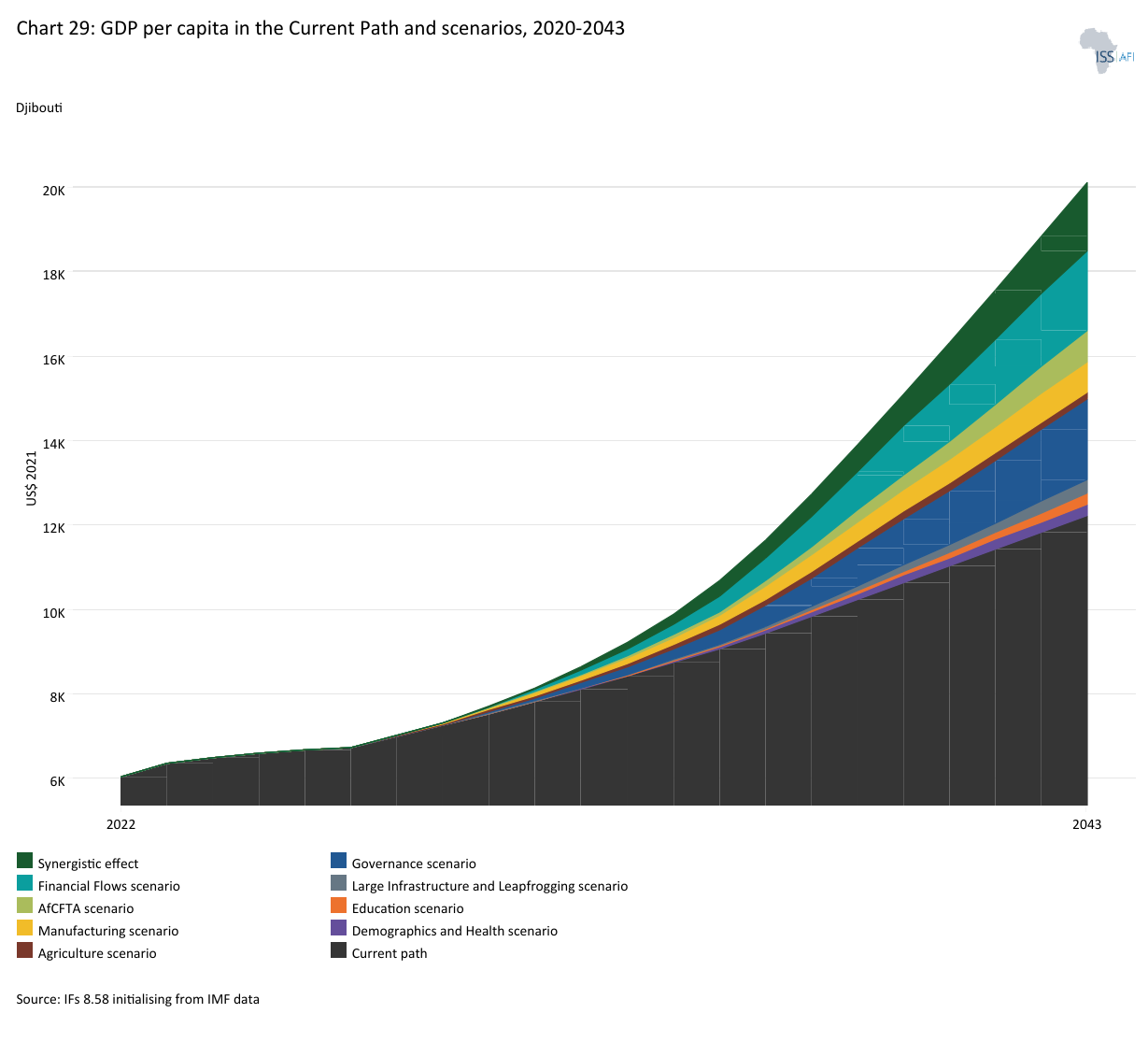

- GDP per capita in purchasing power parity (PPP) will nearly double to US$12 220 by 2043, but will remain insufficient to meet the Vision 2035 target of tripling income per capita by 2035.

- Djibouti’s Current Path suggests a gradual but meaningful reduction in informality over the 2024-2043 period, with the informal share of GDP falling from 22.4% to 18% and informal employment from 36.6% to 28.2%. Reducing informality is not only a labour issue, but central to fiscal sustainability and productivity growth.

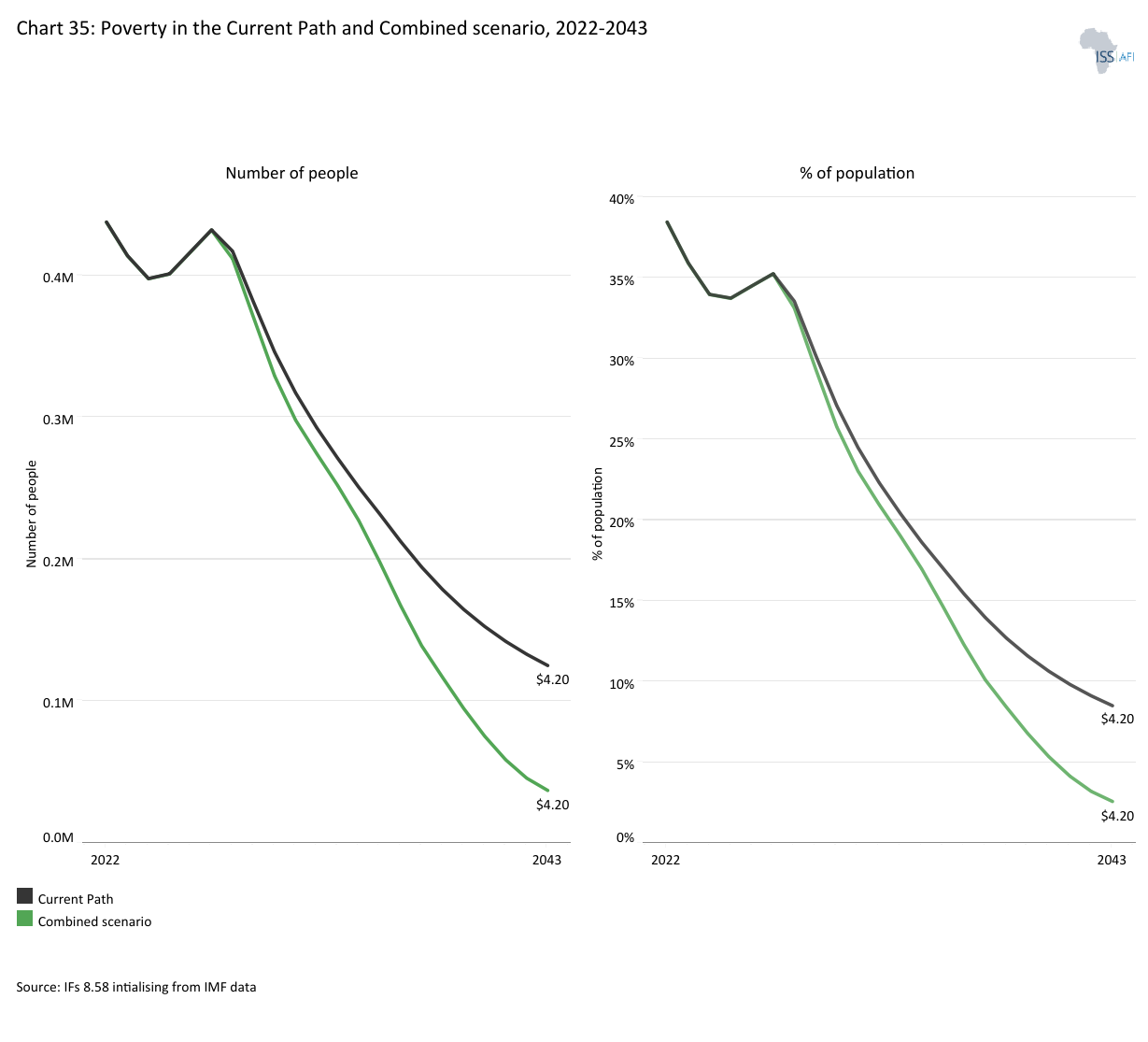

- Poverty declines significantly, reaching 3.1% at the US$3.00 line and about 8.5% at the US$4.20 line by 2043, though risks will remain from debt, climate stress and corridor dependence.

- Djibouti’s development strategy is anchored in Vision 2035, which is built around governance, economic diversification, private-sector investment, human capital and regional integration.

The next section compares progress on the Current Path with eight sectoral scenarios . These are Demographics and Health; Agriculture; Education; Manufacturing; the African Continental Free Trade Area (AfCFTA); Large Infrastructure and Leapfrogging; Financial Flows; and Governance. Each scenario is benchmarked to present an ambitious but reasonable aspiration in that sector, comparing Djibouti with other countries at similar levels of development and characteristics.

- The Demographics and Health scenario will accelerate progress toward SDG 3.2 targets, reducing infant mortality to 6.8 per 1 000 by 2043, which represents about 2.8 fewer infant deaths per 1 000 live births than the Current Path forecast.

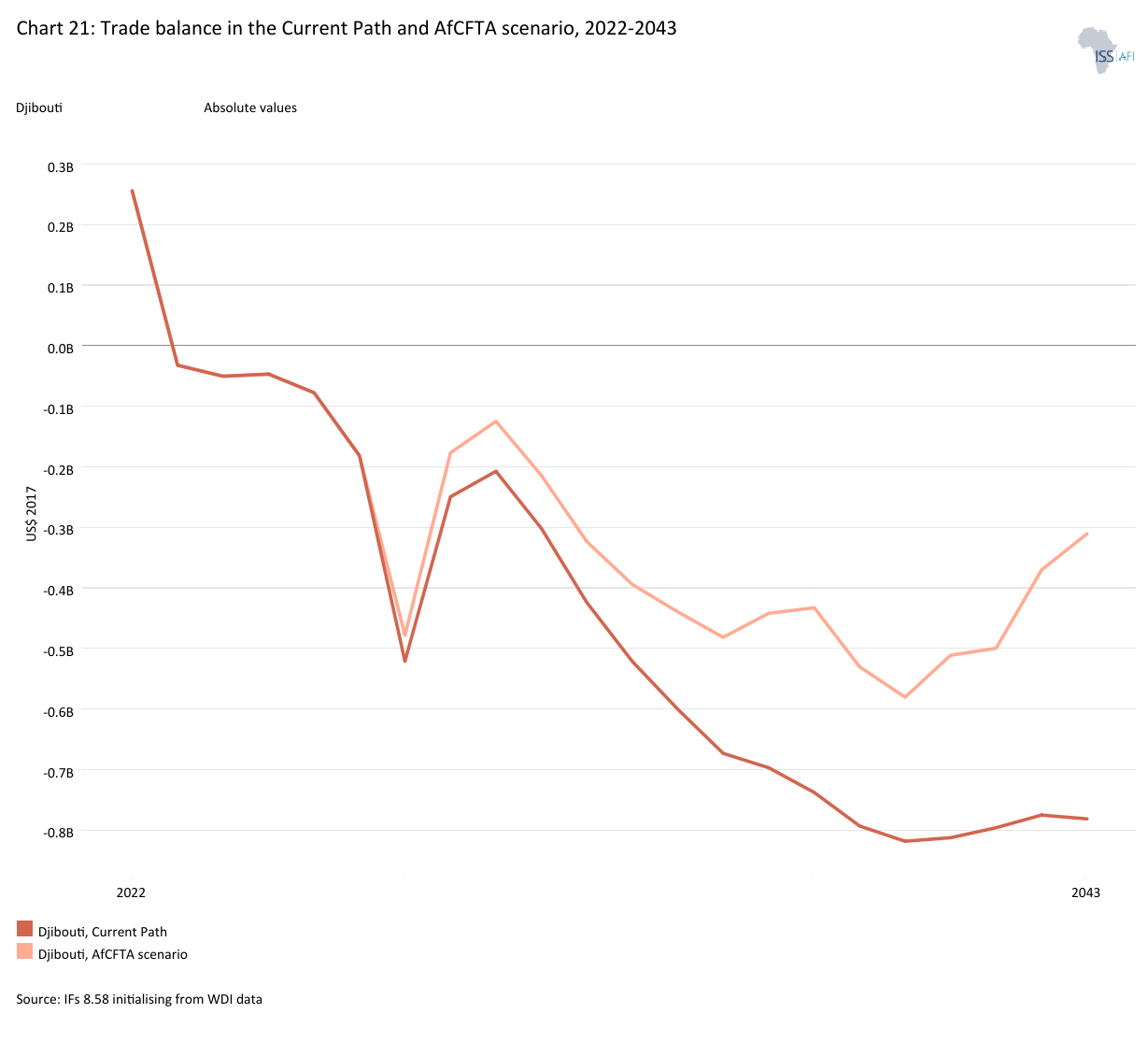

- Improvements in agriculture under the Agriculture scenario will reduce the trade deficit from 11.8% of GDP in 2024 to 7.1% by 2043. However, structural dependence on imports due to climate, land and water constraints remains. This deficit will be 0.1 percentage points lower than the Current Path forecast.

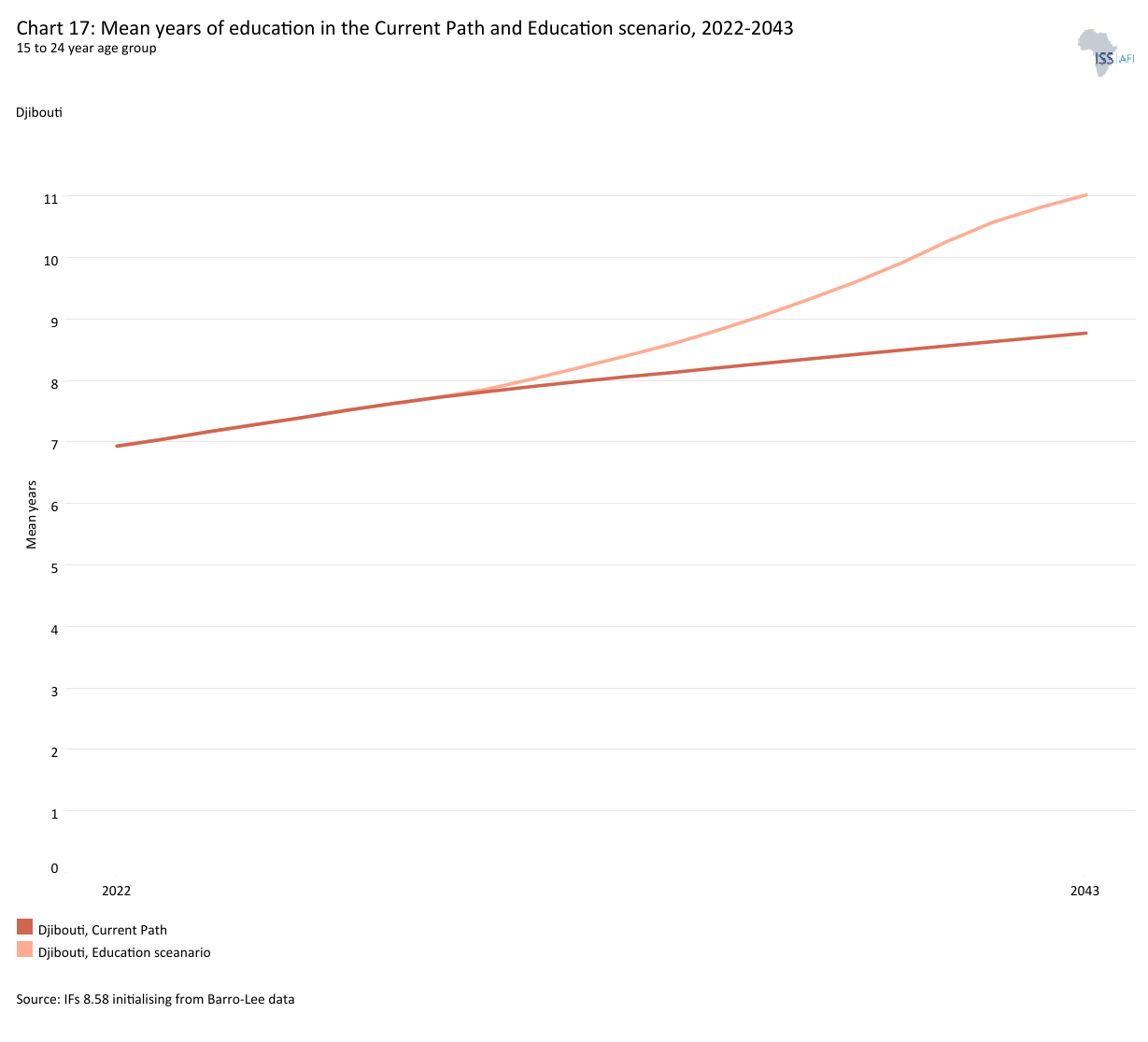

- The Education scenario suggests that by 2043, the average years of schooling for individuals aged 15 to 24 will increase to about 11 years, 2.2 years higher than in the Current Path. This improvement indicates that more young adults are nearing completion of upper-secondary education and pursuing tertiary education, which will boost future workforce productivity.

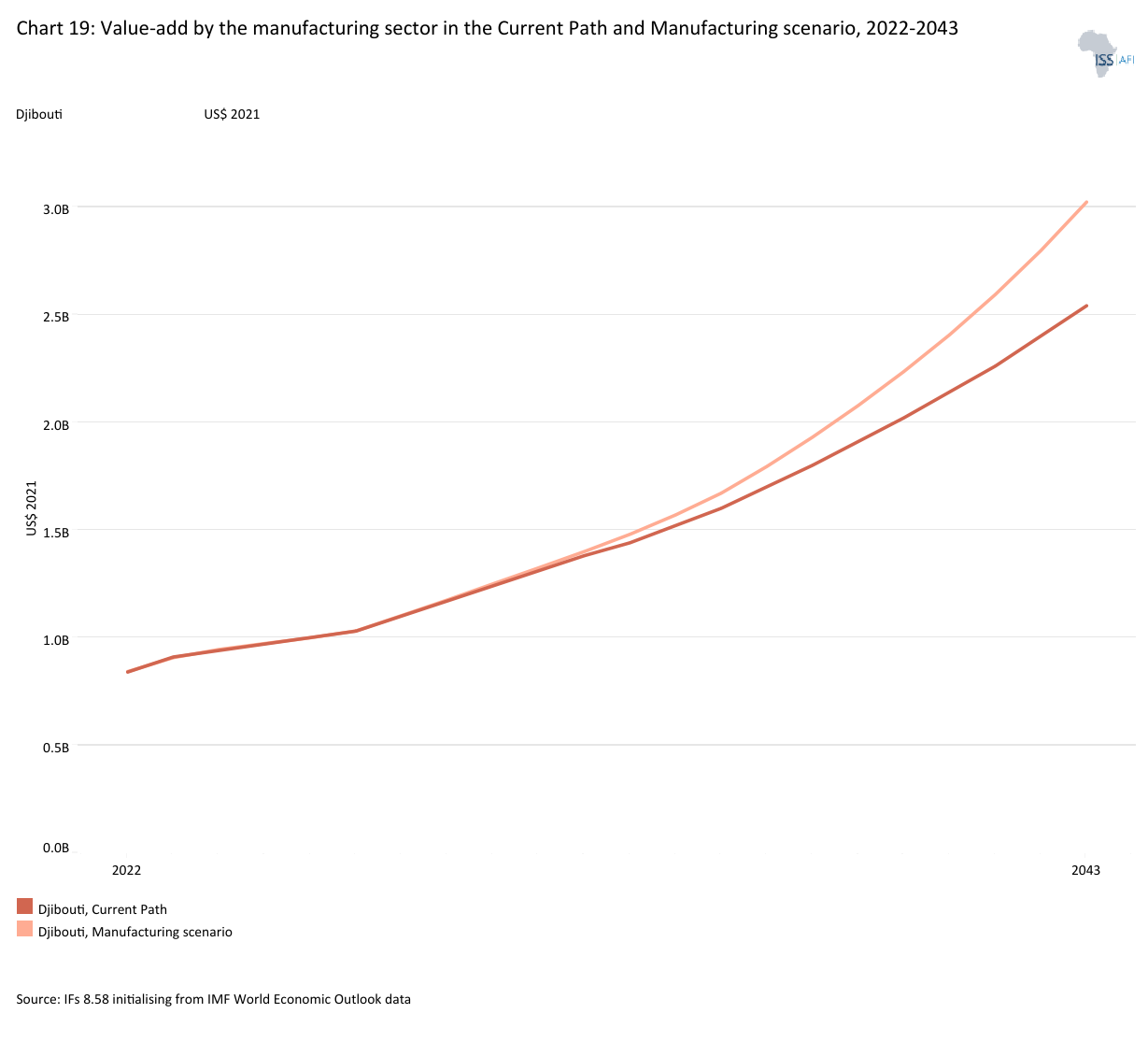

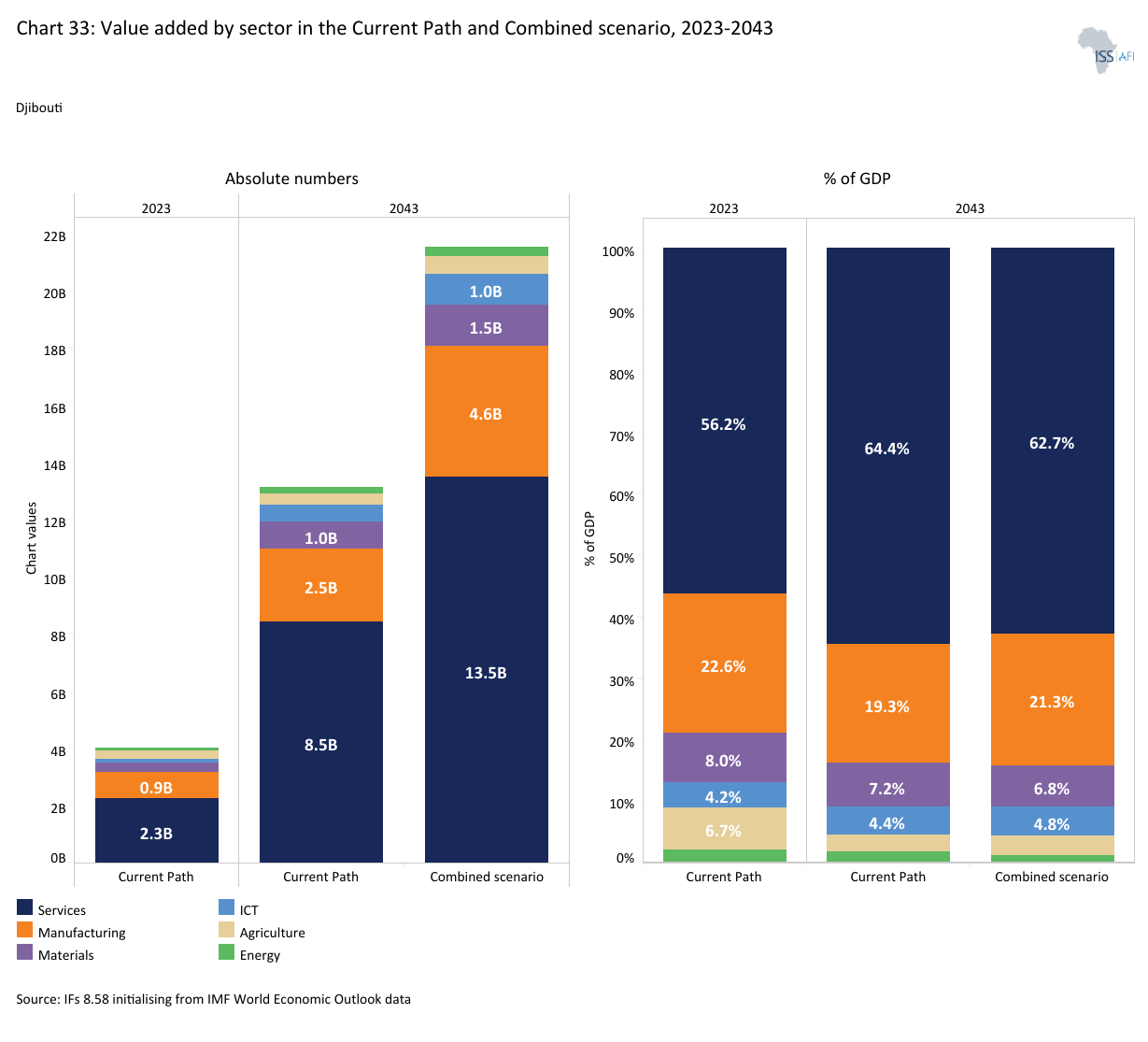

- In the Manufacturing scenario, the sector’s growth will modestly shift the economic structure toward industry, though services will remain dominant. By 2043, only the manufacturing and materials sectors will have higher GDP shares than in the Current Path. However, in absolute terms, every sector will be larger under the Manufacturing scenario relative to the Current Path, but manufacturing will grow the most.

- AfCFTA implementation will boost export growth, narrowing the 2043 trade deficit forecast from 5.9% of GDP under the Current Path to around 2.2%. Structural constraints will limit full gains.

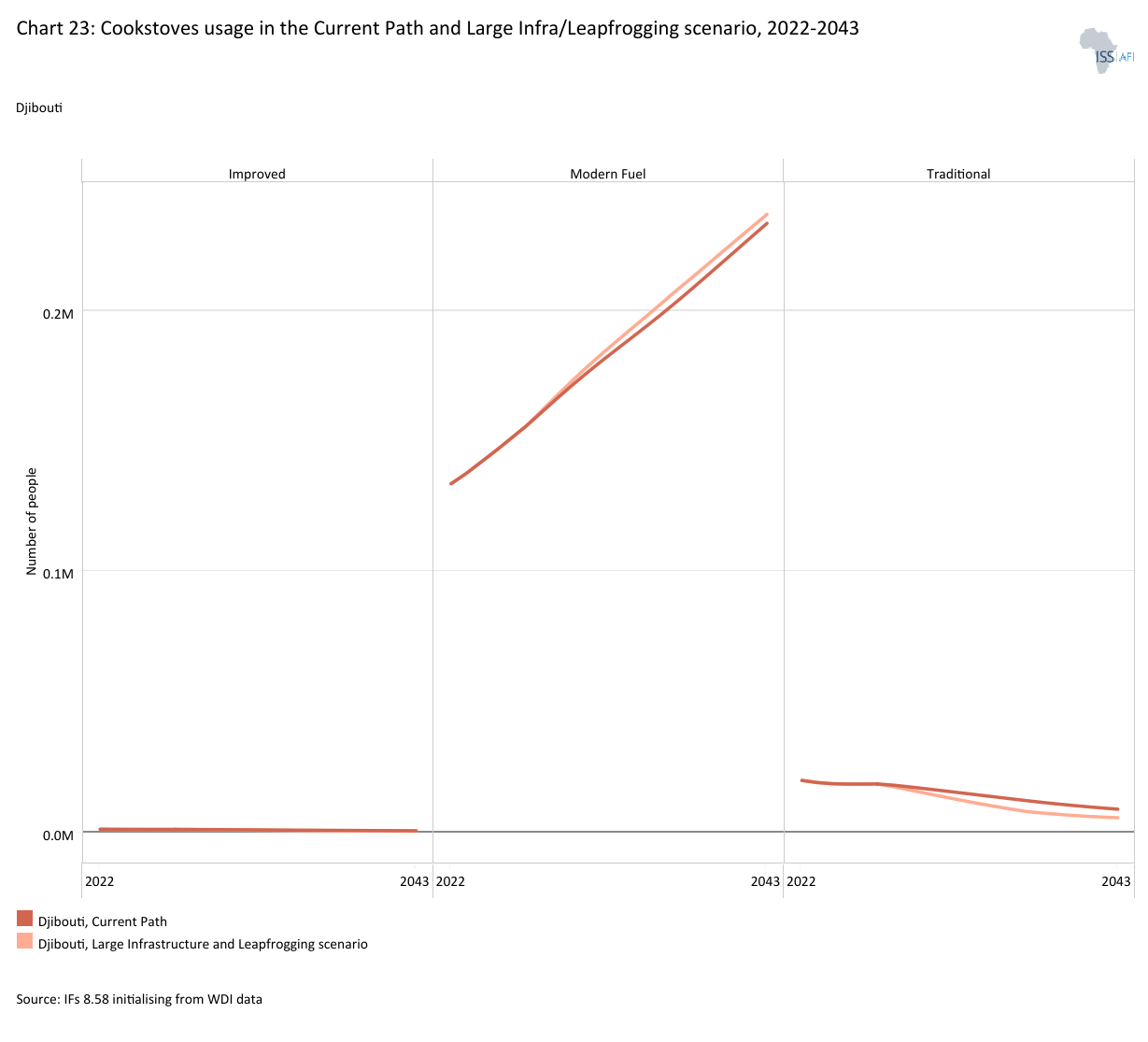

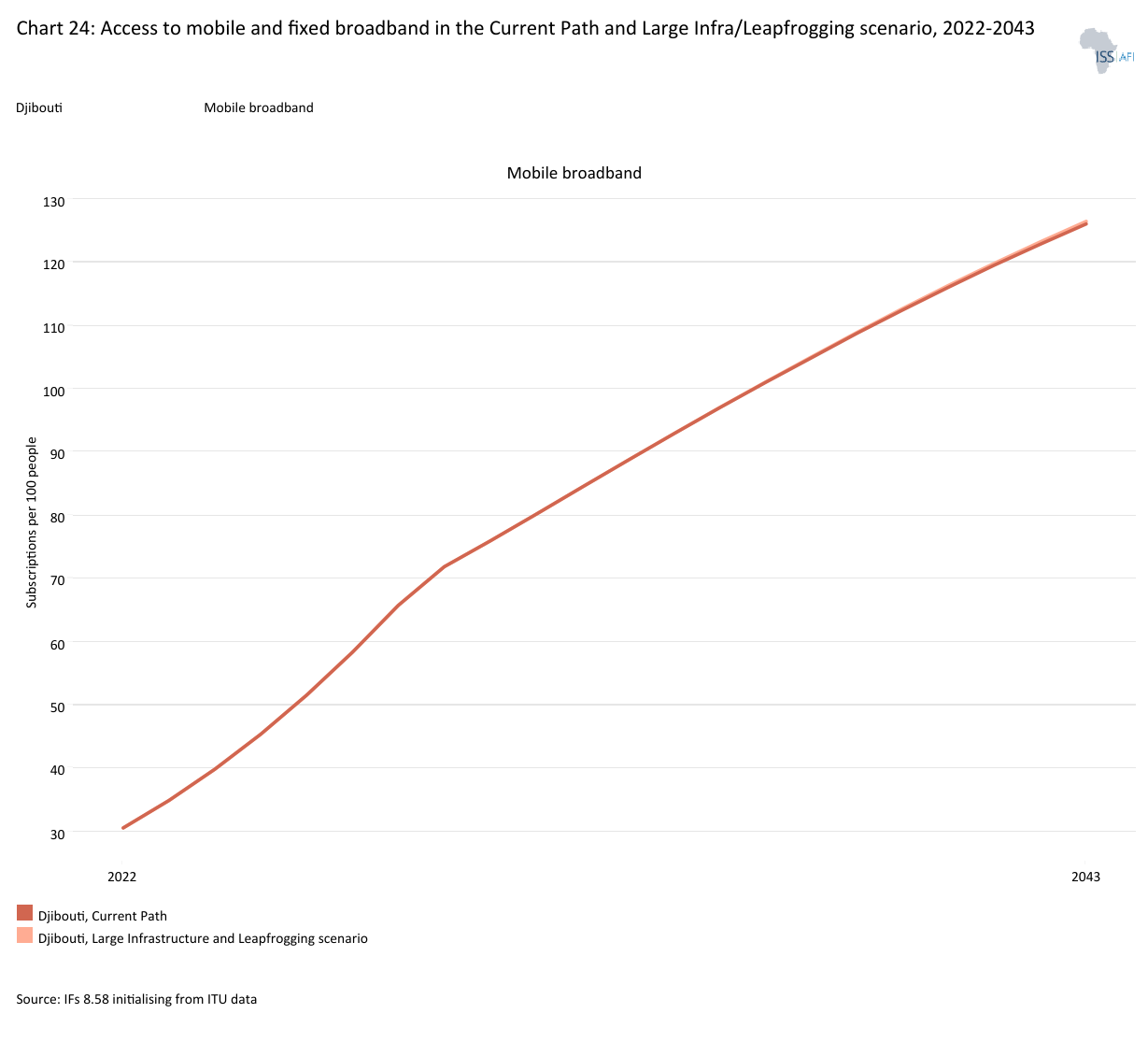

- The Large Infrastructure and Leapfrogging scenario will accelerate fixed broadband and energy access, with near-universal clean cooking achieved by 2043.

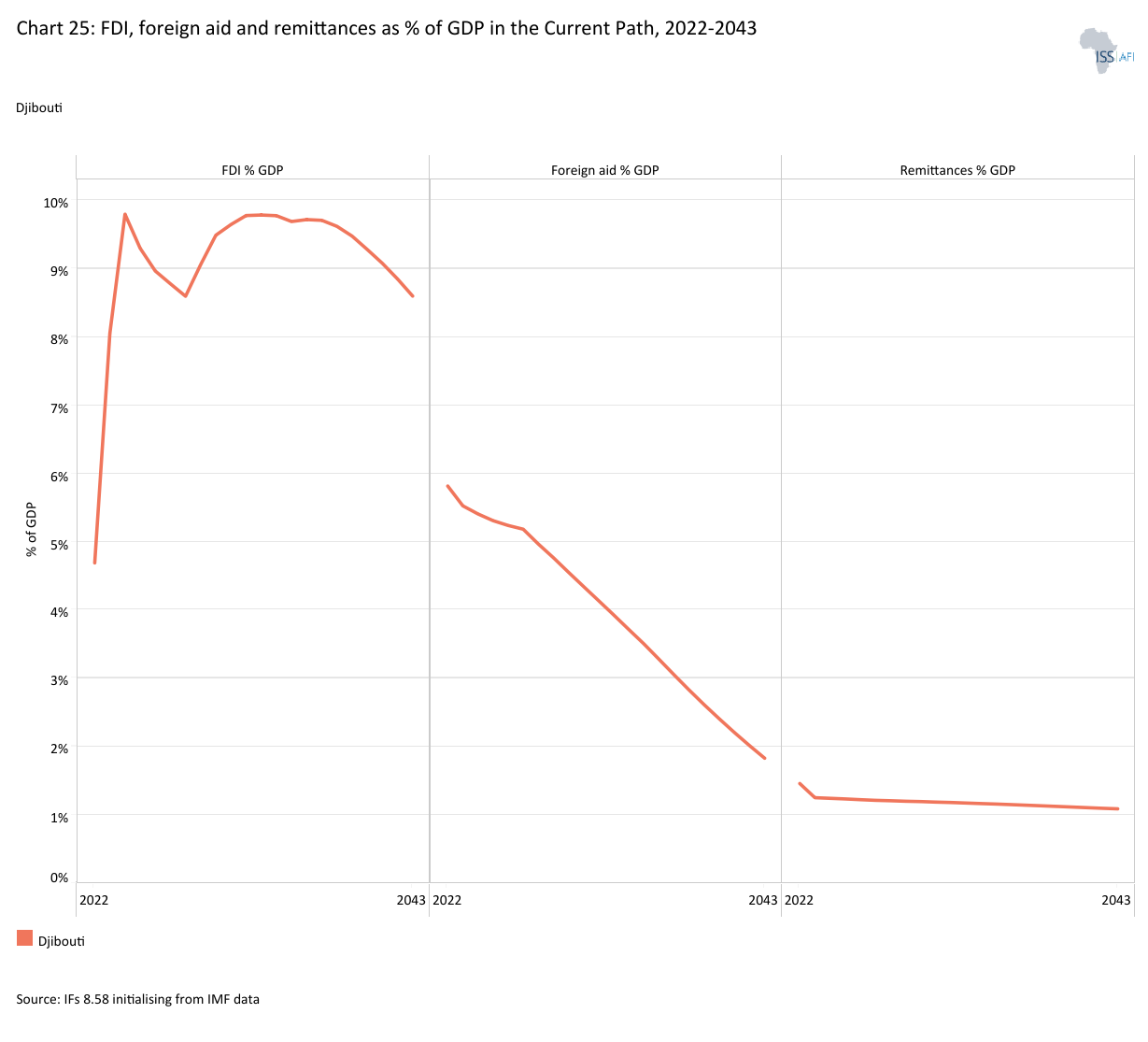

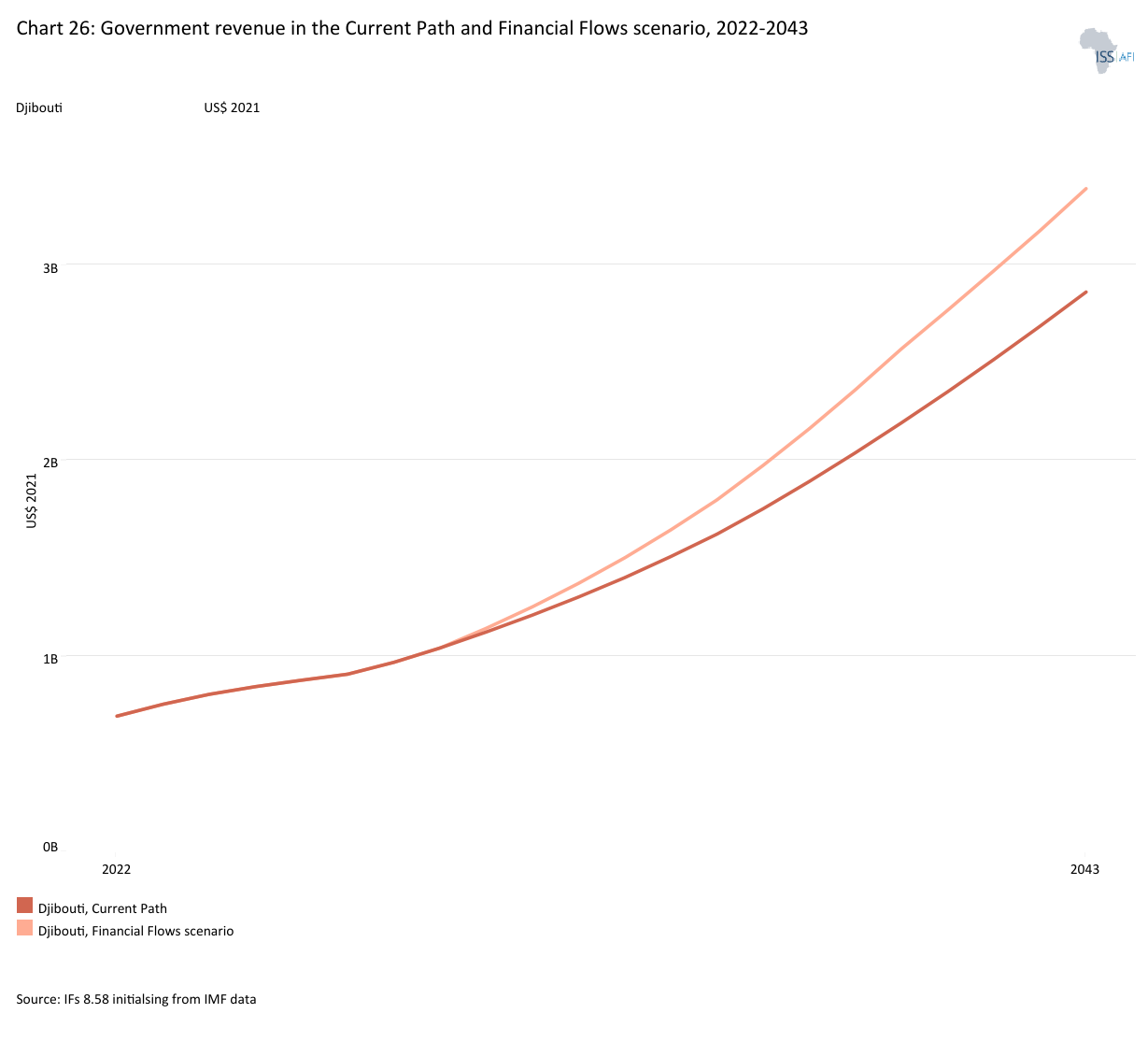

- The Financial Flows scenario will significantly increase fiscal space and investment, with government revenue rising to over 22% of GDP by 2043, which is about 0.3 percentage points above the Current Path forecast. Notably, the rise in revenue as a share of GDP suggests modest but meaningful improvements in tax effort and efficiency, rather than growth alone.

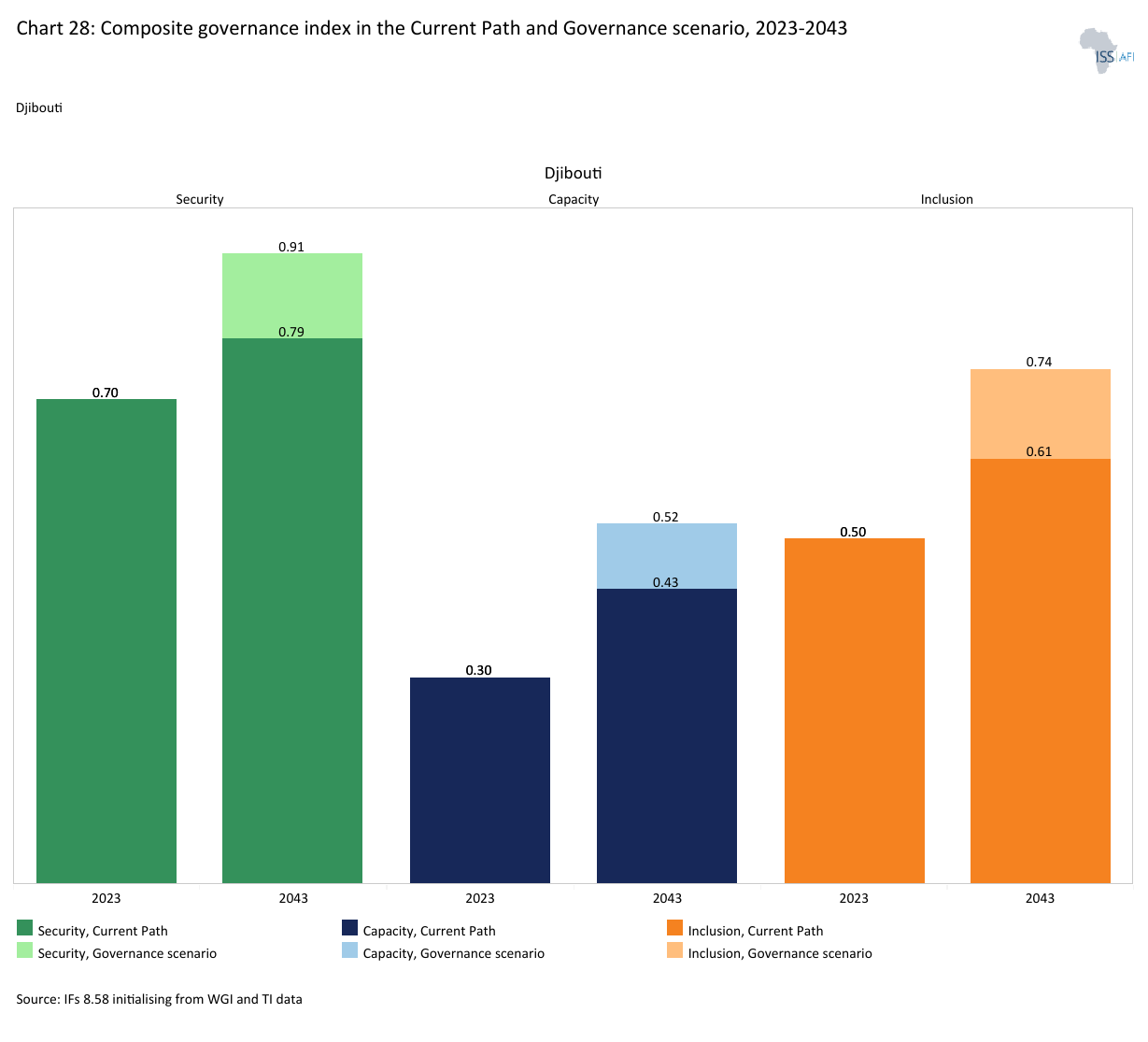

- Djibouti’s overall governance index will improve from 0.50 in 2024 to 0.73 by 2043 under the Governance scenario, compared to 0.61 under the Current Path. This accelerated progress would bring Djibouti closer to the governance levels of Africa’s stronger performers, such as Botswana, which will reach 0.77 by 2043 (from 0.71 in 2024).

The fourth section compares the impact of each of these eight sectoral scenarios with one another and subsequently with a Combined scenario (the integrated effect of all eight scenarios). The forecasts measure progress on various dimensions such as economic size (in market exchange rates), gross domestic product (GDP) per capita (in purchasing power parity), extreme poverty, carbon emissions, the changes in the structure of the economy and selected sectoral dimensions such as progress with mean years of education, life expectancy, the Gini coefficient or reductions in mortality rates.

- Good governance will have the most significant overall impact, greatly enhancing growth, per capita income, poverty reduction, and institutional effectiveness.

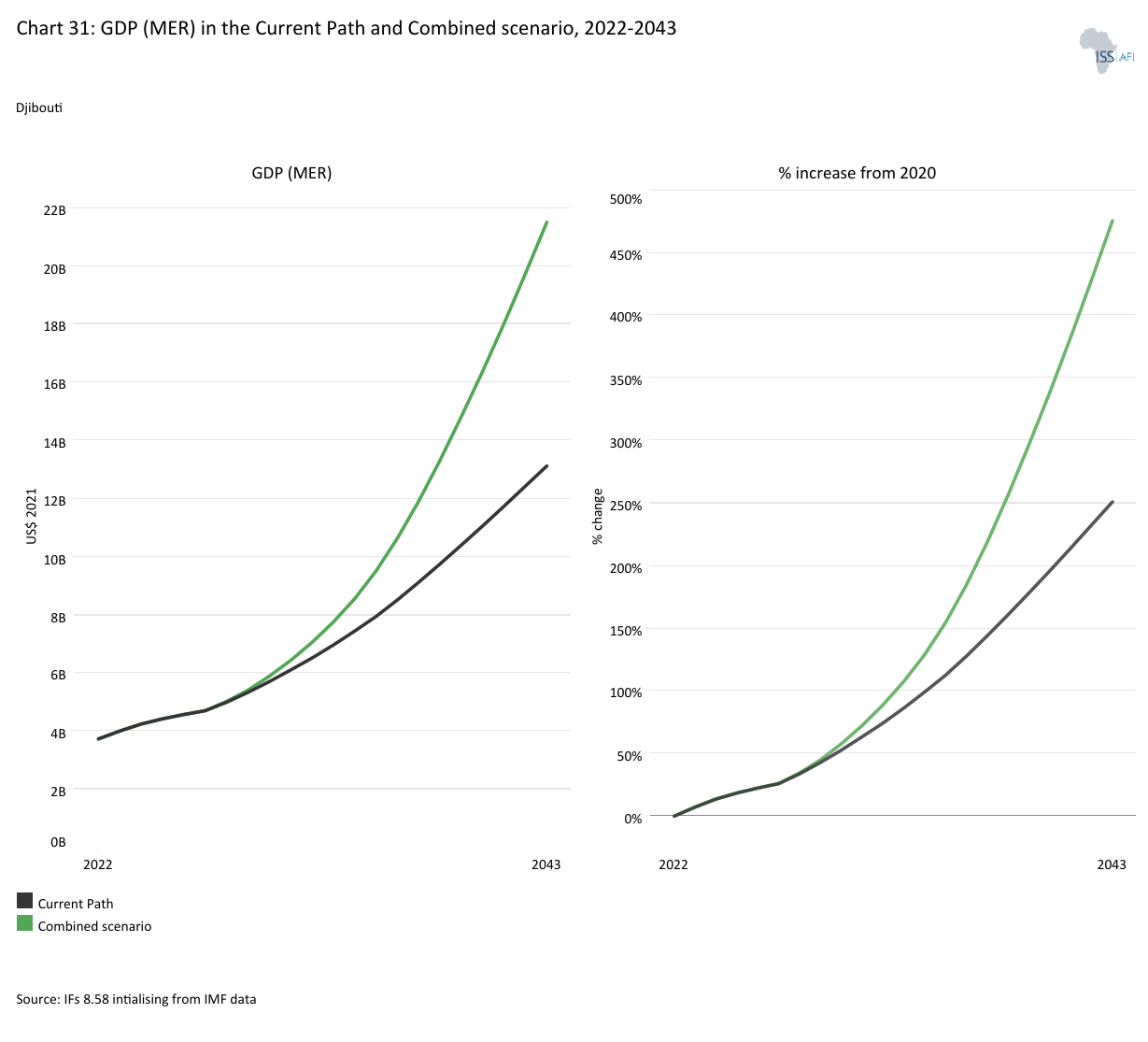

- In the Combined scenario, GDP (MER) will expand to US$21.46 billion by 2043 (approximately US$8.33 billion above the Current Path forecast), with average growth rising to 8.9%, meeting Vision 2035 targets.

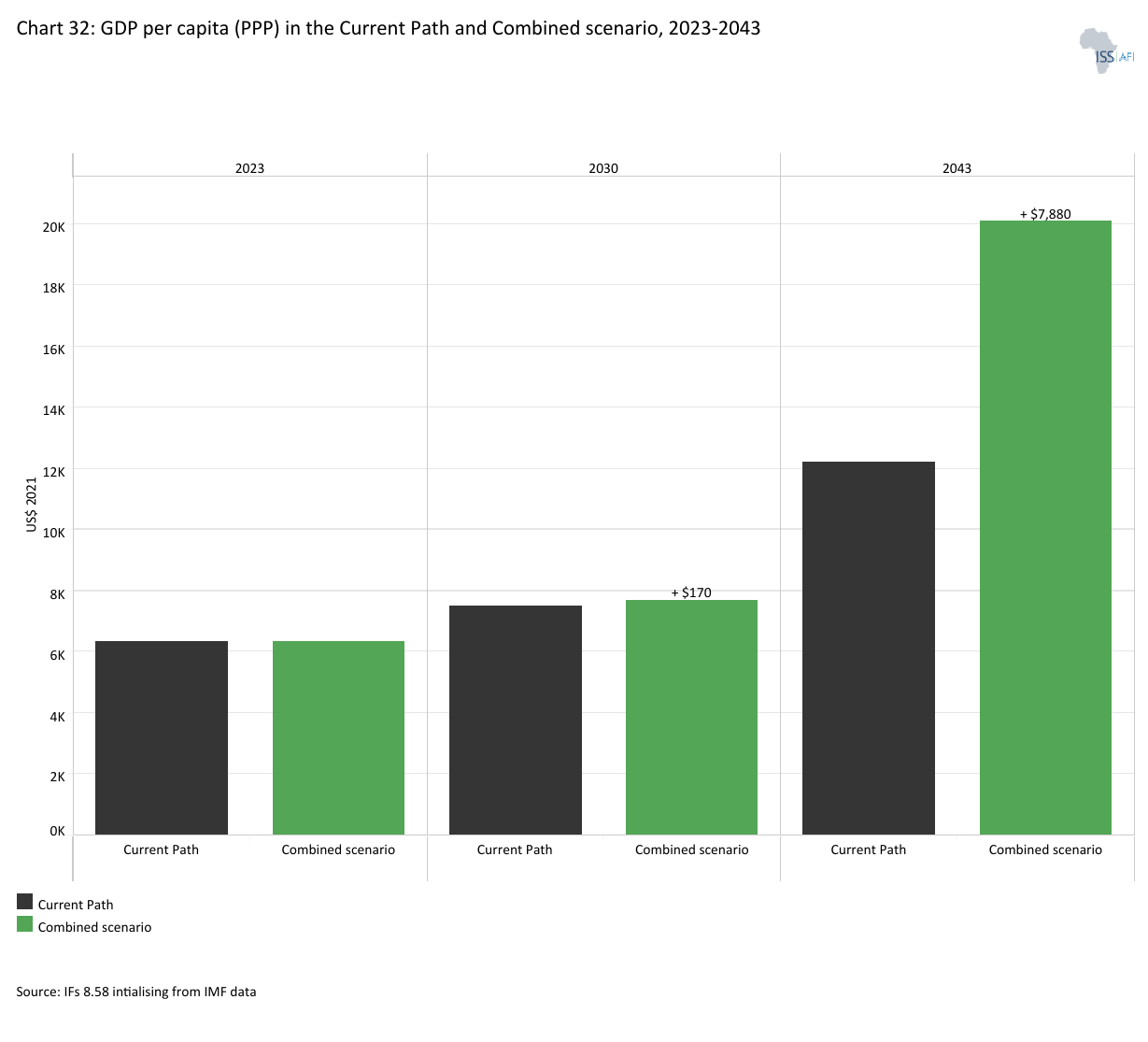

- GDP per capita (PPP) will triple to approximately US$20 090 by 2043 under the Combined scenario (about US$7 870 higher than the Current Path forecast), achieving the Vision 2035 income per capita target, albeit with delay.

- In the Combined scenario, structural transformation will begin, with gains (relative to the Current Path by 2043) in manufacturing and ICT, reducing reliance on a predominantly services-led model.

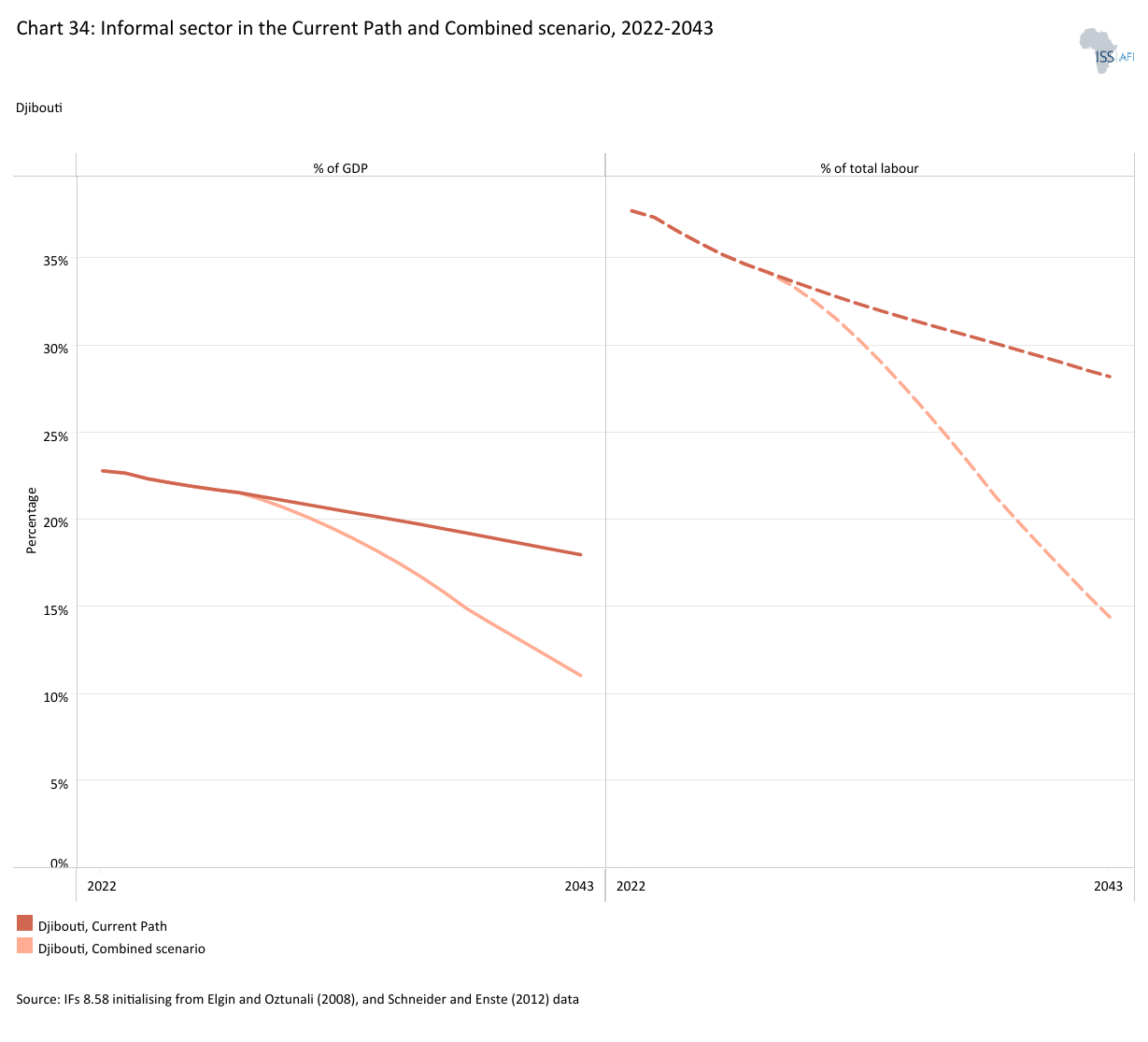

- By 2043, the informal sector’s contribution to GDP will decline to 11.1% under the Combined scenario, about 6.9 percentage points lower than the Current Path forecast. Informal employment in the non-agricultural labor force will also fall to 14.4%, roughly 13.8 percentage points below the Current Path, reflecting a significant shift in the labour market structure from one in three workers being informal to one in seven.

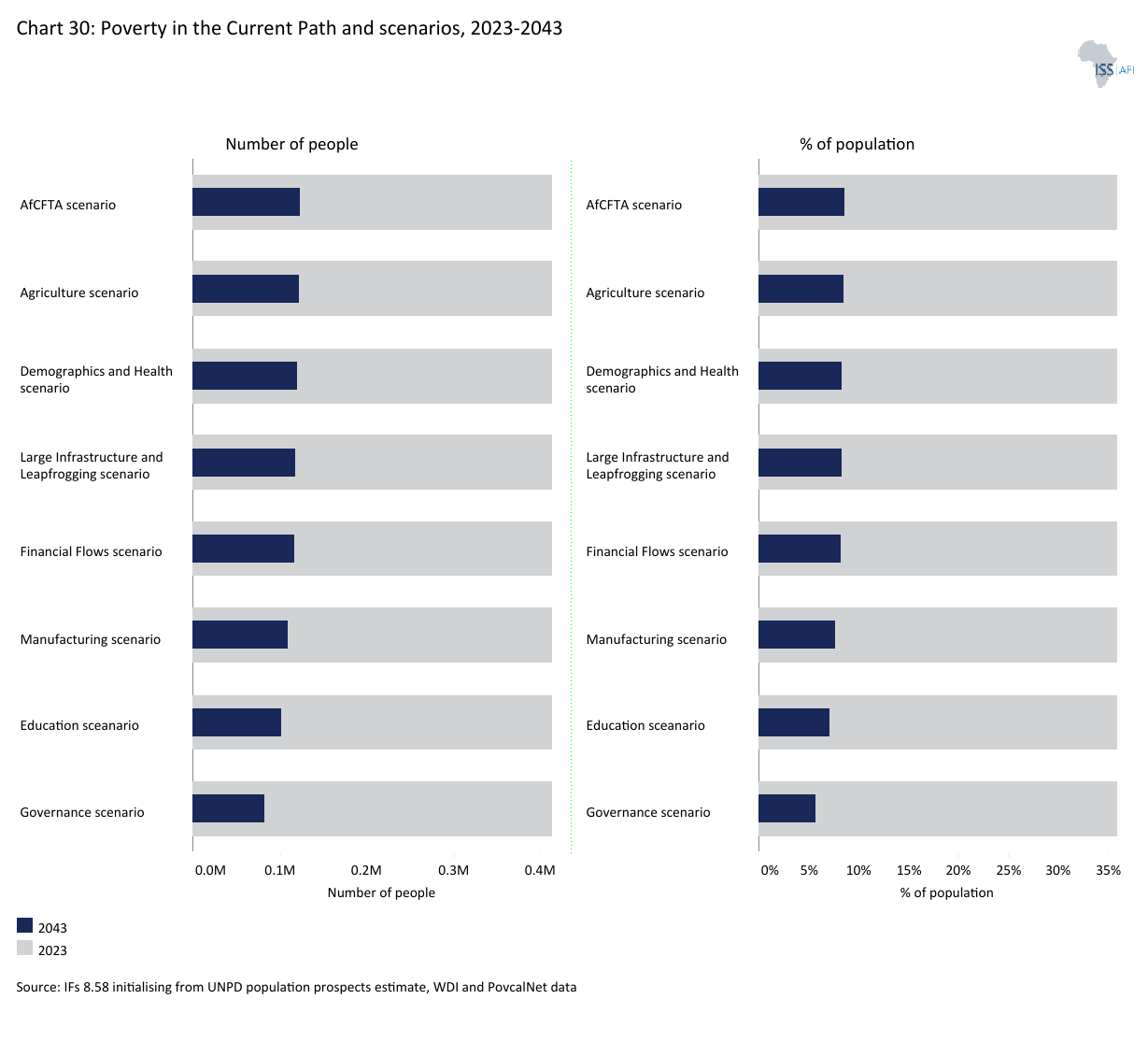

- Poverty (at the US$4.20 poverty line for LIMCs) will drop to 2.6% by 2043 under the Combined scenario, with nearly 88 000 additional people lifted out of poverty relative to the Current Path.

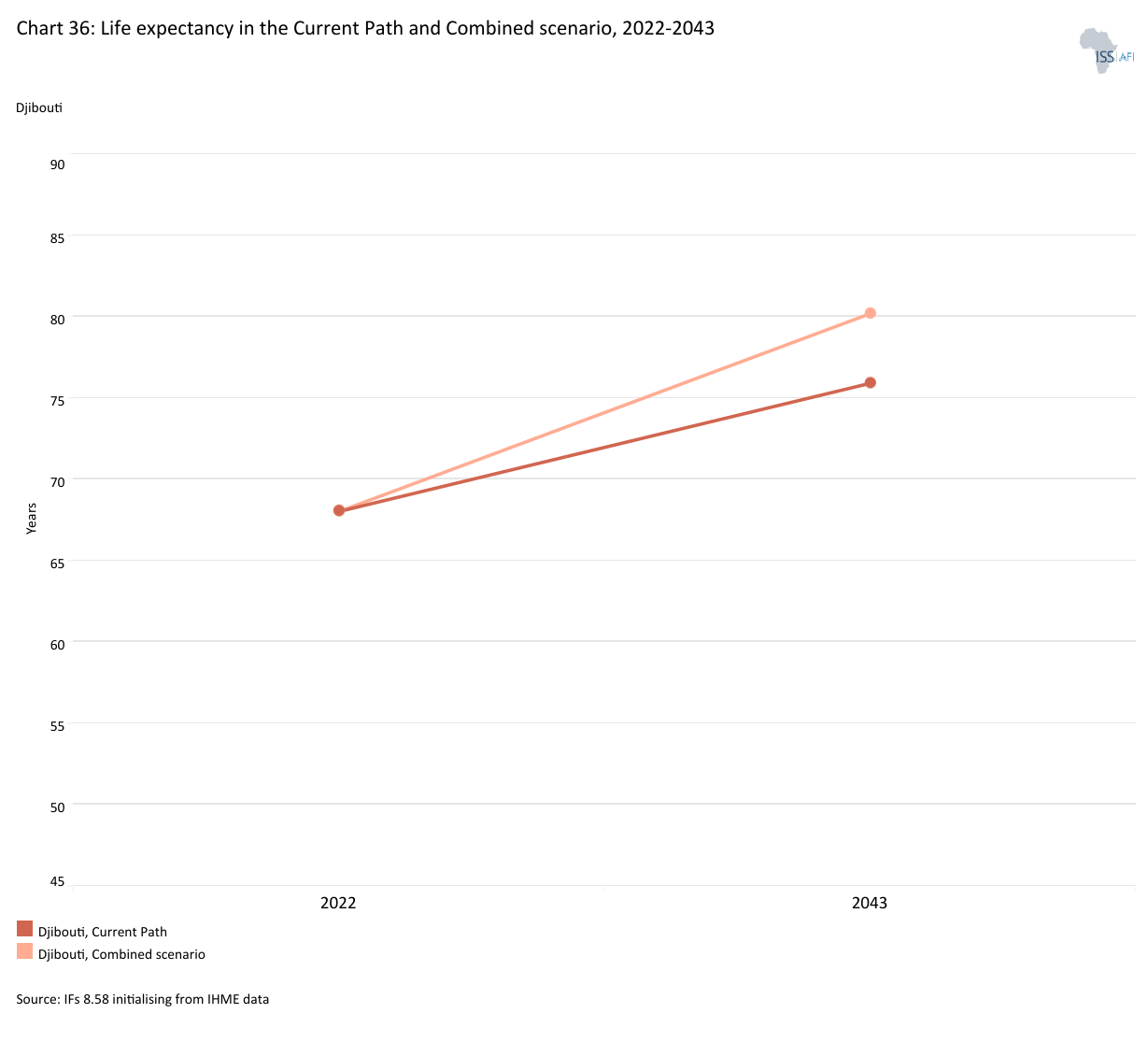

- Life expectancy will rise to 80.2 years by 2043 under the Combined scenario (about 4.3 years above the Current Path forecast), reflecting major improvements in health and well-being.

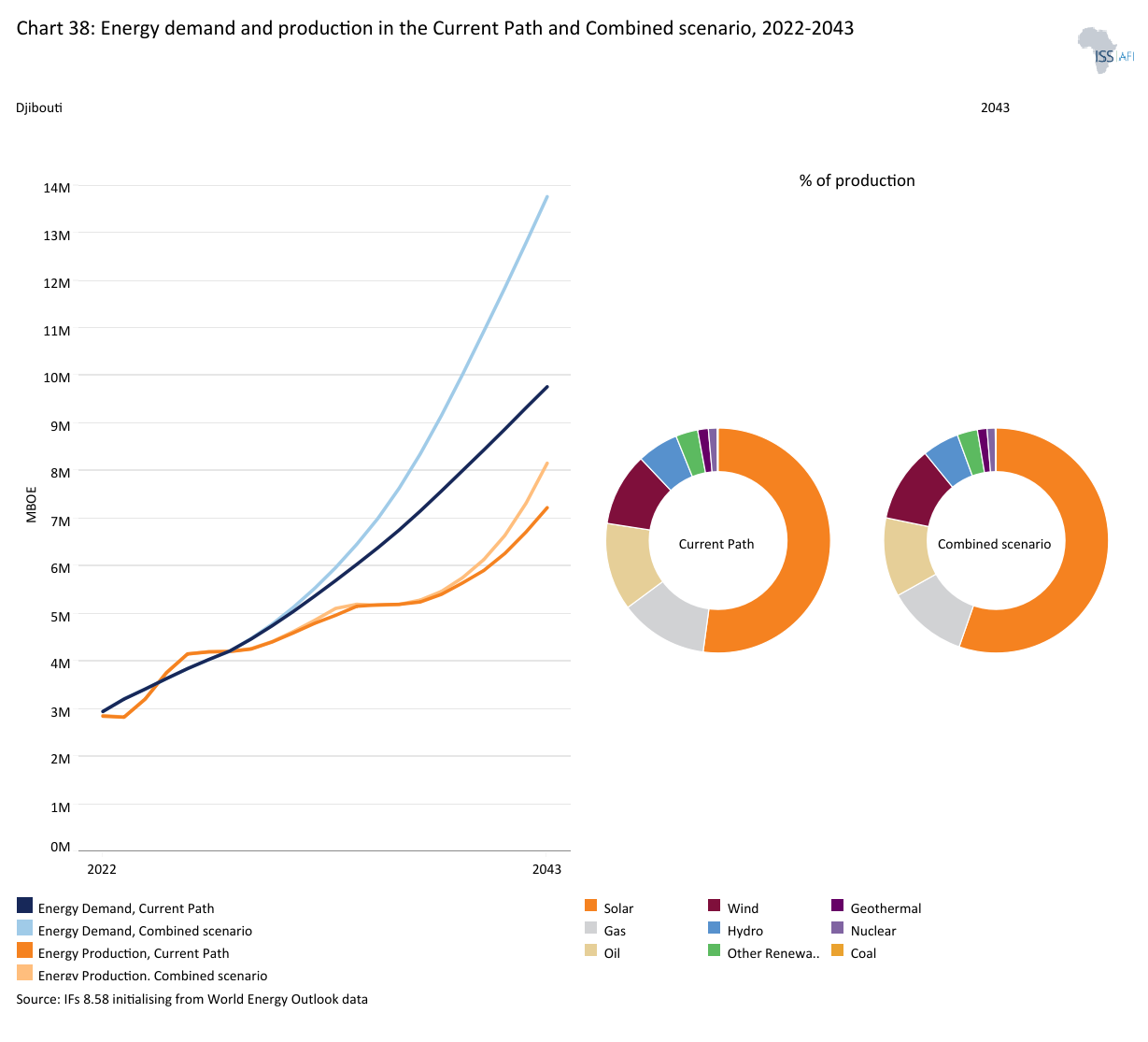

- Fossil-fuel carbon (CO2) emissions will increase with growth and demand but remain low in global comparison. At the same time, renewable energy will expand to almost 76% of production by 2043 (about 5 percentage points above the Current Path forecast), driven mainly by solar.

The report concludes with policy recommendations. Djibouti’s development trajectory to 2043 reflects steady growth under the Current Path, but one that will fall short of the ambitions of Vision 2035, particularly in terms of inclusiveness, job creation and income growth. The analysis shows that the country’s main constraint is not infrastructure, but the efficiency and inclusiveness of its existing growth model. Governance, financial flows and regional integration emerge as the highest-impact drivers of change, while sectors such as agriculture and infrastructure will play more enabling roles. Under a Combined scenario, growth will accelerate significantly, poverty will decline to very low levels, and informality will fall sharply, supported by stronger institutions, human capital and private-sector development. The findings underscore that Djibouti’s long-term success depends on shifting from a capital-intensive, corridor-based model toward a more diversified, productivity-driven and inclusive economy.

All charts for Djibouti

- Chart 1: Political map of Djibouti

- Chart 2: Population structure in the Current Path, 1990–2043

- Chart 3: Population distribution map, 2024

- Chart 4: Urban and rural population in the Current Path, 1990-2043

- Chart 5: GDP (MER) and growth rate in the Current Path, 1990–2043

- Chart 6: Size of the informal economy in the Current Path, 2022-2043

- Chart 7: GDP per capita in Current Path, 1990–2043

- Chart 8: Extreme poverty in the Current Path, 2022–2043

- Chart 9: National Development Plan of Djibouti

- Chart 10: Relationship between Current Path and Scenarios

- Chart 11: Mortality distribution in the Current Path, 2024 and 2043

- Chart 12: Infant mortality rate in Current Path and Demographics and Health scenario, 2022–2043

- Chart 13: Demographic dividend in the Current Path and the Demographics and Health scenario, 2022–2043

- Chart 14: Crop production and demand in the Current Path, 1990-2043

- Chart 15: Import dependence in the Current Path and Agriculture scenario, 2022–2043

- Chart 16: Progress through the education funnel in the Current Path, 2024 and 2043

- Chart 17: Mean years of education in the Current Path and Education scenario, 2022–2043

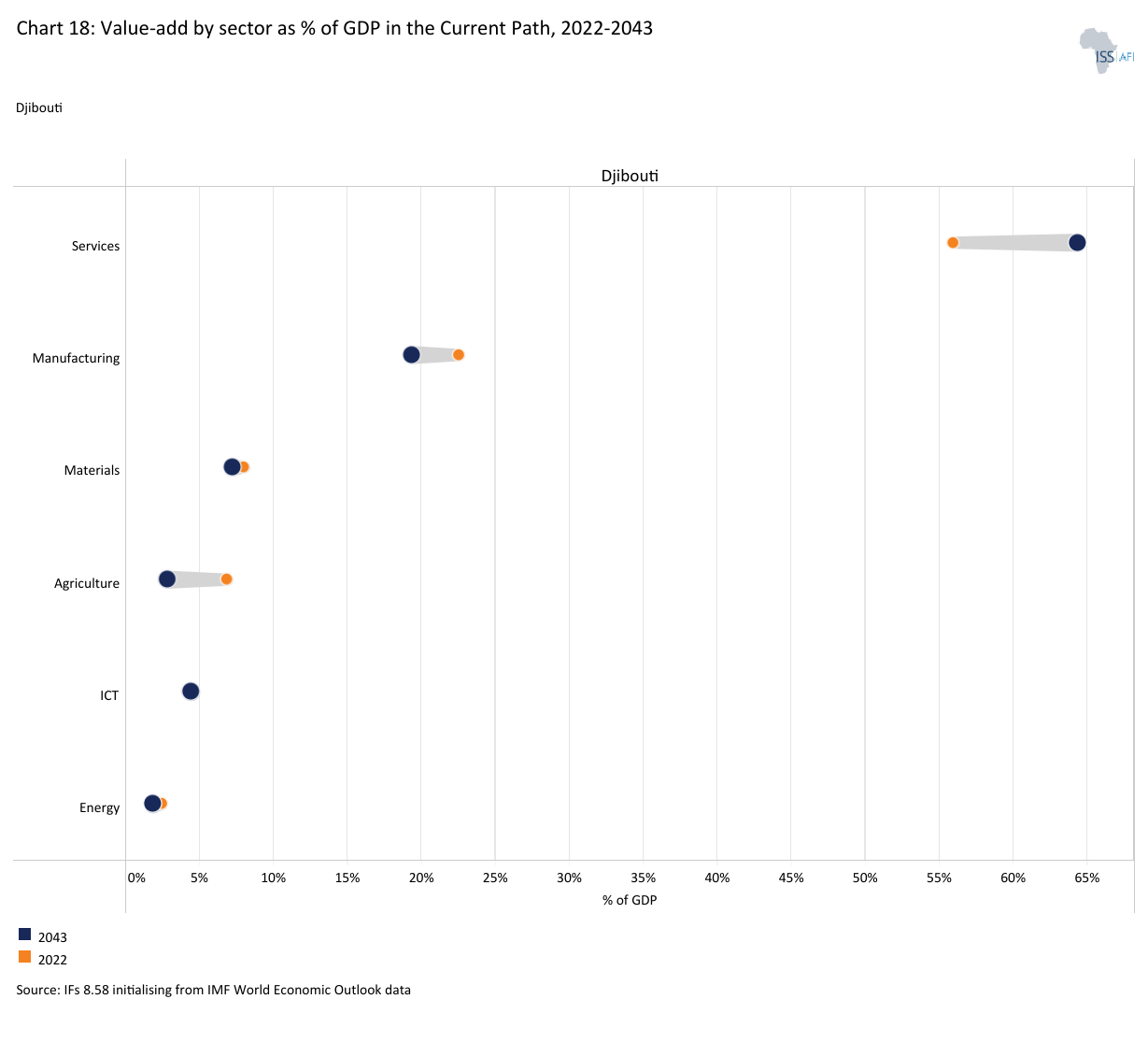

- Chart 18: Value-added by sector as % of GDP in the Current Path, 2024 and 2043

- Chart 19: Value-add by the manufacturing sector in the Current Path and Manufacturing scenario, 2020–2043

- Chart 20: Exports and imports as % of GDP in the Current Path, 2000-2043

- Chart 21: Trade balance in the Current Path and AfCFTA scenario, 2022–2043

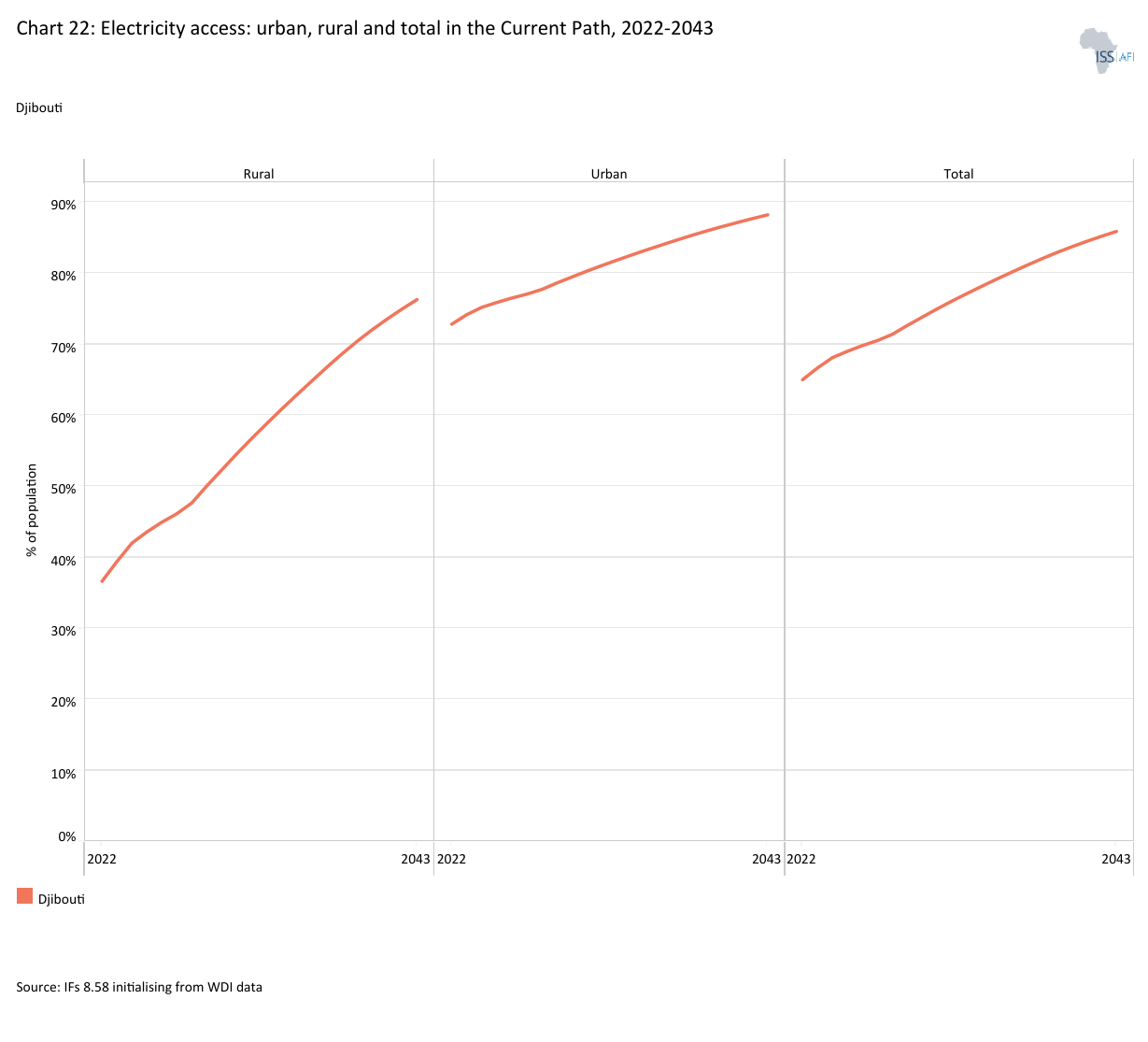

- Chart 22: Electricity access: urban, rural and total in the Current Path, 2000-2043

- Chart 23: Cookstove usage in the Current Path and Large Infra/Leapfrogging scenario, 2022–2043

- Chart 24: Access to mobile and fixed broadband in the Current Path and the Large Infra/Leapfrogging scenario, 2022–2043

- Chart 25: FDI, foreign aid and remittances as % of GDP in the Current Path and in the Financial Flows scenario, 1990-2043

- Chart 26: Government revenue in the Current Path and Financial Flows scenario, 2020–2043

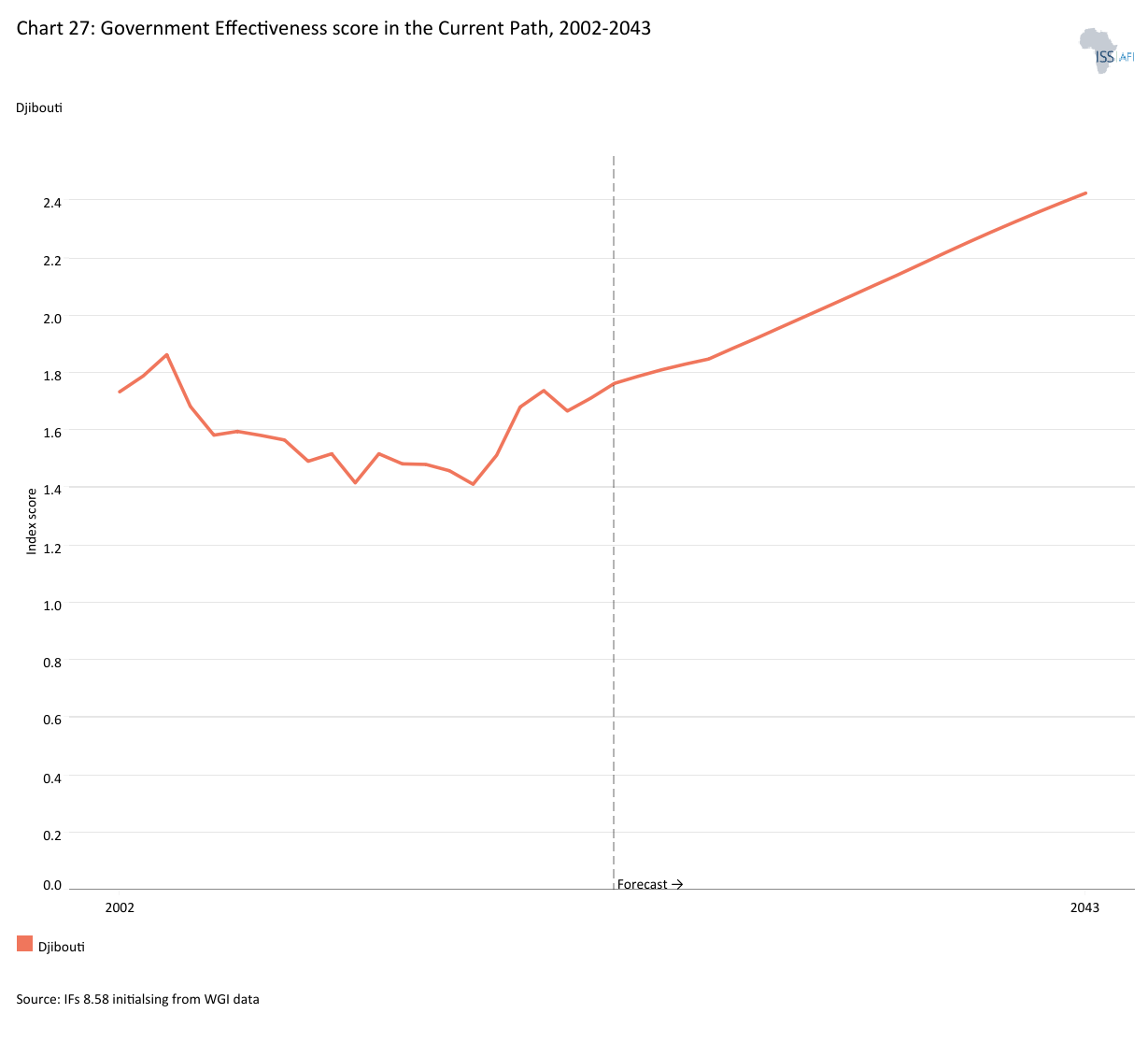

- Chart 27: Government effectiveness score in the Current Path, 2002-2043

- Chart 28: Composite governance index in the Current Path and Governance scenario, 2024 and 2043

- Chart 29: GDP per capita in the Current Path and scenarios, 2022–2043

- Chart 30: Poverty in the Current Path and Scenarios, 2022–2043

- Chart 31: GDP (MER) in the Current Path and Combined scenario, 2022–2043

- Chart 32: GDP per capita in the Current Path and the Combined scenario, 2022-2043

- Chart 33: Value added by sector in the Current Path and Combined scenario, 2024 and 2043

- Chart 34: Informal sector in the Current Path and Combined scenario, 2022–2043

- Chart 35: Poverty in the Current Path and Combined scenario, 2024 and 2043

- Chart 36: Life expectancy in the Current Path and Combined scenario, 2022–2043

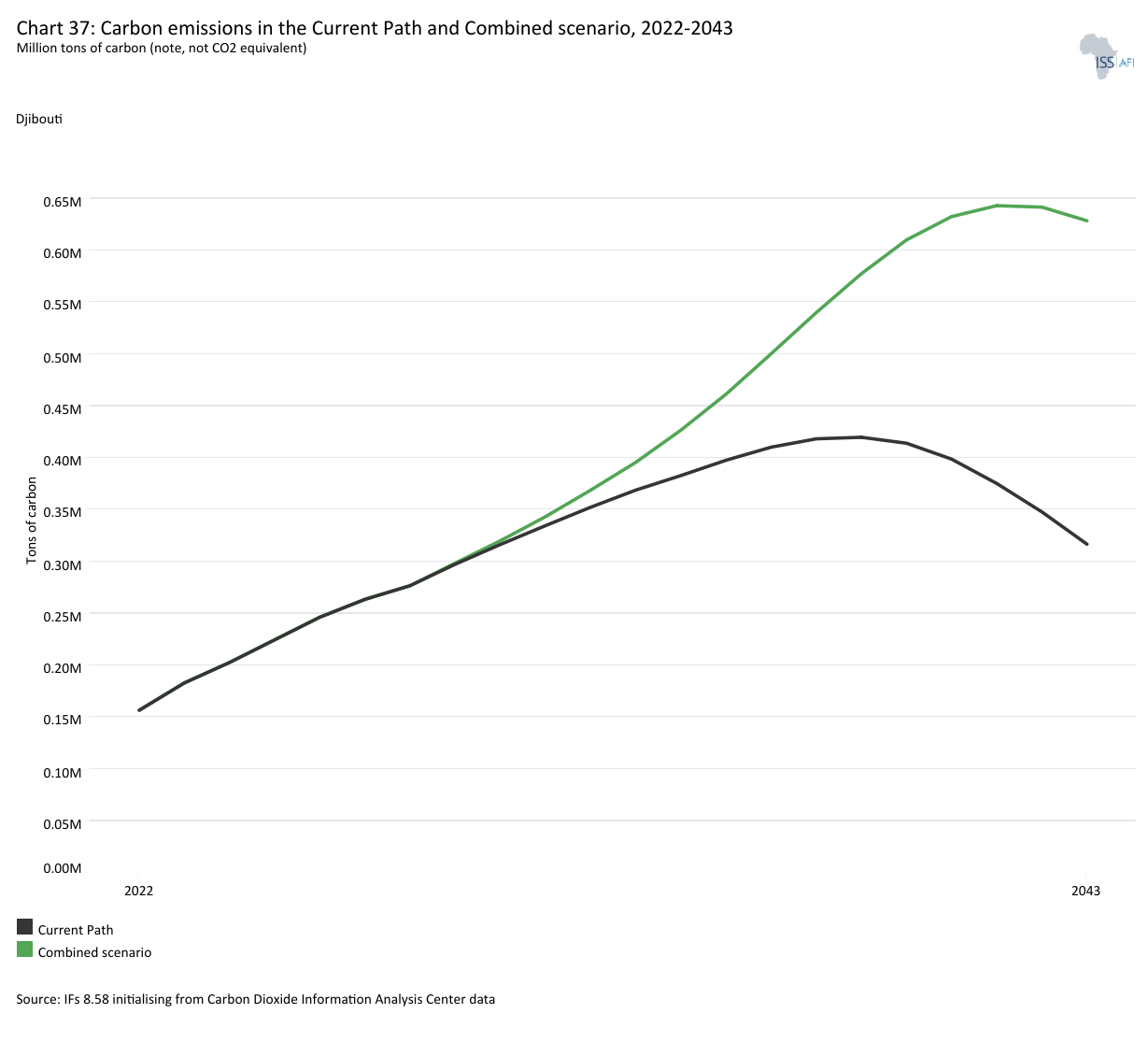

- Chart 37: Carbon emissions in the Current Path and Combined scenario, 2022–2043

- Chart 38: Energy demand and production by type in the Current Path and Combined scenario, 2022-2043

- Chart 39: Policy recommendations

Chart 1 is a political map of Djibouti.

Djibouti is a small, lower-middle-income country at the Horn of Africa’s maritime choke point, located along the Gulf of Aden at the southern entrance to the Red Sea, bordering Eritrea, Ethiopia and Somalia. Its land area is approximately 23 180 km², with a coastline of around 370 km. This geography is the central driver of Djibouti’s development model; it is the structural foundation of Djibouti’s national development narrative. Vision Djibouti 2035 frames the country’s aspiration as becoming a regional hub (“Lighthouse of the Red Sea”) and a bridge across Africa and adjacent regions by leveraging port services, logistics and connectivity.

Djibouti is among the world’s most climate- and water-stressed settings. The 2021 World Bank’s Climate Risk Country Profile characterises the country as highly arid, with nearly 90% classified as desert and limited arable capacity. The same profile reports a historical climatology baseline (1901–2019) of a mean annual temperature of approximately 27.8°C and mean annual precipitation of approximately 244.6 mm, with high intra-annual variability and generally low rainfall outside short wet periods.

Topography and geology reinforce both risks and opportunities. The World Bank profile describes terrain comprising plateaus, plains, volcanic formations and mountain ranges reaching up to 2 000 m, with altitudes varying from 155 m below sea level at Lake Assal to over 2 000 m at Mount Moussa Ali. These physical characteristics shape settlement, transport costs, disaster risk exposure (including flash flooding in wadis and coastal hazards) and the feasibility of renewable energy development, particularly geothermal and wind.

Djibouti’s constitutional framework (Constitution of 4 September 1992) defines the state as a sovereign democratic republic, establishes Arabic and French as the official languages and identifies Djibouti City as the national capital. The constitution specifies the structure of state authority, including that executive power is exercised by the President of the Republic, who is also Head of Government. The preamble also states that Islam is the religion of the State, which matters for social policy and institutional context.

Administratively, Djibouti’s decentralisation architecture distinguishes between (i) five decentralised regional collectivities, Ali Sabieh, Dikhil, Tadjourah, Obock and Arta, and (ii) Djibouti City, which has a distinct special status. The Presidency’s official regional page states that these five regions have legal personality and financial autonomy and are administered through directly elected regional councillors, while Djibouti City has a special status under Law No. 122/AN/05/5èmeL. This law establishes “Djibouti-ville” as a territorial authority and specifies that the city comprises three communes: Ras-Dika, Boulaos and Balbala. These institutional arrangements matter for the scenario analysis that follows because many interventions (education expansion, rural electrification, social transfers, governance reforms, tariff implementation under AfCFTA) depend on multi-level implementation capacity and local service delivery.

Djibouti gained independence on 27 June 1977 following its transition from French colonial administration, and its early post-independence political development required balancing ethnopolitical cohesion and state-building in a complex regional environment. Djibouti also experienced internal conflict in the early 1990s; a key milestone in stabilisation was the 1994 Peace and National Reconciliation Accord, captured in peace agreement datasets as dated 26 December 1994, which is commonly referenced as a turning point in the conflict trajectory. In the Vision 2035 framing, peace and national unity are emphasised as prerequisites for economic transformation, reflecting the view that sustained stability is essential for investment, corridor performance and tourism, as well as for protecting the country’s role as a regional logistics hub.

The social geography of Djibouti is primarily centred around the capital region. Moreover, the country serves as a host for refugees and asylum seekers living in a fragile neighbourhood. According to the UN Refugee Agency (UNHCR) operational overview, as of 31 January 2025, Djibouti was providing international protection to 32 920 refugees and asylum seekers, which accounts for over 3% of the total population.

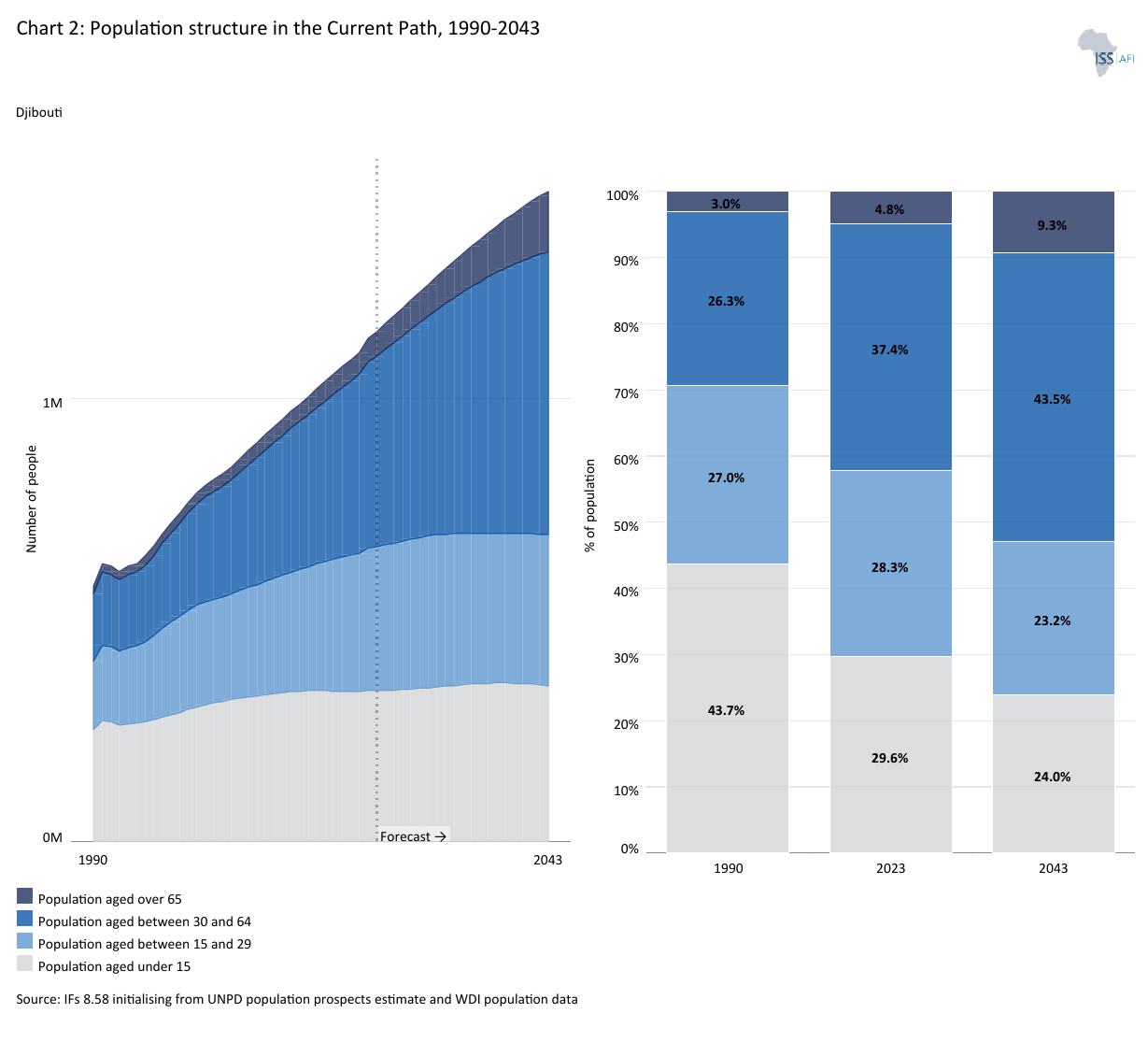

Chart 2 presents the Current Path of the population structure from 1990 to 2043.

Djibouti’s population structure shifted from a classic youth-heavy pyramid in 1990 toward a more working-age-dominant profile today and through 2043. The total population roughly doubled from 579 500 in 1990 to about 1 169 820 people in 2024. The Current Path indicates a further increase to almost 1.5 million people by 2043. In global comparative terms, Djibouti’s population remains a very small fraction (0.014%) of the world total, ranking around 160th globally by population size, with a median age of about 25 years.

The underlying demographic transition is visible in the changing shares of children (under 15 years), the working-age population (15-64 years) and the elderly (65+ years). The working-age population rose from about 53% in 1990 to 65.9% in 2024, and will edge up to 66.9% by 2043 under the Current Path. At the same time, the child share continued to narrow from 43.5% to 29.2% and then to 24%. The elderly share, while small, has risen from about 3% in 1990 to about 5% in 2024, and will reach 9.3% by 2043.

Conceptually, the population pyramid is thickening through the central age bands, indicating that Djibouti is already within a potentially favourable demographic window (detailed in Chart 13) where the working-age population dominates the age structure. The fiscal implications of Chart 2 follow directly from the shifting composition of dependency. The falling child share can gradually reduce cohort pressure on primary education and child health systems, enabling a rebalancing from access expansion toward quality and completion, provided policy and financing keep pace. But by 2043, the rising 65+ share (9.3% under the Current Path) will imply that Djibouti must also plan early for higher demand for chronic disease care and support for older adults.

Fertility decline is the primary driver of this structural shift. Djibouti’s total fertility rate fell from about 6 births per woman in 1990 to roughly 2.6 in 2024. The Current Path depicts a further decrease to 2 births per woman by 2043. This trajectory aligns with the standard dynamics of the demographic transition, as fertility approaches the replacement level of approximately 2.1 births per woman. At replacement level, each generation effectively replaces itself in the absence of migration. As Djibouti’s fertility rate will reach 2 births per woman by the early 2040s, population growth is therefore expected to gradually slow.

The dependency ratio summarises how these moving parts affect the economic balance between potential producers and dependants. The dependency ratio declined from 0.88 in 1990 to 0.52 in 2024, and will decline to 0.5 by 2043 under the Current Path. A dependency ratio close to 0.50 is generally considered favourable at the macroeconomic level, but this is true only if labour markets can effectively absorb the working-age population. Essentially, a ratio of about 50 dependants per 100 working-age individuals indicates a significant potential productive base relative to the non-working-age population.

However, it is critical to distinguish age dependency from economic dependency. The International Labour Organisation (ILO) and Worldometer explicitly caution that dependency ratios do not account for labour force participation and unemployment; some people counted as “working-age” may not be employed, while some “dependants” may be working. This distinction is central to interpreting economic implications under Djibouti’s Current Path.

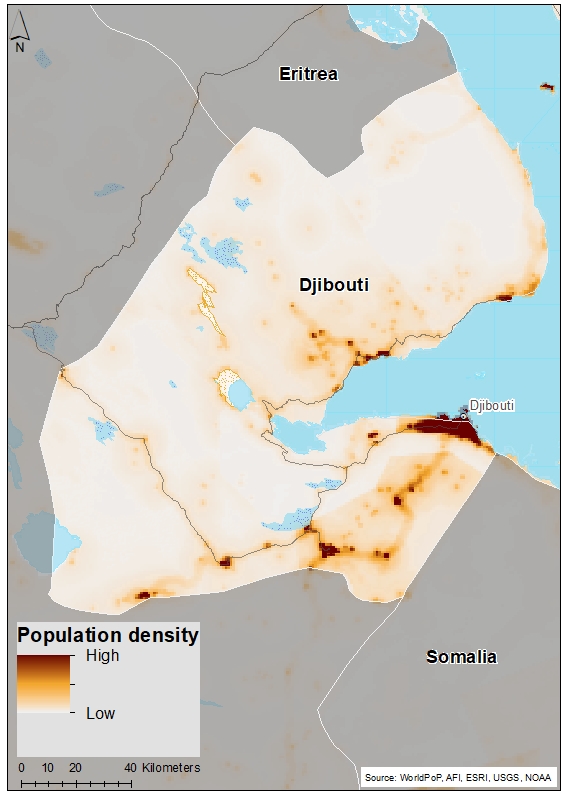

Chart 3 presents a population distribution map for 2024.

Djibouti’s population distribution is characterised by extreme spatial concentration in and around Djibouti City and the coastal corridor. This pattern reflects both the country’s geographic constraints and a political economy centred on port and logistics activities. In 2024, Djibouti’s population density was approximately 50 people per square kilometre, based on a total land area of 23 180 square kilometres. Under the Current Path, density will increase to about 63 people per square kilometre by 2043.

As indicated in the introduction section, Djibouti’s social geography is highly urbanised. In 2025, Djibouti City accounted for more than 62% of the national population, followed by Ali Sabieh (7.5%), Tadjoura (5.4%) and Dikhil (4.7%). This pattern of concentration is consistent with broader urbanisation trends. According to the World Bank’s climate risk profile, around 78% of Djibouti’s population was already living in urban areas in 2019, and the urban share is forecast to increase further to approximately 85% by 2050.

Djibouti’s urban primacy has economic benefits and costs. On the upside, a dominant capital region can generate strong agglomeration economies: concentrated labour pools, denser consumer markets, lower per-capita cost of some infrastructure networks (for example, electricity distribution in dense neighbourhoods) and faster diffusion of services and innovation. This logic is consistent with Vision 2035, which explicitly frames the country’s objective as positioning itself as a hub for the regional and continental economy. The World Bank’s climate profile further highlights that the port complex is the principal economic driver, linking the spatial concentration of people and jobs to port-adjacent economic activity.

On the cost side, this same concentration amplifies the challenge of urban services keeping pace with urban growth. With the population rising to roughly 1.5 million by 2043, the demand surge is not abstract; it translates into higher requirements for housing, water supply, sanitation, electricity connections, urban mobility and broadband capacity, especially in dense and often informal peripheral settlements. Djibouti is among the world's most water-scarce countries. It faces compounding climate risks, including drought, heat waves, floods, earthquakes and sea-level rise, which raise the cost and complexity of servicing dense coastal populations. When land-use planning and drainage infrastructure lag, dense urbanisation can turn climate shocks into repeated economic losses through port disruption, damaged housing and roads and heightened public health risks. In effect, the spatial pattern intensifies the need for urban resilience investments, including flood control, coastal defences, heat mitigation and reliable water systems.

Spatial concentration also carries a distributional dimension. The Strategy of Accelerated Growth and Promotion of Employment (SCAPE) identifies the need for more balanced territorial development. It explicitly includes an axis on “poles of both regional development and sustainable development,” while also aiming to reduce social disparities and guarantee access to basic services. In a country where the capital concentrates most people and formal economic activity, peripheral regions risk being trapped in a low-access equilibrium characterised by weaker service delivery, higher transport costs, fewer formal jobs and greater vulnerability to shocks. This is not only a rural–urban issue but also a corridor dynamic, given Djibouti’s dependence on port and transit activities, particularly those linked to Ethiopia.

A further spatial dimension shaping Djibouti’s development is the distribution of displaced populations and refugee hosting, which extends beyond the capital into peripheral regions. According to UNHCR, Djibouti hosts approximately 32 000 forcibly displaced people, of whom around 85% reside in refugee settlements, with the remainder living in urban areas, including Djibouti City. These settlements are primarily located in border regions, Holl Holl and Ali Addeh in the Ali Sabieh region, and Markazi in the Obock prefecture, highlighting a distinct geography of displacement that places additional pressure on already underserved areas.

Refugee-hosting regions are not only sites of humanitarian response but also emerging nodes of service delivery and infrastructure demand. Operational updates consistently highlight the need to expand access to water, energy, transport and social services in settlements such as Ali Addeh and Holl Holl, underscoring persistent infrastructure gaps in peripheral areas.

The above trends suggest that regional development strategies should go beyond fostering secondary economic hubs to explicitly incorporate refugee-hosting areas into national planning frameworks. Investments in these regions can serve dual objectives: addressing humanitarian needs while strengthening local economies, improving social cohesion and reducing spatial inequalities. Integrating refugee populations into local service systems and labour markets, where feasible, can also support more inclusive and resilient growth, particularly in a country where geographic concentration and resource constraints already shape development outcomes.

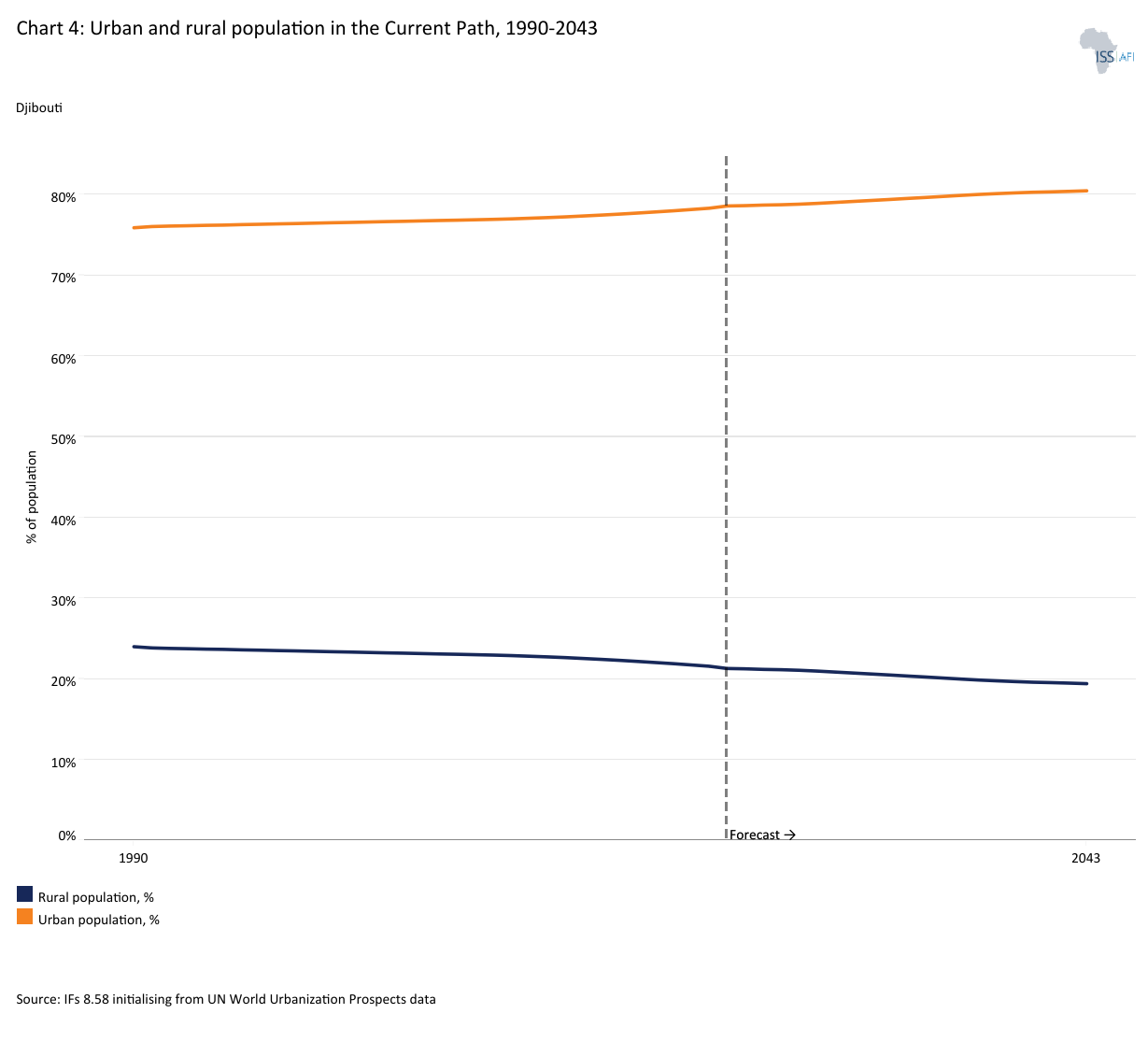

Chart 4 presents the urban and rural population in the Current Path, from 1990 to 2043.

Djibouti is already one of Africa’s most urbanised countries. Urban share rose rapidly between 1960 and 1983 (from 50.4% to 74.5%) and continued upward to 76% in 1990. Since then, the pace of change has slowed. The urban share reached 79% in 2024 and will increase modestly to 80.5% by 2043 under the Current Path. The Current Path is broadly consistent with the World Bank’s Climate Risk Country Profile Report forecast of an 85% urban rate by 2050, up from 78% in 2019. This flattening of the urbanisation trend is typical as a country approaches saturation, a point at which urban shares can still rise, but the dominant dynamic shifts to absolute urban population growth rather than sharp shifts in the urban–rural balance.

In absolute terms, the Current Path implies a large increase in the number of urban residents over the next two decades, even though the urban share changes only marginally. Djibouti’s urban population rose from roughly 440 200 in 1990 to about 920 690 in 2024, and will reach about 1.18 million by 2043. The rural population also grew in absolute terms, from roughly 139 300 to about 249 130 and around 285 930 in the same period, even as the rural share declined. The key planning implication is that rural service demand does not disappear; it remains material and grows, while the urban service burden grows faster.

The economic implications of Chart 4 hinge on the interaction between urban primacy, infrastructure capacity and labour-market absorption. Djibouti’s economy is anchored in the capital’s port–logistics complex; the World Bank profile describes the complex as the country’s economic driver, which explains why people and jobs concentrate in Djibouti-Ville and its peri-urban communes. High urban concentration can generate agglomeration economies, dense labour markets, proximity to customers and services, and lower per-capita costs for some network infrastructure (electricity distribution, broadband rollout) when density is high. Under the Current Path, this can support productivity in tradable services (logistics administration, transport services, ICT-enabled activities) if the business environment and human capital allow firms to scale.

At the same time, the costs of high urbanisation are visible: housing deficits, congestion and undersupplied basic services can push a large share of the population into informal settlements and vulnerable living conditions. Vision 2035 explicitly acknowledges that rapid urbanisation (especially between 1977 and 2010) contributed to the “rapid development of precarious districts” driven by rural exodus and commits to a policy for “cities without shantytowns,” including economic housing and sanitation of the built environment. This is not merely aspirational; Djibouti’s Integrated Slum Upgrading Project (launched in 2018) aims to improve living conditions in deprived urban areas of Djibouti City and to strengthen institutional capacity for the government’s Zero Slum Program (Programme Zéro Bidonville), explicitly targeting vulnerable groups, including refugees and displaced populations. Development partners also document acute service gaps in fast-growing peri-urban areas. For instance, AFD notes that Djibouti City hosts a very large share of the national population and that rapid urbanisation contributed to the explosive growth of Balbala, with water and sanitation networks described as “almost non-existent” in parts of the district.

Labour-market dynamics amplify these urban pressures. As Chart 2 shows, Djibouti’s working-age population increases sharply in absolute terms under the Current Path; Chart 4 suggests much of this additional labour supply will continue to concentrate in urban areas. If labour demand in higher-productivity sectors fails to expand, the likely outcomes include higher unemployment and informality. This risk is already visible: the World Bank’s modelled ILO estimates place total unemployment at 26% in 2025 for Djibouti. In such a context, high urbanisation can magnify social and fiscal strain (pressure for public employment, informal coping strategies) unless reforms accelerate private-sector job creation and skills development in line with national planning goals.

Urbanisation also intersects with displacement geography. As indicated in the previous section, UNHCR reports that 85% of the refugees hosted in Djibouti reside in refugee villages such as Ali Addeh, Holl-Holl and Markazi. At the same time, the remainder live in urban areas like Djibouti City. This means that even under a highly urbanised national profile, substantial service delivery needs exist in non-urban or peri-urban settings (camps and host communities), while urban systems must also plan for a share of refugees and asylum seekers integrated into city neighbourhoods. The urbanisation story is thus best understood as a two-track service challenge: scaling urban systems in the capital while ensuring infrastructure and basic services in refugee-hosting and rural areas keep pace with absolute population growth.

Finally, Djibouti’s environmental and spatial constraints intensify the stakes of urban planning. The World Bank climate profile characterises the country as highly arid, with most land classified as desert, resource scarce and vulnerable to hazards that can be exacerbated by water scarcity and weak land-use planning. For a predominantly coastal, capital-focused settlement pattern, this raises the premium on climate-resilient infrastructure: reliable water production and distribution, flood management during extreme rainfall, heat mitigation and coastal risk management (all essential for protecting households, ports and critical logistics infrastructure).

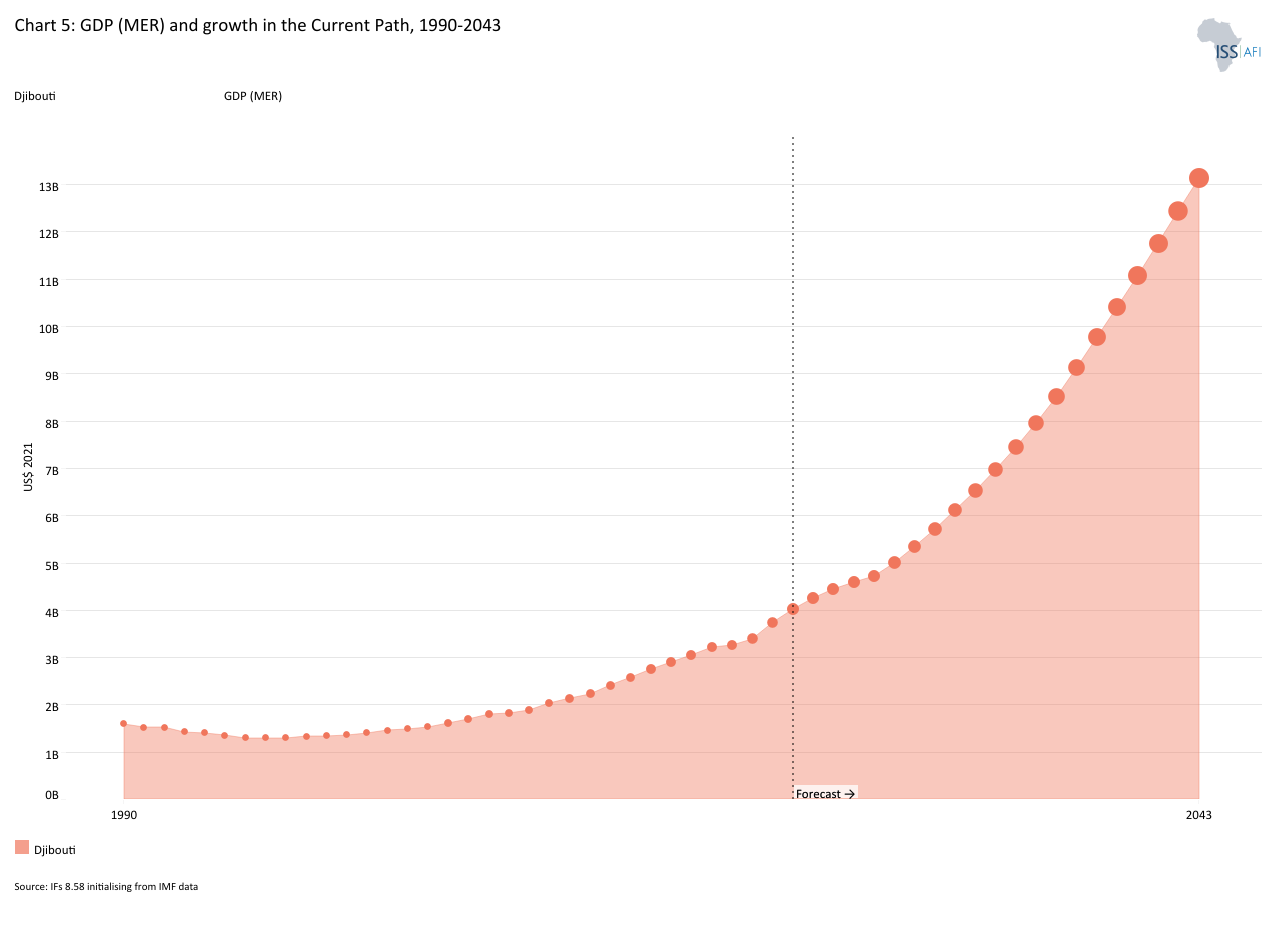

Chart 5 presents GDP in market exchange rates (MER) and growth rate in the Current Path, from 1990 to 2043.

Djibouti’s GDP (MER) expanded from US$1.47 billion in 1990 to US$4.25 billion in 2024, reflecting an average annual growth rate of 3.3%. Despite this growth, the country remained relatively small in terms of GDP, ranking 164th out of 193 countries in 2024. Looking ahead, GDP will reach approximately US$13.13 billion by 2043 under the Current Path, implying a significantly faster average annual growth rate of 6.1% over the 2025–2043 period. Overall, Djibouti’s growth trajectory since 1990 underscores its transformation into a capital-intensive, services-driven economy anchored in logistics and regional connectivity.

The historical pattern of GDP growth from 1990 to 2024 is consistent with the dominant narrative in official diagnostics. Djibouti’s growth has been strongly shaped by large-scale investment in port and transport infrastructure, conversion of its strategic geography into service activity, and renewed corridor linkages to Ethiopia, often financed by a mix of external borrowing and partner-supported investment. The Government’s National Development Plan 2020–2024 (Djibouti ICI) explicitly notes that the economy’s performance improved since 2000, with growth around 5–7% per year, especially starting 2010, and it attributes recent performance in part to the implementation of SCAPE (2015–2019) and the associated rollout of state-of-the-art infrastructure such as the Djibouti–Addis Ababa railway, ports and a Free Zone. This investment-led pattern is corroborated by the World Bank’s Systematic Country Diagnostic (SCD), which observes that Djibouti achieved “impressive growth,” averaging 8% in 2013–2016, driven by public and private investments in port and transport infrastructure, while warning that this inward-investment strategy also triggered large public borrowing and debt-financed capital accumulation with sustainability concerns.

Two implications from these primary sources are central to interpreting the 1990–2024 period. First, the growth model has been services-heavy and capital-intensive. The World Bank SCD notes that the recent investment wave has generated a predominantly capital-intensive, services-based economy, with services accounting for close to 80% of GDP, and that growth has been limited in its inclusiveness, with high unemployment and persistent poverty. Second, macroeconomic vulnerability and fiscal space constraints have been recurring issues. The World Bank SCD documents the rapid rise in public and publicly guaranteed external debt during the investment boom and emphasises Djibouti’s exposure to external shocks given its dependence on Ethiopia-linked port activities; it notes that Ethiopia’s trade accounts for more than 80% of Djibouti’s port activities and that any adverse shock or strategic reorientation could jeopardise Djibouti’s ability to service its debt and sustain growth. These constraints matter because GDP growth, even when strong, does not automatically translate into broad-based jobs and incomes unless complementary reforms raise productivity, lower input costs (notably electricity) and improve the business environment.

The 2025–2043 acceleration to an average 6.1% annual GDP (MER) growth under the Current Path will therefore be a meaningful shift. It implies that the economy will sustain a growth pace close to doubling in size about every 12 years (rule-of-72 logic), which is much faster than the 1990–2024 pace (doubling roughly every 22 years). Interpreting this forecast requires linking it to the country’s stated policy direction and to the kinds of drivers emphasised in IMF and World Bank diagnostics. Djibouti’s long-term strategy explicitly targets high growth. Precisely, Vision 2035 sets an objective to raise average real GDP growth to 8–10% per year over 2013–2035, with growth expected to be enabled by increased port-related services and expansion of transport, commerce and industry, alongside diversification into sectors such as logistics, ICT, finance, tourism, fisheries and manufacturing.

Meanwhile, the Government’s SCAPE framework sets goals that demonstrate the same logic, accelerating growth, modernising the economy, increasing the role of the private sector, promoting employment and reducing social and territorial disparities. Read against these targets, the Current Path forecast of 6.1% average GDP (MER) growth per annum will be below the Vision 2035 target. However, it represents a robust acceleration in the medium- to long-run relative to the past three decades.

From an economic perspective, the IMF 2025 Article IV helps explain the types of drivers that can plausibly support such an acceleration, as well as the conditions required for sustainability. The report notes that Djibouti’s investment-focused strategy has propelled average growth of about 6% over the past decade, and notes that 2024 growth was about 6.5%, driven by robust transhipment amid Red Sea maritime disruptions, showing how Djibouti’s hub role can translate geopolitical shocks into short-run trade and service gains. At the same time, it emphasises that high public investment and rising debt service have constrained fiscal space and calls for reforms to boost private investment, diversify the economy and create jobs, highlighting actions such as leveling the playing field between firms under special and general regimes, lowering electricity costs, improving small and medium enterprises (SMEs) financing and strengthening education and job training (aligned with the national Vision 2035 strategy).

The same diagnostics also clarify the downside risks. Debt sustainability and corridor dependence are structural constraints, not marginal issues. The World Bank SCD explicitly frames debt-financed growth as raising sustainability concerns and highlights the vulnerability created by reliance on Ethiopia-linked port activity and exposure to shocks (including adverse climate events) that can reduce fiscal space and undermine growth. In practical terms, this means that the Current Path trajectory to 2043 should be interpreted as achievable only if (i) corridor and transshipment services remain strong, (ii) Djibouti progressively broadens its service export base and reduces input costs (notably power and ICT costs, which the SCD and IMF treat as competitiveness constraints) and (iii) fiscal consolidation and improved public investment efficiency prevent debt service from crowding out human capital and resilience investment. Climate risk is also a material macro risk driver for Djibouti, especially given water scarcity and exposure of critical infrastructure to extreme heat and episodic flooding, risks that can raise operating costs and disrupt transport and logistics activity.

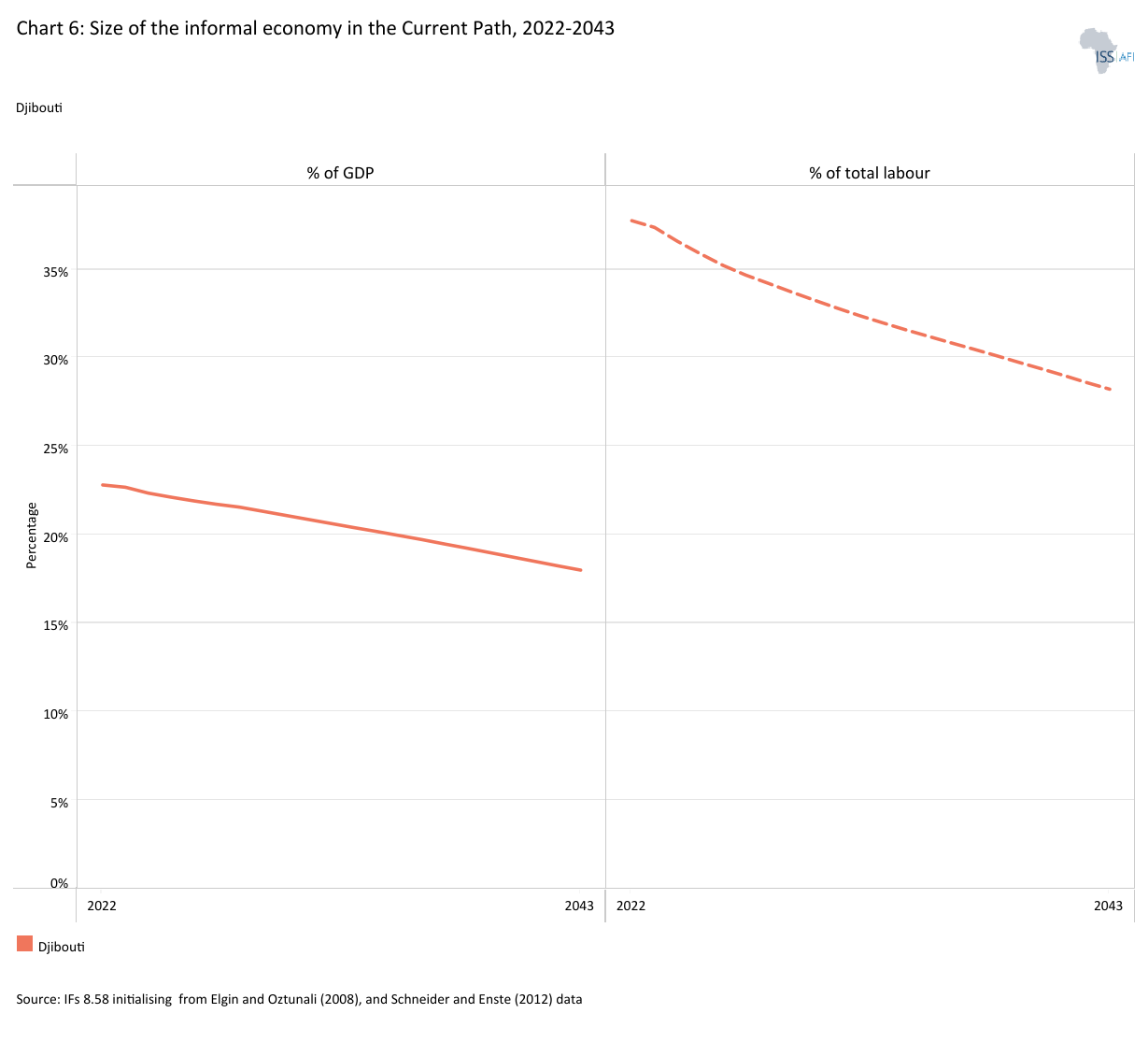

Chart 6 presents the size of the informal economy as a percentage of GDP and percentage of total labour (non-agriculture), from 2022 to 2043. The data in our modelling are largely estimates and therefore may differ from other sources.

Djibouti’s Current Path suggests a gradual but meaningful reduction in informality over the next two decades. Informality will already be lower than the African lower-middle-income (LMIC) average and will widen that gap by 2043. The informal economy's share of GDP will decline from 22.4% in 2024 to roughly 18% in 2043. Over the same period, the informal share of the non-agricultural labour force will decline from 36.6% to 28.2%. By comparison, the African LMIC average will decline from 30.3% to 26.3% of GDP and from 57% to 53% of the non-agricultural labour force. These trajectories imply that Djibouti’s Current Path will reduce informality at least as fast as the LMIC average in GDP terms, and substantially faster in labour-market terms, moving from one-third informal toward about one-quarter informal non-agricultural employment by 2043.

Before 2024, Djibouti’s informality is best understood as a structural feature of a services-led, urban economy in which highly capital-intensive logistics and port activity coexist with a large base of low-productivity urban services and trade. The World Bank’s SCD characterises Djibouti’s services dominance and notes that, outside the public sector, “most workers are engaged in low-value informal wholesale and retail trade,” and that a large share of the working-age population is unemployed, informally employed or out of the labour force. This diagnosis aligns with the classic informality dualism: a narrow modern sector (ports/State Owned Enterprises (SOEs)/public sector and some formal services) alongside a broad set of microenterprises and casual work in trade, transport, personal services and construction. Informality is therefore both a livelihood strategy and a sign of limited economic transformation, especially when it reflects survivalist self-employment rather than dynamic entrepreneurship.

Measurement and definition matter when interpreting any informality trajectory. The ILO distinguishes between the informal sector (enterprise-based) and informal employment (job-based) and provides the international statistical guidance used by many countries and datasets. The World Bank also emphasises that informality is measured using multiple approaches and has compiled a multi-method Informal Economy Database, reflecting how different estimation methods can yield different levels and trends. For this report, the critical interpretive task is not to claim a single true informal share but to explain what a declining trajectory implies for productivity, inclusion and fiscal space.

The Current Path decline in informality is consistent with Djibouti’s long-run policy intent to shift from a state-led, capital-accumulation model toward a more competitive, private-sector-driven economy with higher employment intensity. The Vision 2035 framework explicitly defines a pillar of “a diversified and competitive economy with the private sector as the engine,” alongside governance and human capital pillars that are essential for formal, productive job creation. SCAPE (2015–2019), positioned as a principal operational instrument of Vision 2035, targets large-scale job creation and emphasises private-sector-led economic growth, human capital development, strengthened governance and regional development poles. In this policy context, falling informality in the Current Path can be interpreted as the model’s assumption that a larger share of firms and jobs will become registered and regulated over time, particularly as infrastructure will improve, the business environment will reform, and formal services and value-adding activities will expand around the ports, free zones and corridor economy.

Economically, the payoff from reducing informality is substantial. Lower informality generally implies higher productivity (through better access to finance, technology adoption and scale), stronger worker protections and expanded participation in formal systems. The ILO frames transitions to formality as a core development challenge and highlights that policy packages for transition support sustainable development (SDG) progress and decent work. For the state, formalisation broadens the tax base and strengthens the contributory base for social protection, enabling more sustainable financing of service delivery and public investment. The IMF’s 2025 Article IV stresses that revenues are limited relative to spending needs and identifies priorities, including standardising tax regimes to broaden the tax base, narrowing exemptions and pursuing reforms that foster private-sector development and formal job creation, alongside energy-sector reforms and human capital investment. These recommendations are consistent with the Current Path, in which informality will decline as fiscal institutions improve, firms’ incentives to formalise strengthen, and the regulatory burden becomes more predictable.

Nonetheless, the persistence of informality, 18% of GDP and 28% of non-agricultural employment by 2043 under the Current Path, signals that structural constraints will remain. Djibouti’s corridor-dependent model is exposed to regional disruptions and geopolitical shocks that can move workers into informal coping strategies. Climate and water stress can also suppress productivity and raise the cost of formal operations, especially for small firms, reinforcing informality in low-margin activities. The Current Path improvement is therefore best read as gradual progress, not automatic transformation. To realise the forecast reductions, Djibouti must expand formal private-sector job creation faster than population growth and ensure that formalisation is not simply enforcement-driven but incentive-compatible (cheaper compliance, better services, better access to finance).

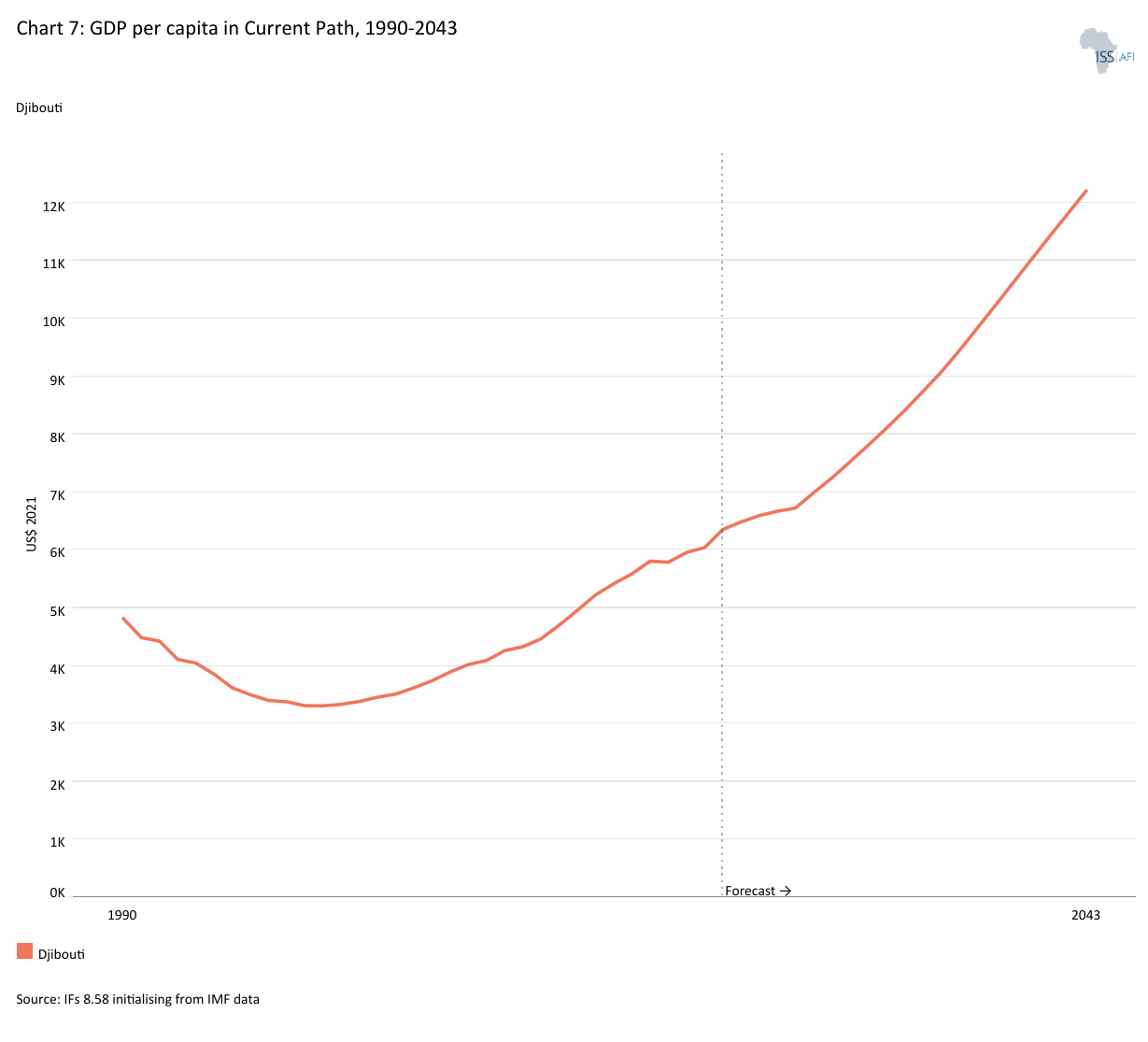

Chart 7 presents GDP per capita in the Current Path, from 1990 to 2043, compared with the average for the African income group.

Djibouti’s GDP per capita trajectory reflects three distinct phases: a sharp contraction in the 1990s, a strong recovery after 2000, and a forecast acceleration after 2024, with the country surpassing the African LMIC average around 2030/31. GDP per capita declined from about US$4 820 in 1990 to US$3 310 in 2000 before rising steadily to approximately US$6 840 in 2024. This recovery aligns with evidence from the World Bank’s SCD, which shows that average per capita GDP growth shifted from −4% in 1991–1999 to 2.6% during 2000–2014 and accelerated further to about 5.8% between 2015 and 2017, reflecting a broader structural turnaround after 2000. Under the Current Path, GDP per capita will nearly double to approximately US$12 220 by 2043, roughly US$2 600 above the African LMIC average forecast. However, the country is unlikely to achieve its Vision 2035 target of tripling GDP per capita by 2035.

The historical drivers of Djibouti’s post-2000 per-capita recovery are closely linked to services- and infrastructure-led growth stemming from its strategic location. The World Bank SCD notes that Djibouti's stable domestic political environment enabled it to leverage its strategic position to attract investors and highlights major investments, including port development and the electric railway connection to Ethiopia. As indicated in Chart 5, these investments helped fuel a predominantly capital-intensive, services-based economy. The same diagnostic emphasises that Ethiopia’s trade accounts for more than 80% of Djibouti’s port activities, clarifying both the scale of the opportunity and the vulnerability embedded in the corridor model. This structure helps explain why per-capita growth can be strong during periods of corridor expansion and transhipment booms, while also being exposed to external shocks and strategic competition from alternative routes.

Those vulnerabilities are central to interpreting the forecast period under the Current Path. The IMF’s 2025 Article IV notes that Djibouti’s “investment-focused strategy” has yielded average growth of about 6% over the past decade, and states that growth remained strong at about 6.5% in 2024, driven by “robust transhipment amid Red Sea maritime disruptions.” These dynamics, Djibouti capturing logistics and transhipment rents from regional disruptions, can temporarily lift GDP and, depending on inflation and population growth, can support higher GDP per capita. However, the report simultaneously warns that substantial public investment, declining revenues and rising debt service have constrained fiscal space and increased pressure on debt sustainability. The World Bank SCD echoes this risk, arguing that capital accumulation has been increasingly debt-financed and that debt service can constrain fiscal space and limit necessary spending in social sectors.

In short, the Current Path’s strong per-capita forecast to 2043 is consistent with ongoing expansion of services and corridor activity. Still, it is contingent on maintaining debt sustainability, strengthening institutions and improving the inclusiveness of growth.

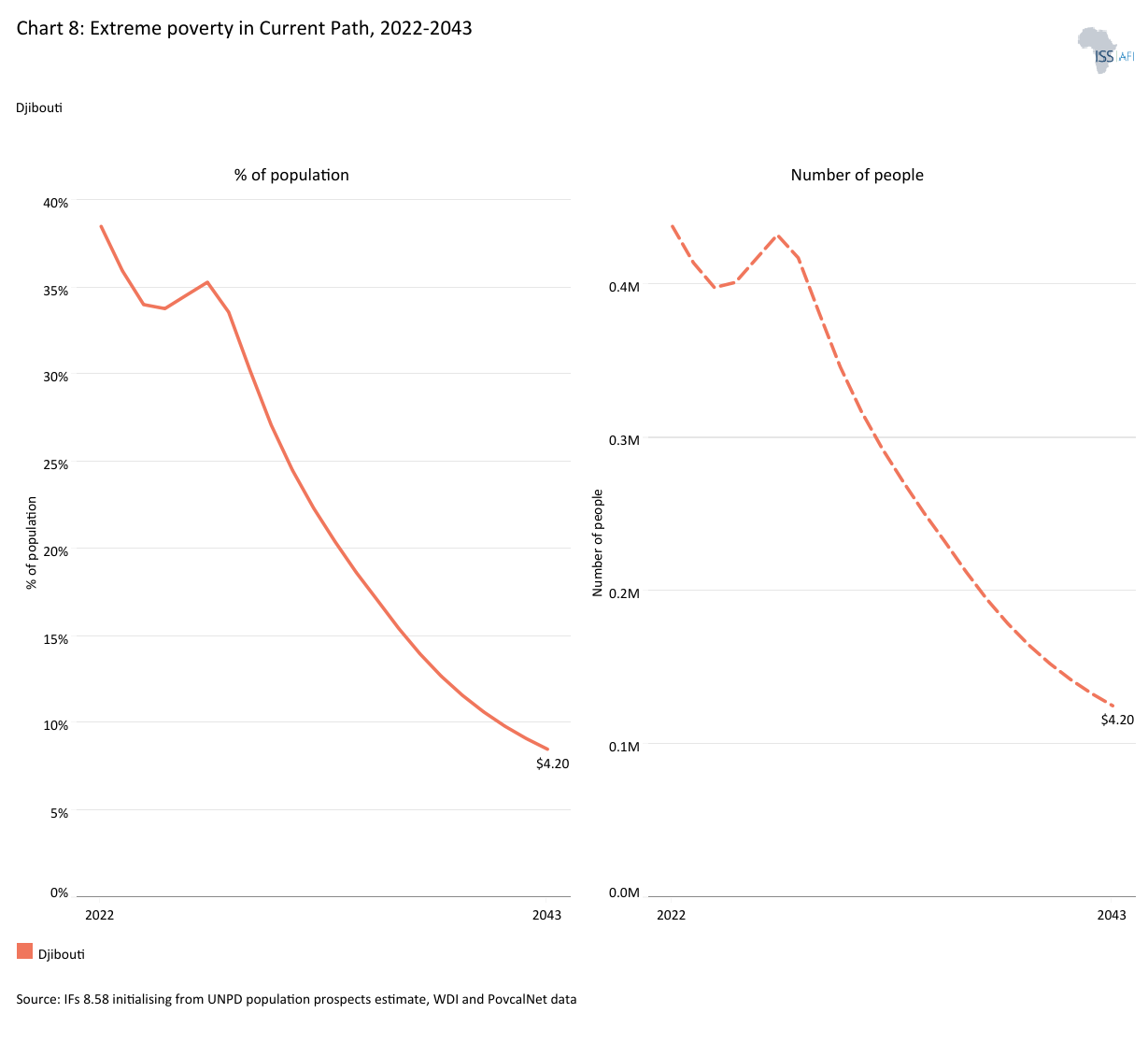

Chart 8 presents the rate and number of extremely poor people in the Current Path from 2022 to 2043.

In June 2025, the World Bank updated its poverty lines to 2021 PPP terms, now using US$3.00 per person for extreme poverty, US$4.20 for lower-middle-income countries (LMICs) such as Djibouti, and US$8.30 for upper-middle-income countries (UMICs).

Djibouti’s poverty reduction story before 2022 is best described as growth with weak inclusiveness, shaped by a services-led, infrastructure-heavy development model that generated sizable output gains but did not consistently translate into low poverty and broad employment. The World Bank’s SCD emphasises that, despite strong growth during the 2013–2016 investment boom, “growth has not been inclusive,” and notes that a 2017 national household survey found that 20.8% of the population lived in extreme poverty. At the same time, the extreme poverty rate measured at the older World Bank’s US$1.90 line stood at 22.5%, worse than the average poverty rate of 16.4% for LMICs. The same SCD links persistent poverty to structural constraints: capital-intensive growth dominated by capital accumulation with limited labour contribution, high unemployment and informality and a narrow base of private formal job creation. This aligns with Djibouti’s own planning narrative in SCAPE (2015–2019), which frames accelerated growth as necessary but explicitly pairs it with job creation, improved access to basic services, and a commitment to reducing poverty as part of the Vision 2035 trajectory.

Recent World Bank macro and poverty monitoring indicates that poverty has been declining but remains widespread. Precisely, the Djibouti Macro Poverty Outlook reports that the share living below US$3.00 per day fell from 25.4% to 20% between 2017 and 2024, while the US$4.20 per day poverty rate dropped from 43.7% to 35.4% over the same period, with further decline forecasted through 2027. The Current Path, likewise, indicates that the downward momentum in poverty will continue and accelerate. At the US$3.00 line, extreme poverty will drop to 3.1% (45 440 people) by 2043. At the US$4.20 line, the Current Path shows poverty declining to roughly 9% (125 120 people) at the same time, substantially outperforming the Africa LMIC average and placing Djibouti within the targets of its National Development Plan (NDP) 2020–2024 (Djibouti ICI) to cut poverty by 28% in 2025. The headcount will fall by approximately 171 040 people and 272 630 people between 2004 and 2043, respectively.

This scale of poverty reduction (both at US$3.00 and US$4.20 lines) is consistent with an economy that continues expanding in high-value services (ports, logistics) while gradually improving access to basic services and human capital, drivers emphasised in official strategies (SCAPE/Vision 2035) and in partner diagnostics as necessary for inclusive outcomes. The IMF’s 2025 Article IV similarly acknowledges that Djibouti’s investment-focused strategy has produced robust growth, but stresses that rising debt service and constrained fiscal space increase the need for reforms that support private investment, job creation and sustained human capital spending. In poverty terms, the Current Path’s sharp decline at US$4.20 implies that growth is assumed to translate more effectively into household incomes than in the pre-2022 period, through some combination of (a) expanding employment and earnings in services linked to ports and logistics and ancillary urban services, (b) reduced informality and improved productivity that raise earnings per worker and (c) stronger social protection and service delivery that prevents households from falling into poverty during shocks.

The main risks to this poverty trajectory mirror Djibouti’s structural vulnerabilities. First, corridor dependence and regional instability can rapidly affect service revenues and employment. Second, climate and water stress can raise food and living costs, especially in dense urban areas, slowing poverty reduction or reversing gains during shocks. Third, macro-fiscal constraints can limit the state’s capacity to expand targeted transfers and human capital spending at the pace implied by these forecasts.

Chart 9 depicts the National Development Plan (NDP).

Djibouti’s national planning hierarchy is anchored in Vision Djibouti 2035, a long-term national vision intended to guide development toward “a desired future” by 2035. Vision 2035 is organised around five pillars. (1) Peace and National Unity, (2) Good Governance, (3) A diversified and competitive economy driven by the private sector, (4) Consolidation of Human Capital and (5) Regional Integration, explicitly linking national cohesion, institutional performance and economic transformation to inclusive development and international integration. Implementation is designed through five-year planning cycles: the Government describes SCAPE (2015–2019) as the first operational version of Vision 2035, implemented in these five-year cycles. SCAPE and Vision 2035 define a high-ambition development trajectory, tripling per capita income, creating more than 200 000 jobs, reducing unemployment to roughly 10% by 2035, reducing absolute poverty by more than one-third and achieving universal access to energy, water and basic services, providing a clear target framework for the Current Path and scenario interpretation in the rest of this report.

The second major operational plan is the National Development Plan (NDP) 2020–2024, “Djibouti ICI”, explicitly presented as consolidating SCAPE achievements and the COVID-era National Solidarity Pact, and developed within the Vision 2035 framework. Djibouti ICI is structured around three strategic axes, inclusion, connectivity and institutions, reinforced by intersecting themes including human capital development, environment and climate change and renewable energy. It also explicitly situates national planning within continental and global agendas, stating that it encompasses Djibouti’s international commitments, including the AU Agenda 2063 and the UN 2030 Agenda. Djibouti ICI includes explicit distributional targets and social objectives, for example, a stated target to reduce poverty by 28% and reduce the Gini index from 0.42 to 0.35 in 2025, while expanding access to schooling, basic health services and energy, water and sanitation. It also signals an intent to mobilise external resources (including Aid and diaspora engagement) and explicitly notes that measures to mobilise the diaspora would increase remittances.

The feasibility of this planning architecture hinges on three binding trade-offs repeatedly highlighted by development partners. First, the growth model has been investment-heavy and corridor-dependent. Second, fiscal space is constrained by the interaction of development needs and debt service. Third, environmental constraints increase delivery costs. These trade-offs shape how the report maps plan targets to the Current Path, sectoral scenarios and the Combined scenario forecasts.

The Technical Page explains the eight sectoral scenarios and their relationship to the Current Path and the Combined scenario. Chart 10 summarises the approach.

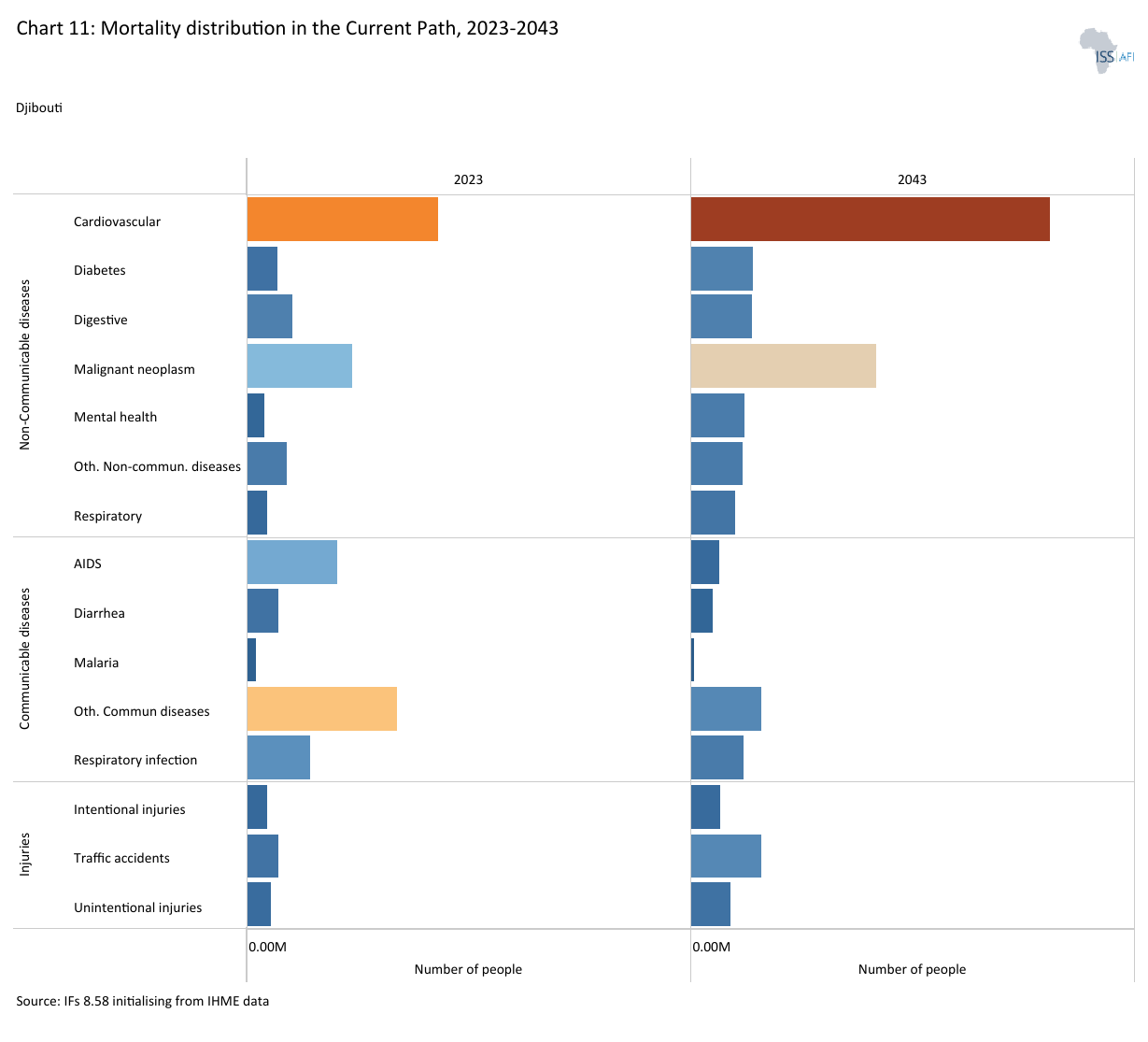

Chart 11 presents the mortality distribution in the Current Path for 2024 and 2043.

The Demographics and Health scenario envisions ambitious improvements in child and maternal mortality rates, enhanced access to modern contraception, and decreased mortality from communicable diseases (e.g., AIDS, diarrhoea, malaria, respiratory infections) and non-communicable diseases (e.g., diabetes), alongside advancements in safe water access and sanitation. This scenario assumes a swift demographic transition supported by heightened investments in health and water, sanitation, and hygiene (WaSH) infrastructure.

Visit the themes on Demographics and Health/WaSH for more details on the scenario structure and interventions.

Djibouti’s Current Path mortality distribution indicates that the country is now firmly in a double-burden phase of its epidemiological transition, where non-communicable diseases (NCDs) rise rapidly while communicable diseases continue to decline and injuries remain a persistent risk. WHO’s DataDot country profile for Djibouti shows that by 2021, an estimated 47% of deaths were from NCDs, 42% from communicable conditions and 9% from injuries, suggesting that Djibouti was at (or very near to) the point where NCD mortality became the largest share.

Under the Current Path, NCD mortality will become the dominant and fastest-growing pressure on the health system over the next two decades. Deaths from NCDs will rise from about 4 060 in 2024 to 7 110 by 2043, an increase of 3 050 deaths. Over the same period, deaths from communicable diseases will fall from about 2 910 to 1 530, a decline of 1 380 deaths. This is the classic signature of an epidemiological transition: as fertility declines and the population ages (as shown in Chart 2), chronic conditions become a larger share of avoidable mortality, while infectious disease burdens retreat but do not disappear.

Regarding mortality distribution, in 2024, the largest single cause was cardiovascular disease (approximately 1 700 deaths), followed by other communicable diseases (approximately 1 260), malignant neoplasms (approximately 950), AIDS (approximately 750) and respiratory infections (approximately 550). By 2043, the ranking will change further toward NCD dominance: cardiovascular deaths will rise to approximately 3 110 and malignant neoplasms will rise to roughly 1 610. At the same time, other communicable diseases will decline but remain material at about 622 deaths, indicating a persisting infectious burden even as the country transitions. AIDS and respiratory infections will become less threatening from the 2030s, while digestive diseases, diabetes and traffic accidents increase into the top-five causes.

The World Bank emphasises that NCDs pose a growing threat to health and development in LMICs, driven by ageing populations, urbanisation and lifestyle change, and that many countries face a double burden with unfinished communicable disease challenges alongside rising NCDs. For Djibouti, the growth in cardiovascular disease, cancers and diabetes implies greater demand for long-term, continuous care (hypertension screening, chronic medication, oncology pathways and dialysis and complication management) rather than episodic acute care. That raises recurrent operating costs for the health system and increases the risk of catastrophic household spending if service coverage is incomplete, particularly among poorer urban households and vulnerable groups. Policy guidance from the World Bank highlights that effective NCD response often requires a greater focus on publicly financed, primary-health-care-based services, underscoring the need to strengthen primary health care (PHC) platforms rather than relying only on hospitals.

At the same time, the decline in AIDS and respiratory infections in the Current Path implies continued gains from prevention, treatment and public health programs. Djibouti’s development partners nonetheless flag institutional constraints. A UNFPA/UNDP country program draft notes that the Ministry of Health has a National Health Development Plan (NHDP) 2020–2024 and a strategy to accelerate maternal and newborn mortality reduction, but that decentralisation, coordination and accountability remain key challenges, alongside limited high-functioning facilities and large urban–rural disparities in service coverage. These governance and capacity constraints matter because NCD care requires reliable follow-up systems, supply chains for essential medicines and consistent quality across districts.

Finally, the emergence of traffic accidents as a rising top-five threat by the 2030s will economically be important because road injuries disproportionately affect working-age adults, directly reducing labour productivity and raising health costs. Globally, the UN system frames road safety as a development priority, with commitments to reduce road traffic deaths by at least 50% by 2030 under the Decade of Action for Road Safety 2021–2030. If injuries will rise while NCDs accelerate, Djibouti risks a triple pressure on the health system: chronic disease management, still-meaningful infectious disease control and injury care, each with distinct infrastructure and workforce needs.

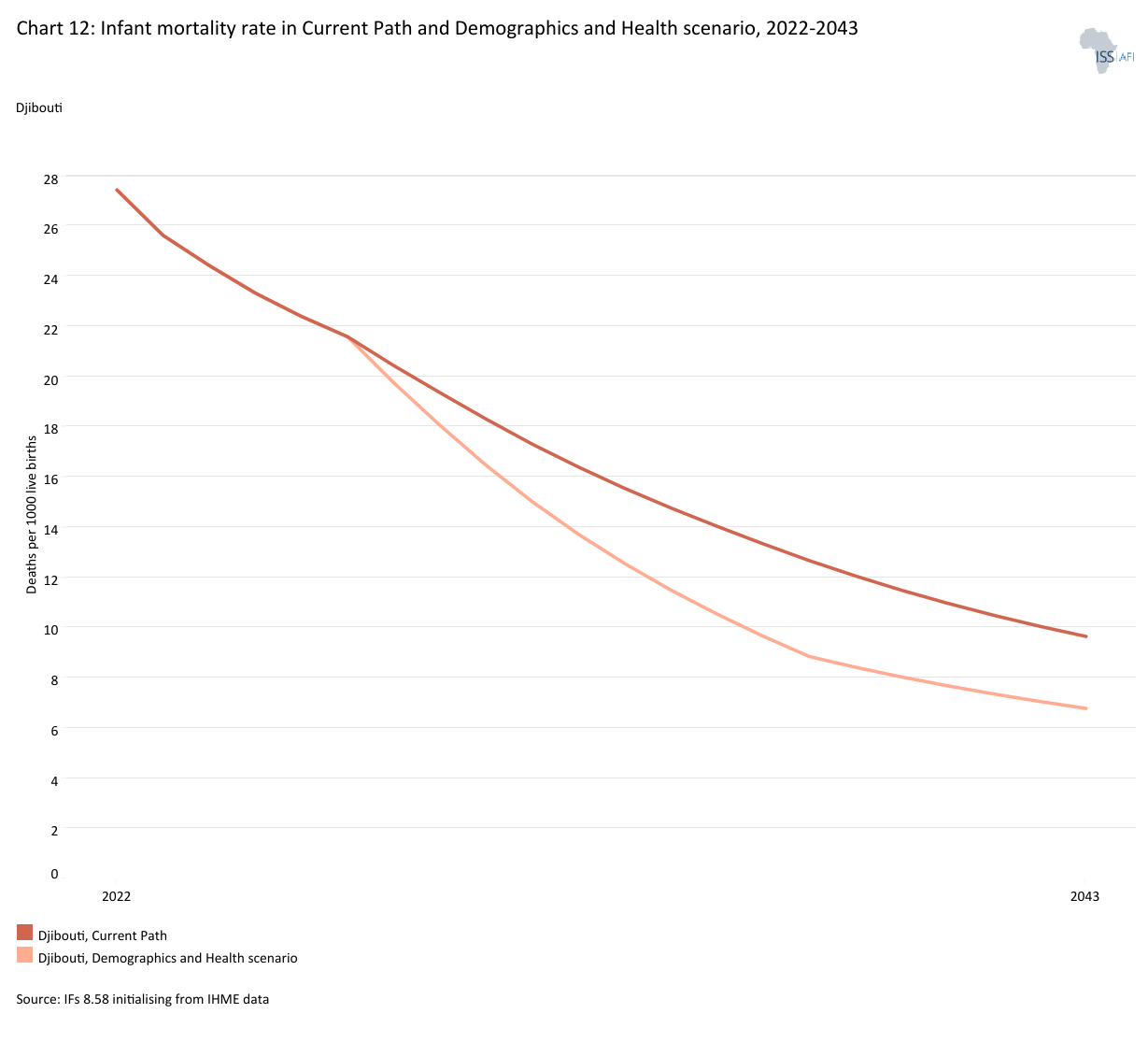

Chart 12 presents the infant mortality rate in the Current Path and the Demographics and Health scenario, from 2022 to 2043.

Infant mortality, defined as deaths between birth and 365 days per 1 000 live births, is a crucial indicator of maternal health, newborn care quality, nutrition, immunisation and water and sanitation conditions. Chart 12 should therefore be read as both a health-system performance signal and an inclusion signal. Historically, Djibouti has reduced infant mortality substantially since 1990, but entered the 2020s with a level still consistent with major preventable causes of newborn and early-childhood deaths. UN IGME’s Levels & Trends in Child Mortality statistical table reports that Djibouti’s infant mortality rate fell from 91 per 1 000 in 1990 to 44 per 1 000 in 2022. This long decline reflects progress in child survival. Still, the remaining burden points to persistent constraints in neonatal care, limited access to quality care outside the capital and vulnerability to shocks (drought, floods) that affect nutrition and service delivery, issues also flagged in recent UN program diagnostics that highlight institutional and service coverage gaps, particularly across the urban–rural divide.

The Current Path and the Demographics and Health scenario forecasts imply that Djibouti would achieve exceptionally rapid gains in child survival over the next two decades, well beyond the pace of other African LMICs. Under the Current Path, the infant mortality rate (IMR) will decline from 24.4 in 2024 to 9.6 per 1 000 live births by 2043. Under the Demographics and Health scenario, IMR will fall further to 6.8 per 1 000 by 2043, which is about 2.8 fewer infant deaths per 1 000 live births than the Current Path in 2043.

Globally, SDG 3.2 commits countries to ending preventable deaths of newborns and children under five, with benchmarks of neonatal mortality ≤12 and under-5 mortality ≤25 per 1 000 live births by 2030. Achieving such targets typically requires stronger antenatal care, skilled birth attendance, emergency obstetric and newborn care, postnatal follow-up and effective community health systems. In Djibouti, how these inputs are organised is shaped by constraints on health system capacity and equity. As indicated in the previous section, the Ministry of Health has an NHDP (2020–2024) and a strategy to accelerate reductions in maternal and newborn mortality, but UNFPA highlights persistent institutional constraints, including coordination and accountability as well as notable urban–rural disparities in service coverage. The Demographics and Health scenario assumes effective interventions to address these constraints, thereby achieving the SDG3.2 targets in the early 2030s, rather than in the later 2030s under the Current Path.

The economic and fiscal implications of achieving and sustaining reductions under the Demographics and Health scenario are substantial. Lower infant mortality improves human capital accumulation and long-run productivity (by enabling more surviving children to reach school age and adulthood). Still, it also requires reliable recurrent spending, especially for frontline services, supply chains for essential medicines and WaSH investments. UNICEF’s operations in Djibouti illustrate the continued importance of combined health–nutrition–WASH responses (under the Demographic and Health scenario) during shocks; for example, UNICEF programming priorities include access to safe water and nutrition assistance for children in affected areas, reflecting how drought and vulnerability intersect with child health outcomes.

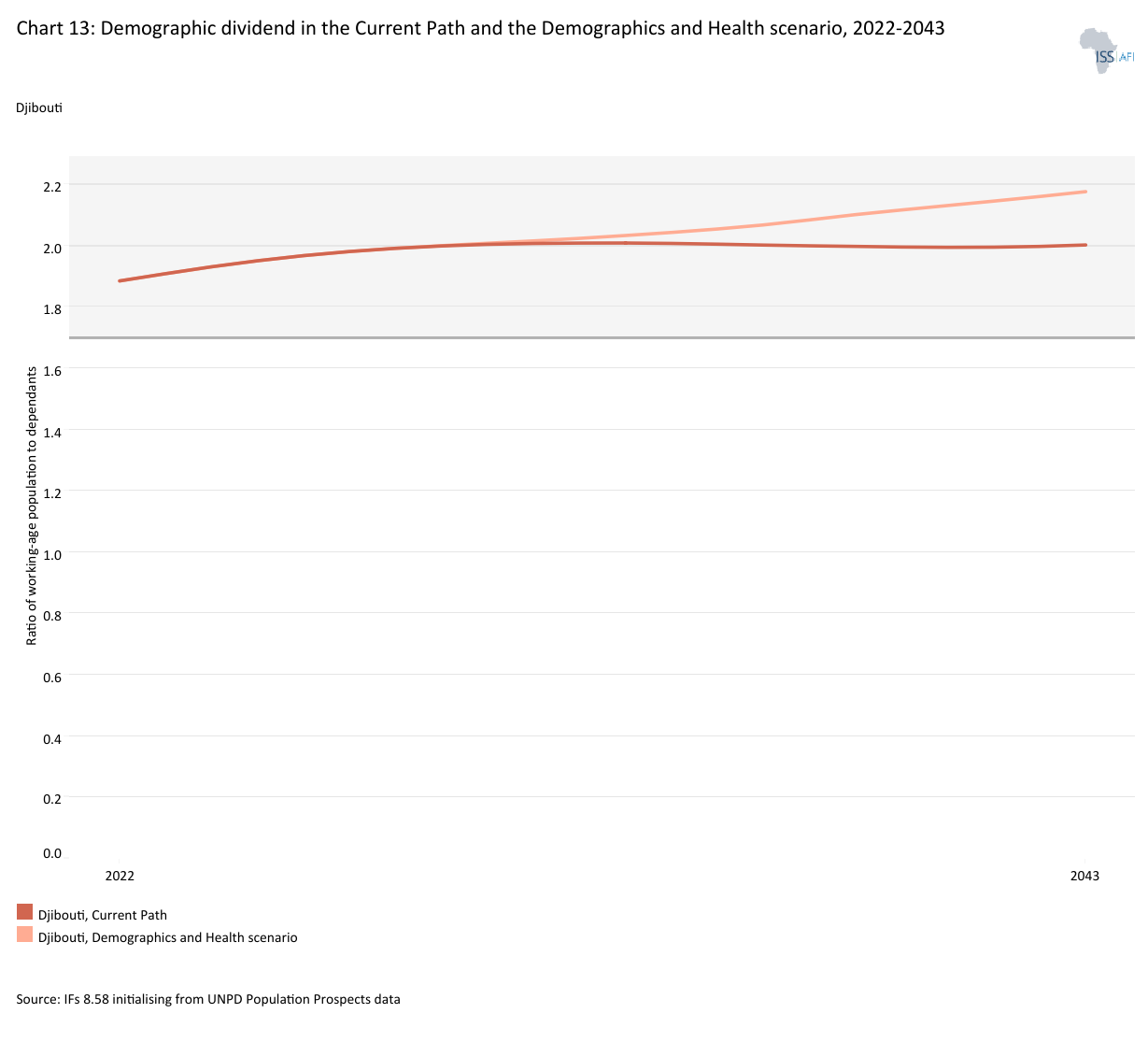

Chart 13 presents the demographic dividend in the Current Path and in the Demographics and Health scenario, from 2020 to 2043.

UNFPA defines the demographic dividend as economic growth potential arising mainly when the share of the working-age population exceeds the non-working-age or dependants’ share (under 15 and 65+). This window emerges when the ratio of working-age individuals to dependants rises to about 1.7 to 1 or higher. The World Bank’s demographic dividend operational guidance emphasises that it is typically a 20–30 year period driven by fertility decline and age-structure change and that capturing it requires timely policies and investments, especially in health, education, governance and the economy, to ensure the bulge cohort finds well-paying jobs rather than unemployment or low-productivity work. Djibouti’s age structure, as depicted in Chart 2, is consistent with the conditions for a demographic dividend, but the economic payoff hinges on the country’s ability to translate that labour supply into productivity and earnings.

Djibouti crossed the demographic dividend threshold in 2018, and the ratio has since increased to roughly 1.9 in 2024. Under the Current Path, it will rise further to about 2 by 2043. In the Demographics and Health scenario, the ratio will increase more rapidly, reaching nearly 2.2 over the same period, suggesting a stronger potential boost to economic growth if supported by appropriate employment, education and health policies.

The most immediate implication is the scale of labour-market absorption required. If the working-age population rises from about 791 000 in 2024 to about 1 004 000 by 2043, Djibouti must create productive opportunities for a net increase on the order of approximately 213 000 additional working-age residents over two decades, through formal wage jobs, viable self-employment and productivity gains that raise incomes per worker. Today’s labour-market conditions sharpen this challenge: The World Bank modelled ILO estimates place total unemployment at 26% in 2025 and youth unemployment (ages 15–24) at 76.8% in the same year. If these conditions persist under the Current Path, the demographic window will not translate fully into faster per-capita growth; instead, it can manifest as higher pressure on public employment, household coping strategies and low-productivity informal work, exactly the risk highlighted by the World Bank’s demographic dividend guidance if job creation lags.

Human capital is a second binding condition for realising the dividend. The World Bank’s Djibouti Human Capital Review states that, based on a Human Capital Index (HCI) simulation, a child born in Djibouti in 2022 would achieve only 41% (HCI of 0.41) of full human capital potential by age 18, leaving 59% of potential untapped, an explicit productivity constraint. In a population structure where two-thirds of citizens are of working age, low learning outcomes, health burdens and limited skills formation directly reduce the return from favourable demography. Accordingly, human capital improvements are not just social goals, but fundamental economic requirements for converting a large working-age cohort into higher output and wages.

Female labour force participation is a third decisive lever. The World Bank’s demographic dividend note links stalled demographic transition to “lower levels of women entering the labour market” and weaker women’s empowerment, alongside higher youth unemployment and instability risks. In Djibouti’s context, raising women’s participation is not merely an equity agenda; it is a mechanism to expand the effective labour supply, increase household incomes and raise savings and investment, but only if labour demand expands and constraints (safety, childcare, skills, norms) are addressed. The demographic structure can therefore amplify the payoff from gender-inclusive growth strategies, especially those that increase women’s access to higher-productivity sectors (services, ICT, logistics administration and formal SMEs).

The World Bank demographic dividend framework emphasises a potential second dividend later in the transition, driven by the savings and investment behaviour of the bulge cohort as it ages. Capturing that second dividend typically requires financial deepening and credible long-term policy (pensions, savings vehicles, stable macro-fiscal conditions). Without such preparation, ageing can instead raise fiscal stress.

Djibouti’s national development plans directly frame the demographic transition as an opportunity that must be matched by economic transformation. Vision 2035’s overarching aim is to position the country as a hub for the regional and continental economy, and it emphasises a “diversified and competitive economy, driven by the private sector,” with growth anchored in port-linked services, transport, industry and ICT. It also includes a pillar on “Consolidation of Human Capital,” explicitly linking well-being and development to needs in health, education and training, jobs and the promotion of women and young people. The SCAPE reflects this same logic: it sets explicit objectives to accelerate growth, modernise the economy, assert the role of the private sector, promote employment and reduce social and territorial disparities. In other words, Djibouti’s planning architecture is aligned with the conditions the demographic dividend literature identifies as essential: jobs, human capital and institutional capability.

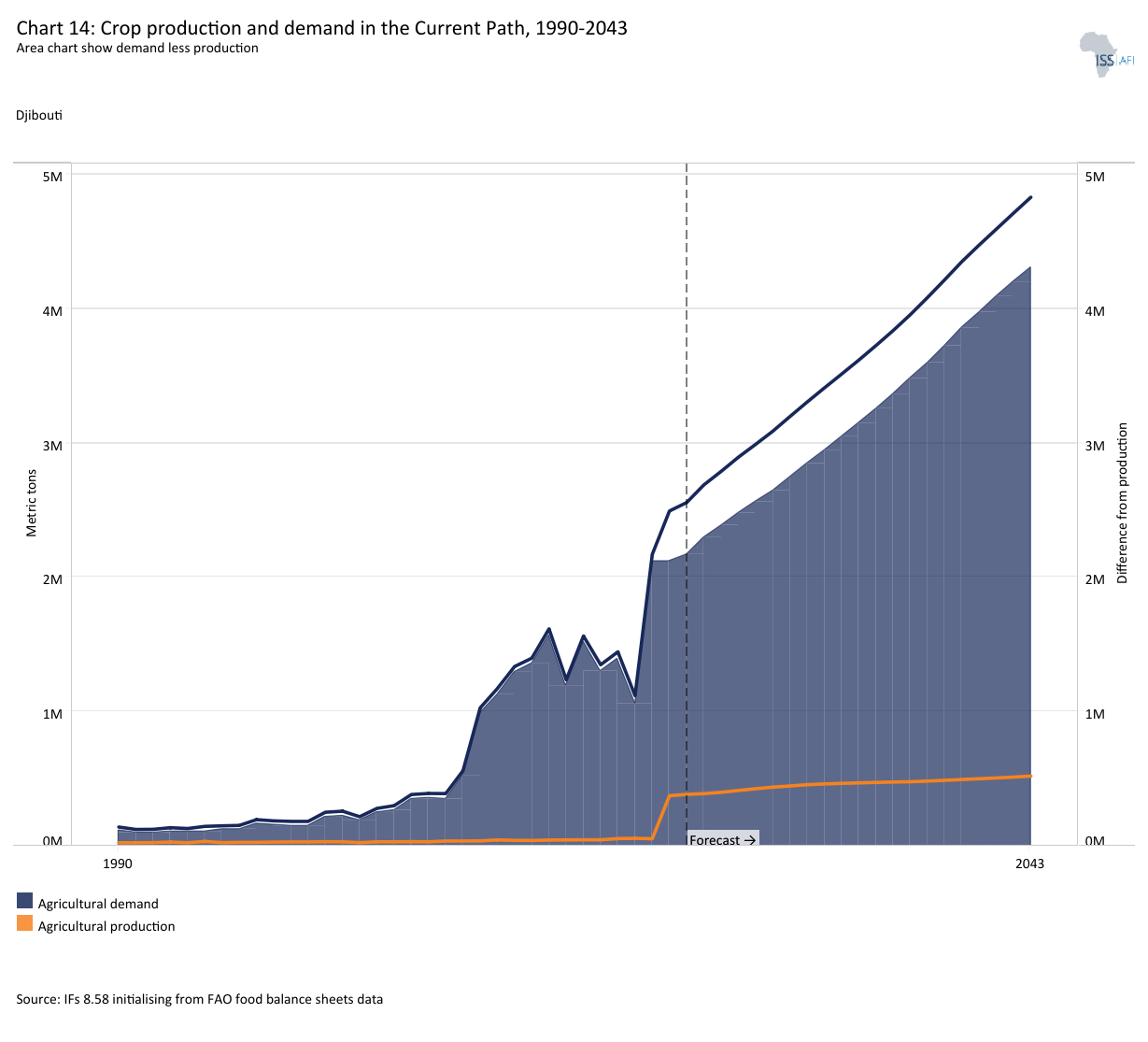

Chart 14 presents crop production and demand in the Current Path from 1990 to 2043.

The Agriculture scenario envisions an agricultural revolution that ensures food security through ambitious yet feasible increases in yields per hectare, driven by improved management, seed and fertiliser technologies, and expanded irrigation. Efforts to reduce food loss and waste are emphasised, with increased calorie consumption as an indicator of self-sufficiency and prioritising it over food exports. Additionally, enhanced forest protection demonstrates a commitment to sustainable land-use practices.

Visit the theme on Agriculture for our conceptualisation and details on the scenario structure and interventions.

Djibouti’s agricultural sector remains structurally constrained, reflecting the country’s arid climate, limited arable land and acute water scarcity. Of the roughly 1 010 hectares equipped for irrigation, only about 38.6% (approximately 390 hectares) were actually irrigated in 2024, pointing to significant underutilisation of existing infrastructure. Under the Current Path, the area effectively irrigated is forecasted to decline slightly to around 360 hectares by 2043, suggesting persistent constraints in water access, maintenance and agricultural investment.

Productivity challenges further underscore the sector’s limitations. Average crop yields have remained relatively stagnant at around 17 metric tons per hectare from the early 1990s to 2024, well below the country’s historical potential. Between 1980 and 1990, Djibouti achieved a notable 47.1% increase in yields, from 18.7 to 27.5 metric tons per hectare, indicating that improvements are possible under favourable conditions. The subsequent stagnation reflects structural bottlenecks, including limited irrigation, low input use and weak extension services.

Water scarcity remains the binding constraint. Djibouti’s desert environment and highly variable rainfall severely limit agricultural expansion and productivity. In response, the government and its partners have prioritised water infrastructure and climate-resilient agriculture. Key initiatives include the Saday dam, which enhances water storage capacity for irrigation and livestock, and the Ethiopia–Djibouti water pipeline, designed to improve water supply to urban and peri-urban areas while easing pressure on scarce groundwater resources. At the regional level, the Intergovernmental Authority on Development (IGAD) strategy on drought resilience and sustainable water management promotes more efficient water use and climate-smart irrigation practices. Recently, the World Bank approved a US$35 million grant to the Government of Djibouti to expand access to safe, reliable water resources for rural communities.

Additional climate adaptation efforts enshrined in the IGAD climate adaptation strategy (2023-2030), such as investments in desalination, groundwater development and agricultural mechanisation, are aimed at improving water availability and raising productivity. These interventions are expected to support moderate gains in agricultural output. Under the Current Path, crop production will increase from about 390 860 metric tons in 2024 to approximately 520 000 metric tons by 2043. Despite this progress, Djibouti will continue to face a substantial and widening food production deficit. Agricultural demand will rise sharply from 2.69 million metric tons in 2024 to 4.83 million metric tons by 2043, far outpacing domestic production.

These trends highlight the structural limits of domestic agriculture in ensuring food security. While investments in irrigation, water infrastructure and climate-smart agriculture are essential to maximise local production, Djibouti will remain heavily reliant on food imports. Strengthening trade logistics, regional food supply chains and strategic food reserves, alongside targeted support for niche, high-value or water-efficient crops, will therefore be critical to ensuring food security in a context of growing demand and environmental constraints.

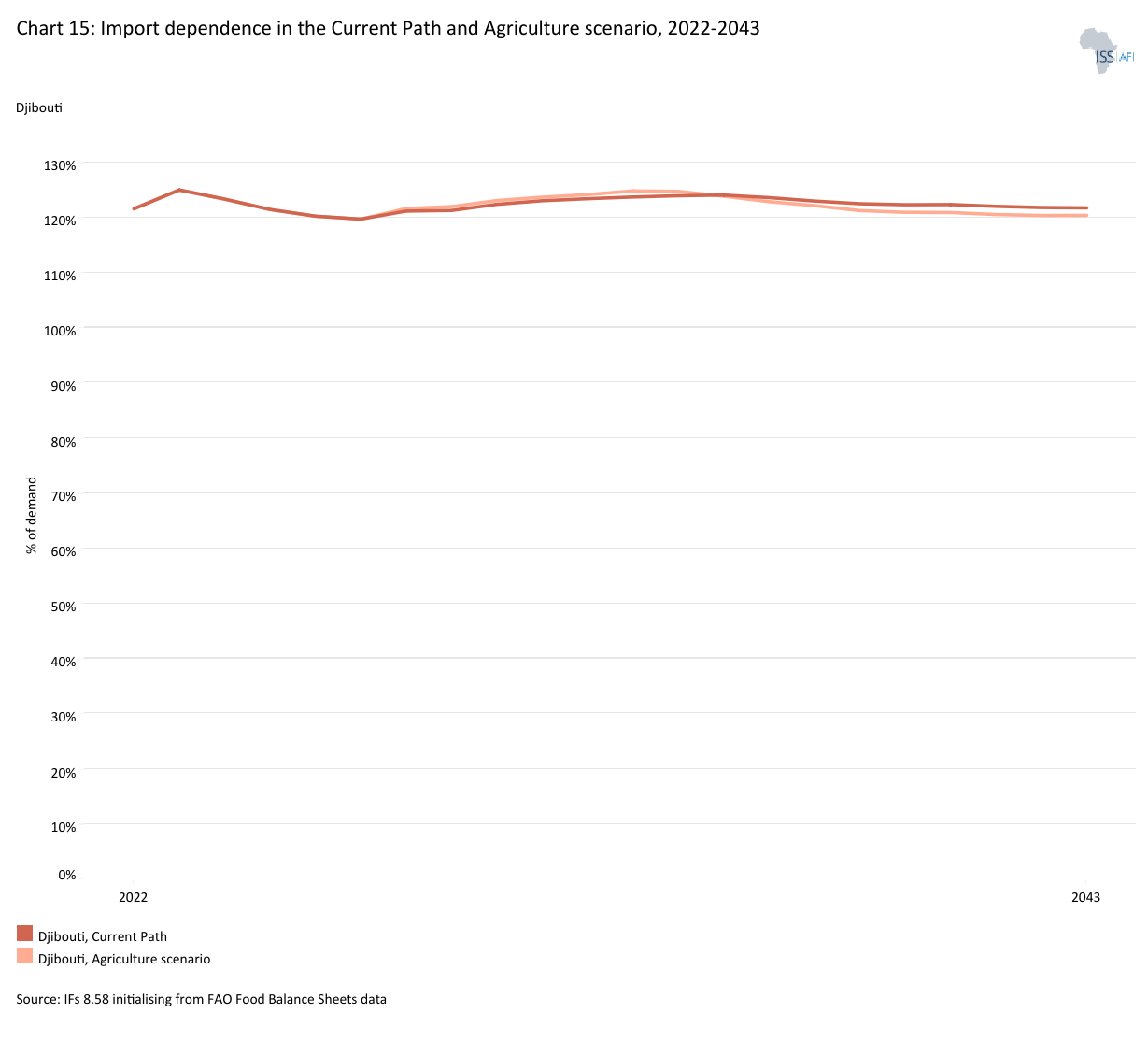

Chart 15 presents the import dependence in the Current Path and the Agriculture scenario, from 2022 to 2043.

In the Agriculture scenario, Djibouti’s agricultural performance will improve significantly relative to the Current Path, although structural constraints remain. Crop production will increase to approximately 750 000 metric tons by 2043, about 230 000 metric tons higher than the Current Path forecast. At the same time, total demand will rise slowly relative to the Current Path, reaching 4.7 million metric tons, around 130 000 metric tons below the baseline forecast. As a result, the agricultural trade deficit will narrow from 11.8% of GDP in 2024 to 7.1% by 2043, compared to 7.2% under the Current Path.

These gains are underpinned by improved water management, increased investment in irrigation and the adoption of climate-smart agricultural practices. Ongoing and planned initiatives, such as expanding water infrastructure through projects like the Saday dam and the Ethiopia–Djibouti water pipeline, are expected to play a central role in enhancing water availability for agriculture. In parallel, regional frameworks such as the IGAD Drought Disaster Resilience and Sustainability Initiative (IDDRSI) promote efficient water use, rangeland management and climate-resilient farming systems across the Horn of Africa, directly supporting Djibouti’s agricultural adaptation efforts.

Further improvements are likely to come from policies aimed at strengthening agricultural productivity and value chains. Government strategies emphasise irrigation expansion, greenhouse farming, hydroponics and the use of drought-resistant crops, which are better suited to Djibouti’s arid conditions. Investments in agricultural mechanisation, extension services and access to inputs are also critical for raising yields, reversing historical stagnation and improving the utilisation of existing irrigable land. In addition, donor-supported programs, particularly the World Bank’s Agri-Food Value Chain Development Project, IFAD’s water and climate resilience initiatives and FAO-led agrifood system interventions, have focused on strengthening value chains, expanding rural infrastructure and building institutional capacity. These programs reflect a shift from subsistence support to market-oriented, climate-resilient agriculture, with a strong emphasis on water management, private-sector participation, and livelihood diversification.

On the demand side, the modest reduction relative to the Current Path reflects efficiency improvements, reduced post-harvest losses and gradual dietary shifts supported by better market functioning and food systems management. This is in line with the Malabo Declaration commitment to halve post-harvest losses by farming practices, storage and rural roads to reduce wastage.

The Agriculture scenario demonstrates that while Djibouti cannot eliminate its dependence on food imports, it can meaningfully reduce its vulnerability. Achieving these gains will require scaling up investment in water-efficient technologies, strengthening the link between infrastructure and on-farm productivity and prioritising high-value, low-water-intensity crops. At the same time, integrating domestic production with efficient import systems and regional trade will remain essential to ensuring long-term food security in a resource-constrained environment.

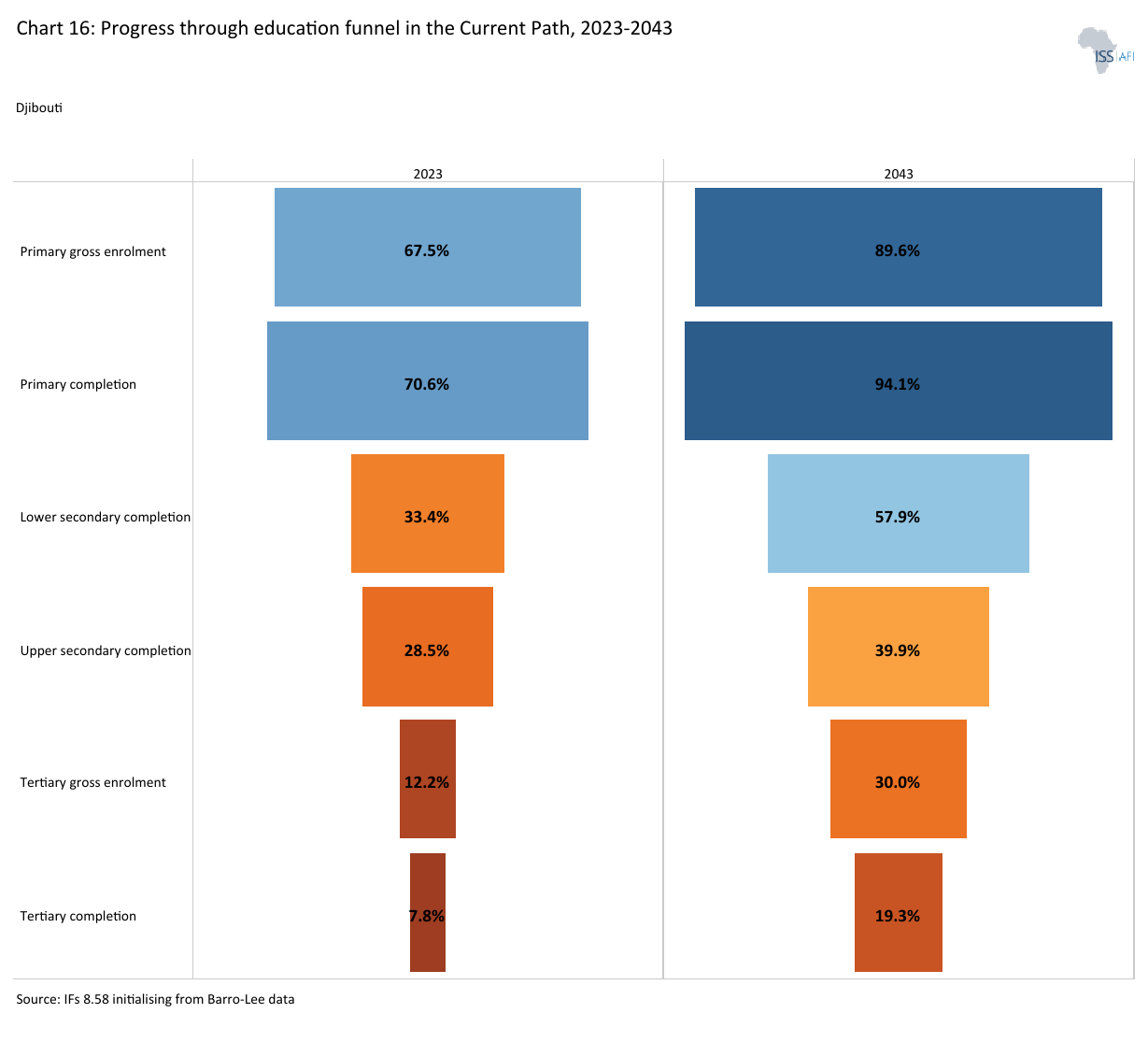

Chart 16 depicts the progress through the educational system in the Current Path, for 2024 and 2043.

The Education scenario represents reasonable but ambitious improvements in intake, transition and graduation rates from primary to tertiary levels, and in the quality of education at primary and secondary levels. It also models substantive progress towards gender parity at all levels, additional vocational training at the secondary school level, and increases in the share of science and engineering graduates.

Visit the theme on Education for our conceptualisation and details on the scenario structure and interventions.

In the Current Path, Djibouti will make significant gains in primary enrolment and completion. Still, the system will remain constrained by (i) incomplete universal access at primary, (ii) transition bottlenecks at lower and upper-secondary education that do not return to historical peaks, (iii) stagnant vocational enrolment in lower secondary and persistent gender gaps in TVET at upper secondary, and (iv) a declining science-and-engineering share among tertiary graduates, even as tertiary enrolment expands. This matters economically because Djibouti’s long-term strategy is to become a regional services and logistics hub, which will require a larger and more skilled workforce than the current education pipeline can deliver. Vision 2035 explicitly frames national transformation around a diversified, competitive, private-sector-driven economy and consolidation of human capital, linking education and skills formation directly to the development model.